CTRA - Coterra: Management Remains Defensive Despite Outlook

2023-05-17 07:45:00 ET

Summary

- Coterra's management has scaled back operations, as the economic outlook dims.

- Oil prices and natural gas prices could be heading up due to the base effect from Chinese demand, and lower Russian gas production.

- CTRA stock has value for investors willing to hold.

Investment Thesis

Coterra’s ( CTRA ) stock has continued to retrace in recent times, despite significant revenue increases in 2022. The retracement has largely been a result of natural gas, and oil prices coming down off of their highs in 2022, and the increasingly uncertain future the energy market faces.

Coterra should see revenue decline slightly in 2023, but the company's future may be brighter than investors believe, as multiple themes play out, but mainly: a possible increase in natural gas and oil prices in the second half, as conditions improve for both commodities and secondly, which would then be likely followed by an increase in output from Coterra owing to the company’s high-quality resources. The further mitigating effects of the improved output should help revenue remain around current levels for the year, and this means with the current valuation Coterra could be a value play.

Commodity Prices Outlook

Oil prices have been affected by two big themes firstly, recession fears, and secondly, inventories and supply.

Recession fears: remain a strong theme throughout the year, with the latest results showing that the U.S. economy continues to remain weak through the first quarter, as growth slowed down to 1%, as inflation and high-interest rates affected overall economic activity. Global outlook also remained weak, and this led to oil prices declining by 4%, for the time being. Should the global economy continue to slow, which is likely, oil demand which stood at 100.8 million BP/d in December 2022 , will likely be the base case in terms of demand, largely as China re-opens, and emerging economies, help demand along. Therefore assuming 101 million BP/d of base demand for 2023 on average, if not more, oil prices might have found a bottom for now.

For now, the EIA is forecasting that demand is expected to grow by 2.6 million BP/d up from the 710,000 BP/d previously forecasted, with demand rebounding in the first quarter of 2023. Meanwhile, OPEC+ decided that it will cut oil production by 1.2 million barrels in order to offset the potential decline in demand . This would mean that oil production despite record production from the US, is likely to fall below 100 million barrels per day in 2023 .

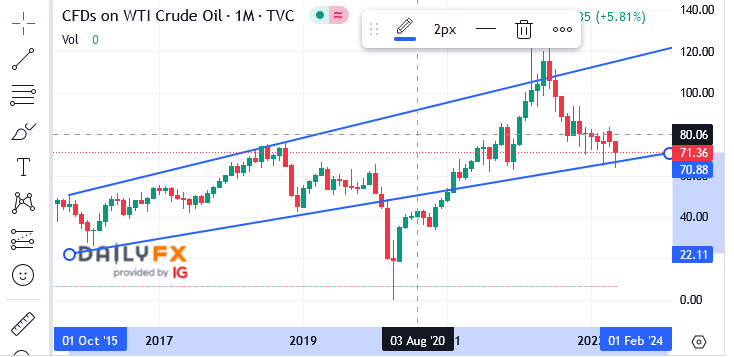

This has led EIA, to forecast oil will head towards $100 a barrel, but with oil inventories continuing to decline oil prices could head to $115-$120 if a breakout occurs, in line with the current technical channel . (See image below)

{kind=link}

Meanwhile, natural gas, which is far more dependent on weather has a brighter outlook with a dryer, and hotter summer due to El Nino, and subsequently a potentially colder wetter winter. With the Ukraine war expected to continue and natural gas supplies still sparse, prices could be heading up as and, investors expect inventories and supply to balance out. As a result, natural gas prices could potentially hit $3-4, in the near future, which is what the EIA's expects, despite the short-term bearish technical outlook.

Inventories and Outlook

US oil inventory remains an important indicator, of where oil prices might be headed and it continues to see drawdowns, as shale has continued to struggle in recent times, as rising interest rates weigh on production. Despite record output, many shale producers are likely to cut back on production and remain cautious, mainly due to historical precedent, where low prices previously led to many shale producers going out of business.

Coterra like other shale gas players has been slowly reducing its production , firstly with a reduction in natural gas from 203 to 193 BCF, in the Marcellus Shale, which is its largest source of production. On the other hand, Anadarko and Permian both witnessed an increase in both shale and oil production slightly. Overall, production came in at 635, BOE (barrel oil equivalent) per day, a slight increase over the previous year.

Management is clearly waiting to see where oil prices head, and remains circumspect like many competitors, about the future. Oil prices and natural gas prices are likely to rise, but the timeline remains uncertain, with a number of factors at play.

A Further Look at Production

Management is clearly remaining cautious into 2023, as currently projects a $2.1 billion capital expenditure outlay, 20% above 2023 levels, mainly as inflation continues to affect costs. Management will likely continue to wait to see if the price of oil and natural gas rises before they take any clear steps to increase production.

Considering the broader market dynamic an increase may come later this year, with management updating its production outlook, but for now expect lower output, as it looks to curtail costs on a bearish outlook. Yes, the bearish outlook might be overdone, as demand remains strong, despite economic uncertainty, but considering how capital-intensive shale can be, management may not be willing to commit more than is needed until prices are more stable and higher.

Investor Relations

Furthermore, as previous contracts roll off, revenue may actually worsen, especially since the average realization price for natural gas was $5.34 when the company was hedged. Considering that oil prices are significantly lower than they were previously, there could be significant revenue reduction during the current timeline.

Hedges Run-Off (Investor Relations)

Taking a Look At Coterra's Financial

With capital expenditure at $2.2 billion and Coterra likely to see natural gas revenue decline by 50%, in the near term, the company's finances aren't looking great for now. This is based on the average price realized in 2022, which was $5.8 versus the current price of $2.35. Considering natural gas revenue is likely to decline by 50%, and oil revenue is likely to decline by 20%, for now, the situation is not ideal.

Coterra faces a plethora of risks, including the increasingly slowing global economy, and further deterioration of commodity prices, as demand slows. A slowing economy and rising interest rates tend to also make the dollar stronger, which itself could weigh on the price of oil and natural gas, thereby further putting downward pressure on revenue.

Coterra's current valuation remains relatively moderate as investors take stock and is increasingly reflective of the global risk that stems from a slowing economy and a recessionary outlook. Adding to the negative sentiment issue of Coterra's own defensive stance. As mentioned should prices remain at current levels, revenue could decline significantly this year, and this could lead to profitability coming in much lower than previously expected. Especially as hedges roll off, and no long cushion lower energy prices, management will remain reluctant to 'bail out' investors.

Current forward P/E estimates are around 10-11x if you were to project out based on current energy prices. Should natural gas prices head upwards, owing to improved conditions, we could see revenue rebound, and forward P/E could be potentially move closer to 8-9x, assuming EIA's forecast of $3.40 is more or less correct in the medium term. Meanwhile, if oil prices were to similarly head up, that could further fall to 6x, at which point the stock price could quickly head back up, as valuation would be quite cheap.

But, currently, the price reflects lower levels of cash flow, and therefore, the dividend, which currently stands at around 8%, is likely heading lower. Free cash flow came in $3 billion in the 2022, with $5 billion from operations, and $1.9 billion paid in dividends. Cash flow in 2023, provided prices head nowhere, is likely to be around $2.5-3 billion, which means the dividend payout could be closer to $500 million, which is significantly below last years, and that would send the dividend closer to 2%.

Investors who want a company that has strong long-term prospects should take a look Coterra, but the short term outlook remains tough. The company is well managed, and there no major risks such as debt, which currently stands at around, $2.5 billion, but until the outlook improves, the stock price likely remains, remains rangebound. Things could change later on this year, once the conditions improve, so it's clearly a buy and hold situation with Coterra.

For further details see:

Coterra: Management Remains Defensive, Despite Outlook