CTRA - Coterra Energy: An Oil And Gas Superstar At A Discount

2023-11-04 07:42:23 ET

Summary

- The oil and gas industry is expected to enter a new supercycle, driven by geopolitical tensions, accumulated underinvestment in capex, and the massive projected economic long-term growth of India.

- Coterra demonstrates best-in-class profitability metrics, and its balance sheet is a fortress, making the company well-positioned to absorb industry tailwinds.

- The stock is 20% undervalued, according to my dividend discount model simulation.

Investment thesis

Coterra Energy (CTRA) grabbed my attention because it has one of the highest Quant rankings among the U.S. upstream oil and gas companies. I am firmly convinced that we are currently at the early stages of the new oil and gas supercycle due to multiple strong factors that I describe in my analysis of CTRA. As a company with a fortress balance sheet and massive operating leverage, Coterra is well-positioned to capture secular tailwinds and create long-term value for shareholders as the management prioritized dividend growth and stock buybacks. Overall, I assign Coterra Energy a "Strong Buy" rating.

Seeking Alpha

Company information

Coterra Energy Inc. is an independent oil and gas company engaged in the development, exploration, and production of oil, natural gas, and natural gas liquids [NGLs]. The company operates in one segment.

Coterra's fiscal year ends on December 31. According to the latest 10-K report , natural gas represented 57% of the company's total sales in FY 2022.

{kind=link}

Financials

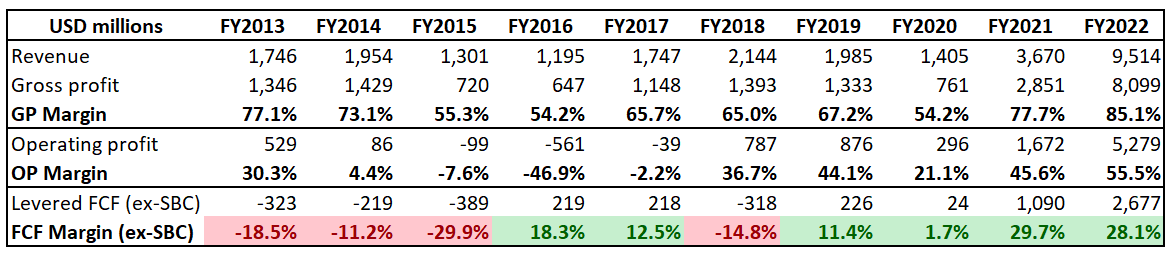

Coterra's financial performance over the past decade has been stellar. Revenue compounded at a staggering 21% CAGR. Still, the central part of the growth happened in FY 2022 due to the spike in energy commodity prices after the commencement of the Russia-Ukraine war. On the other hand, even without the FY 2022 commodity prices spike, the company demonstrated strong profitability metrics and generated almost 30% in free cash flow [FCF] margin ex-stock-based compensation [ex-SBC] in FY 2021.

{kind=link}

I like the management's approach to capital allocation as it has efficiently utilized massive last fiscal year's tailwinds to improve the balance sheet significantly. Despite being in a notable net debt position, the leverage ratio is low at about 20%, and the covered ratio is far above enough. Near-term liquidity metrics are also in excellent shape. The company's balance sheet gives the company plenty of room to invest in capex to fuel long-term revenue growth. At the same time, the company kept shareholders happy over the past decade with a staggering 34% dividend CAGR and consistently buying back shares.

Seeking Alpha

The latest quarterly earnings were released on August 7, when the company missed consensus revenue estimates by a notable margin but delivered in terms of the adjusted EPS. It is no surprise to me that quarterly revenue dropped by more than 50% because the comparative quarter was affected by last year's shock in energy commodity markets due to the war in Ukraine, which started in February 2022.

Seeking Alpha

What is crucial is that despite such a massive revenue drop, Coterra's profitability metrics are still stellar, with the operating margin at 24%. This allowed the company to generate $646 million in operating cash flow, which is more than 50% of the quarterly revenue. The major part of the operating cash flow was allocated to capex, which is good for the company's long-term revenue growth prospects.

The upcoming quarter's earnings are scheduled for release on November 7. Consensus estimates project quarterly revenue at $1.36 billion, which means that the top line is poised to demonstrate a sharp YoY decline again. On the other hand, the comparative quarter was also affected by last year's massive spike in energy prices. It is also important to underline that the YoY revenue decline in Q3 is expected to be 46%, which indicates a positive dynamic compared to Q2.

Seeking Alpha

Revenue is also expected to demonstrate a 14% sequential growth, which is also a positive sign. The major catalyst here would be the average WTI futures price increase in Q3 compared to Q2, according to historical prices . According to my calculations derived from historical prices, the Q3 average crude oil price was $81.94, compared to $73.72 in Q2. This indicates an 11% increase in average prices. Apart from price, production volumes also play a crucial role in the top line, and I am optimistic from this perspective since the company demonstrated solid outperformance in Q2. That said, I expect CTRA to deliver a strong quarter with a wide FCF margin, which will be distributed between dividends and the balance sheet improvement.

Coterra's latest earnings presentation

Overall, I am optimistic about Coterra's prospects for the next multiple years. There are several factors indicating that we are in the early stages of a new oil and gas supercycle.

First, in the macro economy, everything is cyclical. That said, after almost a decade of low energy prices when oil and gas companies had much fewer resources to invest in capex , substantial struggles with the supply side are inevitable.

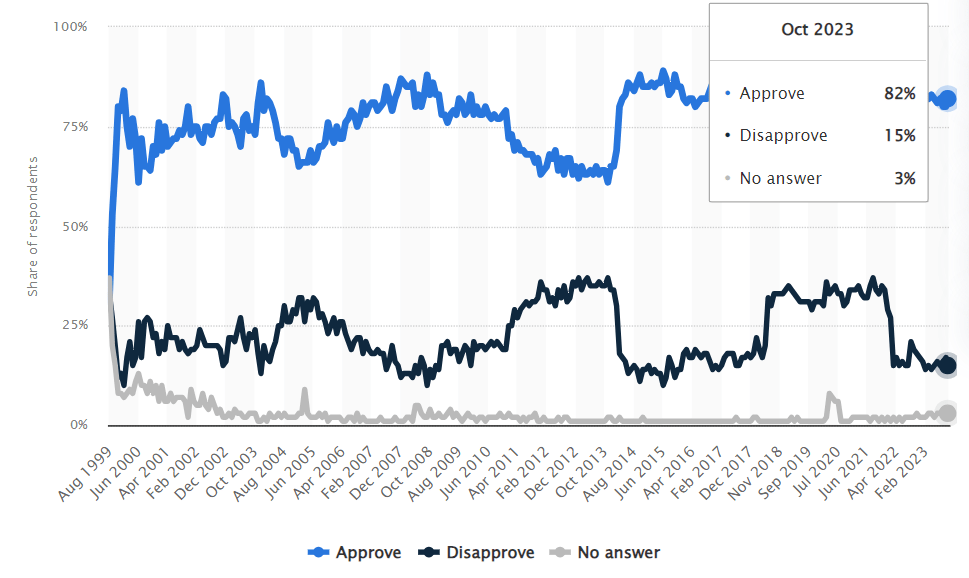

Second, apart from macroeconomic equations, the geopolitical factor is also a big catalyst for oil and gas prices. And right now, we are in the middle of the biggest war in Europe since WWII, with one of the world's largest energy producers and exporters under sanctions. And this war can last up to 2025, according to Defence Procurement International . From my point of view, the war can last as long as Vladimir Putin is the Russian president, and his reign is likely to go far beyond 2025, given his above 80% approval rating, according to statista.com . Apart from the Russia-Ukraine war, the recent escalation between Israel and Hamas also brings vast geopolitical uncertainties to another world's oil-rich part, the Middle East.

{kind=link}

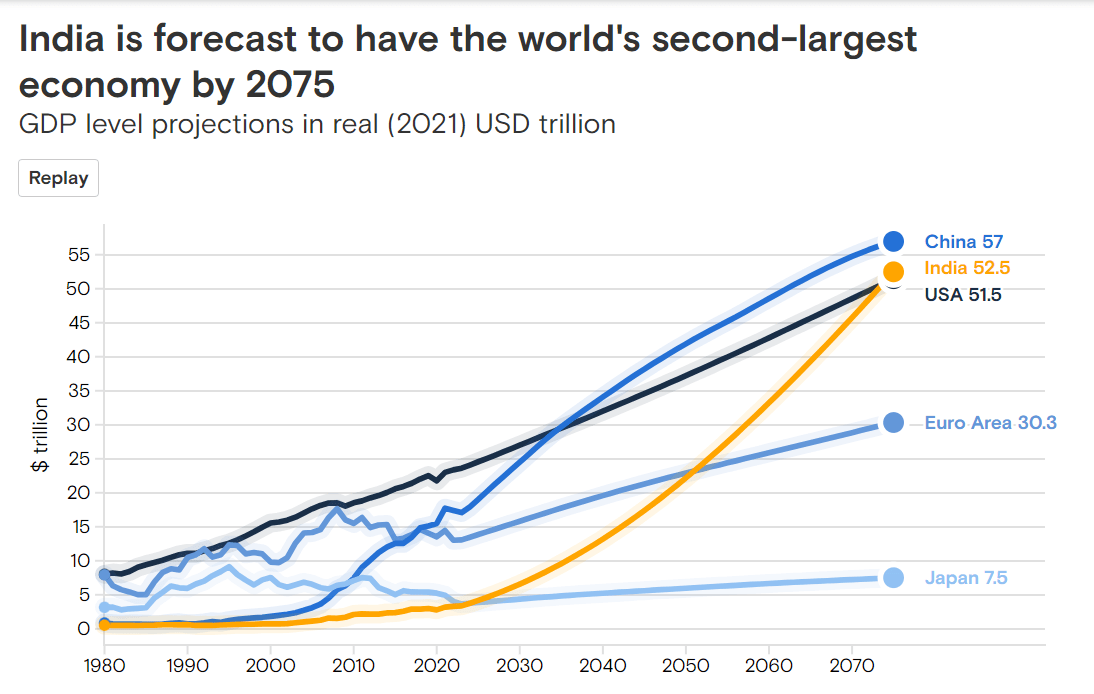

Third, the massive economic growth of China, when the GDP mainly grew double-digits per annum between the 1990s and 2010, was a strong catalyst for the previous oil and gas supercycle. While the Chinese economy nowadays demonstrates signs of running out of gas , it looks like India is poised to become the "new China" to drive global economic growth. According to Goldman Sachs , India can surpass the American GDP over the next 50 years. Given that the U.S. economy was about seven times larger than India in FY 2022, it means that the GDP of India is likely to compound at an impressive growth rate over the next multiple decades. This factor will also likely become a strong secular tailwind for energy markets.

{kind=link}

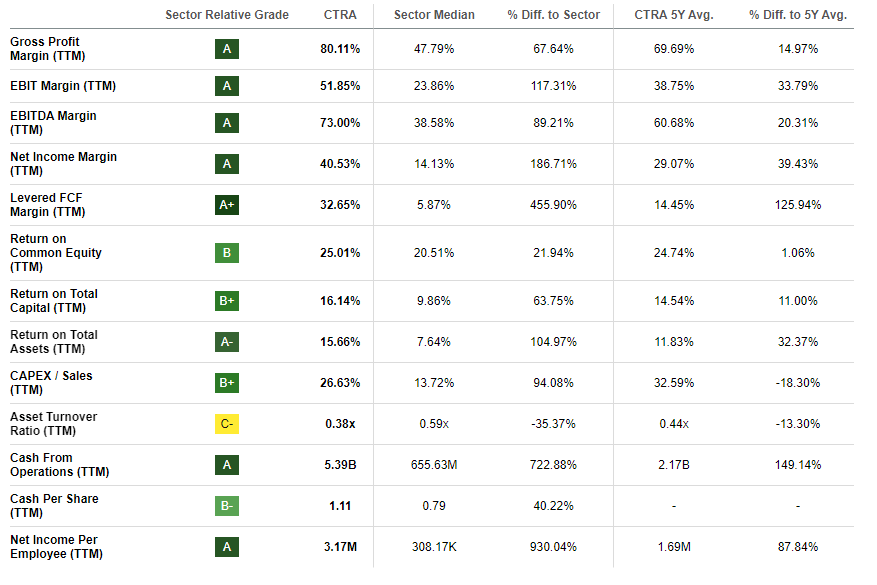

As we can see above, there are numerous solid secular tailwinds for the oil and gas industry. Companies with the strongest operating leverage and financial position will likely be the most successful in capturing positive industry trends. Coterra is apparently one such company, as it is in a fortress financial position, and its profitability metrics are best-in-class across the board.

{kind=link}

I also like the management's capital allocation approach, prioritizing shareholder returns while maintaining a clean balance sheet. Multiple decades of dividend payouts together with massive dividend CAGR over the last ten years is a vital quality sign for potential investors.

The company has more than sufficient inventories to capture favorable industry trends as it operates in the largest U.S. petroleum-producing basin, the Permian Basin. Coterra also operates in two other large formations, Marcellus and Anadarko. The latter two have substantially shorter estimated duration, but still, the company's average between 15 to 20 years looks solid. Apart from the longevity of the inventory, I would also like to underline the high quality of it. According to the latest earnings call presentation , the company consistently demonstrates strong oil price realizations of above 98%, which is impressive and means that discounts from the benchmark WTI oil are narrow.

Coterra's latest earnings presentation

With the top-line likely to be safe across all three major fields where the company operates for at least ten years, it is also important that the management strives to improve efficiency to drive down costs. During the latest earnings call , the management underlined that it sees potential to reduce well costs by about 5%, which is likely to be notable for the profitability improvement. For me, as a person who worked many years in the oil and gas industry, this looks doable as the company's initiatives are sound: drilling and completion rigs mobilization schedule streamlining, optimizing the oilfield infrastructure across more wells, implementing improved frac design to intensify pressure in wells.

To conclude this part, given the company's solid expected inventory duration and its high quality, together with a very responsible approach to cost efficiencies, I think that Coterra is well-positioned to sustain its high profitability in case crude oil prices stay higher for longer.

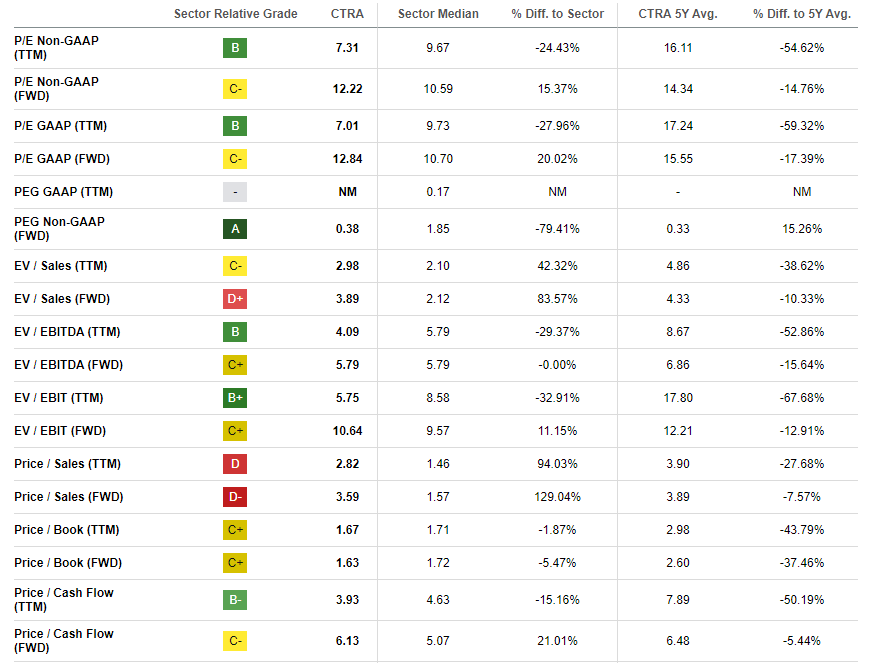

Valuation

The stock price increased by 23% year-to-date, outperforming the broader U.S. market and the Energy ( XLE ) sector. Seeking Alpha Quant assigns the stock an average "C" valuation grade, which indicates that the stock is fairly valued. However, Coterra consistently demonstrates stellar profitability and impressive long-term revenue growth. Therefore, it is more appropriate to compare current valuation ratios to historical averages. From this perspective, the stock looks undervalued as most ratios are currently lower than 5-year averages.

{kind=link}

I want to proceed with simulating the dividend discount model [DDM]. Consensus dividend estimates forecast FY 2024 payout at $0.84. I use a 10% WACC as a required rate of return. The company delivered staggering dividend growth over the past decade, but I use a very conservative 7.5% dividend CAGR assumption.

Author's calculations

According to my DDM calculations, the stock's fair price is almost $34. That said, CTRA is about 20% undervalued, which is an attractive upside potential to me, especially given the stellar dividend growth history.

Risks to consider

Share prices of energy companies are highly dependent on commodity prices, which makes stocks like CTRA very volatile. Share prices of these companies can experience big short-term moves, both upward and downward, based on news and rumors related to expectations in energy commodity prices.

As an energy company, Coterra also faces substantial regulatory and environmental risks. Changes in regulations or environmental disasters caused by the company's operations can bring substantial adverse consequences to Coterra's earnings and reputation.

Bottom line

To conclude, Coterra Energy's stock is a "Strong Buy". The company's stellar track record of success gives me a high conviction that CTRA is ready to absorb massive oil and gas industry tailwinds as we are highly likely in the new energy supercycle. The company's balance sheet is very strong, and the management's capital allocation is not only very shareholder friendly but balances between keeping the financial position healthy and improving the operating leverage.

For further details see:

Coterra Energy: An Oil And Gas Superstar At A Discount