COTY - Coty: Strong Execution Continues

2023-12-04 13:03:35 ET

Summary

- Coty's Prestige segment continues to outperform, with prestige fragrance sales growing 2.5x the market in fiscal Q1.

- The company raised its full-year guidance for the second time in less than a month.

- Investors continue to underappreciate the turnaround the company has undergone under its most recent CEO.

Back in February , I placed a "Strong Buy" rating on Coty ( COTY ), arguing that CEO Sue Nabi was in the midst of transforming the company after years of missteps from various prior management teams and that it was a nice deleveraging story. More recently, in August , I said the company was shining while rival Estee Lauder ( EL ) was struggling. The stock is up nearly 13% since my initial write-up, just ahead of the nearly 11% return for the S&P 500. Let's catch up on the company after it reported earnings earlier this month.

Company Profile

As a reminder, COTY is a beauty company with a portfolio of owned and licensed fragrance, cosmetic, and skincare brands in both the mass and prestige categories. It has licenses with the likes of Marc Jacobs, Gucci, Hugo Boss, Burberry, and Calvin Klein, while its own brands include CoverGirl, Max Factor, Rimmel, Lancaster, and philosophy, among others.

Prestige is about 65% of its revenue, with most of that coming from the fragrance category. In fiscal Q1, EMEA represented 45% of its sales, while the Americas was 43% and APAC 12%.

Fiscal Q1 Results

COTY reported its fiscal Q1 results last month , seeing an 18% increase in sales to $1.64 billion, both as reported and on a like-for-like (LFL) basis. The revenue results beat the analyst consensus of $1.58 billion.

The company said volumes grew double digits in its Prestige segment and were stable in its Consumer Beauty segment, while overall pricing was up high single digits.

Adjusted gross margins came in at 62.8%, down -60 basis points year over year but up 70 basis points sequentially. The year-over-year decline was the result of COGS inflation, a mix shift away from gift sets, and increased excess and obsolescence tied to the inventory build-up.

Adjusted EBITDA for the quarter jumped 17% to $360.3 million from $307.9 million a year earlier. Adjusted EPS came in at 9 cents versus 11 cents a year ago and missed analyst estimates of 17 cents.

In the Prestige segment, revenue climbed 23% (22% on an LFL basis), to $1.06 billion. Adjusted EBITDA for the segment jumped over 22% to $287.6 million.

Management said that COTY prestige fragrance revenue grew 25% on an LFL basis versus 10% for the prestige fragrance industry as a whole. Burberry fragrance revenues nearly doubled, spurred by the launch of Burberry Goddess. Burberry makeup, meanwhile, saw double-digit growth. In skincare, its Lancaster brand also saw double-digit growth.

In the Consumer Beauty segment, sales rose 10%, as reported and on an LFL basis, to $576.7 million. Adjusted EBITDA was flattish at $72.7 million versus $73.0 million a year ago.

Management called out an acceleration of growth in mass fragrances and solid growth in cosmetics and skincare in Brazil.

By geography, Americas revenue jumped 17% on both a reported and an LFL basis to $708.0 million. EMEA sales climbed 20%, or 18% on a LFL basis, to $732.2 million, while Asia Pacific revenue rose 16%, or up 19% on an LFL basis, to $201.2 million.

Prestige sales continue to grow in China, up double digits in Mainland China and up triple digits in Hainan, a popular Chinese island vacation spot. Travel retail revenue grew over 20%, although Chinese travel cohort levels still remain 50% below 2019 levels.

Turning to its balance sheet, COTY ended the quarter with $3.93 billion in financial net debt. Leverage was 3.8x, or about 2.8x if it were to sell its remaining stake in Wella. The company has ended the sale process currently but will look to divest its full stake by the end of calendar year 2025. COTY also issued 500 million of 2028 senior secured Euro notes in September. It then tendered to retire $400 million in 2026 U.S. bonds.

The company is dual listed on the Paris Exchange, in which it issued 33 million shares at $10.80, or $10.28 euros, netting $384.5 million in the process. In fiscal Q3, it will exercise a 27 million share buyback through a prior equity swap it entered into. It plans to buy back another 23 million shares in FY25 using its second equity swap. After its earnings report, the company also announced it would enter another total return swap to buy back 25 million shares at around current prices in 2026.

It generated $186.2 million in operating cash in the quarter. Free cash flow came in at $124.0 million.

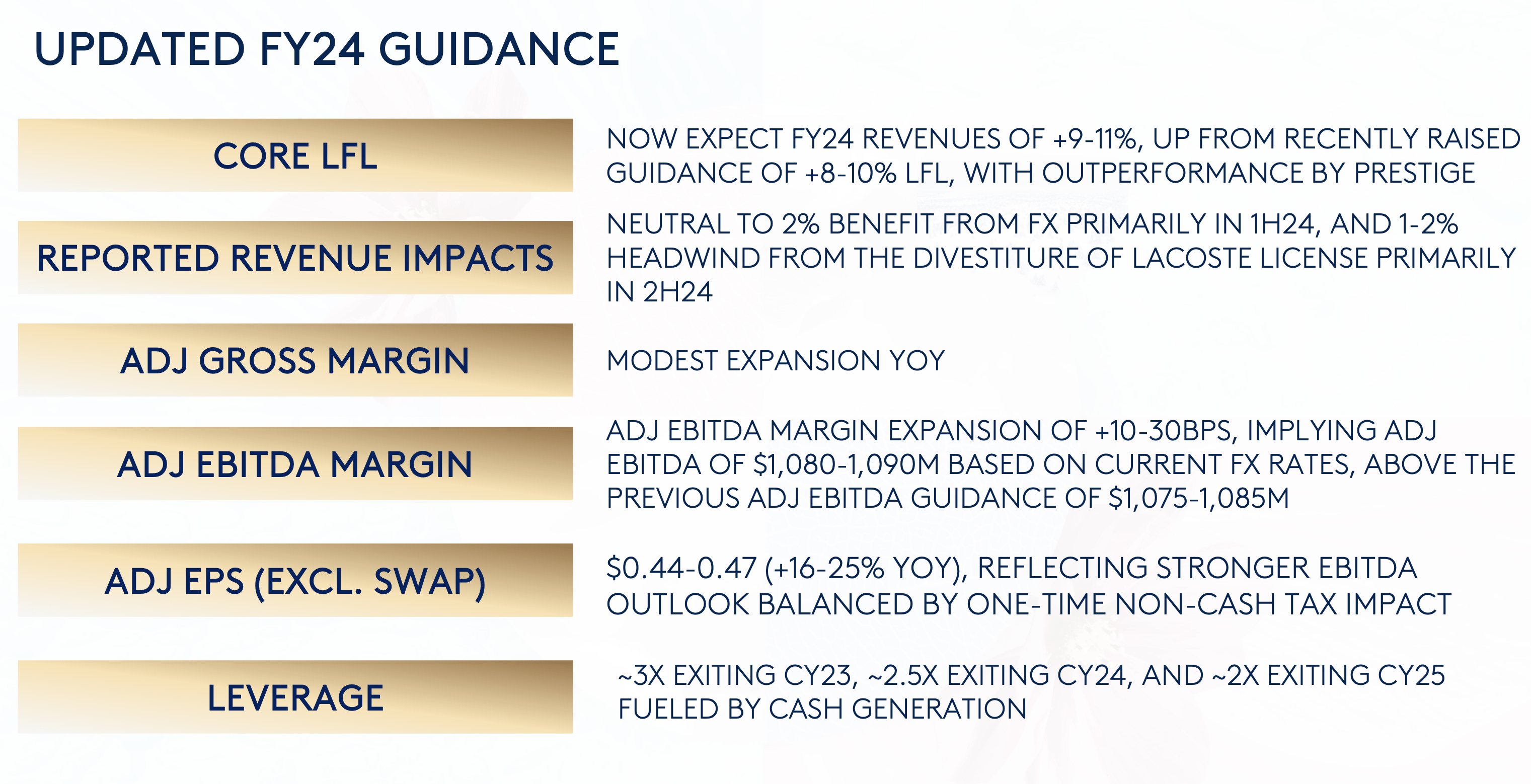

Looking ahead, COTY raised its full-year guidance for fiscal 2024. The company expects to post full-year sales growth on a LFL basis of between 9-11%, with Prestige outperforming. It had just raised its LFL revenue growth forecast in late September , taking it to 8-10% from 6-8%.

COTY forecasts full-year adjusted EBITDA between $1.080-1.090 billion. That's up from its September update of $1.075-1.085 and up from its original guidance of $1.065-1.075 billion. It expects adjusted EBITDA margins to improve 10-30 basis points, and it is looking for a significant improvement in COGS inflation starting in FQ2. It forecast adjusted EPS to rise 16-25%, implying adjusted EPS of between 44-47 cents.

{kind=link}

COTY expects to end CY23 with 3x leverage, CY24 with 2.5x leverage, and CY25 with 2x leverage.

On its fiscal Q1 earnings call , CEO Sue Nabi was bullish on medicated beauty being the next big thing, saying:

"I think what we have shared with all you guys several times is that the skin care market, and by the way, the beauty market in generally speaking, is going in the direction of the medicated beauty. And this is something that we see very, very strongly. And that's the reason why we have decided to reposition some of our brands quite strongly on this area. If you allow me, may I remind everyone that we just did the launch behind Orveda Skin Care of the first serum that uses technologies, inspired by the medical world that we call [senolytics], which is the first time a skin care brand is using this kind of technologies in a topical cream, as you say it. On Lancaster, the story that is really resonating very well is the story of using this vectors, liposomes that penetrate deep inside the skin. And this is really what is making the brand resonate with the Chinese consumers. And also on philosophy in the U.S., we've decided that the brand will stand for the brand that's going to bring a bit of wisdom in the craze around dermatologic ingredients. So as you hear from my words, it's all about a kind of medicated beauty. In the beauty world, we are using ingredients and formulations that are acting on the upper layer of the skin, and we are not allowed to go lower."

COTY continues to perform well, with the company raising its guidance twice within a few weeks period. Prestige fragrance sales continue to shine buoyed by new launches, and the company impressively outgrew the market by 2.5x. China and the Travel segment, meanwhile, continue to recover, and the company's Mass segment is growing in line with the market and seeing continued strength in Brazil.

Nabi, meanwhile, continues to be forward-looking, something I believe her predecessors were afraid to do. This includes looking to push into medicated beauty, which is where the company feels the market is moving towards. Skincare remains a big opportunity for the firm in my view, and this is an area of expertise for Nabi, who had run her own skincare company before joining COTY.

In addition, the swap agreements to buy back stock at current prices in the future remain innovative. The agreements made in 2022 look like they will prove to be very well-timed, while the latest one could prove to be attractive as well if the stock trades much higher from here over the next few years.

Valuation

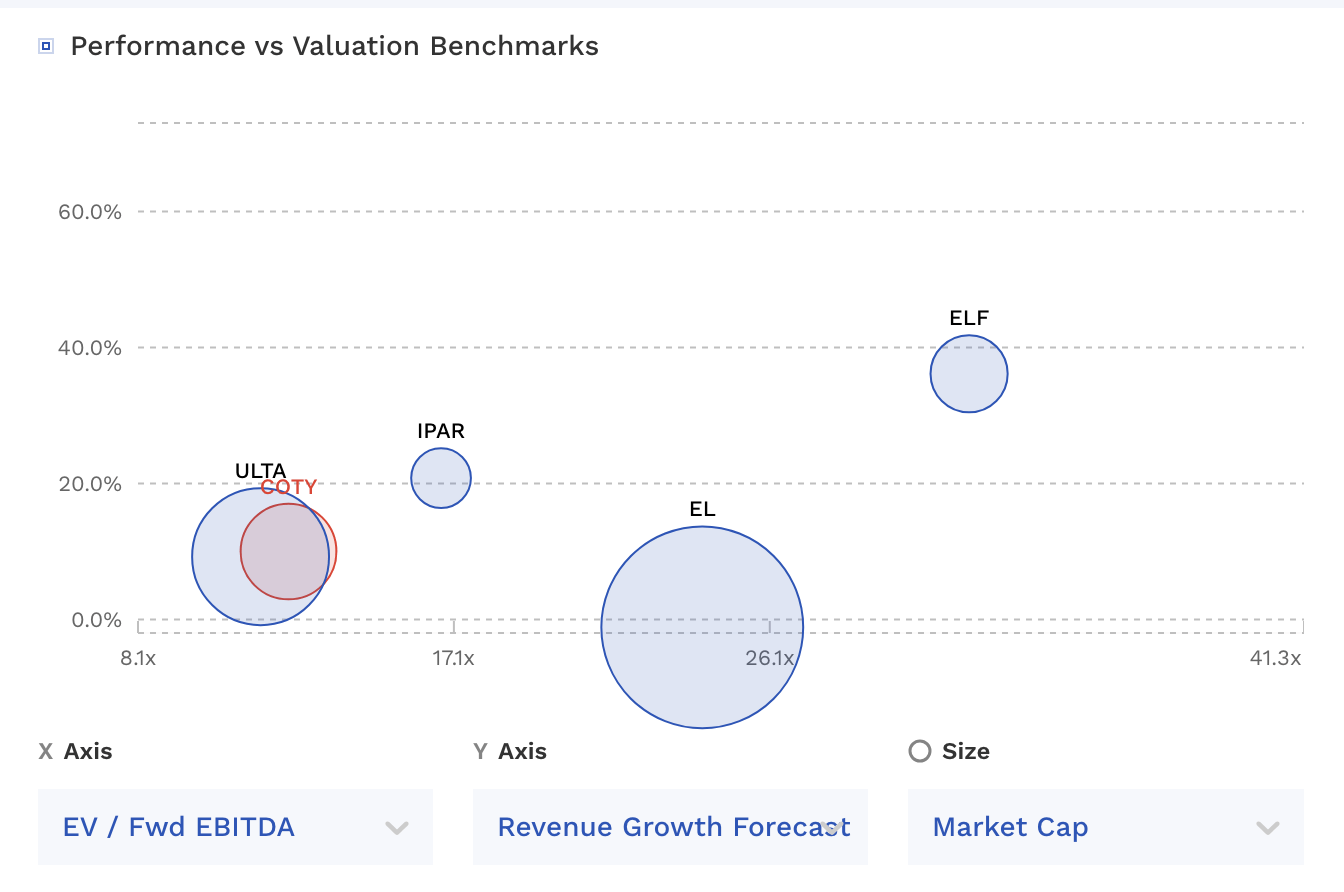

COTY stock trades around 12.5x the FY2024 (ending June) consensus EBITDA of $1.09 billion and 11.6x the FY2025 consensus of $1.18 billion.

It trades at a forward P/E of 28.5x the FY24 consensus of 40 cents. Based on 2025 analyst estimates of 55 cents, it trades at 20.7x.

COTY is projected to grow revenue by 10% this year and 5.6% next year.

Outside of retailer Ulta ( ULTA ), COTY remains the cheapest beauty company is the space. Its higher leverage and past mistakes remain the most likely reasons.

By comparison, the struggling EL trades at 24.5x fiscal year '24 (ending June) EBITDA of $2.17 billion and 17.3x estimates of FY25 EBITDA of $3.08 billion. EL is projected to see a -1.2% decline in revenue this year, and it badly missed sales estimates when it reported its FQ1 in November.

{kind=link}

COTY will reduce its share count by 27 million later this fiscal year at the cost of just over $235 million. It should generate an FCF of about $400 million. Taking that into account, and placing a 16x multiple on the stock's FY25 EBITDA, I get a target price of $17.50.

Conclusion

I continue to believe that COTY is not getting the respect it deserves under CEO Sue Nabi. The fragrance and cosmetic company's sales growth has been outstanding under her leadership, while its debt reduction plan is on schedule. There is no reason in my view why the stock should be trading at such a large discount to its peers, especially the struggling EL.

The prestige fragrance market has been strong, with no signs of letting up, and COTY clearly has gained some share, as evidenced by its sales easily outpacing the market. The biggest risk to the stock is a slowdown in the category, and its competition picking up their games. Meanwhile, there has been talk of Gucci wanting to buy back its license and Kim Kardashian wanting to re-acquire the 20% stake she sold in SKKN, but I view those more as headline risks at this point. Gucci would be the bigger loss, but it would have to pay up to get its license back early, which would only help in COTY's deleveraging.

All in all, I continue to rate COTY a "Strong Buy."

For further details see:

Coty: Strong Execution Continues