COTY - Coty: Upping Price Target

2023-07-12 04:48:03 ET

Summary

- Coty has raised its Q4 revenue growth forecast to 12-15%, up from 10%, attributing the increase to momentum in the Prestige category and recovery in China.

- The company aims to double its sales in China to over $600 million in the next few years and increase its Retail Travel business by 50% to more than $600 million in sales over the next three years.

- Despite some concerns about Coty's reliance on licensed brands, the company's stock remains a "Strong Buy" with a new target price of $18, up from my previous estimate.

Cosmetic company Coty ( COTY ) continues to perform nicely since my initial write-up in early February, up nearly 30% versus a 7% increase in the S&P over the same time period. I placed a "Strong Buy" rating on the stock at the time, calling it a strong turnaround and deleveraging story.

Company Profile

As a refresher, COTY is beauty company that sells fragrances, color cosmetics, and skin and body care products. It has a portfolio of owned and licensed brands in both the mass and prestige categories. It also owns a stake in haircare business Wella, which owns brands such as Clairol, Wella, and OPI. However, COTY is in the process of winding down its stake in Wella.

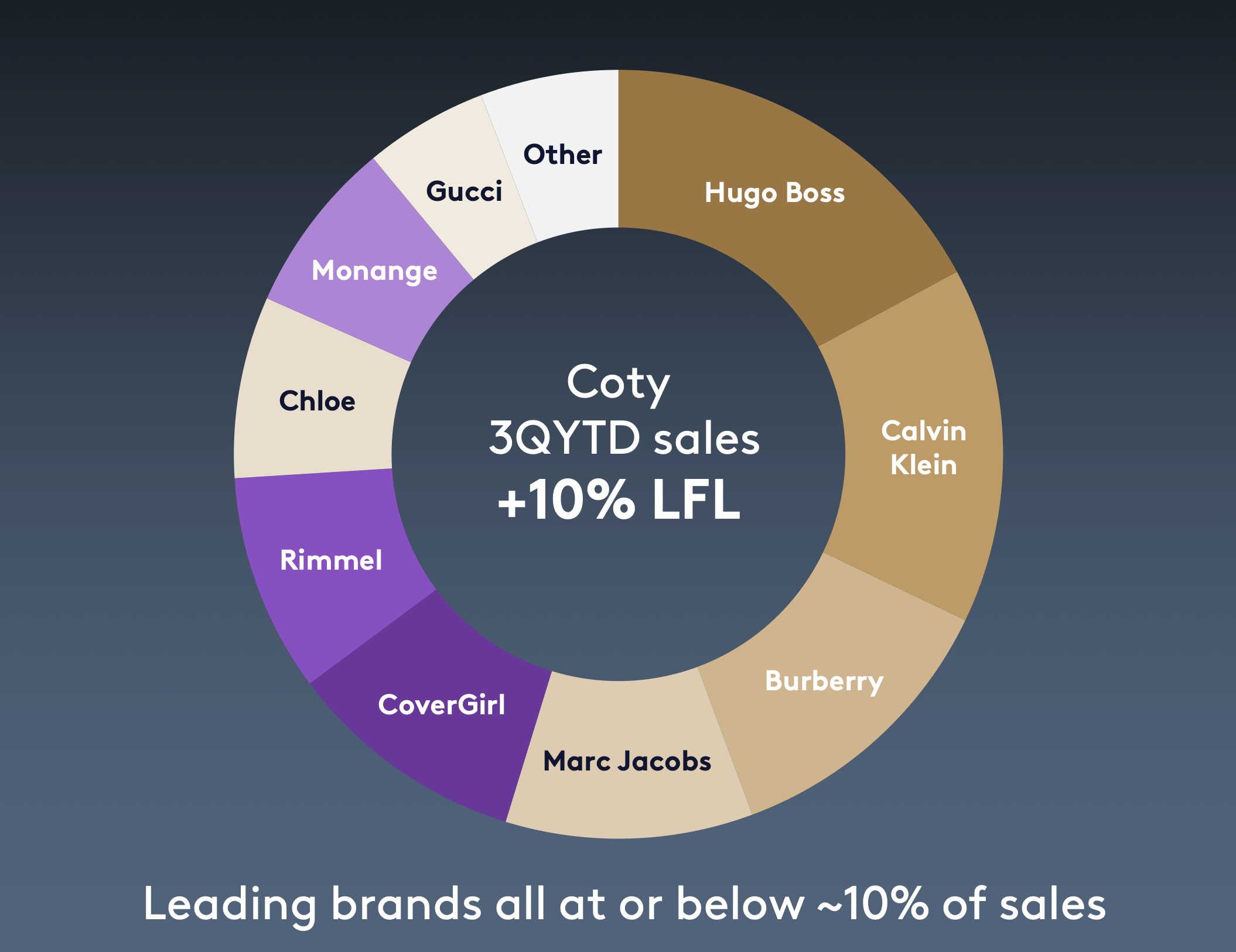

Its owned brands include CoverGirl, Max Factor, Rimmel, Sally Hansen, Lancaster, and philosophy. On the licensed side, it has licenses with Calvin Klein, Gucci, Burberry, Tiffany,, and Hugo Boss, among others.

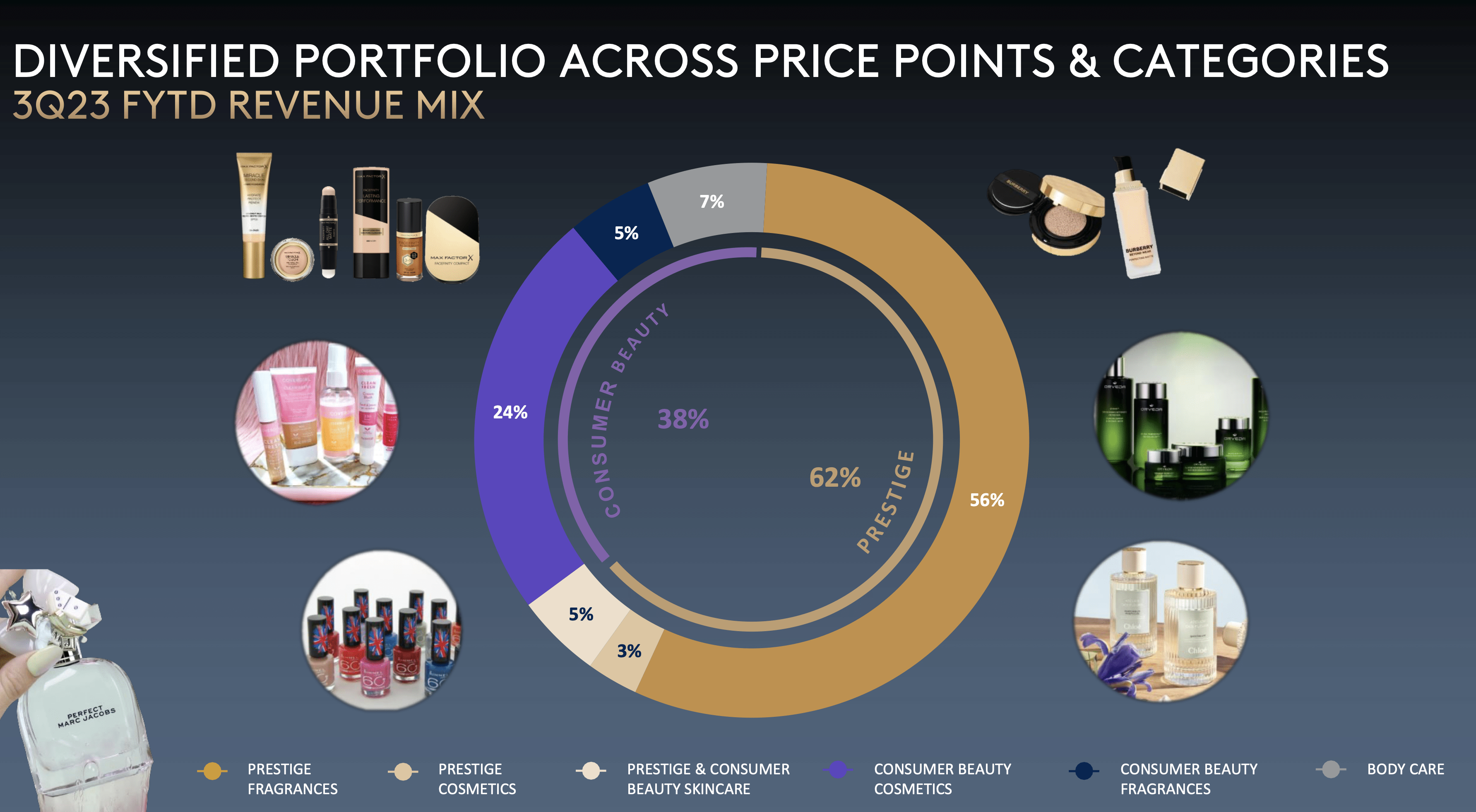

Prestige is about 62% of its revenue, while mass is 38%. Prestige fragrance, meanwhile, is about 56% of sales. North America accounts for 30% of its sales, while western Europe is 26%, Eastern Europe 18%, APAC 6%, China 4%, LatAm 8%, and global travel 8%.

{kind=link}

Guidance Raised and Investor Day

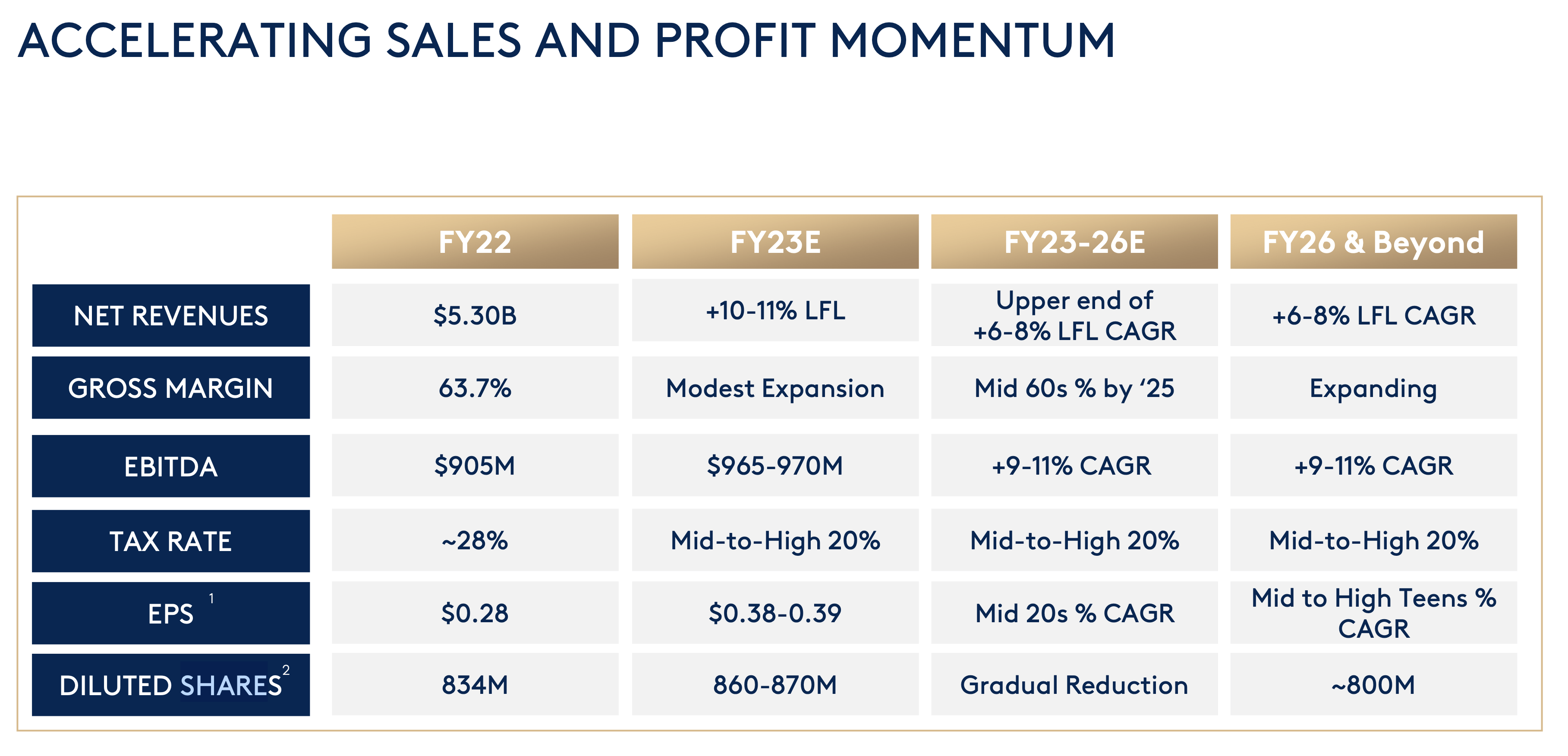

Ahead of its analyst day in Paris, as it looks towards a dual listing on the Paris Euronext Exchange, COTY upped its fiscal Q4 and full-year revenue and EBITDA guidance. The company now expects 12-15% like-for-like revenue growth in fiscal Q4, up from prior guidance of 10% growth. The company credited momentum in the Prestige category as well as a recovery in China for its increased outlook.

The company also raised its full-year EBITDA guidance. It now expects adjusted EBITDA to come in between a range of $965-970 million, up from prior guidance of $955-965 million.

{kind=link}

In my original write-up, I noted that at the time being under-penetrated in China was good thing given the Covid-related lock-downs, but that the company was smartly looking to attack the market. At its investor day, China was a big focus for the company.

On the investor call, CEO Sue Nabi said:

The 2 areas (China and Travel Retail) which represent the next legs of outsized growth for the company, where economic factors in China steadily improve. We remain as confident as ever in the structural drivers, which will drive outsized beauty growth in China for the many years to come. Number one, China per capita beauty consumption is still less than half of mature markets like U.S. Europe, Japan or Korea. Number two, while China's beauty market continues to be dominated by skin care, demand for prestige fragrances and mass fragrances has increased by over 60% versus 3 years ago, growing at 1.5x the growth of the overall beauty market. Number three, fragrance are now over 10% of China's beauty market and Chinese consumers continue to gravitate towards the most premium fragrances, even more than Western consumers. So the beauty opportunity for Coty in China is immense. Against this very attractive market backdrop, our business in China is still small at 4% of our revenues. However, we have been scaling our China business very quickly and building out our footprint in the market. …. Our ambition is, therefore, to more than double our China sales in the next few years to over $600 million."

Nabi noted that the company has greatly expanded its presence in China over the past two years, growing to 400 cities, with its prestige counters in 130 doors and its consumer beauty products in over 38,000 doors. It also now has 18 e-commerce stores in the country for its various brands. However, Nabi noted that this footprint is still just a fraction of some larger players and that it's just introducing its skin care and ultra-premium fragrance products to the country.

In addition to China, COTY is also looking to increase its Retail Travel business by 50% over the next three years to more than $600 million in sales. The company said that pre-Covid most of its sales in this category were prestige fragrance, but that prestige skin care and cosmetics will are helping drive growth. Meanwhile, as travels return, the category has grown 30% year to day, with Nabi saying there were no signs of its slowing down.

Brazil is another area of growth the company brought up, saying that this is the biggest opportunity for its mass fragrance business. Brazil is the largest mass fragrance market in the world, and COTY just launched its mass fragrance portfolio in 2,000 doors. It sees an opportunity of getting into 15,000 locations, so there is a lot of white space ahead it.

While most analysts came away from COTY's presentation bullish, JP Morgan, which has missed out on the COTY rally, was an exception. Analyst Andrea Teixeira cited the company's reliance on licensed brands in her argument, writing :

"It remains a top concern in particular as Gucci is an important part of the portfolio and its brand owner (Kering, covered by Chiara Battistini) has been investing more in beauty through acquisitions and new hires. Contracts can be renegotiated and break-up fees are not unheard of in the industry if Kering decides to unwind the contract."

She also said that COTY's traditional brands like Covergirl, Max Factor and Sally Hansen were struggling to attract younger consumers. Generally, though, its mass brands have been seeing stable to slightly growing market share.

Now Gucci did recently buy fragrance maker Creed , so it very well could look to bring that business in house. But it should be noted that Gucci is COTY's 9th largest brand. It should also be pointed out that none of its top licenses are up for renewal before the next 5 years, with the majority running longer. In fact, its top-7 licenses don't expire for another 11 years on average. COTY said there is no early exit mechanism in its licenses.

{kind=link}

Yes, Gucci could buy out the license, but it likely won't be cheap to do so, which would help COTY in its deleveraging process. Notably, COTY also appears to be doing well with the Gucci brand, with Gucci makeup sales growing over 30% faster than the category growth in the U.S.

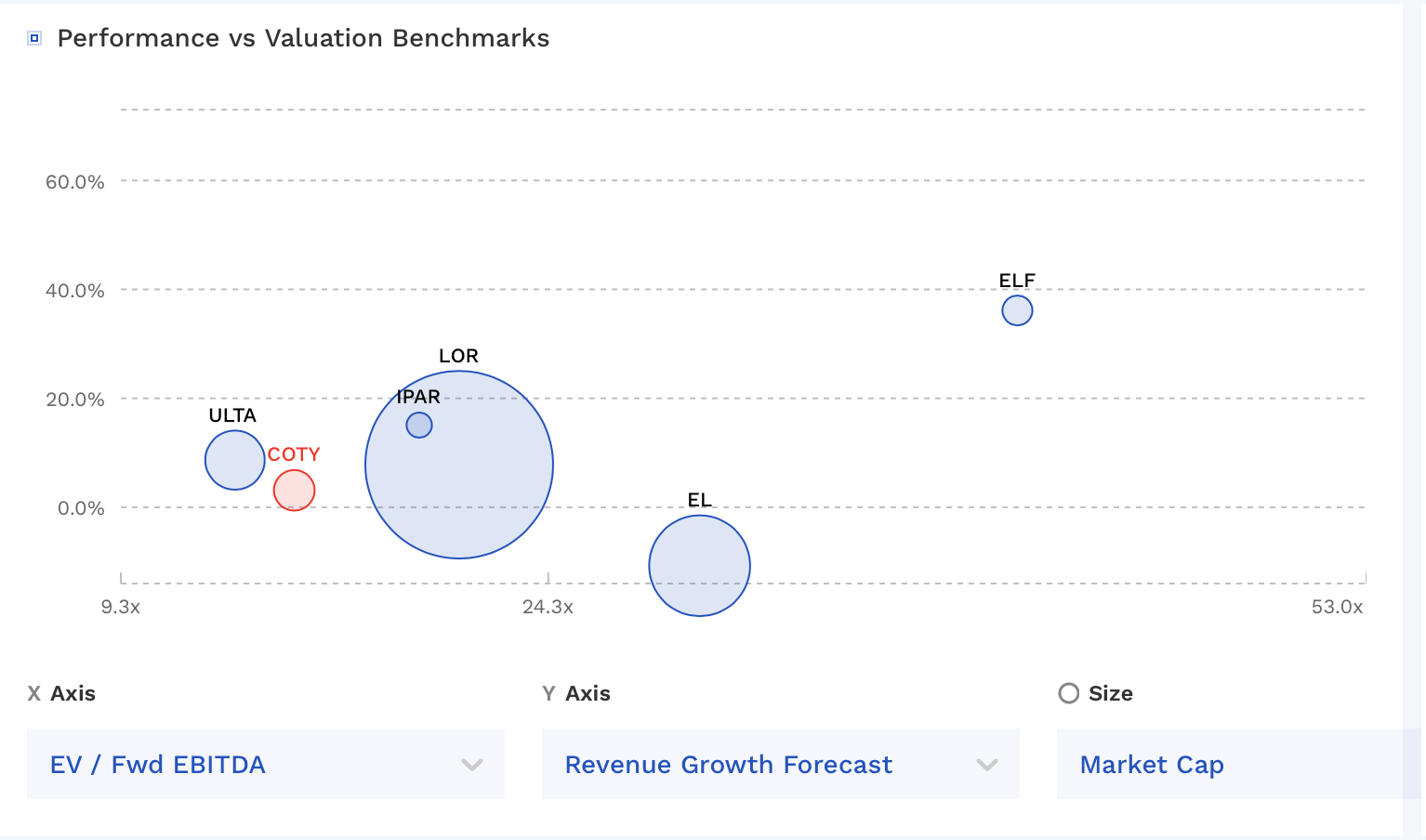

Valuation

COTY stock trades around 13.8x the FY2024 (ending June) consensus EBITDA of $1.07 billion and 12.6x the FY2025 consensus of $1.17 billion.

It trades at a forward P/E of under 27x the FY24 consensus of 48 cents. Based on 2025 analyst estimates of 58 cents, it trades at over 22x.

COTY remains the cheapest beauty company is the space outside of retailer Ulta Beauty ( ULTA ). Notably, retailers usually trade at a pretty nice discount to brands.

COTY Valuation Vs Peers (Company Presentation)

{kind=link}

Conclusion

COTY has executed nicely since I placed a "Strong Buy' rating on the stock back in February. The stock remains one of the cheapest in the space, and the deleveraging story has yet to fully kick in. The company also has a future $200 million buyback in place at prices below $7.50 after it locked in swap agreements with banks last year. This out-of-the box move looks like it will pay off in a big way. A dual listing, meanwhile, should only increase the investor base for the company.

I'm going to raise my target price to $18, which is an under 16x multiple on FY25 EBITDA estimates, after $500 million in debt reductions from here. That multiple is still well below the 20x-plus multiple that peers currently trade at. The stock remains a "Strong Buy."

For further details see:

Coty: Upping Price Target