EL - Coty Continues To Deliver Strong Results In Q4

2023-08-24 14:30:39 ET

Summary

- Coty reported strong fiscal Q4 results, with a 16% increase in sales and a 17% increase in like-for-like revenue, topping analyst estimates.

- The company's deleveraging story remains on track, with leverage down to 4.1x.

- COTY is shining when other rivals such as EL have run into some issues.

With "Strong Buy" rated Coty ( COTY ) recently reporting earnings, I wanted to catch up on the name. The stock is up over 11% since my initial write-up , but down about -15% since I upped my target price in July .

Fiscal Q4 Results

COTY reported fiscal Q4 results recently, seeing a 16% increase in sales to $1.35 billion. Like for like ((LFL)) revenue soared 17%, as the company saw a -1% currency headwind. The revenue results beat the analyst consensus of $1.31 billion.

Management attributed the strong sales to robust global beauty demand across categories, geographies, and channels.

Adjusted gross margins came in at 62.8%, up 70 basis points. The improvement came from pricing, mix, and supply chain productivity.

Adjusted EBITDA for the quarter soared 60% to $105.1 million from $65.1 million a year earlier. Adjusted EPS came in at 1 cent versus -1 cent a year ago and missed analyst estimates of 2 cents.

In the Prestige segment, revenue climbed 21% (21% on an LFL basis as well), to $799.6 million. Adjusted EBITDA for the segment jumped nearly 43% to $112.7 million.

The company said it saw double-digit growth in both the Americas and EMEA, and that China sales were up 15% versus 2 years ago, and up 2x year over year. Travel retail, meanwhile, grew revenue 30% year over year on an LFL basis. It also noted that retail inventory was at healthy levels entering its most important period.

In the Consumer Beauty segment, sales rose 9%, or 10% on an LFL basis, to $552.0 million. Adjusted EBITDA for the segment fell from $53.5 million to $52.7 million.

Management said that consumer beauty segment saw particular strength in Brazil and Latin America. It saw double-digit LFL revenue growth with its Rimmel, Bourjois, Risque, Monange, Bozzano, and Paixao brands.

By geography, Americas revenue jumped 11%, or 13% on an LFL basis, to $567.9 million. EMEA sales climbed 15%, or 13% on an LFL basis, to $594.62 million, while Asia Pacific revenue soared 34%, or up 40% on an LFL basis, to $189.5 million.

Overall, this was a very strong quarter from Coty, as revenue came in above its raised guidance level. Prestige fragrance continues to outperform, and the company is making strides in China and the Travel Retail segment. Meanwhile, the company is doing well to grow revenue in the Consumer Beauty segment, as it looks towards Brazil to power growth.

Outlook

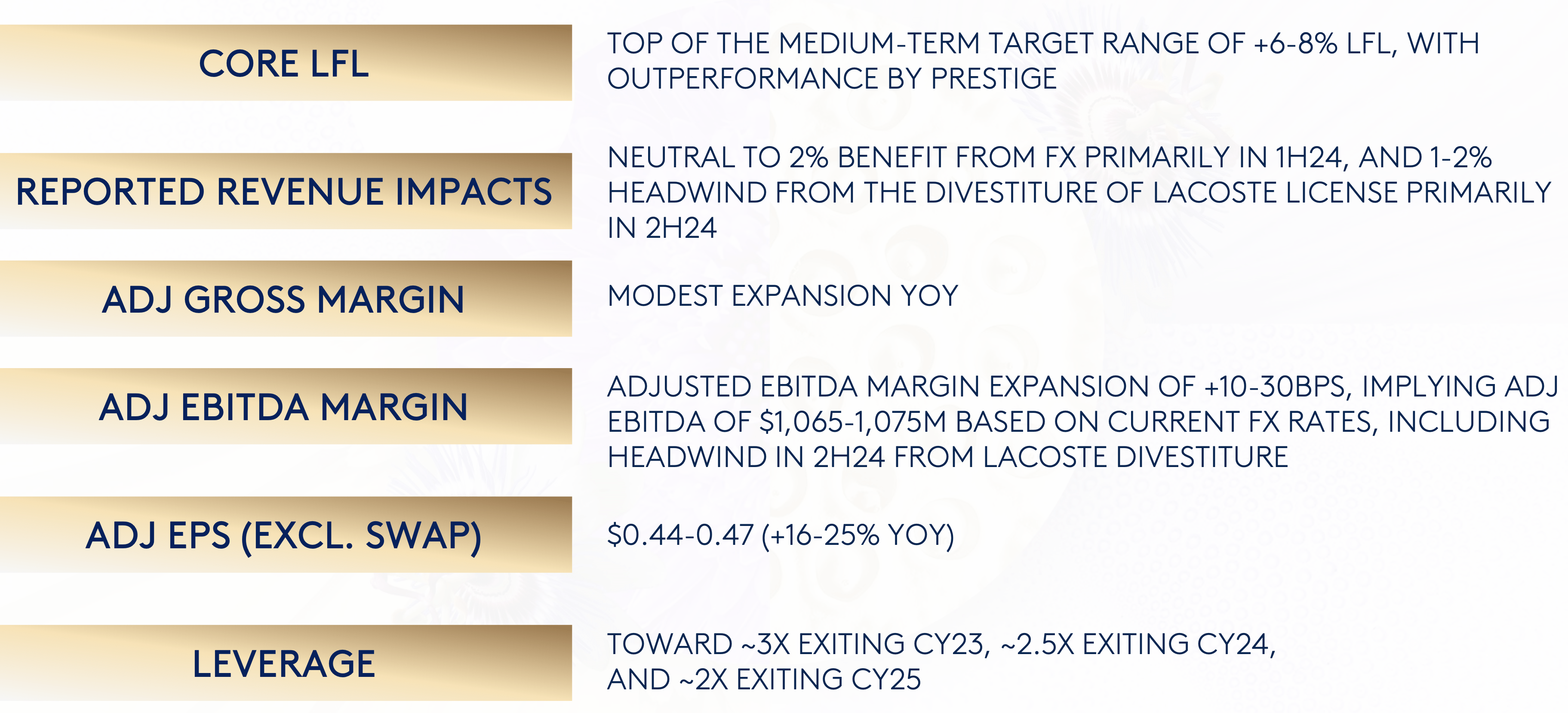

Looking ahead, COTY issued its full-year guidance for fiscal 2024. The company expects to post full-year sales growth on an LFL basis of between 6-8%, with Prestige outperforming. It is expecting FX to be neutral to a 2% benefit, with the divestiture of Lacoste being a 1-2% headwind in the second half. It is projecting fiscal 1H24 revenue to be up between 8-10%.

{kind=link}

On the earnings front, COTY now expects full-year adjusted EPS of between 44-47 cents, excluding mark-to-market adjustments of its equity swaps. This would represent between 16-25% growth. For the first half of the year, it is projecting adjusted EPS on the same basis of 35-38 cents.

COTY forecast full-year adjusted EBITDA between $1.065-1.075 billion. It expected adjusted EBITDA margins to improve 10-30 basis points.

On its fiscal Q4 earnings call , CEO Sue Nabi said:

"As we enter fiscal '24, we see no signs of slowing in fragrance demand. And while we are already a leader in prestige fragrances, we still have ample white space opportunities in this category, even within our stronghold geographies. This is anchored on 2 areas. First, in our core prestige fragrance business. We have historically been the leader in the $13 billion male fragrance category, but has ample room to improve our position in the much bigger female fragrance category which is roughly double the size of male fragrances at $24 billion and where we are currently in the top 3. Second, we are still having limited scale but are actively strengthening our positioning in the smaller but rapidly growing $4 billion ultra-premium fragrance category, whether it's through our Chloe Atelier des Fleurs collection whose sales have grown by 5x versus 2 years ago, or through the upcoming launch of our internally developed Infiniment Coty Paris fragrance brand. … . And that brings me to a key milestone in our strategic ambitions to elevate our share in female fragrances, which is our newly launched Burberry Goddess Eau de Parfum female fragrance, which is now appearing across global distribution. … First, Burberry product is already a top 3 fragrance at leading airports. Second set out is 1.5 to 3x higher than recent Coty blockbuster launches. And third, the Burberry Goddess launch is having a strong halo effect on the men's fragrance Burberry Hero as well as on Burberry Her line."

Management said inflation remains elevated but that it expects a significant moderation of COGS inflation in the 2nd half. The company continues to believe that it can eventually get to gross margin expansion into the mid-60s and beyond. It is implementing a mid-single digit price increase in Q1.

On the cost-cutting front, COTY is looking at $100 million in savings in F24, up from $90 million, and $75 million in FY25.

COTY issued strong guidance for FY24 with sales growth more tilted towards the first half of the year. With solid demand and a price increase in Q1, guidance could prove to be conservative. The company is doing well in China and Travel Retail, two markets where some others have struggled, pointing to the company taking some share in these markets. Meanwhile, Brazil remains a big opportunity on the mass side of the business.

If you wanted to nitpick, it would be about 1H margin guidance, as inflation continue to be a drag. However, it is expected to moderate in the second half.

Debt and Leverage

Deleveraging has been one of the central tenets of my COTY thesis. It ended the quarter with $4.03 billion in net debt. It generated an operating cash flow of $104.9 million in the quarter and $625.7 million for the fiscal year. Free cash flow was $38.1 million for the quarter and $402.9 million for the fiscal year.

Its leverage at quarter end was 4.1x, down from 4.4x last quarter and 4.7x a year ago. Excluding its remaining stake in Wella, which it plans to sell, its leverage was 3.1x

COTY said it is still targeting leverage of 3x exiting calendar year 2023 and 2.5x exiting calendar year 2024. About 85% of its debt is fixed.

COTY did a great job on the deleveraging front this past fiscal year, delivering on its FCF goals. It will sell a little bit more of its Wella stake to KRR soon for $150 million, which will further reduce debt. The company looks well on its way to reach its deleveraging goals, as EBITDA rises, and it uses FCF to pay down debt.

Valuation

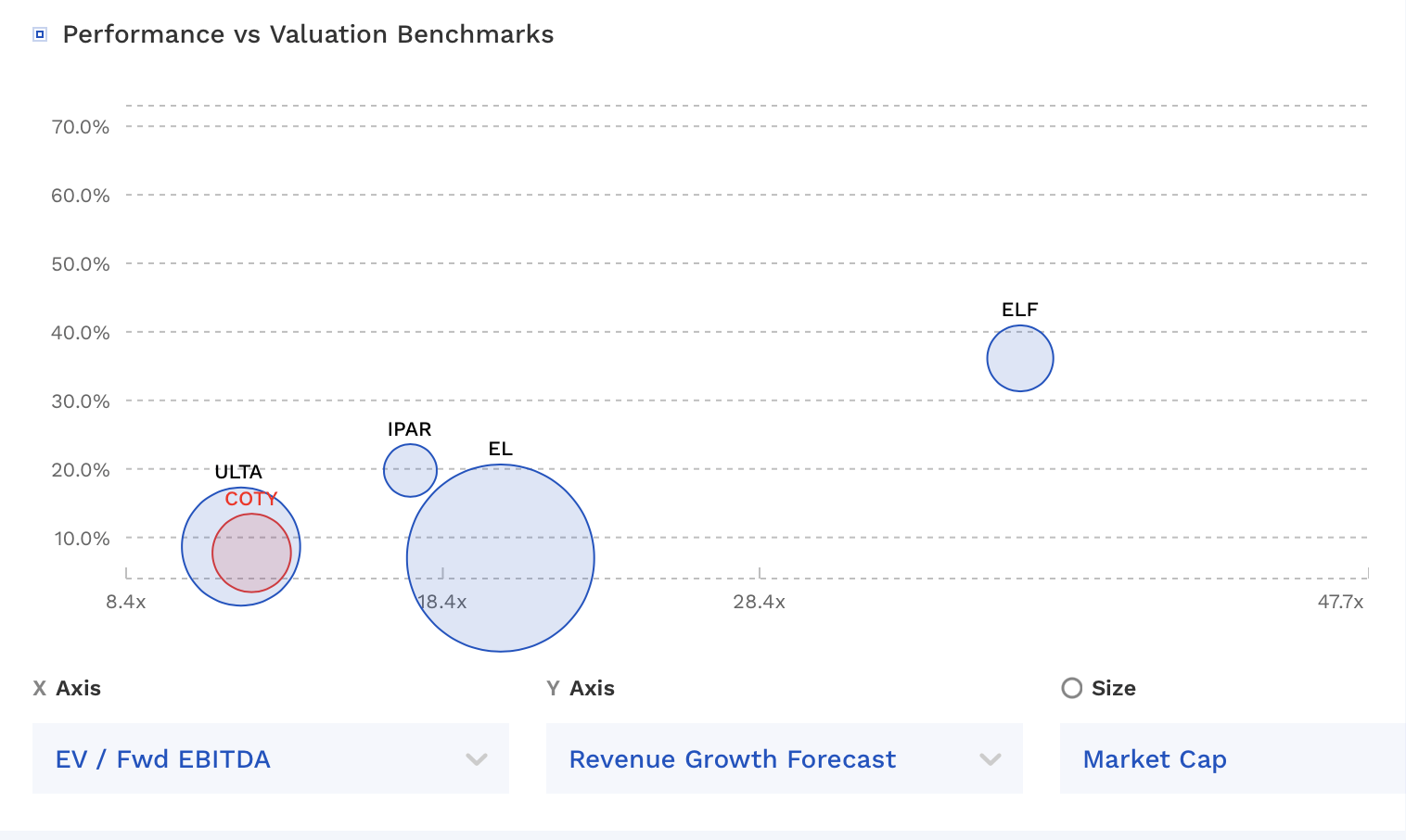

COTY stock trades around 12.4x the FY2024 (ending June) consensus EBITDA of $1.07 billion and 11.3x the FY2025 consensus of $1.17 billion.

It trades at a forward P/E of under 24x the FY24 consensus of 47 cents. Based on 2025 analyst estimates of 56 cents, it trades at 20x.

Outside of retailer Ulta (ULTA), COTY remains the cheapest beauty company is the space. Its high leverage and past mistakes remain the most likely reasons.

I was asked by a reader if the decline in Estee Lauder ( EL ) stock closed the gap and changed my thesis on COTY. EL still trades at 21.8x fiscal year '24 (ending June) EBITDA of $2.83 billion, so it still trades at quite the premium to COTY despite its recent struggles.

{kind=link}

Conclusion

COTY continues to be firing on all cylinders under the leadership of Sue Nabi. The beauty vet was one of the big reasons why I was bullish on COTY, and the company has delivered under her guidance and vision. The troubles at EL in fact show that COTY is not just riding the waves of a strong beauty and fragrance market, but taking share in important markets and categories.

COTY's deleveraging remains on track, and it is worth reminding investors that the company also has swap agreements with several banks to lock in a future $200 million buyback program at prices below $7.50. That was a great move that should provide a boost to the stock later.

COTY should be able to reduce debt by at least another $500 million this fiscal year, which if the stock price remained flat over the next year would value it at under 11x, which is a huge discount compared to other beauty brands. I continue to think COTY has a ton of upside, and continue to rate it a "Strong Buy" with an $18 target price, which is an under 16x multiple after debt reduction on FY25 EBITDA.

For further details see:

Coty Continues To Deliver Strong Results In Q4