COTY - Coty's Results Continue To Shine And More Catalysts Are Ahead

2023-05-31 02:16:24 ET

Summary

- Coty reported strong fiscal Q3 results, driven by robust fragrance demand.

- The company raised its full-year guidance for revenue and adjusted EPS.

- Coty's deleveraging plan remains on track.

- Coty's stock is undervalued compared to its peers, and I maintain a "Strong Buy" rating with a potential upside of $16+.

With Coty ( COTY ) up only moderately since I put a “Strong Buy” rating on the stock in my initial write-up in February, I want to take a close look at the stock.

Fiscal Q3 Results

COTY reported fiscal Q3 results earlier this month, seeing a 9% increase in sales to $1.29 billion. Like for like (LFL) revenue soared 15%, as the company saw a -4% currency headwind and a -3% negative impact from exiting Russia. The revenue results beat the analyst consensus of $1.23 billion.

Management attributed the strong sales to robust fragrance demand, improvement in its supply, as well as retailers re-stocking inventory. It estimated the latter attributed a mid-single digit positive impact to Q3 results. It believes retail inventories are now at normalized levels and that sell-in and sell-out levels should be pretty aligned.

Adjusted gross margins came in at 62.0%, down -170 basis points. The decline was due to COGS inflation. The company raised prices at the end of the quarter by mid-single digits.

Adjusted EBITDA for the quarter edged lower to $181.9 million from $182.5 million a year earlier. Adjusted EPS came in at 19 cents versus 3 cents a year ago and topped analyst estimates of 5 cents. Excluding mark-to-market swaps, adjusted EPS was 6 cents, beating estimates by a penny.

In the Prestige segment, revenue climbed 10%, or 16% on an LFL basis, to $799.7 million. Adjusted EBITDA for the segment climbed 9% to $169.3 million.

The company said it is seeing increased fragrance usage, particularly among Gen Z, men, and Hispanic consumers. It noted that demand for prestige fragrance in the Americas and Europe accelerated in the quarter to the mid-teens, well above the low to mid-single digit growth the market has historically seen.

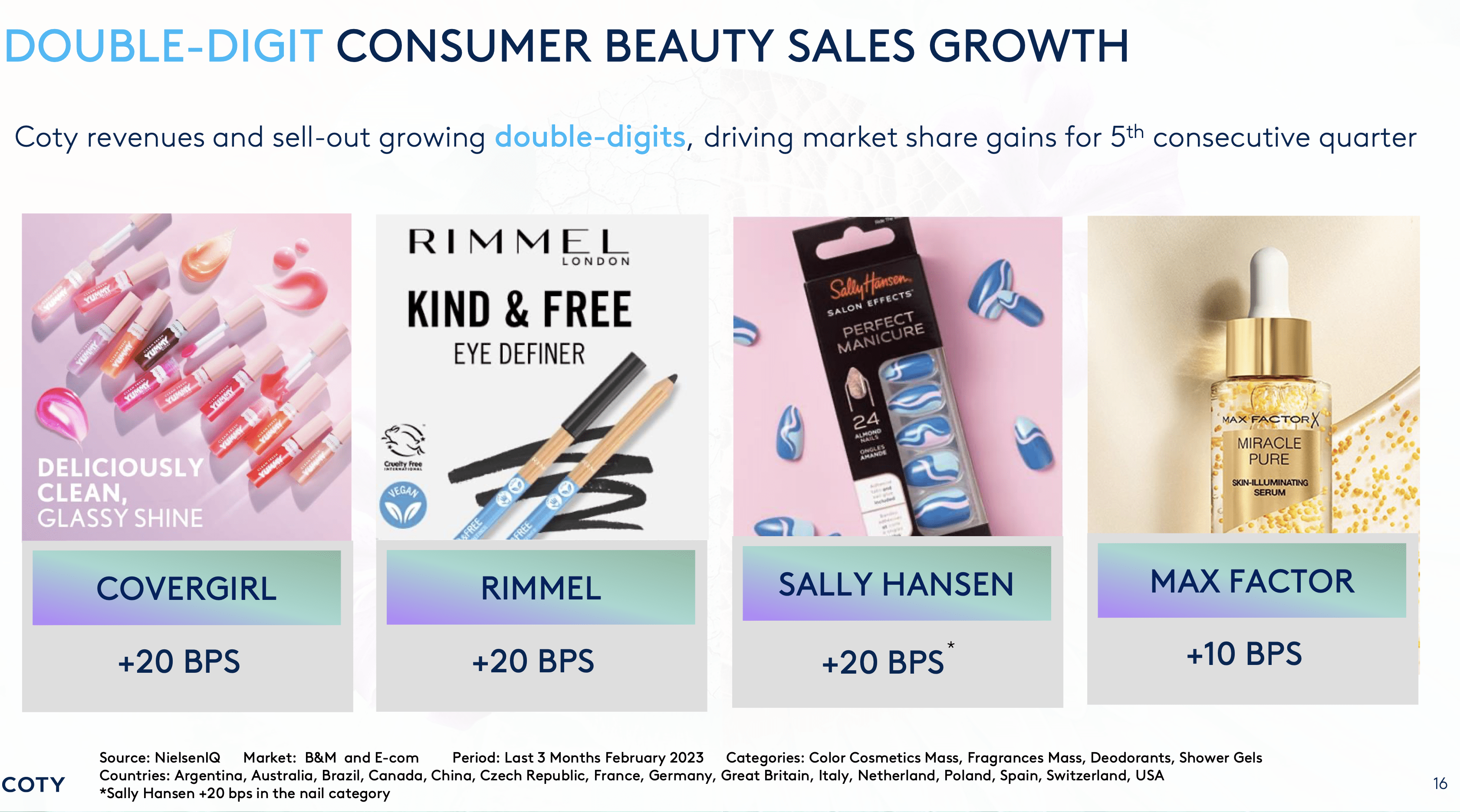

In the Consumer Beauty segment, sales rose 6%, or 12% on an LFL basis, to $489.2 million. Adjusted EBITDA for the segment fell from $26.6 million to $12.6 million. The drop in adjusted EBITDA was attributable to significant marketing investments behind some spring product launches.

Management said that consumer beauty segment once again saw share gains among its top brands. It saw strong double digit LFL sales growth in CoverGirl, Rimmel and Max Factor. It noted that CoverGirl is doing well with Millennial and Gen Z consumers, as well as gaining share amongst Hispanics. Meanwhile, it said Max Factor grew 30% ex Russia.

{kind=link}

By geography, Americas revenue jumped 13%, or 15% on an LFL basis, to $543.8 million. EMEA sales climbed 7%, or 18% on an LFL basis, to $587.6 million, while Asia Pacific revenue was essentially flat, or up 4% on an LFL basis, to $157.5 million.

Management said sales in China were negative but improving in the quarter. However, it notes that April sales in China were higher both year over year and compared to two years ago.

Overall, this was a very strong quarter from COTY. Sales accelerated, with fragrances leading the way. Meanwhile, it continues to re-take share in the mass beauty segment.

The one knock on the quarter could be that EBITDA didn’t grow, but this was due to increased marketing investments made ahead of spring launches for new products. I think this strategy makes sense, as COTY needs to continue to grow its businesses. Investors could also nitpick about gross margins, but it did implement a price increase late in the quarter and is evaluating another price increase in FY Q1 as well.

Outlook

Looking forward, COTY raised its full-year guidance for revenue and adjusted EPS.

The company now expects to post full-year sales growth on a LFL basis of between 9-10%, up from its prior outlook of 6-8%. It is projecting fiscal Q4 revenue to be up 10%+.

On the earnings front, COTY now expects full-year adjusted EPS of between 52-53 cents, or between 38-39 cents excluding mark-to-market adjustments of its equity swaps. Its previous forecast was for adjusted EPS of 35-36 cents.

COTY maintained its full-year adjusted EBITDA guidance of $955-965 million. However, it noted that this now includes a $50 million currency headwind.

Management sees a 2.5% increase in COGs in fiscal Q4. For F24, it expects a similar level as the second half of F23, with a moderation to 1% in the second half. It’s also expecting some inflation in the SG&A line as well.

The company is evaluating another price hike in Q1 FY24. It expects gross margins to modestly expand in Q4 and for FY24. Further out, it is projecting gross margin expansion into the mid-60s and beyond.

On the cost cutting front, COTY is looking at $90 million in savings in F24 and $75 million in FY25.

The company is projecting mid-20% adjusted EPS CAGR through fiscal year 2026.

COTY’s outlook remains strong, with the company raising both sales and adjusted EPS guidance. The company noted that fragrance sales actually have been accelerating in recent months, which is a good sign. A re-opening China and recent luxury launches in that market also bode well for the company. The company also has some skincare launches coming up that should help next year, and it’s recently brought back its philosophy brand as well.

Debt and Leverage

One of the main parts of my COTY thesis was that the company would deleverage. It ended the quarter with $4.1 billion in net debt. Fiscal Q3 is typically a cash outflow quarter for the company.

Its leverage at quarter end was nearly 4.4x. Excluding its remaining stake in Wella, which it plans to sell, its leverage was 3.3x

COTY said it is still targeting leverage of 3x exiting calendar year 2023 and 2x exiting calendar year 2025.

The company is projecting $400+ million in free cash flow for the fiscal year. About 70% of its debt is fixed.

Deleveraging is still a big part of the COTY story, and while that did not happen during FQ3, that is largely due to seasonality. The company is generating solid free cash flow, which along with the eventual sale of its remaining stake in Wella, valued at over $1 billion, should have it on target to meet its deleveraging goals. With its cost savings and strong sales, FCF should be able to get to around $500 next year.

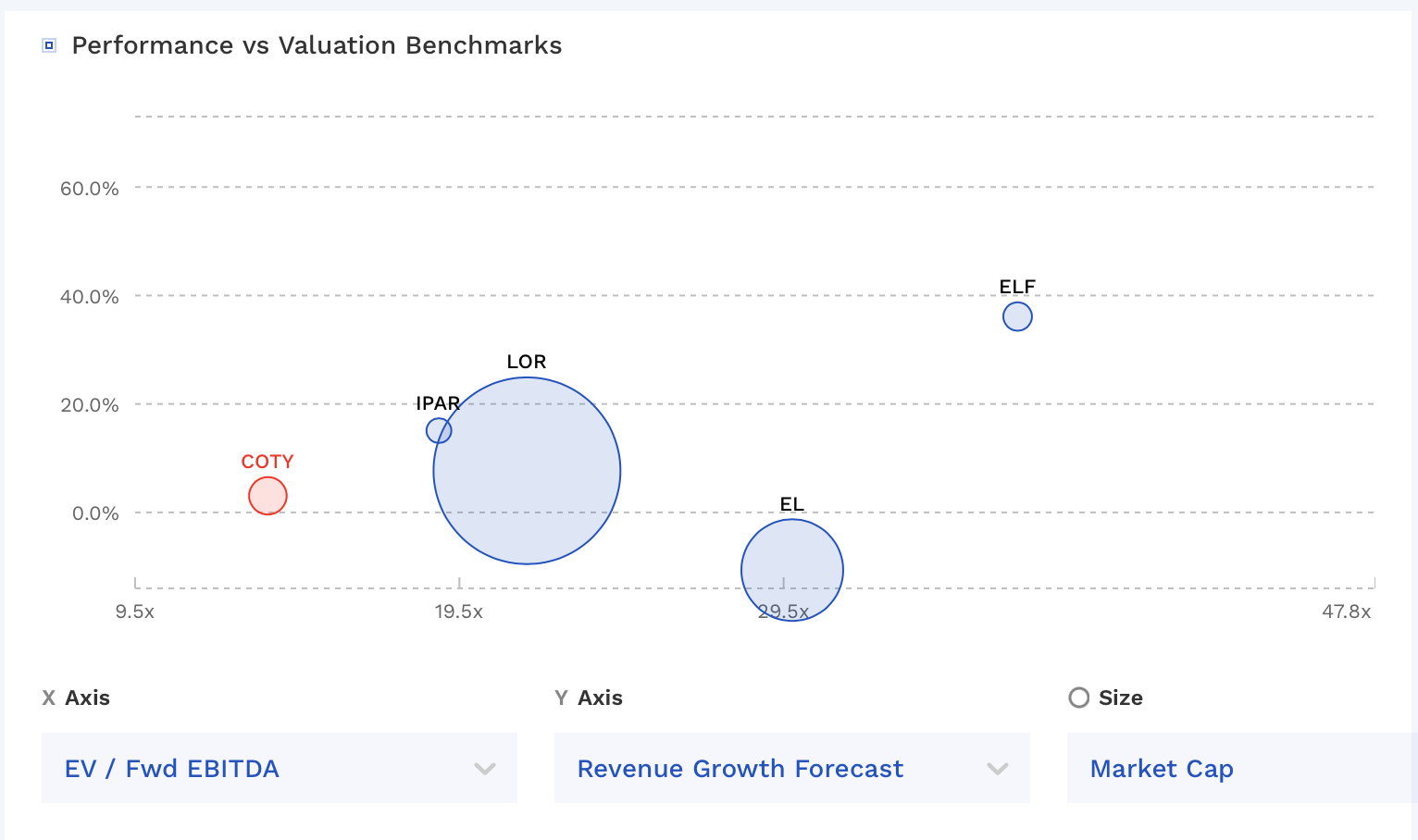

Valuation

COTY stock trades around 12.4x the FY2024 (ending June) consensus EBITDA of $1.06 billion and 11.3x the FY2025 consensus of $1.16 billion.

It trades at a forward P/E of under 24x the FY24 consensus of 46 cents. Based on 2025 analyst estimates of 58 cents, it trades at under 19x.

COTY is the cheapest beauty company is the space by far – the reasons for which I go into in my original article, as it has had some prior missteps under previous management teams.

{kind=link}

Conclusion

The beauty space has been one area that I’ve been bullish on this year, with a “Strong Buy” rating on COTY and a “Buy” rating on e.l.f. Beauty ( ELF ), which I started in February . ELF has been the stronger performer of the two, but I think COTY has more potential upside from here.

COTY is performing well and is the cheapest stock in the space by far. The stock is still not getting full credit for the turnaround CEO Sue Nabi has undertaken at the company. COTY is looking to potentially dual list on the Paris exchange, which could bring some more recognition to the stock.

The combination of a strong fragrance market in both the U.S. and Europe, driving further into China at an opportune time, and a push into skincare are all positives for the company. Its deleveraging plans remain on track, and the company smartly entered into a swap agreement with several banks to lock in a $200 million buyback program at prices below $7.50, well below where it trades today.

I continue to see big upside ahead to $16+ and continue to rate the stock a “Strong Buy.”

For further details see:

Coty's Results Continue To Shine, And More Catalysts Are Ahead