CTRA - Coterra Energy: A Bullish Bet For Energy Investors

2023-07-20 13:33:13 ET

Summary

- Coterra Energy is a strong income play in the energy sector with large reserves, low breakeven prices, and a healthy balance sheet.

- CTRA stands out as one of the best natural gas players in the market, with a less volatile stock price compared to peers.

- The company plans to distribute most of its free cash flow to shareholders through dividends and buybacks, making it an attractive choice for income-focused investors.

Introduction

While I would make the case that I cover a wide number of stocks, I do miss a few good ones that deserve more attention.

Coterra Energy ( CTRA ) is one of the stocks I should have paid attention to much earlier. Not because I'm missing out on capital gains - the valuation is still fine - but because the stock is a tremendous income play in the energy sector, albeit a volatile one.

This natural gas-focused upstream player has large reserves, low breakeven prices, a healthy balance sheet, and the intent and ability to distribute most of its free cash flow to shareholders using its regular dividend, buybacks, and special dividends.

Furthermore, its stock price is less volatile than smaller peers, making it a much better play for conservative, income-focused investors in this segment.

Now, let's dive into the details!

Cautiously Bullish On Natural Gas

I have roughly 17% energy exposure in my dividend growth portfolio. This mainly consists of drillers like Pioneer Natural Resources ( PXD ), Canadian Natural Resources ( CNQ ), Chevron ( CVX ), and Valero Energy ( VLO ). The last one is a refinery company, which is different from upstream players.

In my trading account, I own Antero Resources ( AR ), a natural gas giant with a lot of benefits that I discussed in this article .

However, AR doesn't pay a dividend. It's also much more volatile than CTRA.

While all major natural gas players underperformed the Energy Select Sector ETF ( XLE ) over the past ten years, CTRA had the best total return among its peers, with a decline of less than 6%.

The big problem between 2014 and 2020 was that natural gas producers boosted production too much. Unconventional drilling methods and plenty of reserves provided the US with low energy prices, which kept a lid on inflation.

Energy Information Administration

{kind=link}

Unfortunately, it also kept a lid on the stock price of drillers, as supply growth made it impossible to grow free cash flow.

Now, that is changing.

This is what I wrote in the aforementioned Antero Resources article (emphasis added):

Natural gas presents an attractive investment opportunity. This is driven by supply and demand dynamics. The US's unconventional production methods have led to a decline in prices, but the market is now showing signs of a sustained uptrend .

As natural gas gains importance globally as a cleaner fossil fuel and a bridge technology, demand is expected to increase by at least 38% by 2050 . This growing demand, along with the rise of liquid natural gas exports, will put pressure on declining supply growth and favor higher prices .

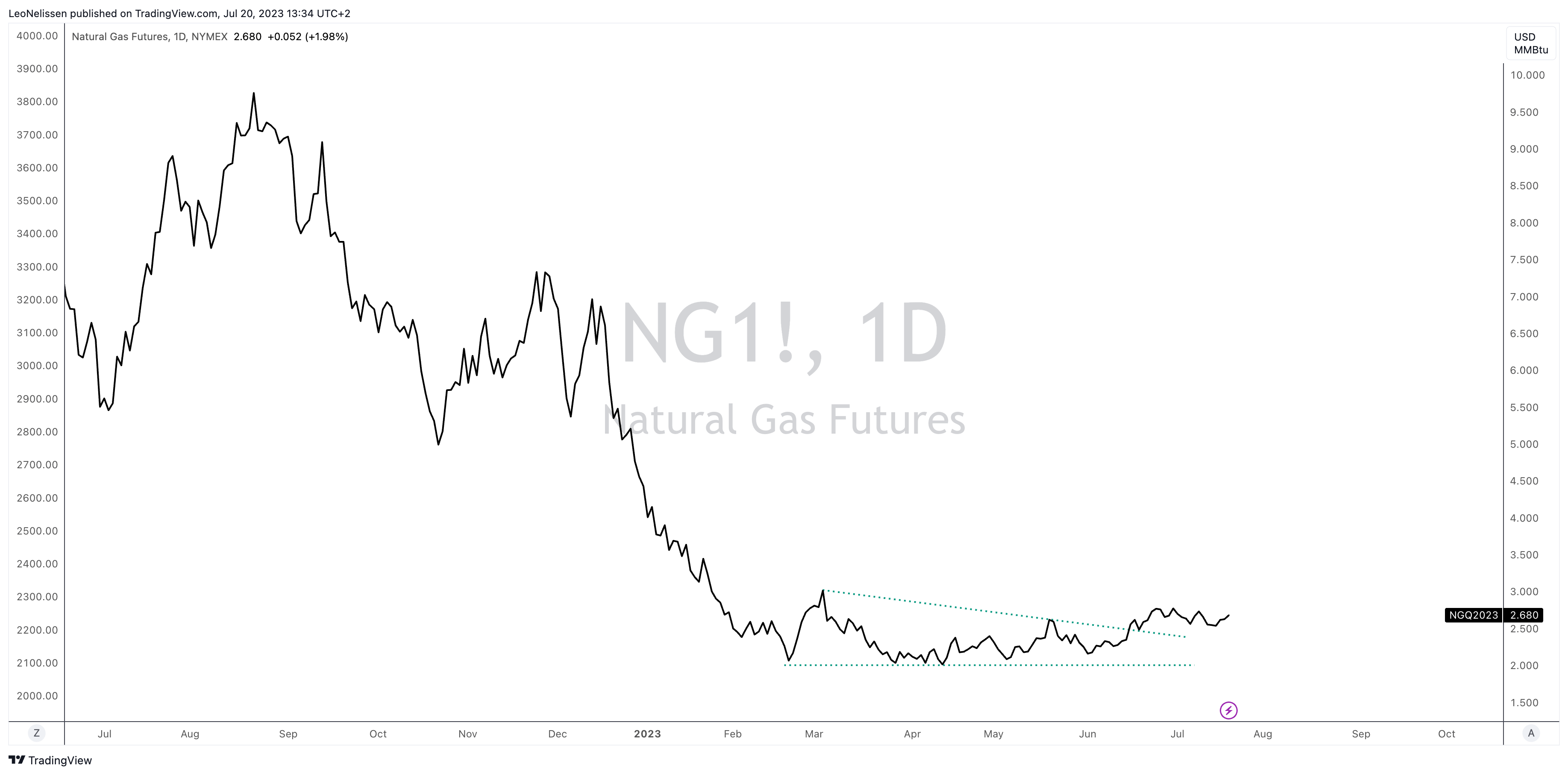

Having said that, natural gas prices are creeping higher after breaking out in June.

{kind=link}

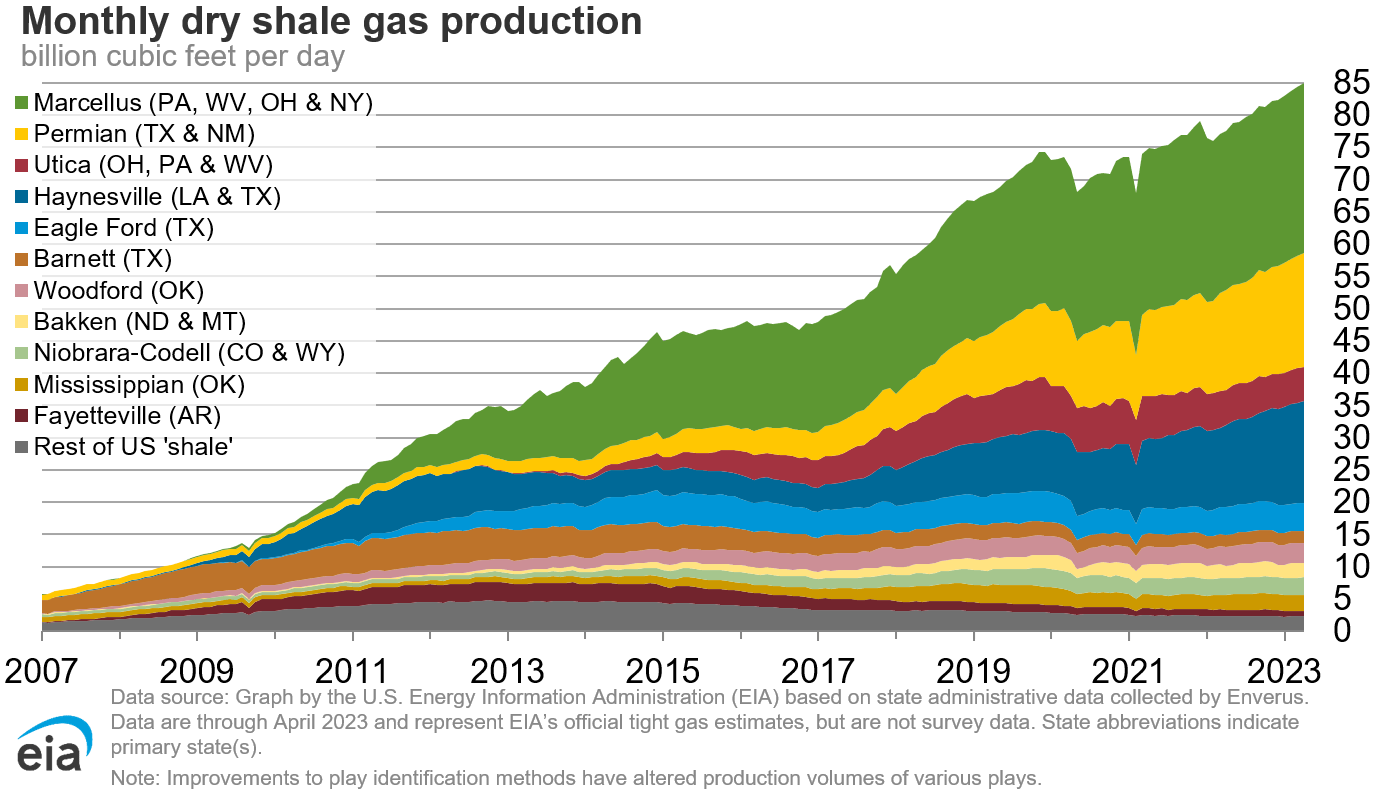

According to the Wall Street Journal , the surge is based on expectations that production levels are beginning to decrease from their all-time highs.

The EIA's monthly Drilling Productivity Report indicated a likely slight decline in natural gas output in the US's seven main shale regions for August, compared to July's record high.

If this trend continues, it could lead to a more sustained rally in prices during the fall, despite weak demand from a shrinking US manufacturing sector.

Energy Information Administration

This is what the EIA wrote in its short-term energy outlook in July:

We expect the Henry Hub spot price will rise in the coming months as declining natural gas production narrows the existing surplus of natural gas inventories compared with the five-year average. Henry Hub prices in our forecast average more than $2.80 per million British thermal units (MMBtu) in the second half of 2023 (2H23), up from about $2.40/MMBtu in the first half of the year.

Now, let's dive into CTRA.

Why This Is Bullish For CTRA

When it comes to energy stocks, I care about a number of things.

I'm not buying risky players anymore. Even if some of them might have sky-high returns. I want quality.

I want producers with deep reserves, low breakeven prices, healthy balance sheets, and the related ability (and willingness) to distribute most of their free cash flow to shareholders.

As I believe in a prolonged (but volatile) bull market for energy commodities, I want the best producers that can provide cash flows for their owners.

CTRA is one of these companies. As its historic stock price performance already suggests, CTRA is one of the best players on the market.

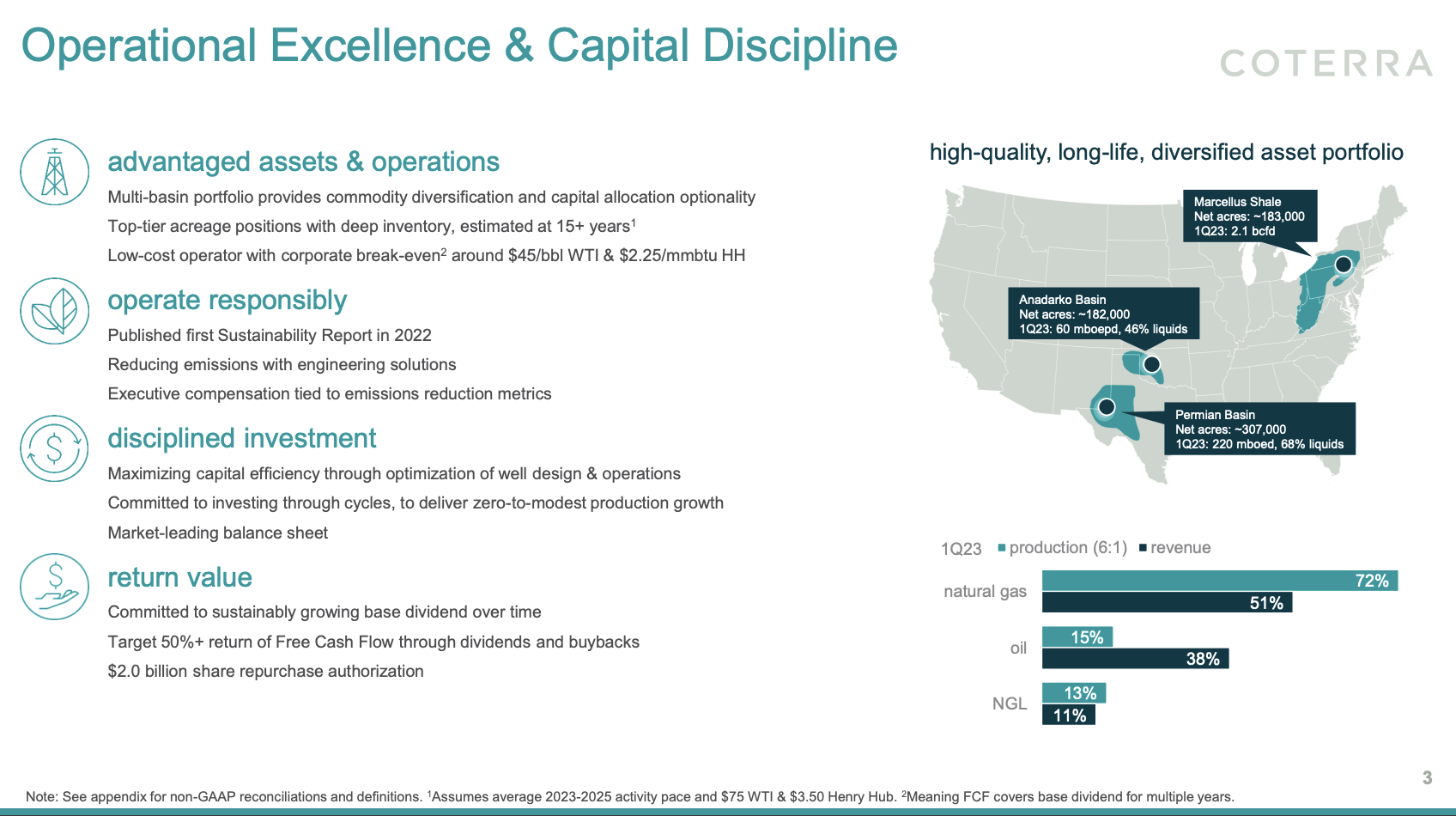

With a market cap of $21 billion, CTRA is one of the biggest players in its industry. Headquartered in Houston, Texas, the company generates roughly half of its money from natural gas. The other half is generated by selling oil and natural gas liquids. Production occurs in the Marcellus Shale, the Oklahoma-based Anadarko basin, and the mighty Permian.

{kind=link}

Furthermore, the company is highly efficient. It is breakeven around $45 WTI and $2.24 natural gas. Both of these numbers make the company a leader in its industry.

Looking at the overview below, reserves are expected to be between 15 and 20 years, which depends on a number of factors that influence both the speed and efficiency of production. Also, bear in mind that the company isn't running out of inventory after 15 to 20 years. New discoveries will consistently add new inventory, albeit at a slowing pace.

{kind=link}

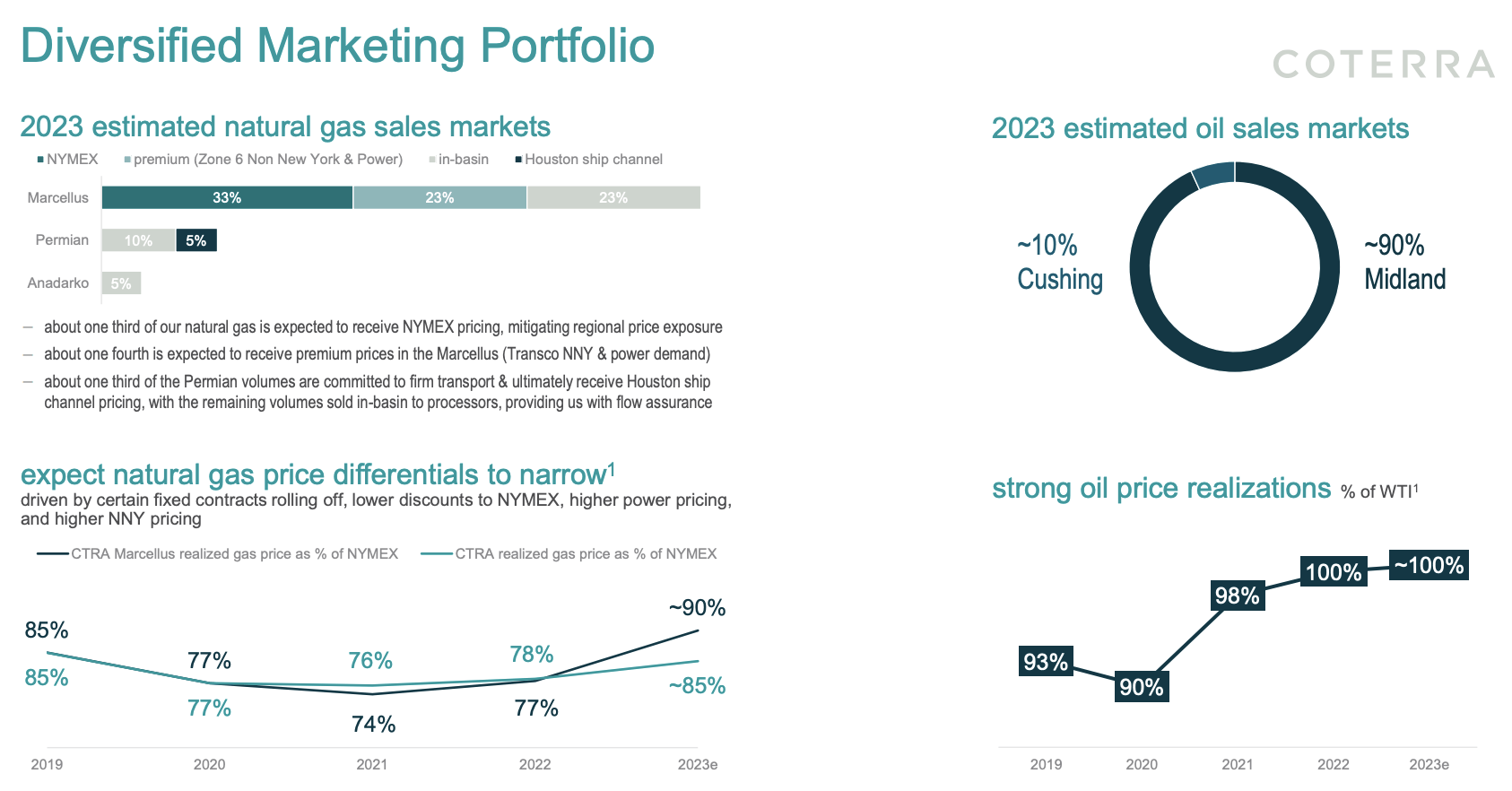

The company also benefits from strong price realization. It realizes roughly 100% of the WTI price and roughly 90% of natural gas in the Marcellus basin. While oil numbers are obviously great, the natural gas numbers are on an uptrend, which I expect to continue as the Marcellus infrastructure improves.

{kind=link}

Having said that, in its 1Q23 earnings call, the company made clear that it remains committed to the three-year plan outlined in its Q1 release.

{kind=link}

They intend to reduce activity in the Marcellus, maintaining two rigs and one frac crew during the second half of the year. Holding this level of activity flat through 2025 could significantly decrease future Marcellus CapEx, providing the option to reallocate activity to the Permian and Anadarko basins, which offer promising returns.

A part of its 3-year plan is also oil production growth of 5% per year and natural gas growth of 0% to 5% per year.

Thanks to this shift in capital, the company expects to achieve these growth rates without boosting capital spending, which is terrific for the company and its shareholders.

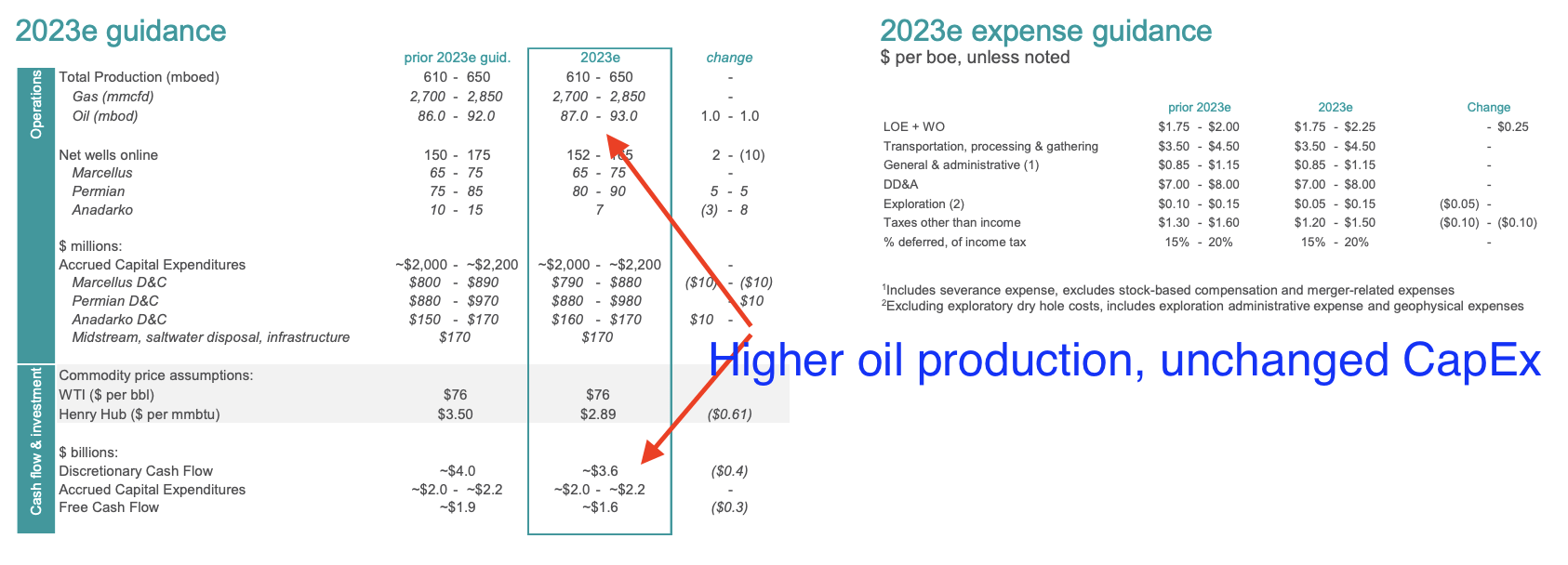

Speaking of capital, Coterra also provided refinements to its 2023 guidance and activity outlook during the aforementioned 1Q23 earnings call.

The company maintained its capital estimate of $2.0 billion to $2.2 billion and increased its full-year oil guidance by 1% to a range of 87 to 93 thousand barrels of oil per day. I highlighted these numbers in the overview below.

Coterra Energy (Author Annotations)

{kind=link}

This increase is attributed to efficient operations and strong well performance in both the Permian and Anadarko basins.

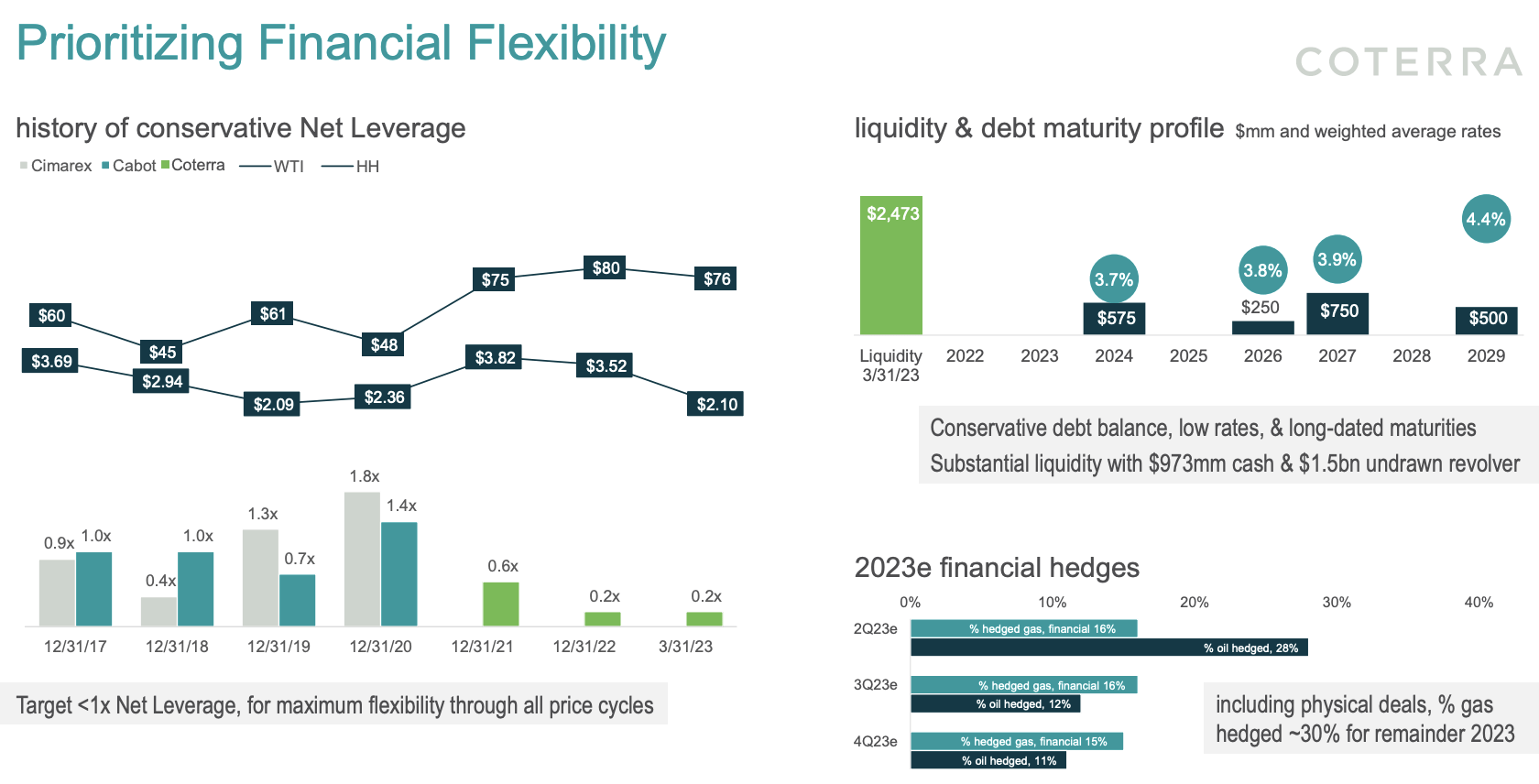

Based on this context, the company has very conservative hedges. Including physical deals, the company has hedged roughly a third of its production, which comes with downside protection, but not too much to keep the company from benefiting from potentially (much) higher prices down the road.

Furthermore, the company has deleveraged. After the merger between Cimarex and Cabot, the company has reduced its net leverage ratio to just 0.2x EBITDA. It has $2.5 billion in liquidity and no maturities larger than $700 million until 2027.

{kind=link}

In other words, when combining a healthy balance sheet with a deep inventory (no requirements for aggressive M&A), and efficient operations, CTRA is in a great spot to return cash to its shareholders.

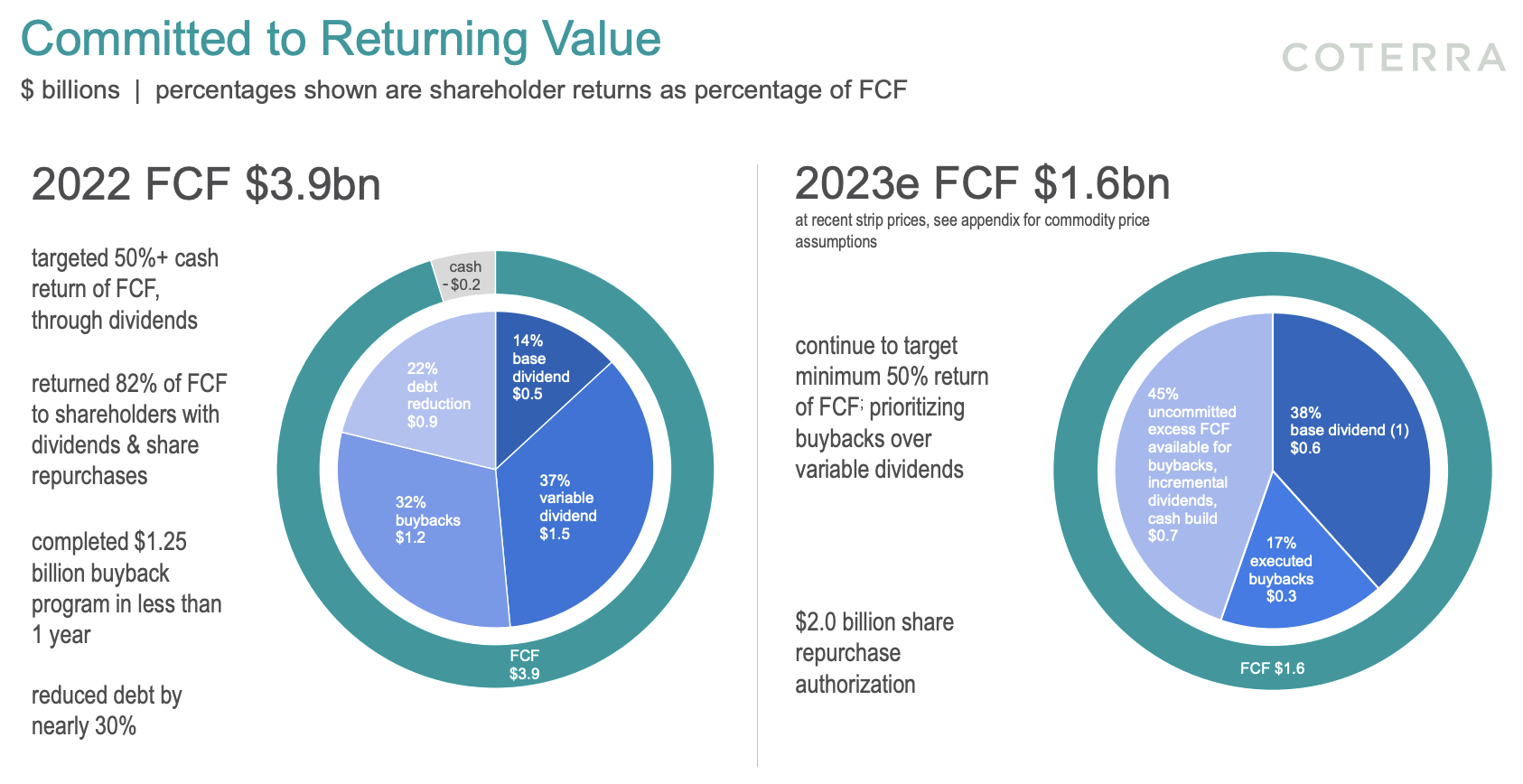

Having said that, during the first quarter, Coterra demonstrated its commitment to shareholders by announcing a $0.20 per share base dividend during the first quarter, maintaining one of the highest-yielding base dividends in the industry.

Based on the current share price, this translates to a 3.0% base yield.

The company plans to increase this base dividend annually.

{kind=link}

Additionally, Coterra repurchased 11 million shares, which totaled $268 million, during the quarter. This represents 76% of free cash flow returned to shareholders.

The company also made clear that it will prioritize strategic buybacks over variable dividends, with over $1.7 billion remaining on the $2 billion buyback authorization.

When combining both dividends and buybacks, Coterra reiterates its commitment to returning 50% or more of free cash flow to shareholders annually, which is a great deal, as it could pave the way for distributions in the high-single-digit percentage range (of the company's market cap) in an environment of elevated energy prices.

Given my bullish view on natural gas prices and the company's qualities that make it a top-tier energy play, I rate CTRA a buy.

Takeaway

I believe that Coterra Energy is a promising income play in the energy sector, offering a reliable dividend and buyback strategy for shareholders.

With large reserves, low breakeven prices, and a healthy balance sheet, CTRA is well-positioned to capitalize on the growing demand for natural gas.

As natural gas prices trend upwards due to declining production growth, CTRA is set to benefit significantly.

Its commitment to conservative hedges, efficient operations, and strategic buybacks reinforces its position as a top-tier energy player.

As an investor with a bullish view on natural gas prices, I believe CTRA is a compelling buy, offering potential high-single-digit to low-double-digit range distributions in an environment of elevated energy prices.

For further details see:

Coterra Energy: A Bullish Bet For Energy Investors