CTRA - Coterra: Why The Variable Dividend Cut Isn't Necessarily A Bad Thing

2023-05-09 11:38:47 ET

Summary

- Low breakeven costs and a large reserve in the Permian basin sets Coterra up for success even in a recession.

- The variable dividend was cut, but in return, it allows the company to be more nimble in the face of tough market conditions.

- The base dividend remains very sustainable, with dividend increases on the horizon.

Thesis

Right now the economy could be teetering on a precipice, depending on your point of view. We may narrowly escape a recession and find the soft landing as the FOMC suggests, or we may dip into the recessionary end of the pool and see GDP in the negatives this year.

No matter your personal belief, I think we can all agree that growth will certainly slow this year and, if you read my previous article on oil prices, we'll likely see some depressed energy pricing as a result. Positioning ourselves prior to this move is important.

I'm a dividend investor, and I try to cater to other dividend focused investors, so in this article we'll explore Coterra Energy (CTRA). They have significant exposure in the lowest breakeven cost basin in the country, and we'll see how that benefits them, and how they could keep paying their base dividend even in a recessionary environment.

They've been positioning themselves to weather a potential market downturn, and this demonstrates fantastic leadership - even in the face of upset investors who only care about the yield. They recently cut their variable dividend and substituted it with share buybacks in its place, and we'll get into that. We'll talk about why they did it, and how they're going to honor their commitment to return at least 50% of free cash flow to investors.

That dividend cut allows them to be incredibly nimble in this coming, potentially tough, market environment. If there's an upstream producer that can weather this, CTRA will do quite well. Now let's get into it!

Company Overview

Coterra Energy is an energy production company based in Houston, TX with natural gas, natural gas liquids, and oil exposure. The company is the result of Cabot Oil & Gas and Cimarex Energy coming together to form Coterra Energy, and the company just celebrated its first year in business operating together under that name. Coterra primarily operates in three key areas - the Permian Basin, the Anadarko Basin, and Marcellus Shale. The company holds a deep inventory of high-quality development projects with an industry-leading cost of supply.

The combination of both companies provides access to a network of assets and infrastructure that help create scale and vertical integration throughout the market - helping to drive down break-even pricing, lower cost and higher return inventory that spans multiple decades, and capital optionality. Coterra's commodity and asset diversification helps mitigate cash flow volatility and support long-term value creation. I also believe the company has excellent leadership as it demonstrated by merging companies and its diverse shale play integration to shield itself from recession worries.

The following is a very important excerpt taken directly from the 2022 Annual Report that I think investors should read. This foresight is exactly what investors should want to see in company leadership:

"We operate in a cyclic commodity price environment in which cycles can be unpredictable and severe. Flexibility is the coin of the realm. With our fortress balance sheet, asset quality, and organizational capability, we can quickly adapt to changing conditions. Although we are not insulated from the effects of market swings, we have the intrinsic ability to adapt in a manner that few can replicate."

According to their Q1 2023 Investor Presentation corporate breakeven pricing for Coterra Energy sits at $45 for WTI and $2.25 for Henry Hub. This means that the price of WTI crude oil needs to be over $45 to be profitable and natural gas prices at Henry Hub need to be over $2.25 to be profitable. Those are two very realistic and favorable breakeven prices compared to the company's peers in other less desirable shale plays.

Operations

Permian Basin

The Permian Basin is one of the oldest oil & gas producing basins in the United States. Coterra has a core acreage position of 307,000 net acres located in the Delaware Basin region which spans across West Texas and Southeast New Mexico. Production levels in 2022 were around 211 MBOEpd with year-end reserves of around 691 MMBOE. The company's production was approximately 66% liquids and 34% natural gas. Investors should note that the Delaware Basin has the lowest breakeven pricing of any shale play in the United States at $46/barrel, making this a favorable geographic area for production.

Marcellus Shale

The Marcellus shale is found in the Appalachian Basin and Coterra's operations in the region are primarily concentrated in northeast Pennsylvania. The company holds approximately 183,000 net acres in the dry gas window of the play. Production levels in 2022 were around 2,204 MMCFpd of natural gas, with year-end reserves totaling around 1,498 MMBOE. The company's position in the Marcellus Shale is 100% natural gas.

Anadarko Basin

The Anadarko basin has produced more oil than any other area in the United States since the first oil discovery in 1892. The mid-continent region is where Coterra's assets are primarily located. The company holds an acreage position of approximately 182,000 net acres. Production volumes for 2022 were at approximately 55 MBOEpd with year-end reserves totaling around 209 MMBOE. The company's position in the Anadarko Basin is around 46% liquids and 54% natural gas. One thing investors should note is that breakeven pricing for the Anadarko Basin is around $66 per barrel, the highest breakeven price among the major U.S. shale plays.

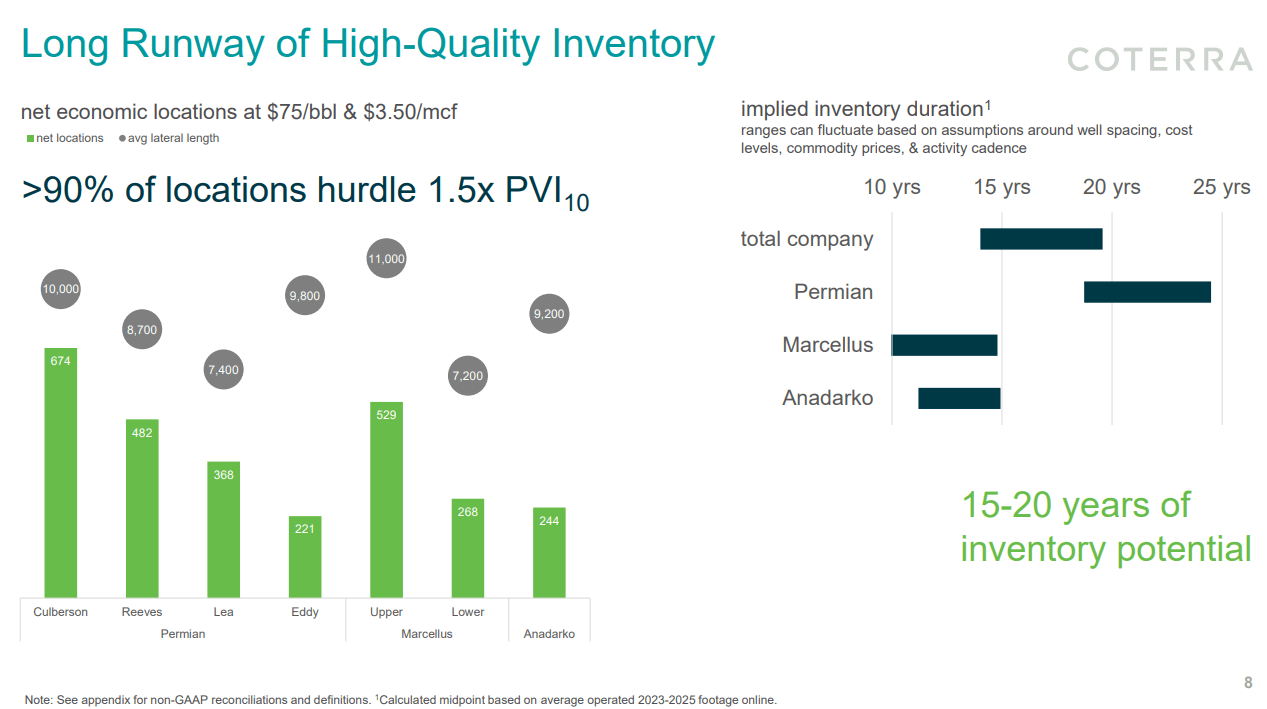

Longevity

CTRA has some serious reserves available in their current acreage, and thankfully most of it is in the low priced Delaware section of the Permian basin.

{kind=link}

Investors getting in now, and looking at the low breakeven pricing, don't need to worry about the company running out of available land to develop and produce from any time soon with anywhere from 18 - 24 years of reserves in the Permian.

Returning Value to Shareholders

The big kerfuffle about CTRA is of course about cutting their variable dividend. According to their Q1-2023 conference call transcript they're replacing their variable dividend with share buybacks as they prioritize returning value to shareholders through buybacks over dividends due to market conditions and the value proposition they see in their business.

They have announced a $2 billion share buyback program, which based on their current outlook can be executed over the next 18 to 24 months. They believe that share repurchases are the best way to return value to shareholders and are committed to returning 50% or more of free cash flow to shareholders.

They may supplement with variable dividends if needed to reach the minimum threshold but are prioritizing share buybacks. This change in strategy comes after conducting intensive study and debate about the macro environment they find themselves in, investor feedback, and their viewpoint on a looming global supply demand imbalance. They also see an opportunity for acquisitions at their current market valuation.

So, is it good for shareholders? I think so. Read on. I love to see companies buying back shares, and I love variable dividends. Especially in oil. Preferably I want both, but sometimes we can't have our cake and eat it too.

The way I read this is that they want to conserve capital in case we see a downturn - that's what they mean by the macro environment and market conditions. If we see a downturn they don't want to be expected to pay variable dividends, and can instead repurchase shares at their leisure.

Now this isn't necessarily a bad thing, like I said. The company wants to remain nimble. In that 2022 Annual Report they said "Flexibility is the coin of the realm." Read that letter to shareholders, because it explains a lot of their philosophy.

I don't view cutting the dividend as a bad thing here. The company can still return value by purchasing shares, and they restated when they announced the dividend: "We reiterate our commitment to return 50%+ of Free Cash Flow to shareholders, with an emphasis on the base dividend and buybacks, in the near-term."

This is further echoed in the 2022 Annual report in the shareholder's letter where they stated, " Our commitment to growing our base dividend is foundational , and the significant increase signals long-term confidence in our business."

These statements lead me to believe that they're going to increase the base dividend further. Which would you rather have, a higher base or a variable? I want a higher base that's easily covered by FCF in terrible market conditions, personally.

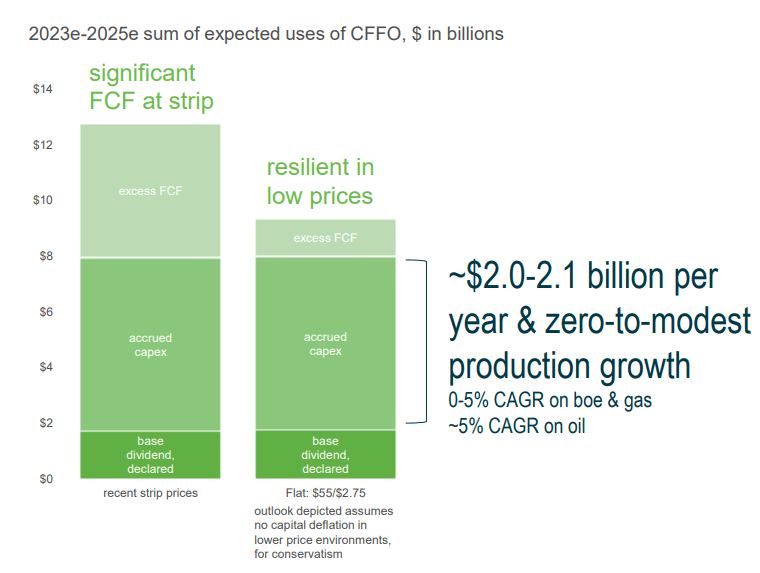

Chart depicting usage of FCF (Q1-2023 Investor Presentation)

{kind=link}

When we're looking at this company to see if they can keep that dividend flowing, since that's what we're interested in, we need to make sure that even at rock bottom pricing they can pay it. And with a breakeven of $45 on WTI to pay base dividends, they're good to go. At $55, as you can see in the chart above, they then have additional excess FCF.

I would be beyond shocked if WTI remained at $45 for any length of time, even in a nasty recession ending in negative GDP for the year (and considering Q1 GDP estimates that would be a whopper of a recession). But even there, they can pay the base dividend ( see slide 3, Q1-2023 investor presentation ). Right now it's yielding 3.19% at a 52% payout ratio.

Valuation

Valuation is a little hard to come to grips with here due to the merger, but let's look at the facts.

First, it's EV/Revenue and Price/book are both comparable to industry peers, according to Seeking Alpha. It's P/E is a little on the high side. Given it's forward revenue estimates, a little higher valuation is appropriate.

Secondly, that forward revenue estimate. Of course 2022 was a great year for oil profits, but let's see what they're estimated to do going forward:

| YEAR |

| 2022 (Actual) |

| 2023 |

| 2024 |

| 2025 |

| 2026 |

| REVENUE |

| $9.05B |

| $6.18B |

| $6.64B |

| $6.97B |

| $7.81B |

| YOY % |

| 74.6% |

| -31.69% |

| +7.36% |

| +5.07% |

| +12% |

Of course they're going to dip in 2023. Pretty much all producers will. But what's important here is that they continue growing after, and they're scheduled to grow at a great pace. Given how much of their capacity is in the cheaper Delaware basin it's no surprise that they'll continue to grow those profits.

Looking at their valuation multiples, their revenue estimates, and their industry positioning I think they're very fairly valued.

Conclusion

Coterra Energy appears well-positioned for near-term market uncertainty amid a looming U.S. recession. The combination of Cabot Oil & Gas and Cimarex Energy brings together a fleet of assets and infrastructure in three of the biggest shale plays in the United States. The company has a diversified product portfolio of oil, natural gas, and LNG that are located in diverse enough regions and shale plays that give the company flexibility and protection from commodity price drops.

While having a significant amount of the company's assets located in the most expensive shale play to drill in is a bit concerning among growing recession worries, the flexibility to shift back to the Delaware Basin in the Permian Basin with $46 breakeven pricing should ease your worries. The reason the company is focusing assets in more expensive shale plays is that there is a developing natural gas market and hub located near the Anadarko Basin. Coterra appears to be taking as large of a market share as possible as this area is expected to dominate natural gas demand growth in coming years.

Investors should be bullish on the future of the company and the resiliency of the company in the face of looming recession effects. Company leadership has strong forethought as evidenced by their acknowledgement of market conditions and positioning themselves to best come through unscathed, even if it makes investors upset in the short term.

The company appears to be committed to strong dividends, share buyback, and debt reduction as well. Coterra has demonstrated flexibility with the ability to focus assets on oil, natural gas, or LNG, in a combination of three of the most prolific shale plays in the country with varieties of breakeven pricing per commodity type. An overall tip of the cap to company leadership in Cimarex and Cabot, as together with Coterra Energy they have become industry leaders when it comes to breakeven pricing, along with a solidly located but diverse product portfolio.

That base dividend isn't going anywhere anytime soon and they have plenty of runway to keep raising it in the future. As dividend investors we love yield, but we also want to keep our capital from running away. Too often dividend investors chase yield and lose capital because the company was robbing Peter to pay Paul. I love seeing companies do this the right way and taking care of their long-term investors first.

I see CTRA as a fairly valued stock for the dividend investor who isn't rattled by short term volatility. I've got to give this one a buy recommendation. This is one stock I'm going to sock away in my IRA and in managed accounts and just watch the dividends roll in for years.

For further details see:

Coterra: Why The Variable Dividend Cut Isn't Necessarily A Bad Thing