CTRA - Coterra Energy: A Buy Driven By Excess Cash From Operations

2023-08-22 14:55:08 ET

Summary

- Coterra Energy's Q2 results showed a decline in revenues due to lower commodity prices, but the company was able to increase production and improve operational efficiency.

- The company's management revised the 2023 guidance upwards, indicating better-than-expected results in the first half of the year.

- Analysts have a positive outlook on Coterra Energy, with a target price forecast that suggests a 12% upside potential.

A couple of weeks ago, Coterra Energy (CTRA) released its results for the second quarter of 2023 with the market positively reacting to the financials. In this article, I will provide an analysis of Coterra’s Q2 results and I will explain my buy thesis. If you are not familiar with Coterra Energy, you can have a look at my first article about the company where I provided an in-depth description of the business.

In short, Coterra Energy is a leading US onshore oil and gas producer with operations focused on three basins: Marcellus Shale, Anadarko Basin and in the Permian Basin.

If you are interested in other oil and gas stocks, you can read my article about Reconnaissance Energy or, if you are more focused on energy stocks in the broader sense, you can look at some of my recent articles about oil tankers companies such as Scorpio Tankers and Teekay Tankers .

Stock performance

Coterra Energy is currently trading at a price of $28.1/share, equivalent to a market cap of about $21 B. The stock is down 9% year-on-year while it is up 13% year-to-date. As you can see from the chart below, the stock is affected by strong volatility with the price that, in the last year, moved between $22.7/share (52-week minimum) and $32.2/share (52-week maximum). The minimum was recorded on March 15 th , 2023, while the maximum was on September 14 th , 2022. Coterra is now trading at about a 14% discount to the 52-week maximum price.

Q2-2023 results

In the second quarter of the year, total revenues declined by 54% to $1.18 B vs the $2.57 B of the previous year. The largest drop was in natural gas revenues, down 70% y-o-y (to $436 M) while oil revenues ($626 M) declined by 29% and NGL by 54% to $129M. The impact of hedging was negative at -$12M, much lower than the precedent year (-$66M).

The drop in revenues is explained by the decline in realized price across all commodities: NatGas was $2.81/mcf in Q2-2023 vs $4.66/mcf in Q2-2022 (-40%), oil was $73/bbl vs $84/bbl (-14%) and NGL was $20.1/bbl vs $38.5/bbl (-48%).

As one can see, in percentage terms, the effect of price decline was lower than the drop in revenues. Indeed, during Q2-2023, Coterra Energy was able to increase its daily production year-on-year. In the table below, production volumes for Q2-2023 can be seen.

Coterra Energy 10-Q

In Q2, the total OpEx slightly decreased by 5% to $909 M mostly due to a decline in D&A (-5% to $395 M) and G&A (-33% to $58 M). EBIT was down 83% to $276 M and net income was down as well by about 83% to $209 M.

Despite these results looking worse when compared to the previous year, it should be noticed that the lower EBIT and net income were only because of the commodity price effect: indeed, the company was even able to increase daily production and improve operational efficiency by reducing OpEx.

Looking at cash flows, Coterra generated $2.14 B of operating cash flows in H1-2023, almost in line with the previous year ($2201 M). Cash flow from investing was negative at -$1.05 B (vs -$741 M in Q2-2022) due to higher capital expenditures in drilling and completion. Cash flow from financing was negative (-$925 M) since the company repurchased common stocks for a total value of $325 M and paid dividends of $588M.

At the end of Q2-2023, Coterra Energy had a net debt exposure of $1.33 B, down 11% from the $1.50 B of Q2-2022. The liquidity amounts to $2.34 B with the first debt maturities coming in 2024 ($575 M).

2023 Outlook and 2023-2025 Snapshot

During the call with analysts, Coterra’s management announced an upward revision of the 2023 guidance, driven by the better-than-forecast results shown in the first half of the year. Particularly, the mid-point for oil, gas and total production was increased by respectively +3%, +2% and +2%.

Coterra Energy 10-Q

For the period 2023-2025, Coterra is planning to achieve consistent and profitable growth while ensuring a return to shareholders and a sound balance sheet. According to the company calculations, assuming an already committed cumulative cash of $8 B to be paid in 2023-2025 ($2 B for dividends and $6 B for CapEx), under a strip price commodity scenario, there would still be $4 B of excess cash flow from operations either to be distributed or reinvested in the business or used to repay the debt. Under a more conservative scenario (oil flat at $55/bbl and NatGas flat at $2.75/Mcf), the excess CFFO would be lower, but still around $1 B.

In addition, Coterra’s management seems optimistic about the possibility of reducing costs for 2024 by at least 5% even though, likely out of caution, they have not revised the CapEx guidance.

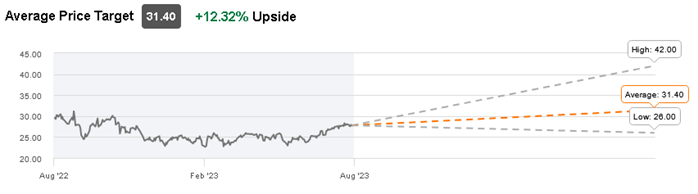

Analyst’s valuation and target price

Coterra Energy is currently covered by 28 analysts from investment banks and equity research firms. 18 of them have issued a hold rating while 10 have proposed either a buy or strong buy rating. It should be worth mentioning that the most recent reports are leaning towards buy/strong buy recommendations.

The average target price forecast by analysts is $31.4/share, which would represent a +12% upside versus the current trading price. Once again, the current forecast for the target price might be negatively affected by older hold reports.

{kind=link}

Peer comparison

In order to have a better understanding of how fair Coterra Energy trading price is, I performed a comparison between Coterra and its peers. I selected oil and gas companies that are mostly focused on the US and with a market cap of at least $5 B. Looking at the EV/EBITDA, one can see that Coterra is trading at a discount to the average EV/EBITDA (-8%) and to the median EV/EBITDA (-9%). Alternatively, looking at the price to earnings ratio, the story is a bit different with Coterra trading at a small premium to the average P/E (+1%) and to the average median P/E (+4%).

Reuters

However, for oil and gas companies, I would consider the EV/EBITDA to be more reliable since EBITDA, differently from net income, excludes the effect of depreciation and amortization. D&A is always a tricky accounting item since it can be managed in different ways and, moreover, in O&G companies is usually quite a large figure that can skew the net income and consequently the P/E ratio.

Risks

As for all oil and gas companies, the commodity price volatility represents the main risk for Coterra Energy. In the last years, commodity prices have wildly fluctuated and, if high prices can ensure huge profits, low prices for a long period could seriously damage the balance sheet of any O&G company, including Coterra. Moreover, under a low-price scenario, companies might even need to revise the economic viability of certain drilling operations with a subsequent reduction in production and proven reserves. Therefore, some oil companies protect themselves from such commodity price volatility using hedging schemes that set a predefined price at which oil and gas production can be sold. However, these schemes also work in the opposite direction setting a cap on potential profits that could be generated by high prices. For this reason, Coterra Energy’s management decided not to hedge the 2023 production, fully exposing itself to the hedging risk. However, as explained above, even under a low-case price scenario, Coterra would still be able to generate a sufficient level of CFFO and, for this reason, I believe that taking the commodity price risk is a savvy move since it leaves room to capture the benefit of future high prices.

Conclusion

Coterra Energy reported Q2-2023 earnings that were worse than the year before but that was expected. Notably, the company was able to increase production during Q2-2023 and to revise upward the full 2023 guidance giving a clear example of its operational excellence. The balance sheet is robust and even under a low case commodity price, the company should not have issues in repaying the first tranche of debt in 2024. With the current strip prices, there is potentially an additional $4 B of CFFO that the company will be able to use in 2023-2025 to further develop value-creating initiatives. Overall, I believe Coterra Energy is worth a buy recommendation.

For further details see:

Coterra Energy: A Buy Driven By Excess Cash From Operations