CTRA - Coterra Energy: Strong Operational Performance But Limited Hedges Against Falling Gas Prices (Rating Upgrade)

2023-12-13 22:34:47 ET

Summary

- Coterra increased its 2023 production guidance again with no change to its capex budget.

- Strong operational performance has resulted in 2023 oil production guidance going up +7% from original guidance, and total production up +5% from original guidance.

- Despite its strong operational performance, near-term free cash flow expectations have been reduced due to weak commodity prices.

- Coterra has relatively limited hedges that provide around $50 million in positive value for 2024 at current strip (including $2.55 NYMEX gas).

Coterra Energy ( CTRA ) has demonstrated excellent operational performance in 2023, allowing it to increase its full-year guidance again. Coterra now expects 7% more oil production and 5% more total production than initially expected, while capex is largely in-line with its original estimates.

Despite the strong operational performance, Coterra's projected 2024 free cash flow at current strip is likely to be under $1 billion now, down significantly from the $1.7 billion I had projected for it in August . Coterra only has around 25% of its 2024 production (both oil and gas) hedged with a combination of physical and financial hedges. Coterra's hedges also have floors that are generally around or only modestly above current strip prices, so its 2024 hedges only have around $50 million in positive value at current strip prices.

I now estimate Coterra's value at $29 per share, down from the $30 per share valuation I had for it in August. Coterra's strong operational performance enhances its value a bit as it should be able to maintain (or slightly) grow production with a lower capex budget. However, the significant decline in commodity prices (combined with its limited hedges) results in a sharp reduction in Coterra's projected 2024 free cash flow.

Despite the $1 decrease in its estimated value, I am upgrading Coterra to a buy based on valuation as its share price has gone down by $4 since August.

Recent Results

Coterra Energy's Q3 2023 production exceeded expectations. It produced 670,000 BOEPD (2% above the high end of its guidance), including 91,900 barrels per day in oil production (1% above the high end of its guidance). This allowed it to generate $250 million in free cash flow during the quarter.

Coterra's excellent Q3 2023 results allowed it to increase its full-year production guidance for 2023 to a new guidance range of 655,000 to 665,000 BOEPD. This is a 3% increase (at midpoint) from its previous guidance and a 5% increase compared to its original guidance.

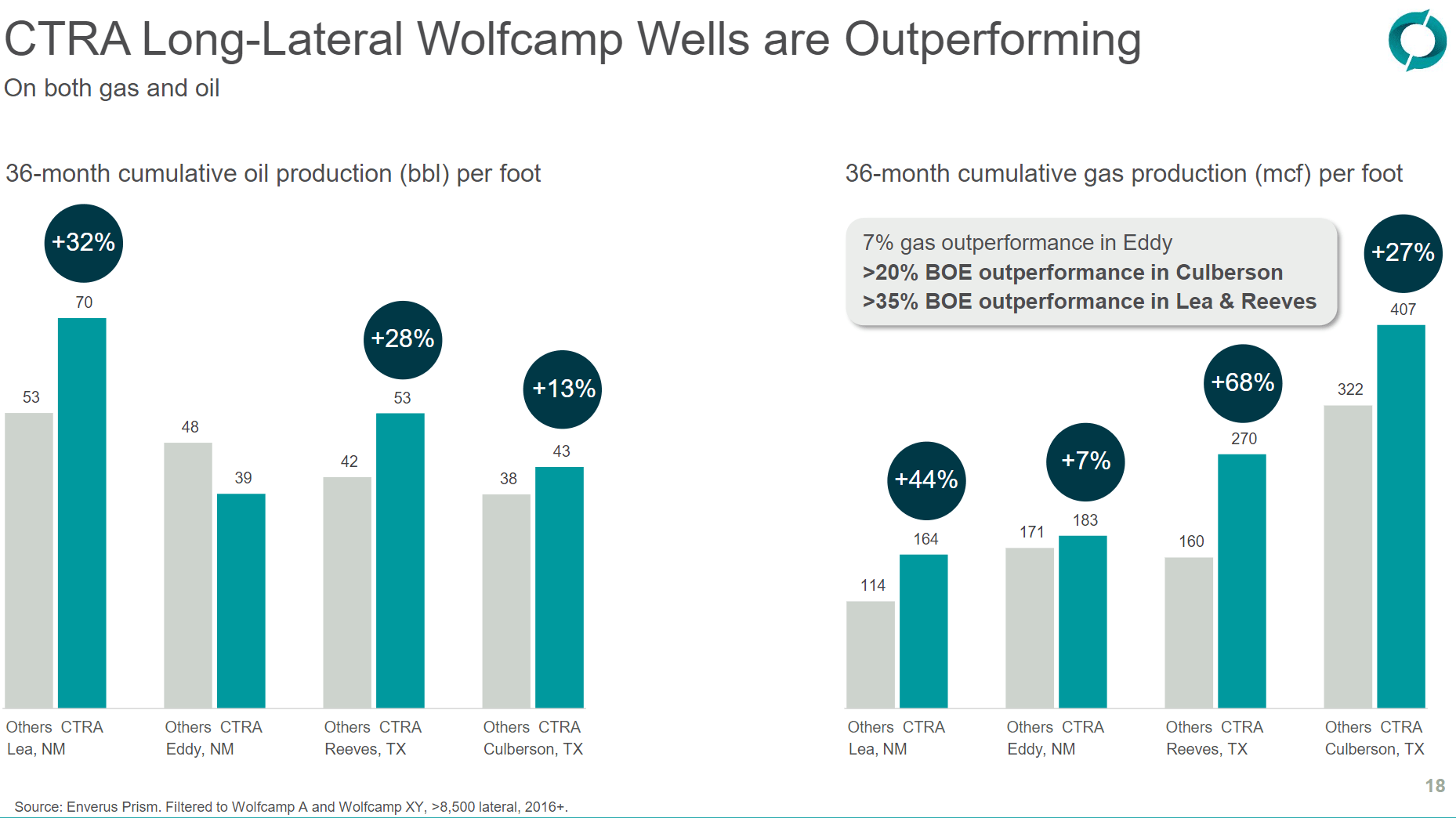

Also, Coterra now expects 94,500 to 95,500 barrels per day in 2023 oil production. This is a 3% increase from its previous guidance update and a 7% increase from its original guidance. Coterra has highlighted the outperformance of its long-lateral Wolfcamp wells as a significant contributor to its strong results.

{kind=link}

Coterra is achieving this with capex that is within its guidance range of $2.0 billion to $2.2 billion, although it expects to end up a bit above the midpoint of that range at approximately $2.12 billion to $2.15 billion.

Coterra expected 2023 free cash flow of approximately $1.3 billion based on strip prices in early November, suggesting approximately $380 million in Q4 2023 free cash flow. Given the deterioration in oil and gas prices, I believe Coterra is more likely to end up with around $1.2 billion in 2023 free cash flow, including around $280 million in Q4 2023.

Hedges

Coterra added some hedges in October 2023, but at last report it still has a relatively modest amount of 2024 hedges. Based on Q4 2023 production levels, Coterra has around 11% to 12% of its 2024 natural gas production hedged with a floor of $3.00 for Q1 2024 and $2.75 for the remaining quarters of 2024. Coterra also uses physical natural gas hedges, which are expected to cover a fairly similar percentage of its natural gas production.

Coterra also has approximately 25% of its 2024 oil production hedged with a floor price averaging in the mid-to-high $60s.

Estimated Valuation

Coterra was previously looking for 5+% oil production growth per year and 0% to 5% natural gas production growth per year during the near-term. Given that the 2024 strip is now around $70 WTI oil and $2.55 NYMEX gas, I'd expect Coterra to reduce development activities a bit though, probably more on the natural gas side.

Coterra's free cash flow is likely to end up below $1 billion in 2024 at current strip unless it significantly cuts capex and allows for some production declines. I do have a more favorable long-term outlook on commodity prices though and thus am only reducing Coterra's estimated value by $1 per share to a new estimated value of $29 per share.

Conclusion

Coterra has demonstrated strong operational performance, resulting in it generating 7% more oil production and 5% more total production than initially expected for 2023, despite an unchanged capex budget. Despite its strong operational performance, Coterra's projected free cash flow has been reduced due to weak commodity prices and relatively limited hedges.

Coterra expected $1.3 billion in free cash flow in 2023 in early November. I now believe it will end up at $1.2 billion in 2023 free cash flow. Coterra's 2024 plans are not finalized, but it is now likely to end up with under $1 billion in 2024 free cash flow with NYMEX gas strip at only $2.55.

Despite its weaker near-term free cash flow prospects, Coterra's improved capital efficiency puts it in a good position in future years. Thus I now consider Coterra to be a solid value given its $24 to $25 current share price, and my estimated value of $29 per share for it.

For further details see:

Coterra Energy: Strong Operational Performance, But Limited Hedges Against Falling Gas Prices (Rating Upgrade)