COTY - Coty: A Deleveraging Story With Strong Momentum

Summary

- New CEO is transforming COTY after years of missteps.

- Fragrance sales have been strong across the industry.

- COTY is a strong deleveraging story.

Cosmetic and fragrance company Coty ( COTY ) is set to massively deleverage, as it benefits from a booming fragrance industry and its entry into the skincare market, where its new CEO has had much success. The company is generating a strong free cash flow (between $500-$600 million a year) and the sale of its remaining stake in haircare company Wella should take it down to about 2x leverage in the next couple of years, erasing the mistakes of former execs.

Company Description

Coty is beauty company with a portfolio of owned and licensed brands in the categories of fragrance, color cosmetics, and skin and body care. It also owns a 25.9% stake in haircare business Wella, which includes the brands Clairol, Wella, and OPI.

Among the well-known brands it owns are CoverGirl, Max Factor, Rimmel, Sally Hansen, Lancaster, and philosophy. It also has licenses with Calvin Klein, Gucci, Burberry, Tiffany, Lacoste, and Hugo Boss, among others.

Approximately 53% of COTY’s fiscal 2022 sales were from prestige fragrances, of which approximately 82% was from its top-six prestige fragrance brands. None of its top eight licenses are up for renewal before the end of calendar 2026, with the majority running longer than that and providing for renewal without licensor consent. Three other licenses are up for renewal in fiscal 2024.

Earlier Missteps

In 2016, COTY completed the purchase of P&G’s ( PG ) specialty beauty business for $12.5 billion. The acquisition doubled its revenue to $9 billion making it the third-largest beauty company in the world and the #1 fragrance company.

The deal was orchestrated by former CEO Bart Becht, who at the time was also one of the heads of COTY’s largest shareholder, JAB Holdings. Becht was a numbers guy more than anything and saw lots of synergies between the two businesses. However, both companies were struggling to grow at the time and Becht failed to embrace COTY’s luxury history, instead favoring the mass market.

As such, what was left in the aftermath of the merger was a highly leveraged company with dwindling sales. Brands, such as CoverGirl and Max Factor, bought from PG were in worse shape than COTY management had believed, as consumers continued to trend away from mass-market cosmetic brands.

Meanwhile, there became a revolving door at CEO. These CEOs did all have something in common, though, none of them had experience in the beauty industry.

New CEO, New Strategy

Enter Sue Nabi, who became CEO in September 2020. The executive worked her way up the ladder at cosmetics leader L’Oréal to head leading brands such as Lacombe and L’Oréal Paris before starting her own premium skincare line Orveda in 2014. Orveda was eventually purchased by COTY.

Nabi has already put her mark on COTY’s direction by repositioning its brands. On the mass-market side, the company is now successfully reaching younger audiences through TikTok and the use of influencers.

At the other end of the market, she’s repositioned the company’s sunscreen and skincare brand Lancaster, playing on the brand’s historic ties to the Monaco Royal Family and putting a more luxurious spin on it. Nabi also convinced Gucci and Burberry to expand their licenses from just fragrances to helping them launch new cometic lines as a springboard into China.

Nabi’s latest move is to tackle the skincare market, an under-penetrated area for COTY but one where she has had past success with her Orveda brand. At an event last month, COTY laid out plans to double its skincare revenue to $500-600M by FY2025, and further accelerate growth in FY26 and beyond. It also expects the growth to be gross-margin accretive.

COTY Investor Day

Debt Issues and Valuation

{kind=link}

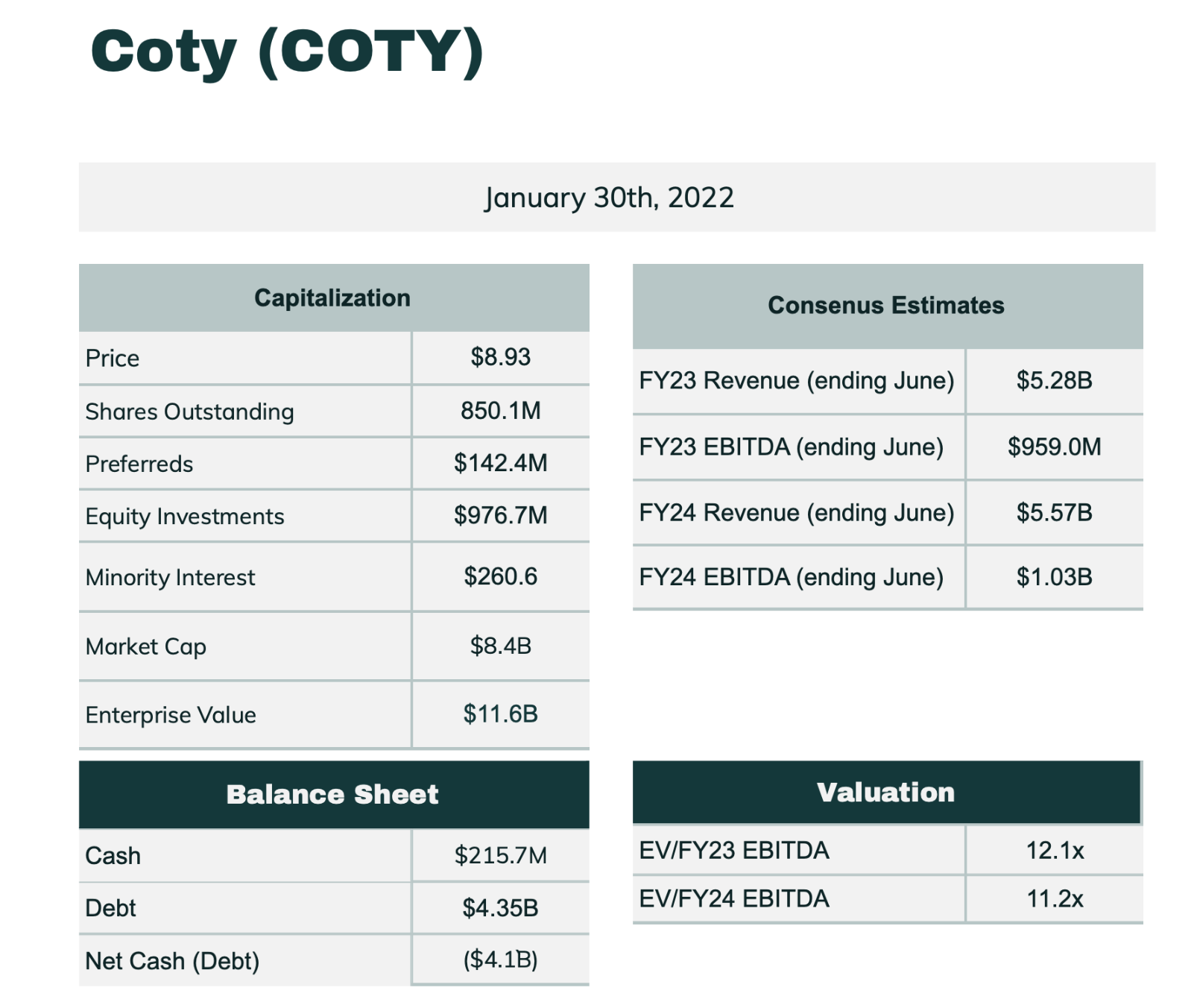

COTY has been trying hard to get out from under the pile of debt it was left with after the botched P&G Beauty acquisition. It ended last quarter with debt of $4.3 billion. It said it is on track to drop leverage to 4x by the end of calendar-year 2022.

The company is in the process of divesting its Wella business and it now owns a 26% stake, which it values at $800 million. It expects to divest the rest of its Wella stake by FY2025. Last fall, the company sold a nearly 14% stake in Wella to KKR in exchange for the redemption of convertible notes that KKR held. Earlier, COTY sold 60% of Wella to KKR in December 2020 for $2.5 billion.

In FY2021, COTY was able to wipe out the preferred stock owned by KKR, saving $77 million in annual dividend payments. The preferred shares had an interest rate of 9.0% annually.

The company is projecting leverage to drop to 3x at the end of CY2023 and 2x in CY2024. With projected FCF of ~$500-$600 million a year, plus the remaining sale of Wella ($800 million), the company is well on its way to accomplishing these targets. A $2 billion reduction in debt and $1 billion in EBITDA gets them there.

Trading at 12x FY23 EBITDA, COTY currently trades at a big discount to peers because of its elevated leverage and past issues. That’s a big discount compared to other beauty peers. e.l.f. beauty ( ELF ), for instance, trades at ~31x FY‘23 EBITDA (ending March), while Estee Lauder ( EL ) is valued at ~30x fiscal ’23 EBITDA (ending June). Fragrance company Inter Parfums ( IPAR ) has a multiple of ~19x ’23 EBITDA, while cosmetic retailer Ulta Beauty ( ULTA ) is valued at ~15x FY’24 EBITDA (ending January).

Once COTY is able to get its leverage down, the stock should be able to re-rate higher. COTY is projected to grow revenue MSD in FY24, slightly below IPAR and ULTA. EL, which trades at a much higher multiple, just projected -2% to flat sales for FY2023 due to its Chinese exposure, which COTY does not have.

Here is what a de-levered COTY multiple would look like with the stock at $16.

| COTY |

| Price |

| $16.00 |

| Shares outstanding |

| $850,112,500 |

| Market capitalization |

| $13,601,800 |

| Equity Investments |

| $176,700 |

| Cash |

| $215,700 |

| Preferred |

| $142,400 |

| Debt |

| $2,345,500 |

| Min Interest |

| $260,600 |

| Enterprise value |

| $15,673,100 |

| FY24 EBITDA Consensus |

| $103,400 |

| EV/FY24 EBITDA |

| 15.1x |

| FY24 Rev Growth Consensus |

| 5.5% |

| Leverage |

| 2.1x |

Opportunities

As presented above, COTY is well on its way to meeting its leverage goals, and it should be a $16 stock just by re-rating to the low-end of its peer multiple given its similar growth rate to its peers. This is the most important thing the company can do, but it must be done conjunction with an improving, growing business.

Two areas where COTY really lacked were skincare and exposure to China. However, these are two areas where Sue Nabi is really going after.

Nabi has a strong background in skincare, having run the unit at market leader L’Oréal, and through founding her own successful luxury skincare company. Skincare has been one of the most consistent growing areas of beauty for a while, so I really like this strategy.

Being underexposed to China during a period of COVID lock-downs has been a good thing for COTY. In fact, EL issued weak 2023 guidance because of its exposure to China. However, with China slowly reopening, now is a good time to start to put more emphasis on the country.

Discussing China at Deutsche Bank Conference in June, Nabi said:

“So for us, it's going to be the growth, growth, growth in China, very profitable growth. The gross margin of our Chinese business is 10% or more higher than the one of the average company. So it's going to be a very, very profitable growth for the coming quarters and coming years. And last but not least, something new versus this discussions we had about China and Coty in China just a few months as a go, is that the fragrance business is the $3 billion opportunity in this market. And we've seen that if we have our fair share, it's a $200 million business extra for us. So super confident in China, honestly.”

Fragrance, meanwhile, has become one of the hottest categories in beauty since the start of the pandemic. Lipstick and cosmetics have long been known to perform well during recessions, but it was fragrance sales that did well during Covid. This can be seen in the numbers of all the major fragrance players

Most recently, IPAR pre-announced very strong fragrance sales in both Europe and the U.S. showing a continuation of this trend. Its fragrance sales grew 47% year over year in Q4. EL, meanwhile, saw double-digit fragrance sales at its Estée Lauder, Tom Ford and Le Labo brands. For its part, COTY said it was seeing sell-outs when it issued its Q4 guidance.

In an interesting move, the company also entered a swap agreement with several banks to lock in a $200 million buyback program at prices below $7.50. The buyback program is planned for CY2024. With the stock trading over $10, this looks like it will be a prudent move.

Risks

The biggest risk to COTY remains its hefty debt load, and investors saw rival REV file for bankruptcy this year. While leverage has come down, the company is not out of the woods yet. It has a lot of debt at some pretty attractive interest rates due in 2025 and 2026. FCF and the full disposition of Wella should make a serious dent, but the company needs to continue to execute.

COTY is also still controlled by its largest shareholder JAB, which owns about 54% of the company. They historically have gotten too involved with the business and done a poor job in the process. However, they are paying Nabi some serious cash giving her a $3.5 million base salary and over 20 million RSUs (restricted stock units). My guess is with that pay package they are going to left her run with her vision for the company and not get involved.

Conclusion

First and foremost, COTY is a deleveraging story and the company is well on to hitting its 2x leverage target. Meanwhile, CEO Sue Nabi has already shown that she is in the midst of turning the company around, retaking market share. Nabi is an experienced beauty-industry vet who has both run major brands as well as her own company, not one of the consumer staples execs the company has trotted out in the past. Her early results speak for themselves.

Coty Investor Day

At the same time, the company's skincare and China push make a ton of sense, and the company is back to innovating and marketing instead of simply looking to cut its way to profits.

Despite all the positives, the bitter taste of past mistakes leaves the stock as the cheapest in the sector. Given its debt load COTY does carry risk, so it’s not for the risk adverse. However, the company is riding strong industry trends and the deleveraging projections are on track. I see upside to $16 and beyond for the stock.

For further details see:

Coty: A Deleveraging Story With Strong Momentum