EQIX - Could Equinix Make A Potential Short Leg Of An AI Pairs Trade?

2023-07-11 07:39:35 ET

Summary

- Data center REITs are thought of as key infrastructure for the roll out of AI, but this thinking is flawed.

- Their position within the AI supply chain results in low pricing power and high maintenance costs which inevitably lead to sub-par results.

- I investigate the possibility of constructing an AI pairs trade with Equinix forming the short leg of that trade.

Dear readers/followers,

It's been a while since I first wrote about Equinix REIT ( EQIX ). As many of you know, I like to invest in key infrastructure, which is what initially drove me to investigate datacenter REITs further.

In light of the ongoing AI boom, investing in data centers that represent important infrastructure for the industry seemed like a good idea. Despite this, I issued a HOLD rating because I wasn't seeing meaningful upside above the already high 25x AFFO. (Note: I'll be using AFFO, which includes maintenance CAPEX, which as you'll see later is very high for data centers)

Since the middle of February, which is when I published the original article , the AI craze has intensified, sparking a major rally in big tech. Companies such as Nvidia ( NVDA ) and Microsoft ( MSFT ) have returned astonishing returns of 100% and 25% respectively, while Equinix has returned a mere 6%.

Moreover, it seems that this underperformance of Equinix wasn't a coincidence as a major competitor Digital Realty Trust ( DLR ) has returned only 3% over the same period.

This naturally led me to question my initial thesis that data centers represent key and necessary infrastructure for AI.

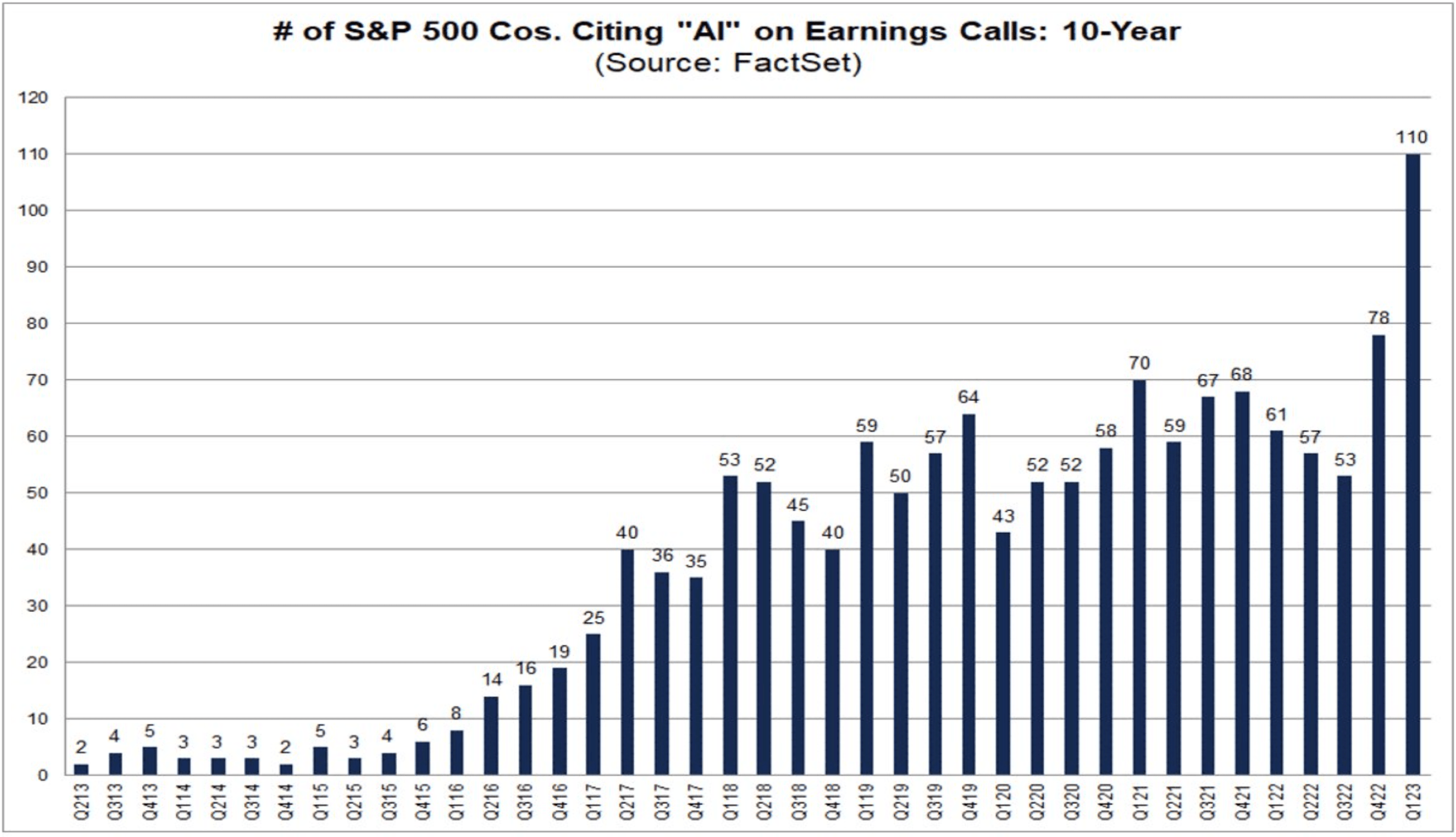

After all, datacenter related stocks are barely going up during a period when AI is the topic in town and everything everyone talks about, as evident from an all-time high number of management teams citing AI on their earnings calls.

{kind=link}

If these bullish tailwinds aren't enough for data centers to at the very least beat a broader market index, which has returned 7% over the period, one must wonder if they're actually as critical to the industry as we thought.

Updated thesis

That brings me to my updated thesis which I have developed through not only studying Equinix and its competitor in more detail but also especially by studying big tech companies such as the above-mentioned Nvidia and Microsoft that surround datacenter REITs in the AI supply chain.

In short, the AI supply chain starts with chip makers that design and manufacture the chips needed. These chips then get put together into powerful servers/computers that are housed in data centers and leased to software operators that develop and run the AI software and sell the output to end users. Importantly, the REIT is responsible for acquiring and maintaining the servers.

Understanding this dynamic is important because it reveals how badly positioned data centers actually are in the supply chain as their margins are getting squeezed from both sides, while they incur most of the costs directly.

Chip makers are high value add businesses and have a lot of pricing power. That means expensive chips for data centers and with new technology being rolled out very fast, the maintenance CAPEX that data centers have to incur just to stay competitive is immense.

On the other side, the tenants of data center REITs tend to be big tech companies and often occupy a large portion of a given data center REIT's space (i.e. not that much tenant diversification for the REIT), which gives the tenants a lot of bargaining power and keeps rents low.

This inevitably puts data center REIT in a tough spot. The upside is largely consumed by those that come earlier or later in the supply chain, while data centers get stuck with the expensive bill to pay for server acquisition and maintenance.

Having said that, I will not be investing in data centers, but I believe EQIX is worth another look because it could make an interesting short leg of a pairs trade on AI.

The idea is to buy a stock that has significant upside if the AI run continues and partly hedge the downside by shorting EQIX which is unlikely to go much higher in the AI trend continues and could get hurt and re-rate to a lower multiple if the AI trend dies down.

Equinix seems to be the best candidate for a potential short in the data center space because it trades at a much higher multiple compared to DLR (25x AFFO vs 19x AFFO).

For completeness, before diving into company-specific metrics, I want to touch on two positive industry factors that are going to make occupancy of data center REIT quite sticky and could represent a risk to our potential short.

- Tenant retention in the industry is high, above 90%, because data migration from one facility to another is very costly.

- High-margin big tech companies that are currently leasing their computational capacity are unlikely to want to get involved in low-margin and capital - intensive data center businesses themselves because they generate a significantly higher return by investing their money elsewhere.

Equinix

In my mind, my updated thesis for the data center automatically disqualifies the company as a buy at the current price.

The goal now is to determine, whether EQIX could make a good short. So let's focus on a handful of metrics that can help us determine exactly that.

Operational performance

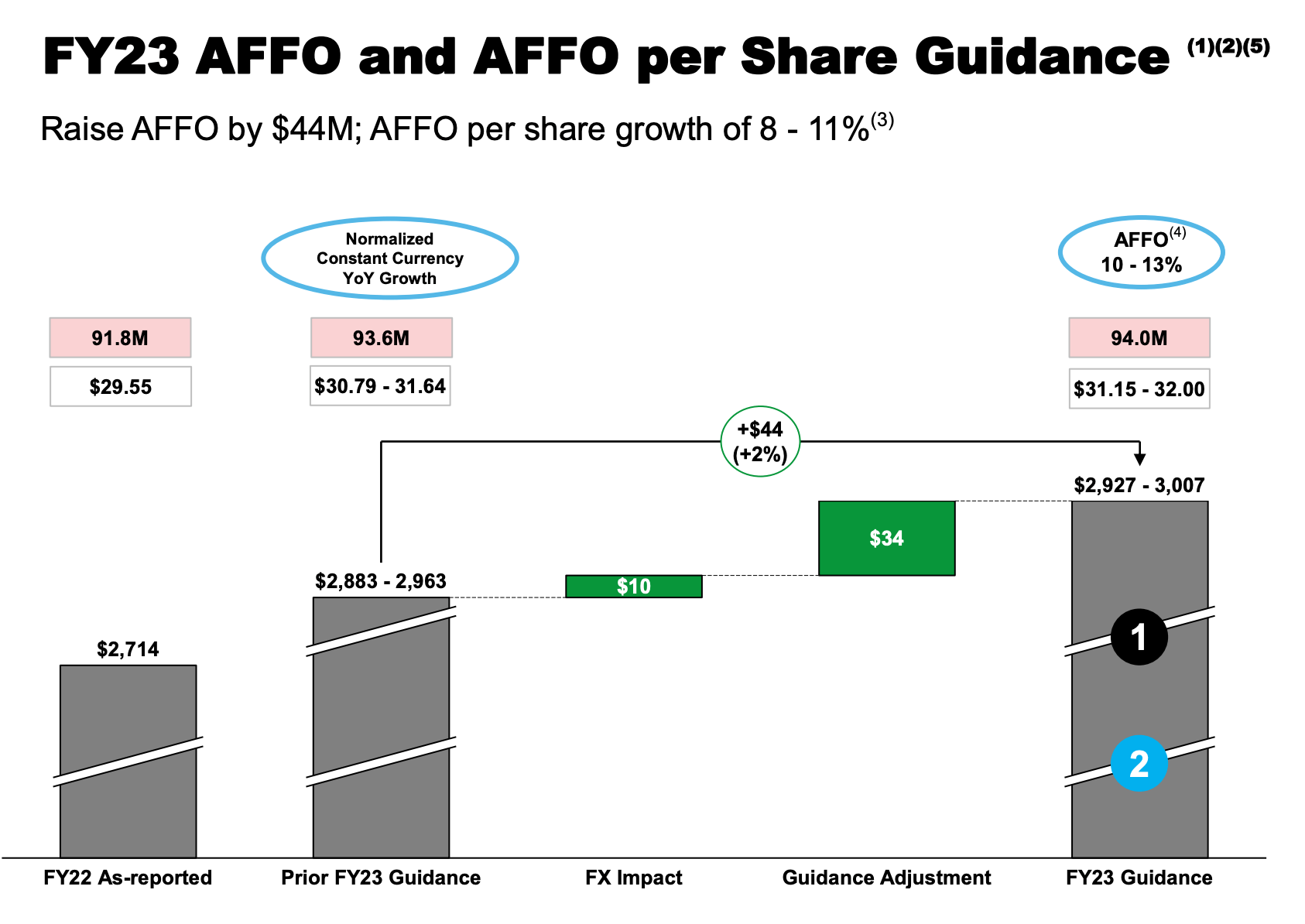

First quarter results have been very good. Revenues as well as adjusted EBITDA grew by over 15% YoY and AFFO per share came in above the top end of guidance.

Strong operational performance led to a 2% upwards adjustment in full-year guidance to an AFFO per share of $31.15-32.00, up 7% YoY at midpoint. And the consensus is generally for high single-digit growth to continue into 2024 and 2025.

{kind=link}

Dividends are expected to grow by around 10% and reach $13.64 per share for the full year, representing a dividend yield of 1.77%. Though low, it corresponds to a very low payout ratio of just 43%.

These are clearly great results, but the market has barely noticed as the price has been flat. Nonetheless, from an operational perspective, the company is doing well.

Balance sheet

From a financial standpoint, things are stable as well.

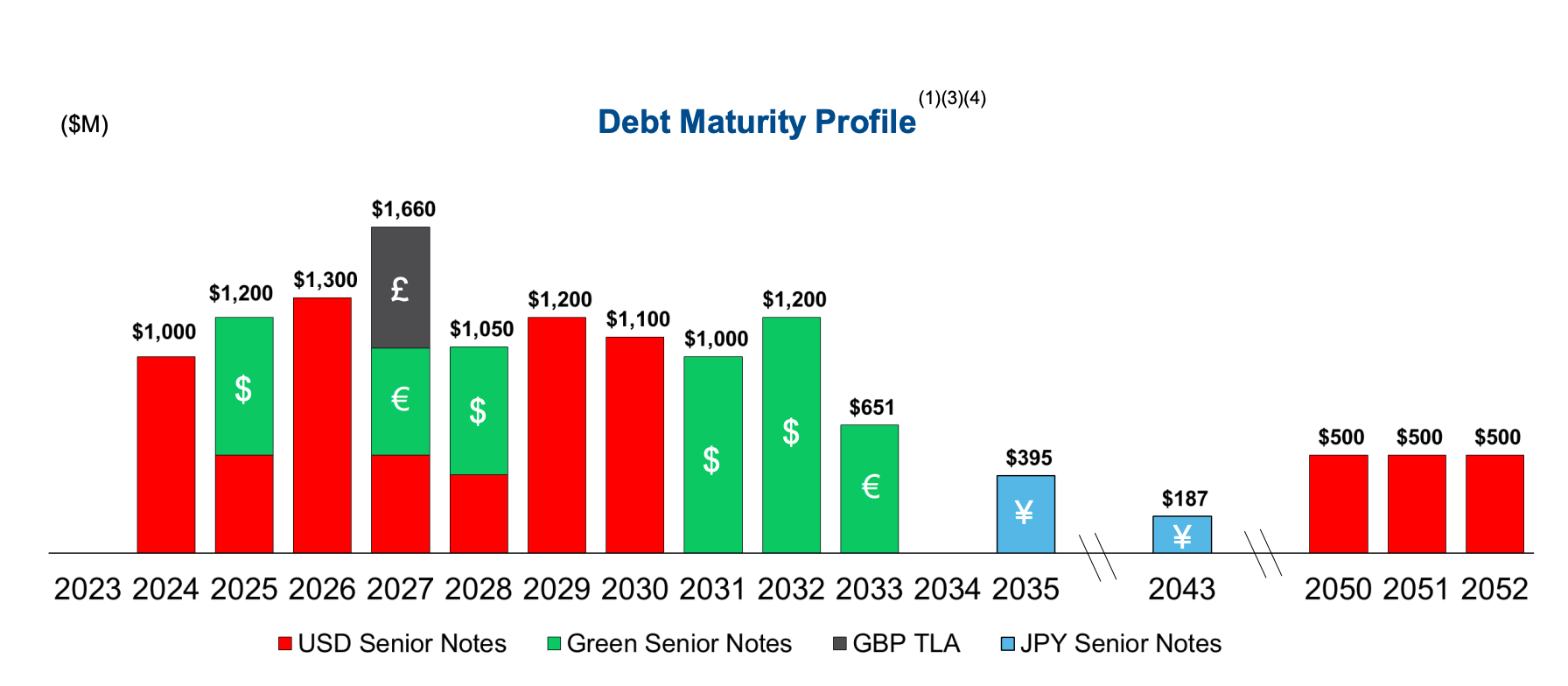

Equinix has a BBB-rated balance sheet with 96% of the debt fixed and a long weighted average maturity of 8.4 years. This translates into a debt profile that's well spread over time, with relatively low maturities of just above $1 billion each year, well manageable with annual AFFO of around $3 billion.

{kind=link}

Valuation

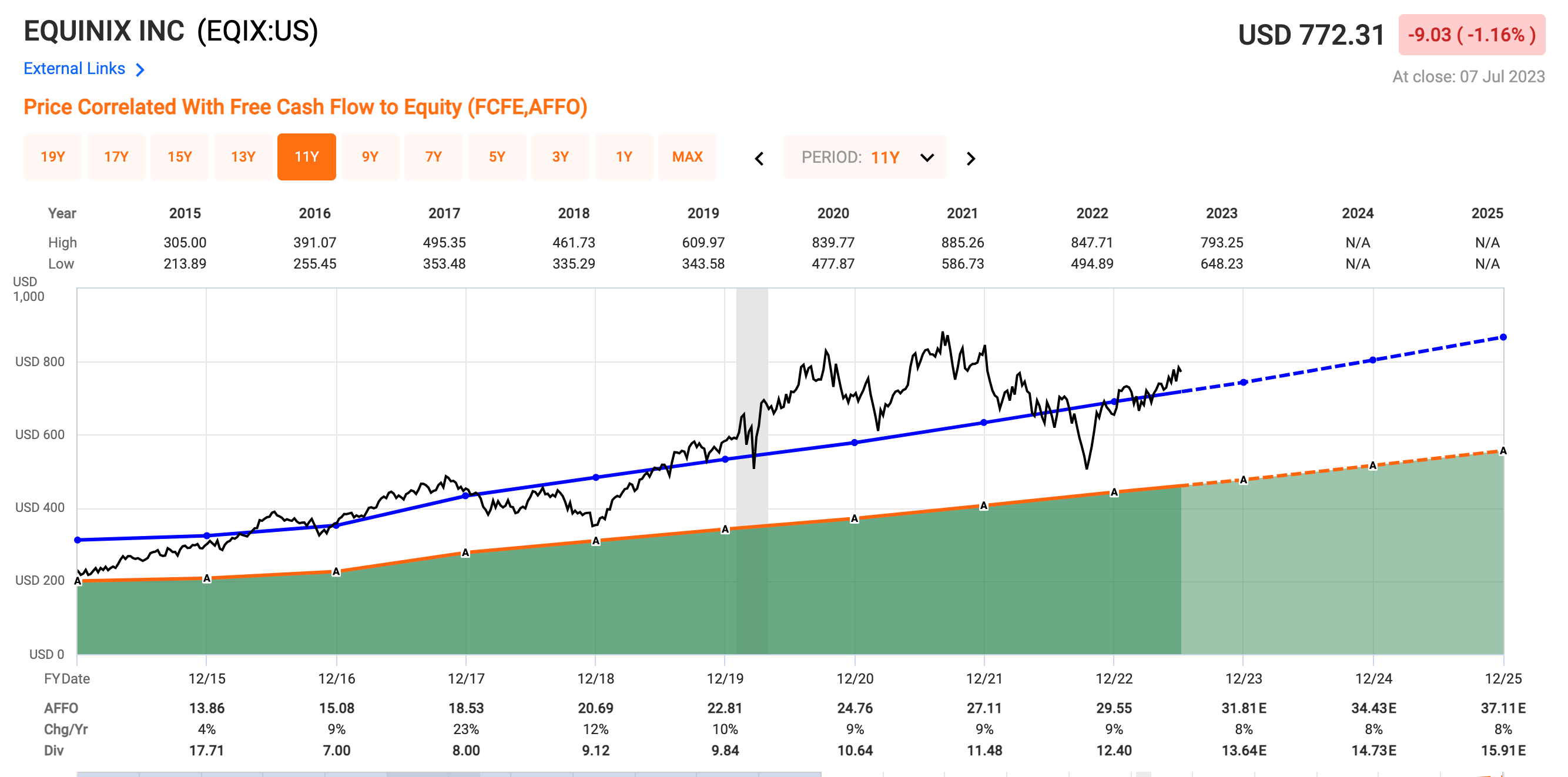

So really it all comes down to valuation and market price action. The price has rebounded sharply from the October low but hasn't responded to Q1 results or the latest AI boom which could indicate a lack of excitement around the stock.

Equinix is also pricey at 24.3x forward AFFO. Over the past decade, the stock has traded as high as 30-33x and as low as 17x with an average of around 23x.

{kind=link}

Compared to peers, the stock does trade at a premium, especially compared to DLR at 19x AFFO.

With that said, assuming that management delivers on the growth forecast and grows AFFO per share to $37 by 2025, let's assume three scenarios for the exit multiple:

- Rates remain elevated and AI hype continues (aka the status quo). In this case, the stock will likely continue to trade around 25x AFFO which would correspond to a price target of $925 per share or around a 20% upside .

- Rates decrease and AI hype continues (aka the most bullish scenario). In this case, I think the stock could rerate to 30x AFFO once again, which would result in a price target of $1,110 per share or a 43% upside .

- Rates remain elevated and AI hype dies down (aka the moderately bearish scenario). In this case, I see the stock re-rating lower to around 20x AFFO. Moreover, in such environment, it would be near impossible to grow AFFO as much as forecasted. Assuming half the growth for AFFO corresponds to a price target of $690 per share, 11% downside from today.

By itself, the risk-reward isn't worth it for a short because there's a risk that the stock could go higher if the bullish scenario materializes.

When combined with a long on another stock, however, that eliminates the upside risk by growing more than EQIX in both the status quo and the bullish scenario, the short could provide some downside protection in the bearish scenario. That's why I rate EQIX as a "Sell" here with the caveat that I wouldn't short it in isolation, but only as part of the discussed AI pairs trade.

Now, for full transparency, I have not found a suitable long leg for the pairs trade, as all AI-related tech companies that I've looked at are currently too expensive for me to jump in. With that said, I'm happy to hear your suggestions in the comments below.

For further details see:

Could Equinix Make A Potential Short Leg Of An AI Pairs Trade?