CTRA - Coterra Energy: An Undervalued Permian Play

2023-09-24 04:33:20 ET

Summary

- Coterra Energy presents a strong value relative to its peers when compared to its operating cash flows.

- Coterra is less leveraged relative to peers exhibiting strong capital discipline and the ability to pay a consistent dividend.

- Coterra was formed in 2021 by a merger between Cabot Oil & Gas and Cimarex Energy and is in the process of executing on their synergistic strategy.

- Coterra is leveraged to the Permian Basin with a good-sized position in the play.

Coterra Energy ( CTRA ) is an energy exploration and production company with a market cap that is nearing 20 billion dollars.

History of Coterra Energy

Coterra Energy as an entity in its current state is very young. That's because it was formed as the "merger of equals" between Cabot Oil & Gas and Cimarex Energy in October 2021. Per a press release, at the time of the merger, the company held 700,000 net acres of drilling inventory. As with any merger, the company hoped to achieve synergy cost savings in the amount of $100 million annually.

When the merger occurred, the combined entity traded at roughly $22 per share. As of today, the company's shares trade near $26 per share.

One of the merged companies, Cabot Oil & Gas, traced its roots all the way to the early 1900s when Godfrey Cabot began a business focused on oil & natural gas in Pennsylvania.

Cimarex Energy also had a very long legacy. It was founded in 2002, as a spinoff from Helmrich and Payne, a contract drilling company. However, the company Helmrich and Payne goes back much further, having been founded in 1920 by Walt Hemerich II and Bill Payne in South Bend, Texas.

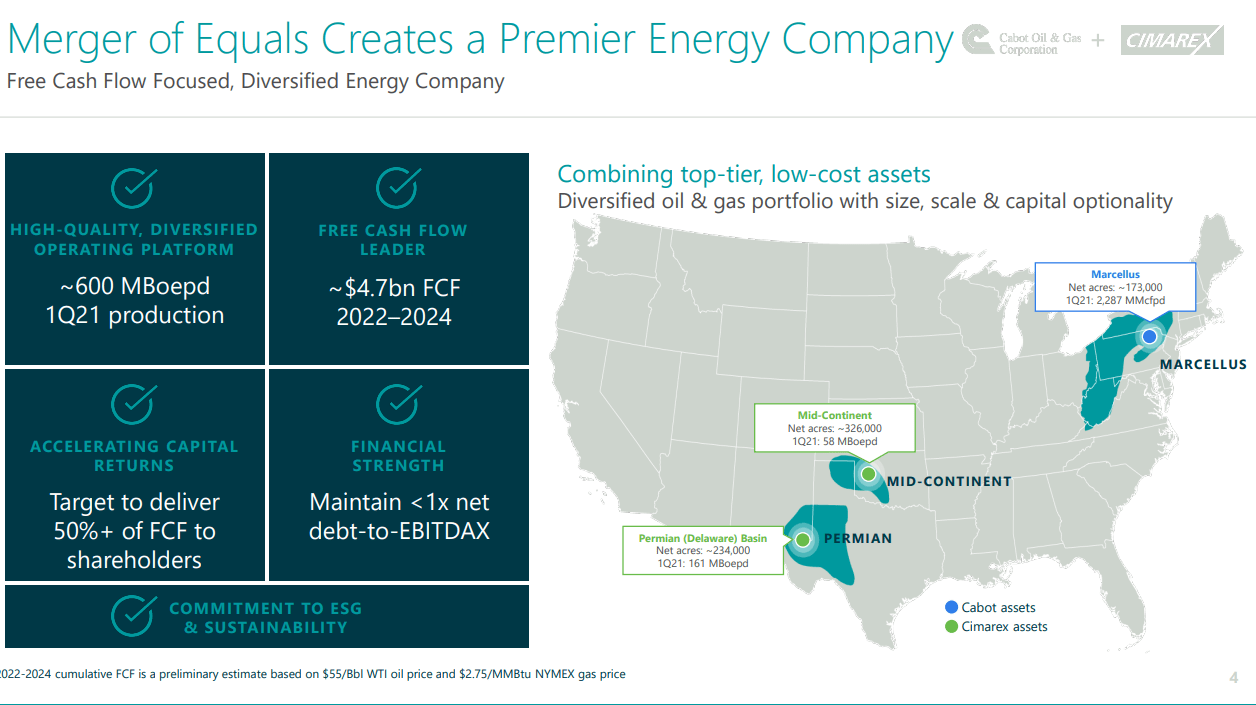

It is worth noting that at the time of the merger, Coterra Energy held roughly 234,000 acres in the Permian basin and today holds 307,000 acres. Here is a graphic showing the company as well as some of their goals over a 3 to 4 year time horizon at the time of the merger. Let's dig deeper to see how the company is performing.

{kind=link}

Coterra's Current Operations

This slide shows where Coterra's current "energy" is focused. Right now they have 2 rigs and 1 frac crew running in the Marcellus Shale, 1 rig and a part-time frac crew running in the Anadarko Basin, and 6 rigs and 2 to 3 frac crews running in the Permian Basin. As with most companies, their primary focus is extracting attractive rates of return from their Permian Basin acreage. More on that later.

Coterra's Asset Locations (Coterra Q2 Presentation)

Currently, Coterra receives most of their production from natural gas, but because there is an energy differential of 6 to 1, the company generates more revenue from its oil and ngls which primarily comes from its oil production in the Permian Basin. Some may not like a company with such a strong natural gas profile, but I have come to view companies like Coterra, where they employ a diversified strategy between natural gas and oil, as a strength. In fact, I've highlighted in several articles how I believe exposure to natural gas provides strategic upside as more and more oil and gas companies discover how to mine bitcoin. Effectively, they will be selling their natural gas to the bitcoin market. I discuss this concept explicitly in my article on Microstrategy , and more conceptually in this article .

Coterra's Production Profile (CTRA Q2 Presentation)

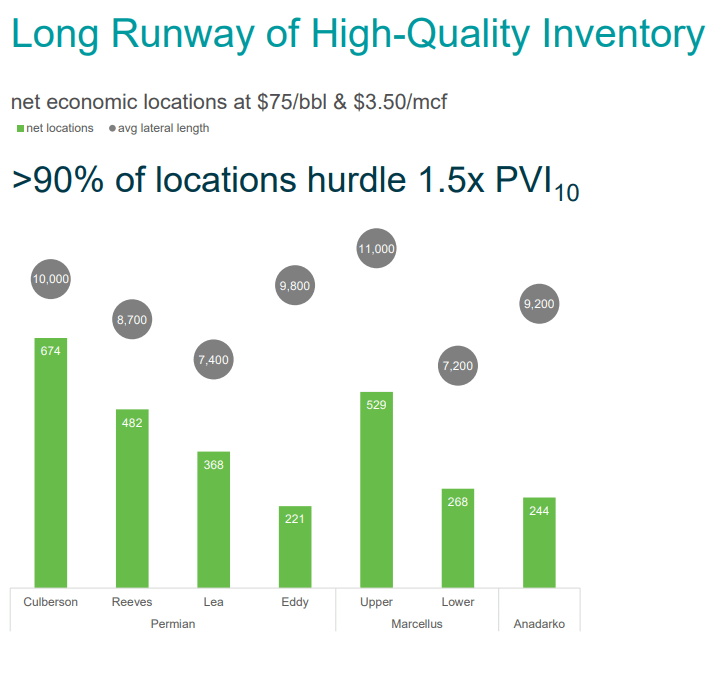

I wanted to present this slide to demonstrate the long time horizon of investment opportunities that the company has, especially in the Permian Basin. For some, this will make you alarmed that at some point in the future, they will run out of opportunities, but we must remember the long-term nature of the oil business. Companies are always replacing their reserves and there have been many times where people believed we would run out of oil, only for more oil to be discovered. See 1913 to 1920 or 2009. The point is, Coterra has a comfortable inventory of drilling prospects, which includes the premier play, the Permian.

CTRA Drilling Inventory Duration (CTRA Q2 Presentation)

This slide goes to show the economics of Coterra's drilling locations. Currently, the company believes that as long as oil remains above $75 per barrel, which seems extremely likely, and that gas remains above $3.50/mcf, these locations will generate a 1.5 PVI. This means that if you discount cash flows back to a present value, after investing capital, it should return a value 1.5 times greater than the capital invested. If this is the PVI with oil at $75 per barrel, what will this look like when oil is greater than $100 per barrel?

Economics of current drilling inventory (Coterra Q2 Presentation)

{kind=link}

Comparable Values Relative to Operating Cash Flow on TTM Basis

Right now, Coterra is undervalued relative to its operating cash flows, when compared to other companies. I like using operating cash flow as a metric because it provides a picture of cash the company has before it reinvests the capital or returns capital to shareholders. Regardless of whether it gets reinvested or returned, this is the cash flow you are "buying" as an investor.

Right now, for Coterra, you are buying a larger stream of cash flows relative to its share price. Let's look at some other metrics to see if there is a possible reason for this.

| (EOG ) |

| ( COP ) |

| ( NOG ) |

| (DVN ) |

| (CTRA ) |

| Operating CF |

| $13,749 |

| $24,589 |

| $1,141 |

| $7,097 |

| $5,395 |

| Market Cap() |

| $71.3 |

| $142.5 |

| $3.6 |

| $29.7 |

| $19.7 |

| MC / OCF |

| 5.19 |

| 5.79 |

| 3.16 |

| 4.18 |

| 3.65 |

Debt Ratios Compared

Given that Coterra trades at a lower multiple compared to its cash flow from operations, I was curious if it had a larger debt-to-asset ratio than its peers. Interestingly, what I found is that it has a lower ratio compared to various other companies I've written about more recently. It even barely edged out EOG Resources.

| (EOG) |

| (COP) |

| (NOG) |

| (DVN) |

| (CTRA) |

| Assets |

| 41,487 |

| 89,605 |

| 3,665 |

| 23,355 |

| 19,879 |

| Liabilities |

| 15,230 |

| 42,074 |

| 2,249 |

| 12,205 |

| 7,212 |

| Debt-to-Assets |

| .37 |

| .47 |

| .61 |

| .52 |

| .36 |

Net Permian Basin Acres Compared

Among each of these companies, I thought it would be interesting to see if Coterra has significantly less acres in the Permian Basin. I thought maybe this was why it was being discounted relative to its cash flows. However, this was not the case. Coterra reports that it holds 307,000 net acres in the Wolfcamp and Bonesprings plays in the greater Permian Basin. On a relative basis, this is a very good proportion of acres to own compared to its valuation.

| (EOG) |

| (COP) |

| (NOG) |

| (DVN) |

| (CTRA) |

| Net Acres |

| ~600,000 |

| ~600,000 |

| ~100,000 |

| ~400,000 |

| 307,000 |

Naturally, this doesn't take into account each company's various assets in the different plays, and so take this with a grain of salt. All that this says is that when you consider its Permian acres, its undervaluation may not be justified.

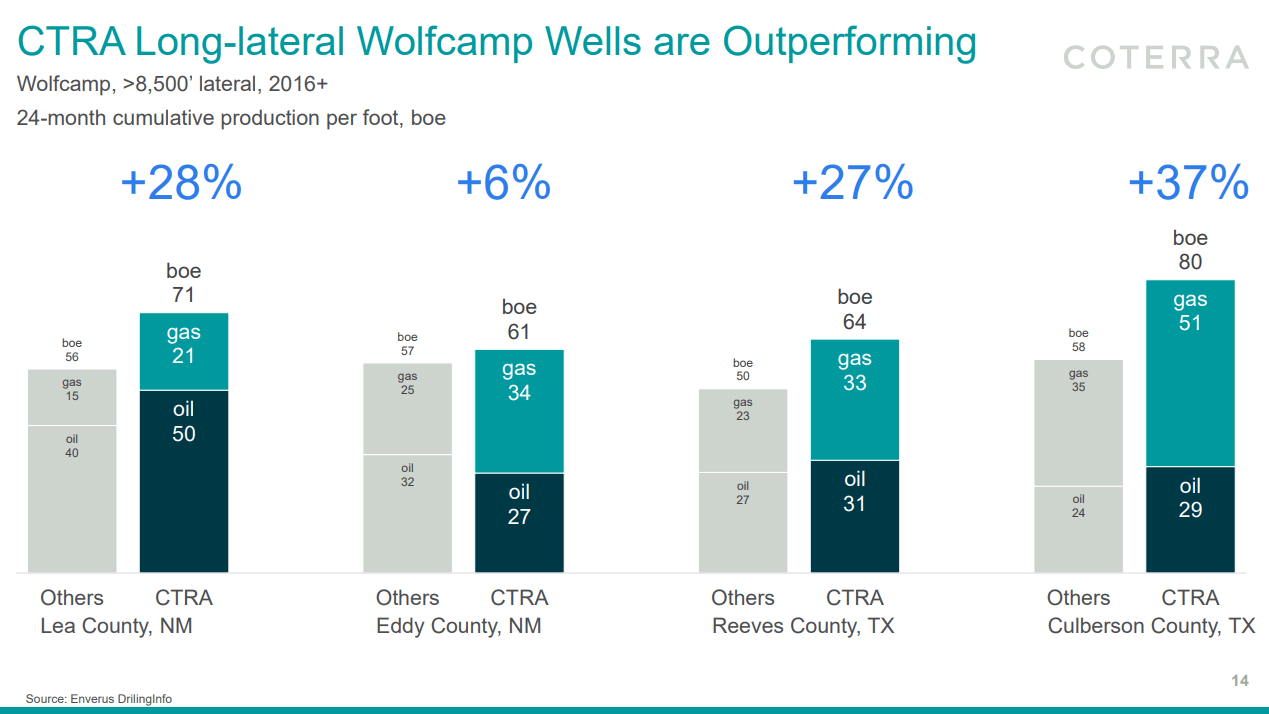

Here's a slide comparing its Wolfcamp well performance to the average well in the play. They have used a long-lateral strategy to gain outperformance which I must assume is worth any additional capital required for the longer-lateral.

{kind=link}

Conclusion

Coterra is positioned to profit from their apparent capital discipline and strong hydrocarbon prices in the coming years and quarters. And although I didn't discuss it, the company is also dedicated to paying a consistent dividend. As the oil and gas industry has transitioned to horizontal drilling in shale plays, company cash flows have generally become predictable, which is why I make the claim that while many traditional dividend stocks are slashing dividends, the oil and gas companies are set to become known as consistent dividend paying stocks .

There are always risks, but with any oil and gas company, and in today's environment, the largest risk is always over-leverage in the face of an oil-price decline.

I rate Coterra a "Strong Buy" considering its position in the greater Permian Basin, undervaluation relative to peers, and its strong balance sheet.

For further details see:

Coterra Energy: An Undervalued Permian Play