SFM - Costco's Growth Will Persist Even If The U.S. Enters A Recession

2023-12-31 03:41:09 ET

Summary

- Costco had a strong Q1'24 with membership growth and revenue growth across all segments.

- The company plans to open 33 new warehouses in FY24, which is expected to drive further growth.

- Costco's margins are expected to widen, and with gasoline prices relieving some pressure, the company is set up for a strong FY24.

Costco (COST) experienced an exceptionally strong q1’24 in revenue across all segments and membership growth. With margins widening towards FY21 levels, the big question is whether Costco will be able to maintain this level of growth and profitability. With an anticipated 33 new warehouses opening in 2024, strong 90.50% global renewal rates, and gasoline prices relieving some of the pressure on gross margins, Costco should be set up for a strong FY24. I provide COST shares a BUY recommendation with a price target of $733.17/share.

Operations

Management is anticipating adding 33 new locations throughout FY24. Comparable same-store-sales have continued to increase on an annual basis, with new store sales outpacing new stores from previous years at $151mm/warehouse in 2023.

With new locations comes new card members. Though some newer locations can be cannibalizing to their current market, the convenience of adding new locations within a similar region can open Costco to more frequent, everyday shopping trips, allowing the firm to increase overall sales across foods and sundries, fresh foods, and ancillary items such as gasoline.

{kind=link}

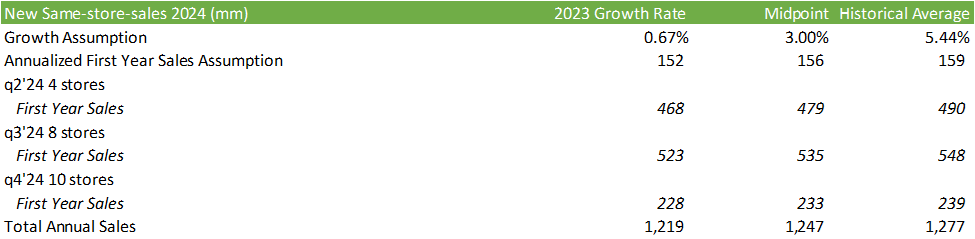

Management discerned on their q1’24 earnings call that ~160 warehouses brought in $300-400mm, ~25 warehouses brought in over $400mm, and a few over $600mm. Applying these growth trends to the 33 new stores set to open in 2024, we can expect a certain amount of growth resulting from these new locations. Net of 2018’s new store sales growth, the geometric mean for new store sales growth is 5.44%. Assuming that growth rate, new stores should bring in $159mm in first-year sales. Spread across the 33 new warehouses, the 2024 cohort of new warehouses should generate an aggregate of $5,254mm in sales in their first year of operations. Costco has already opened 9 new stores in q1’24 with 22 new warehouses to meet management’s FY24 guidance. Given the historical trend of store openings occurring in q1 & q4, we can anticipate a similar trend going into 2024.

{kind=link}

The figures above account for the timing of the store openings as it pertains to the annualized revenue generation assumptions at the top of the chart. Below is the historical chart for reference. I used the geometric mean, net of the negative growth year, to discern the average growth rate.

{kind=link}

Using this data and applying it to revenue growth, we can generally spread out revenue growth expectations throughout FY24.

{kind=link}

And finally, applying this to total revenue while including existing locations, we can come up with total net sales.

{kind=link}

Finally, we can project these figures out down the income statement to build out the firm’s operations.

{kind=link}

My assumption towards margin expansion into q3’24 while tapering off into q4’24 resides in the gasoline margins, as I anticipate WTI to remain in the low-$70/bbl, as discerned in my other reports covering the energy industry. As management concluded in their earnings report, falling oil prices are expansive towards margins as rising oil prices are contractionary. Management also discussed that their black label products under the Kirkland brand experienced 0-1% inflationary pressures, suggesting that there will not be many price increases in the near future.

{kind=link}

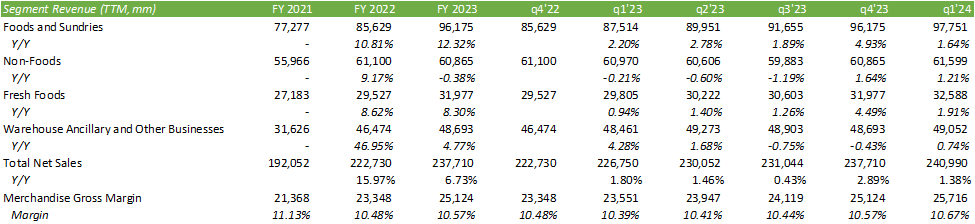

Overall, each segment experienced slowing growth, with ancillary items experiencing modest growth. Costco’s growth will come down to the strength of the consumer throughout 2024 as many households tighten their budgets. On a comparative basis, Costco offers better price points when compared to their peers in the organic foods industry. This has resulted in tighter overall margins as the firm competes to offer the highest quality products at the lowest price. Merchandise gross margins have been improving since q3’23 as gasoline prices have been in decline with oil prices. Aside from a few items, Costco reminds me of Sprouts Farmers Market ( SFM ) in which each firm has a very dedicated clientele and focuses on a limited number of available items. Though each store won’t be the all-inclusive one-stop-shop, the store’s core focus is in high turnover inventory with limited spoilage.

The biggest question that comes to mind is just how durable Costco's growth will be if the US were to go through a recession. My expectations would be a slowdown in big ticket items and non-food goods, while fresh foods and foods & sundries remain steady. Given Costco's black label price point, there may be opportunity to pick up additional customers that consider the long-term value Costco's pricing has to offer.

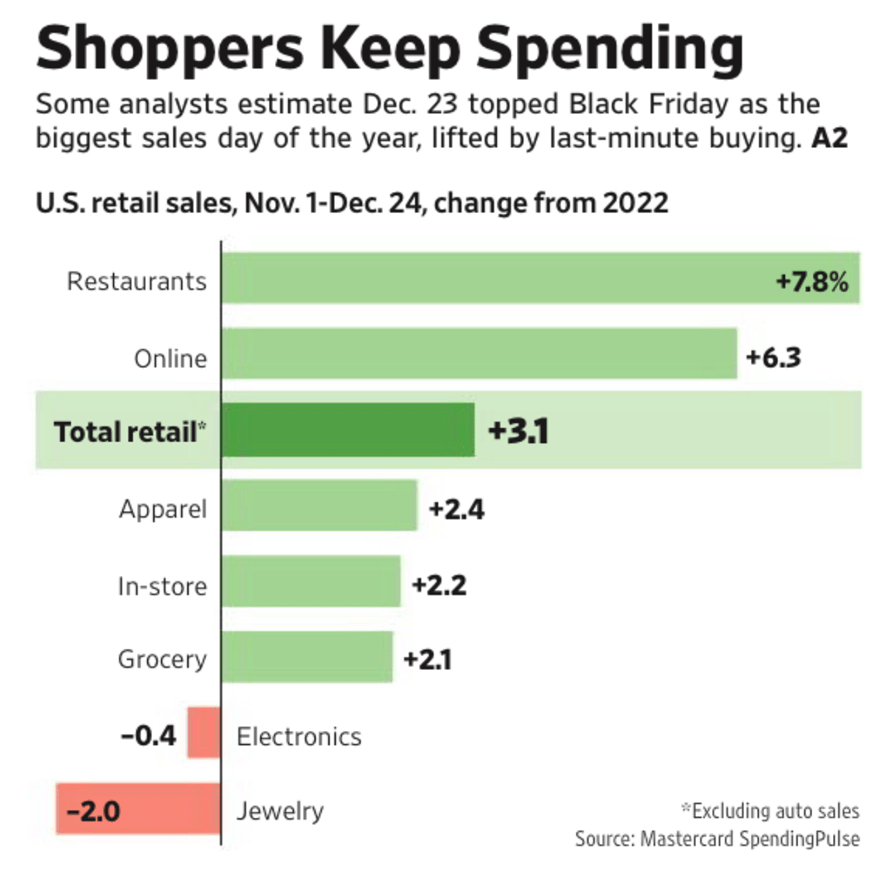

The Wall Street Journal reported strong consumer sales across many of Costco’s verticals, with some downside risk to electronics. For the most part, these figures can be seen as beneficial to Costco, with the exception of electronics sales.

{kind=link}

Despite my optimistic views on the firm, there are some potential headwinds to consider when investing in COST. Consumer strength can turn on a dime as the labor market softens and can challenge Costco's growth potential. Food inflation is heavily tied to geopolitical risk factors, as the US depends on global trade for many of these commodities. An example of this being 35% of the world's potash production resides in Russia and Belarus. Russia and Ukraine account for 25% of the world's wheat production. Given the recent events of the Russia/Ukraine war and how these commodities' prices reacted, it's clear that these exogenous risks heavily affected price inflation. This can have ripple effects to firms like Costco that manage their business on razor-thin margins.

Another headwind can be the effects of a flat or increasing oil market. As management has discerned in their earnings calls, higher oil prices can narrow gross margins and make Costco appear less profitable. I believe a flat oil market can do much of the same, as gasoline prices at the pump can slowly gravitate downward towards a price that reflects oil prices. Given that Costco prices their gasoline relative to surrounding gas stations, I don't believe gasoline prices will be cost competitive in this sense.

Lastly, a tighter consumer budget could potentially benefit Costco in the sense that Costco's Kirkland brand is oftentimes more competitively priced when compared to name brands. Costco also has more control over costs and pricing across the different products that fall under their Kirkland brand. Costco experienced higher penetration of their black label products last year in the range of 1-1.50%, well above their normal penetration rate of 25-50bps. Though penetration has gravitated back towards the historical norms, there may be further opportunity for growth during a recessionary period.

Valuation

{kind=link}

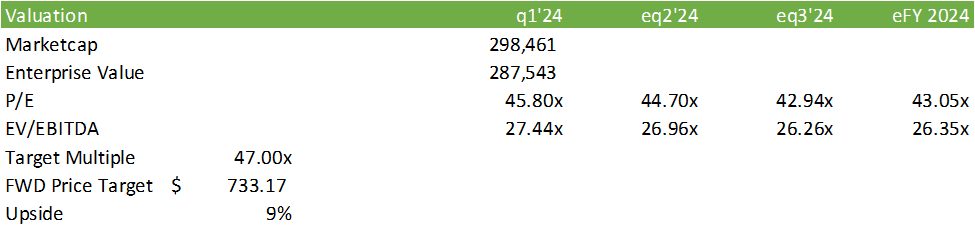

Costco trades at a relatively high valuation when compared to its peers. Looking forward throughout 2024, I anticipate margin expansion through q3’24 with a slight contraction going into the end of the year in anticipation of rising gasoline prices .

{kind=link}

COST has consistently traded at a higher multiple in the range of mid-30s-to-mid-40s, with a peak of 49x P/E. Considering the historical pricing chart as found below, we can expect the multiple to continue to rise before resetting down post-earnings. COST shares may provide some near-term room for its continued share growth.

{kind=link}

Given the growth trajectory and new store openings, I provide COST a BUY recommendation with a price target of $733.17/share at 47x 2024 PE.

For further details see:

Costco's Growth Will Persist, Even If The U.S. Enters A Recession