COTY - Coty: Quarterly Guidance Increase And Lower Leverage Make It Appealing

2023-10-25 18:30:39 ET

Summary

- Coty Inc. has increased its guidance for H1 2024, leading to increased quarterly EPS figures and making it a name to watch in the beauty industry.

- The company is undergoing a transformation plan to simplify its capital structure, focus on market positioning, and reduce debt.

- Coty's focus on innovation, expansion in China, and strengthening of electronic sales channels make it an attractive investment for long-term investors.

Coty Inc. ( COTY ) recently increased its guidance for H1 2024, and many analysts increased their quarterly EPS figures for the next quarter. Taking into account the recent divestitures made, current transformation, and the efforts with respect to innovation in technology at the ecological level, COTY appears to be a name to follow carefully. The total amount of debt is not small, however assuming a lower leverage in 2024 and FCF growth, COTY is definitely trading a bit cheaper than in previous months. It is definitely a good play for investors looking for long-term investment.

Coty Increased Its Guidance In September

With a broad portfolio of fragrance, skin, body care, and cosmetics brands, Coty is a leading company in the global beauty industry. Founded in 1904 and active since that date, the company began a few years ago with a transformation plan aimed at simplifying the capital structure, focusing on strategies for positioning in markets, and deleveraging its balance sheet.

Within the framework of this transformation, the most important development points are innovation in beauty products, specifically in the premium range of international reach, the expansion of its presence in China, and the strengthening of electronic sales channels together with the relationship with consumers and clients.

In the same sense, motivated by the company's capital restructuring, Coty completed the sale of a majority part of the professional and retail hairdressing business, which included globally recognized brands such as Wella and Clairol. In my view, the fact that Coty is already making significant changes in the organization could justify certain attention from the investment community.

Operations are divided into two segments, consumer beauty and prestige lines. In the first of these segments, we find brands such as adidas (ADDYY), Nautica, Bruno Banani, and Jovan among others, while in the prestige line segment, some brands such as Hugo Boss (BOSSY), Gucci, Calvin Klein, and Tiffany & Co.

With that about the business model, I believe that the recent news about better net sales guidance growth in 2024 and better adjusted EBITDA than initially expected makes Coty a must-follow name in the coming months.

Since providing its guidance on its FY23 earnings call four weeks ago, Coty has seen strong momentum in beauty demand across its key markets and categories, particularly in prestige fragrances. Source: Coty Raises FY24 Outlook

In particular, the new figures include double-digit core LFL net sales growth in H1 2024, which is better than what the company stated in August. Given that I took into account these figures in my DCF model, readers may want to have a look at the words given by management.

The combination of these factors is driving an acceleration in Coty's volumes and sales, with the Company now expecting core LFL sales growth in first half FY24 of +10-12%, an increase from its earlier outlook of +8-10%. Source: Coty Raises FY24 Outlook

Coty is expected to deliver adjusted EBITDA of approximately $1.075-1.085 billion and lower leverage in 2023 and 2024. If the final figures are as expected by management, I believe that the demand for the stock may trend higher.

Coty continues to target modest gross margin expansion in FY24 and 10-30 bps of adjusted EBITDA margin expansion, implying adjusted EBITDA of approximately $1,075-1,085M at current FX rates, an increase from the implied adjusted EBITDA of $1,065-1,075M in its prior guidance. Source: Coty Raises FY24 Outlook

The Company remains on track to drive leverage towards 3x exiting CY23, fueled by seasonally strong free cash flow generation, and towards 2.5x exiting CY24.

Beneficial Market Expectations, And Many Increases In EPS Revisions In The Last 90 Days

I believe that the numbers from other analysts are beneficial, and it is worth having a look at them. Other analysts expect sales growth from 2023 to 2026, operating margin growth, and net margin growth in 2026 and 2025. Besides, free cash flow is expected to grow from 2023 to 2026.

More in particular, the market expectations include 2026 net sales of about $6756 million, 2026 EBITDA close to $1.273 billion, and 2026 EBIT close to $1018 million. Additionally, operating margin would be close to 15.1% million, with 2026 net income of $521 million. Finally, 2026 free cash flow would be close to $620 million, with FCF margin of 9.17%.

Source: S&P

It is also worth noting that in the beginning of November, COTY is expected to deliver its new quarterly earnings. Analysts expect EPS GAAP to be close to $0.13, however the most relevant point is that we saw 10 new revisions in the last 90 days improving COTY's EPS revision. For some reason, analysts are becoming more and more optimistic about COTY.

Source: SA

Balance Sheet

As of June 30, 2023, the company reported cash close to $246 million, restricted cash of $36 million, inventories worth $853 million, and property and equipment of about $712 million. Total current assets are below the current amount of liabilities, which is not ideal. With that, Coty reported a significant amount of properties and goodwill. I believe that bankers would most likely offer liquidity if necessary.

With regard to non-current assets, Coty noted goodwill of close to $3.987 billion, other intangible assets worth $3.798 billion, and equity investments of $1.068 billion. In sum, total assets are equal to $12.661 billion, and the asset/liability ratio is larger than 1x. I believe that the balance sheet remains quite stable, but investors may want to follow carefully the total amount of debt.

Source: 10-k

The list of liabilities does not seem worrying, however the total amount of debt will most likely not be appreciated by conservative individuals. It makes the stock a bit risky.

With accounts payable of close to $1.444 billion and accrued expenses and other current liabilities worth $1.042 billion, short-term debt and current portion of long-term debt stood at $57 million. Besides, the company noted long-term debt of about $4.178 billion and pension and other post-employment benefits of $280 million. Total liabilities were equal to $8.428 billion.

Source: 10-k

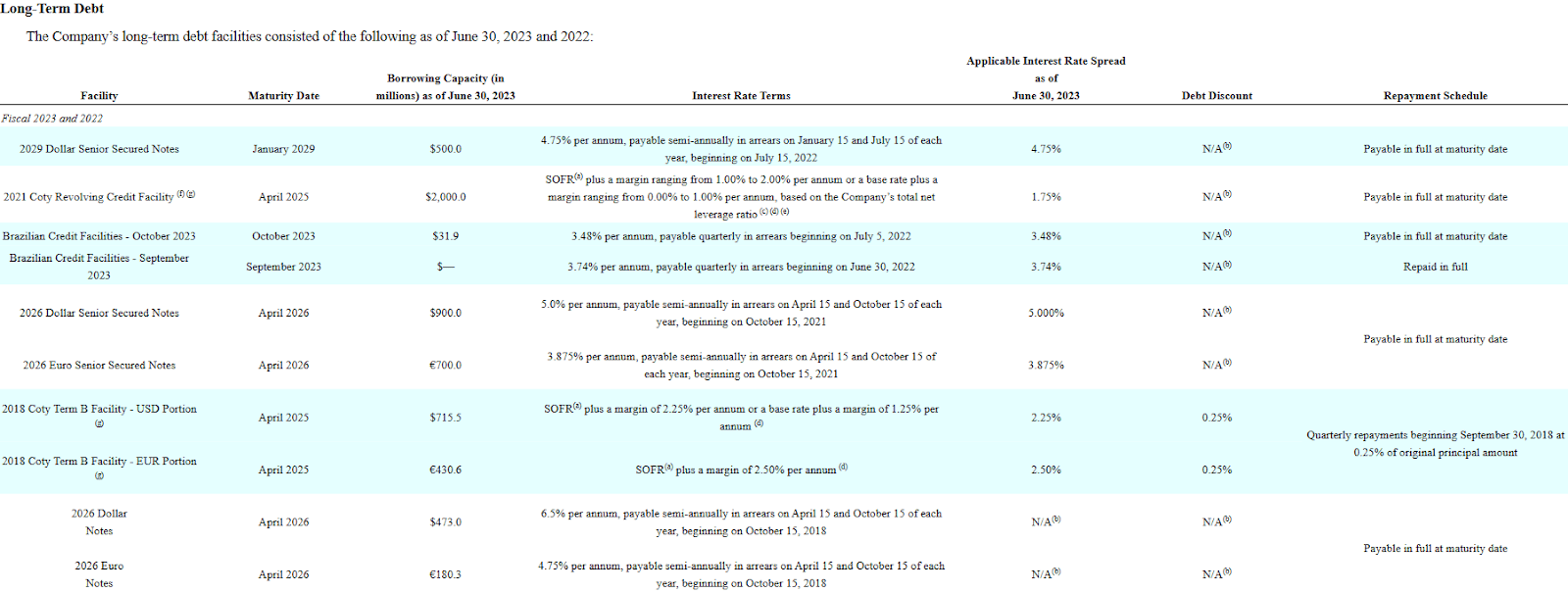

I studied carefully the total amount of debt and the different interest rates paid by Coty. Even considering the total amount of debt, I believe that management is really doing a good job by finding adequate debt agreements. Recently, the company signed senior secured notes due in 2030 including debt of close to 6.625%.

On July 26, 2023, we completed a senior secured notes offering and received net proceeds of $740.6. The new senior secured notes are due in 2030 and bear an annual interest rate of 6.625%. Source: 10-k

With that about the recent debt agreement, Coty reported debt close to SOFR plus 1%-2%, 3.8%, and 2.5%. I took into account these figures in my financial models. In my view, investors who do not feel comfortable investing in companies with significant leverage may not invest in Coty.

{kind=link}

Transformation And New Products Will Most Likely Lead To FCF Growth And Net Sales Growth

I believe that restructuring efforts, the optimization of general operating margins, and the implementation of an aggressive strategy to launch new products to the market will most likely lead to FCF margin expansion. There is also the fact that the company made several divestitures that may bring future financial flexibility, and help the company better finance its operations. In sum, I believe that the recent increase in FCF/Sales seen in 2021, 2022, and 2023 may continue in the near future.

Source: 10-k Source: YCharts

Technological Innovation At An Ecological Level Could Also Bring Net Sales Growth

Technological innovation related to the sustainability of products at an ecological level plays a fundamental role, since it is part of the trend in the beauty industries today. Regarding the market strategy, the focus is on accelerating the growth of prestige fragrance brands and the diversification of the portfolio of skin care product lines. I believe that these strategies will most likely lead to net sales growth in the coming years.

Supply Chain Normalization And Measures To Fight Inflation Could Also Bring FCF Margin Expansion And Lower Net Sales Volatility

In the immediate term, a large part of the company's efforts is subject to normalizing the situation of its supply chain, which has suffered numerous disruptions, along with the tools to cushion inflation variations. In my view, using a global network of third-party manufacturers and primarily using essential oils, alcohol, and specialty chemicals will most likely bring cost savings in the coming quarters.

To capitalize on innovation and other supply chain benefits, we continue to utilize a network of third-party manufacturers on a global basis who produce approximately 21% of our finished products.

The principal raw materials used in the manufacture of our products are primarily essential oils, alcohols and specialty chemicals. The essential oils in our fragrance products are generally sourced from fragrance houses. As a result, we realize material cost savings and benefits from the technology, innovation and resources provided by these fragrance houses. Source: 10-K.

With The Previous Assumptions And Figures Obtained From Previous Cash Flow Statements, I Designed A Valuation Model

The company traded in the past at close to 27x cash flow, but appears to trade a 13x cash flow right now. The sector median trades at close to 12x, so I believe that an exit multiple around 12x appears conservative.

Source: SA

My cash flow statement projections include net income growth with share-based compensation expenses, declines in changes in inventory, and decline in capital expenditures. As a result, we may see FCF growth.

More in particular, my numbers included 2031 net income close to $562 million, 2031 depreciation and amortization worth $104 million, non-cash lease expenses close to -$15 million, no asset impairment charges, and losses on sale of business in discontinued operations.

Additionally, I also included 2031 realized and unrealized gains from equity investments of close to $-200 million, foreign exchange effects close to $100 million, changes in trade receivables worth $272 million, and 2031 changes in inventories of -$1000 million.

My cash flow statements took into account 2031 prepaid expenses and other current assets worth $388 million, changes in accounts payable of $766 million, and accrued expenses and other current liabilities close to -$138 million.

Source: My Cash Flow Expectations

Finally, taking into consideration changes in operating lease liabilities worth $167 million and changes in income and other taxes payable close to $152 million, I obtained net cash provided by operating activities close to $1.709 billion and 2031 FCF close to $1.520 billion.

Source: My Cash Flow Expectations

With FCF ranging from close to $476 million to about $1.5 billion, an EV/FCF multiple of about 10x-14x FCF, and a WACC between 6%, and 12%, I obtained an implied valuation close to $17 per share and $7 per share. Additionally, the internal rate of return would stand between -3% and 10%-11%.

Source: My Cash Flow Expectations

Competitors

Competition in this industry is significant, and comes from internationally established companies and the presence of specific products in the market, marketed by local manufacturers, distributors, or cosmetic centers. In any case, there are few companies that maintain a multinational operating structure like Coty as well as a portfolio of products designed to compete in different markets. Competition also extends to the exclusivity of licenses for the marketing of some products.

Risks

In the sense of the industry, the forecast consolidation of the retail distribution market and the transformations in the ways of consumption, including the advancement of digital sales channels, mean a potential risk in case of failing to adapt to this situation. The company's inability to read customer preference trends and the inability to comply with obligations in contracts with some brands for distribution licenses also reflect risk factors.

On the other hand, there are a series of risks linked to the current global strategy, which is supported by large operating costs of acquisitions and business restructuring, and if it is not achieved or does not meet the expected results, it may lead to a situation financially adverse for the company. These factors come hand in hand with the ability to introduce new products to the market besides making intelligent selection of acquisitions in addition to obtaining positive results in its joint partnerships with other companies.

Operational risks regarding the continuity of the supply chain, dependence on third parties, and the ability to meet the demand for some products are also part of this analysis.

Conclusion

Coty recently increased its guidance for the year 2024 as a result of strong momentum in beauty demand. Expecting double-digit LFL net sales growth in H1 2024, Coty received a significant number of quarterly EPS expectations increases in the last 90 days from other analysts. In the long run, I believe that the divestitures recently made, restructuring efforts, and innovation of technology at the ecological level will most likely bring the attention of more investors. I dislike the total amount of debt, which could be a cause of concern from conservative investors. With that, I think that this is a company for shareholders willing to make a long-term investment.

For further details see:

Coty: Quarterly Guidance Increase And Lower Leverage Make It Appealing