CTRA - Coterra's Shift Towards Oil Should Lift Shares

2023-12-07 02:59:22 ET

Summary

- Coterra Energy has a strong asset base and is focused on growing oil production, which is a medium-term positive.

- Lower natural gas prices have been a headwind for the company, but hedges should limit downside while higher oil production boosts cash flow.

- The company is allocating its capital budget to oil and expects to continue to generate free cash flow, with a commitment to return at least 50% to investors.

- Given low debt, shareholder returns should exceed this benchmark.

Shares of Coterra Energy ( CTRA ) have been dead money over the past year, losing about 3% despite the higher market level. Lower natural gas prices have been the primary headwind, but the company is focused on growing oil production, which I view favorably. Coterra came about from the merger of Cabot and Cimarex in 2021, and as a result, the company has a fantastic asset base, resulting in strong capital efficiencies. I view shares attractively given its asset mix, cash flow, and stellar balance sheet.

{kind=link}

In the company’s third quarter , Coterra earned $0.50, beating consensus by $0.07. This was down from $1.42 in 2022 as revenue fell by 46% due to a significantly weaker market for natural gas. Natural gas realizations were $1.80 before hedges in Q3, down from $5.49 last year while oil was $80.80 from $98.78. Hedges provided $0.21 of uplift to natural gas.

Last year, natural gas surged as investors anticipated a significant shortage following Russia’s war on Ukraine. However, Europe managed through the winter better than many feared, which has helped to normalize prices. It is also important to note that, unlike oil, natural gas is priced primarily based on local market conditions, rather than as one global market. There is limited LNG export and import capacity around the world, with liquefication costly and tankers scarce.

While LNG can certainly marginally impact prices, because a producer cannot route all of their production to the export market, wide differentials in natural gas prices around the world can persist. The International Energy Agency does expect natural gas demand to grow globally in coming years, but most of this demand growth comes from overseas with North American demand forecast to fall slightly. This is likely to limit natural gas appreciation in my view, and all else equal, producers like Coterra would prefer if demand growth were coming domestically rather than internationally.

IEA

Conversely, by 2028, the International Energy Agency (IEA) expects global oil demand to be about 5.5% higher than it was in 2022. While this is actually somewhat slower than global gas demand growth, I have more confidence in this boosting the fortunes of US energy producers because oil is priced much more globally. The location of demand growth is far less relevant. This is why, in general, I prefer E&P companies that are focused on oil rather than gas.

Coterra operates out of the Marcellus, Permian, and Anadarko plays with 51% of revenue coming from oil, 36% natural gas, and 13% NGLs. I view the majority oil mix positively. Based on where CTRA is growing production and allocating capital spending, it seems to share my preference for oil, and I expect oil’s share of production, and likely revenue, to continue to rise over time. In the last quarter, production was 670mboed (thousands of barrels of oil equivalents per day) vs the 625-655mboed guidance, with both oil and gas volumes exceeding consensus. As a result, management expects full-year production of 655-665mboed, coming above the high end of its previous 630-655mboed guidance.

Better-than-expected production is generally positive, but this is particularly the case because it is coming even as it held cap-ex guidance flat at $2-2.2 billion. CTRA is spending the same amount but getting more energy out of the ground more quickly, improving per unit economics. We are still only two years into the combination of the company, and as a result, I think we continue to see management finding new efficiency and optimization opportunities. As a result, cap-ex spending is down to about $8.75-9/mboed while growing production. Coterra is generating 5% per foot cost improvements on its drilling activity, a reason why it has been able to keep cap-ex spending flat.

Based on its full-year guidance, Q4 production should be 645-680mobe/d, up 5% from last year with oil production up 9% sequentially and 10% from last year. Faster oil growth is a definite positive, given stronger margins here. I expect this to continue. It has seven rigs in the Permian, which is more oil intensive, with just two in the Marcellus, where natural gas dominates production. CTRA is allocating its capital budget to oil.

In fact, management expects to continue to spend about $2.1 billion in cap-ex in 2024 and 2025. This should grow production by 3-5% companywide. Management is able to hold cap-ex flat because it can reduce gas-focused cap-ex in the Marcellus by $200 million and keep production flat there. This will continue to shift production gradually towards oil and away from gas. The company has 15-20 years of economic inventory with the Permian having the longest reserve life at 25 years, meaning it can continue with this strategy for quite some time.

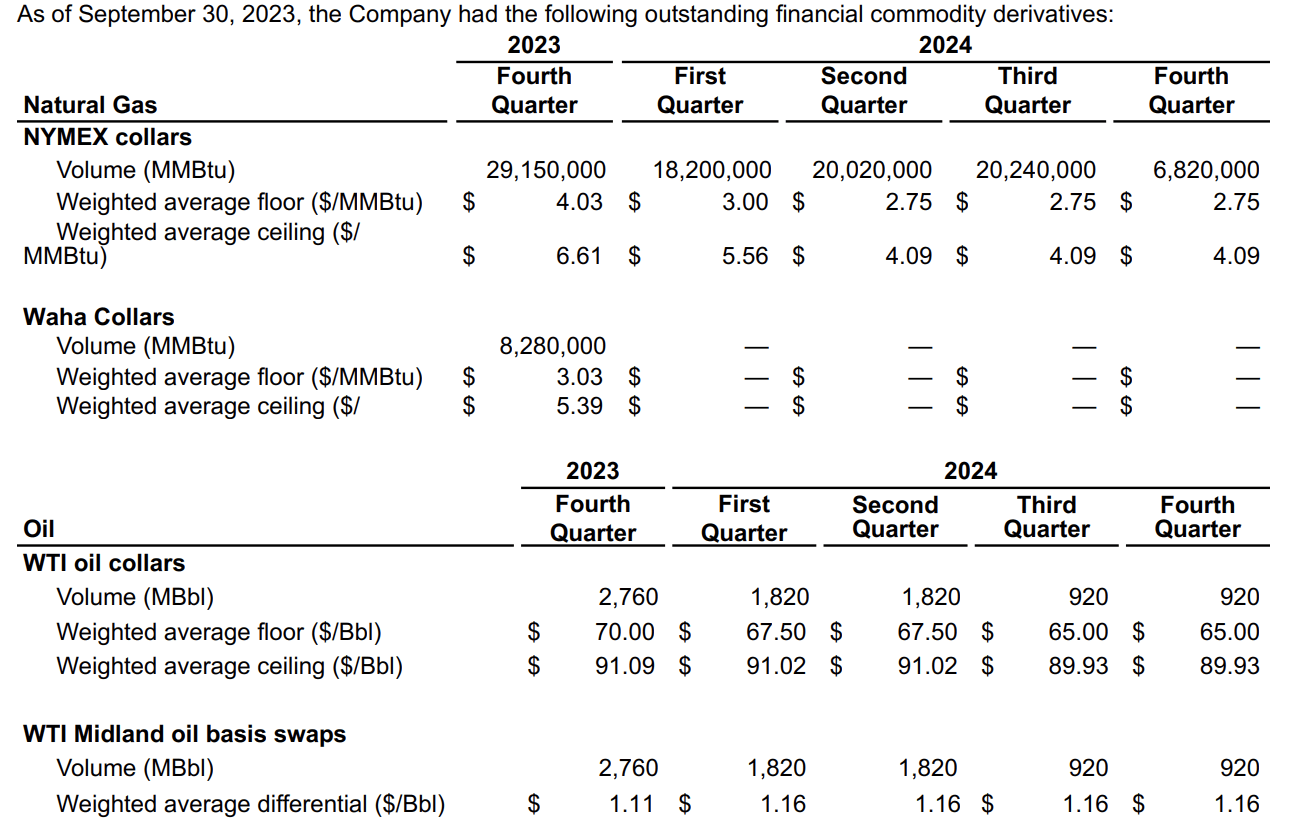

Additionally, management has hedged some 2024 production to limit its exposure to a further downdraft in natural gas prices. It has also been adding to its 2024 hedges at a $2.75-3.00 floor for natural gas next year subsequent to last quarter end, which should keep results in 2024 at or above Q3 levels. Additionally, 28% of Q4 gas production is hedged as is 30% of oil

{kind=link}

Due to this production growth, and productive cap-ex, Coterra generated $250 million in Q3 free cash flow, for about $900 million year to date. That positions the company to generate $1.3 billion in free cash flow this year, from $3.9 billion last year, given lower natural gas prices. Now with its free cash flow, management has committed to return at least 50% of free cash flow to investors; so far this year, it has returned 91%, and it will likely finish the year north of 80%.

CTRA pays a base $0.20 quarterly dividend, which gives shares a 3% yield. This dividend is set so the company has excess free cash flow even at $50 oil and $2.50 natural gas. Beyond this, the company can do variable dividends when commodity prices are very high, as it did last year, or otherwise buybacks. It has a $1.6 billion share buyback authorization. There were $60 million in buybacks in Q3 and $380 million this year.

Thanks to these repurchases, its share count is 5% lower than last year. Combined with 5% production growth, CTRA is growing production 10% per share, an attractive pace of growth that should support increase in per share capital returns over time. Management has said it will not raise its capital return commitment above 50% of free cash flow because it values flexibility. However, its actions speak loudly, returning 80%. I expect returns to stay well above 50%, simply because it has limited other uses for cash.

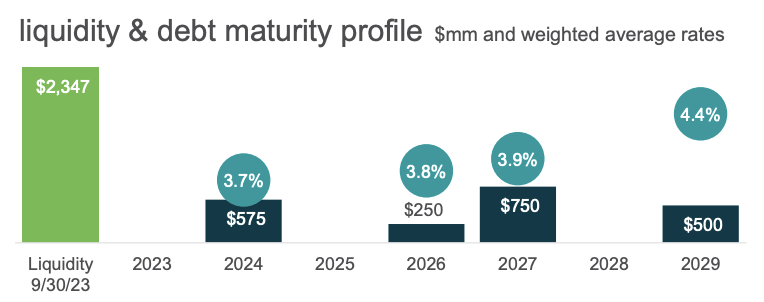

The company targets less than 1x net debt to EBITDA with $1 billion in cash on hand to ensure secure investment grade ratings. Well, it has $847 million of cash already. Additionally, it has just 0.3x leverage currently given gross debt of $2.2 billion and net debt of $1.6 billion. Management may choose to pay down some 2024 debt rather than refinance it entirely next year, but it already has brought debt to where it wants it to be.

{kind=link}

I do not expect material debt reduction from here, just given how low it has brought debt. Absent retaining cash or paying down debt, the only other large potential use of free cash flow is M&A, but CTRA said on the last earnings call it is not looking at large scale M&A. We could see small bolt-on acquisitions to deepen its exposure to the Permian, but with its large inventory life, there is no pressing need to do a deal.

This is why I believe we have seen nearly all free cash flow go to capital returns this year. With net debt so low and no need for M&A, as it harvests gains from its own merger, there is nothing to do with cash flow other than to return it to equity investors. I expect this to continue in 2024 and beyond.

With 5% production growth and flat cap-ex, free cash flow should be about $1.3-$1.5 billion next year, assuming oil is around $80 and natural gas stays between $2.60 and $3.20. That gives shares about a 7% free cash flow yield, even in this fairly weak natural gas environment, which I conservatively assume persists. With more production shifting towards oil, free cash flow should rise somewhat faster than production over the coming years. Given 3-5% production growth and favorable mix shift, CTRA is poised to generate 5-8% free cash flow growth over the next few years, at stable prices, which on top of a starting 7% yield is attractive. Given nearly all free cash flow should flow to stockholders via dividends and buybacks, this can provide 12-15% medium-term returns. I view shares as attractive, given that return profile, and a be buyer at current levels, with shares likely to get back above $30 over the next twelve months.

For further details see:

Coterra's Shift Towards Oil Should Lift Shares