COTY - Coty: High Leverage Ratio And Uncertain Near-Term Demand Are Risks

2023-07-21 11:10:20 ET

Summary

- I recommend a hold rating for COTY despite positive early demand indicators.

- Coty's recent results show a 15% increase in like-for-like sales, driven by strong demand for fragrances, and the company expects this trend to continue, particularly in the US and China.

- However, Coty's high debt levels are a concern, particularly if consumer discretionary spending falls further, which could lead to a downward rerating of the company's valuation.

Overview

My recommendation for Coty ( COTY ) is a hold rating, as I see near-term demand as uncertain, despite early indicators of positive demand. We are on the brink of a deep recession if the Fed decides to gear up for more aggressive rate hikes if economic data points to a resurgence in inflation. COTY high leverage ratio of COTY is also forcing me to stay on the sidelines as I see the risk of valuation continuing to be pressured.

Business

COTY manufactures and distributes beauty products. The Company offers fragrances, color cosmetics, hygiene, sun care, and skin treatment products. COTY supplies its products to department stores, specialty retailers, mass-market retailers, and duty-free shops in airports worldwide.

Recent results & updates

The 15% increase in LFL sales reported by COTY for 3Q23 was significantly higher than the 10% increase forecast by management. Additionally, LFL growth was even across segments as COTY introduced mid-single digits pricing, with Prestige LFL up 16% and Consumer Beauty LFL up 12%.

Management provided additional color by noting that the Prestige top line was driven by the recent and sustained strength in demand for fragrances, which pushed growth for the segment into the mid-teens from the high single digits seen in 2Q23. As retailers restocked their shelves following a dwindling trade inventory in 2Q23's peak holiday season, COTY reaped additional benefits. This was especially true for the company's prestige fragrances. Readers may recall that fragrances experienced supply constraints, particularly in glass bottles, but that the company qualified additional suppliers, and incremental industry capacity, to help alleviate the problem. In addition, the Lancaster Ligne Princiere skincare line was introduced in China and Travel Retail in the 3Q23 as one of the company's prestige skin care offerings.

I anticipate the COTY's prestige fragrances businesses to continue expanding in the years to come, as they have in the years prior. The COTY analyst day in Paris two weeks ago only solidified my opinion. The Chief Commercial Officer of Prestige has made the observation that the increase in sales of high-end perfumes has nothing to do with the COVID pandemic. Management further note that sales of fragrances, which are known to improve consumers' moods, have been on the rise across both online and traditional retail channels in the United States and China. Positively for COTY, the premiumization trend shows no signs of abating, and the rise of social media as a key platform for discovering new fragrances has only accelerated the expansion of the category. From a quantitative point of view, management also elucidated more on the state of fine fragrances in the United States. Super heavy users increased by 5% from 2020 to 38%, while the number of niche fragrance users increased by 5% from 2020 to 33% and the number of heavy users increased by 7% from 2020 to 26%.

Recent results are also consistent with my optimistic outlook, as the company has seen growth in prestige fragrance in both the United States and Europe. In 1Q23, prestige fragrance in the United States grew by 15% compared to the previous year, and in Europe, it grew by 16%. In my opinion, I see the long-term growth prospects as highly favorable due to the positive shift in consumers' perception of prestige fragrances. Previously dominated by gifting, there has been a noticeable change towards self-consumption. This assertion is supported by the company's data, which shows a decline of 1% to 3% in gift sets sales while single bottle sales, which offer higher margins, have increased by 1% to 3%.

Financials

COTY has a lot of debt on its balance sheet (5x net debt to EBITDA). This is not the typical leverage ratio you would see in a discretionary product business. Even if we look at large luxury players like LVMH (LVMHF) and Kering (PPRUF), they have a leverage ratio of less than 1x typically. I don’t think the market will like it if consumer discretionary spending falls further, resulting in lower demand for COTY products, thereby reducing EBITDA (and increasing the leverage ratio). If this happens, I see valuation rerating downwards to reflect this risk.

Valuation and risk

Author's valuation model

According to my model, COTY is valued $14.45 in FY24, representing a 21% increase. This target price is based on my growth forecast of 4%/7%/5% in FY23/24/25 as I expect growth to slow in FY23, followed by a recovery in FY24, and a normalized mid-single digit growth in FY25, which is in-line with industry growth rates .

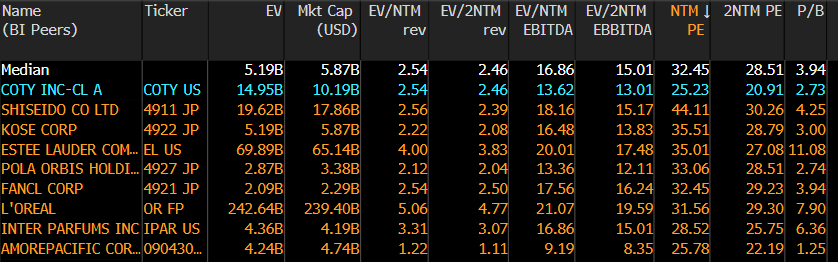

COTY is now trading at 25x forward PE, which is at a discount to its peers median of 32x forward PE. I believe COTY will continue to trade at a discount despite growing at the median rate because of its high leverage ratio. For comparison, the median leverage ratio is -0.85x, but COTY is at near 5x. In particular, with the high interest rates environment, I believe investors are moving away from high debt assets.

{kind=link}

{kind=link}

Bloomberg

COTY nature of business is its biggest risk as it is discretionary in nature. While they come at higher prices, they are often heavily impacted by the economic cycle as consumers cut discretionary spending first, and recovers last. In the current macroeconomic environment, I see this risk as an elevated risk.

Summary

In conclusion, my recommendation for COTY is a hold rating due to the uncertainties in near-term demand and the high leverage ratio. While the company has shown positive early indicators of demand, the potential for a deep recession and aggressive rate hikes by the Fed pose risks to the business. Coty's significant debt level is also concerning, and any further decline in consumer discretionary spending could impact demand for its products, leading to a rise in the leverage ratio and a potential downward rerating of the company's valuation.

For further details see:

Coty: High Leverage Ratio And Uncertain Near-Term Demand Are Risks