VICI - Countercyclical Investment Opportunities For REIT Investors

2023-05-18 14:04:54 ET

Summary

- The economy is clearly slowing, if not contracting. REIT investors should consider pivoting to property sectors with stronger countercyclical performance.

- Top options for a slowing or contracting economy include health care and self-storage, though the oversold retail sector may present some opportunities.

- Despite excellent long-term drivers, industrial stands to see outsized losses in the coming months along with the highly pro-cyclical hospitality sector.

- These repositioning moves should not be overplayed, however. The economy spends vastly more time expanding than contracting, so the prudent investor will want to position for the long haul.

Commercial property owners face some daunting challenges, as I discussed in a recent article , which makes me bearish on REITs overall right now. A credit crunch is spiking just as property market conditions are softening - a deadly combination for many owners. Broad expectations of an economic downtown, if not a recession, portend even tougher times ahead, particularly in the office and multifamily sectors.

Economists have been predicting a recession for so long now that investors can be lulled into believing a downturn will never come. But signs of a near-term slowdown are unmistakable, if not quite ominous. Beyond the lackluster first-quarter GDP growth , consumer confidence has been slipping down to recessionary levels, a fairly reliable indication that spending will decline. Home prices are dropping.

On the business side, the Fed's latest Beige Book reports that both manufacturing activity and freight volumes are either flat or down in most regions of the country, while most other types of economic activity are softening. The small business optimism index remains well below its long-term average, and the net share of businesses that expect the economy to improve has dropped to a dismal -49%.

And the banking sector is playing its part in slowing the economy, taking the baton from the Federal Reserve. The Fed's latest Senior Loan Officer Opinion Survey on Bank Lending Practices found that banks report "tighter standards and weaker demand for commercial and industrial (C&I) loans to large and middle-market firms as well as small firms over the first quarter." The +50% net share of banks tightening standards for commercial loans is at its highest level since the Great Financial Crisis, starving firms of the capital they need to fund inventory, acquisitions, and other business purposes.

Recession Not Inevitable (Yet)

Overall, key indicators point to at least a slowdown in the near future, if not an outright downturn. But count me as a recession skeptic for now. There's just too much underlying strength in the economy to believe the bottom will fall out (unless the Federal government defaults on its debt in June, in which case all bets are off). Job openings remain historically high, while layoffs historically low. Job growth is normally a lagging indicator, so these indicators often don't begin to drop until we're already entering a recession. Still, the labor market is especially robust for this stage of the cycle.

Also critical: corporate and bank balance sheets remain quite healthy. And despite a recent uptick in household delinquencies , rates remain well below rates seen during the GFC. Most importantly, households still hold two-thirds of the excess savings they accumulated during the pandemic, according to Moody's Analytics estimates , equal to over $1.6 trillion or 8% of GDP. That's a lot of money under the mattress to keep consumers spending, even if layoffs do increase.

Still, the consensus call is for the US economy to enter a recession within the next year. The latest Wall Street Journal survey of economists , conducted in mid-April, pegs the probability at 61%, about the same as it's been since October 2022.

The economy will, indeed, eventually lapse into a recession - eventually - though even the bears keep pushing out their recession forecasts, calling into question the usefulness of these outlooks in making investment decisions. But here's the key insight: Though REITs certainly perform better when the economy is growing than when contracting, It may not matter much for how REIT investors position their portfolios whether the economy actually turns down or just slows without falling into a recession, as REITs usually perform similarly in both situations.

REITs in Thick and Thin

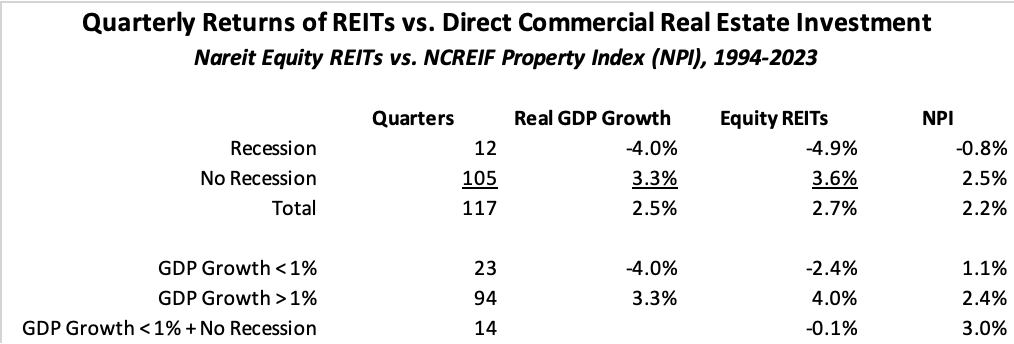

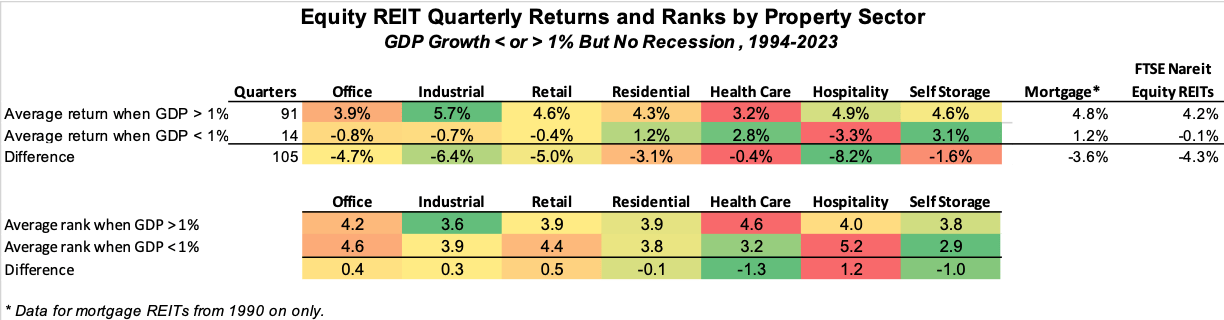

REITs generally outperform during expansions (when occupancies and rents rise) and sag during recessions (when operating performance falls). Since 1994, when Nareit started tracking performance by property sector, quarterly returns have averaged 3.6% during expansions but just -4.9% during recessions, and versus 2.7% overall. What about the slow growth scenario? In quarters when the economy grew by less than 1% but managed to avoid recession, returns averaged -0.1%. So, better than recessions but still well shy of stronger growth periods, as would be expected.

Nelson Economics analysis of data from Nareit, NCREIF, and the Bureau of Economic Analysis

{kind=link}

Given the forecast for slow growth at best for the remainder of 2023 and into 2024 - real GDP growth averages just 0.21% over the next four quarters in the WSJ poll and just 1.6% for all of 2024 - REIT investors should brace for rising vacancies, falling rents, and low or negative returns. Despite the common relief that REITs outperform direct CRE investment during a recession, my own research finds the opposite. REIT returns are more volatile than owning CRE directly, both when the economy is on the way up and on the way down, so REITs outperform during expansions and underperform during recessions, while outperforming overall. Redeploying some capital away from REITs can make sense for many investors comfortable with timing their investments.

But that's the overall REIT outlook. How should investors position their portfolios in the near term? For that, we look to the "quilt of returns."

The Quilt of Returns

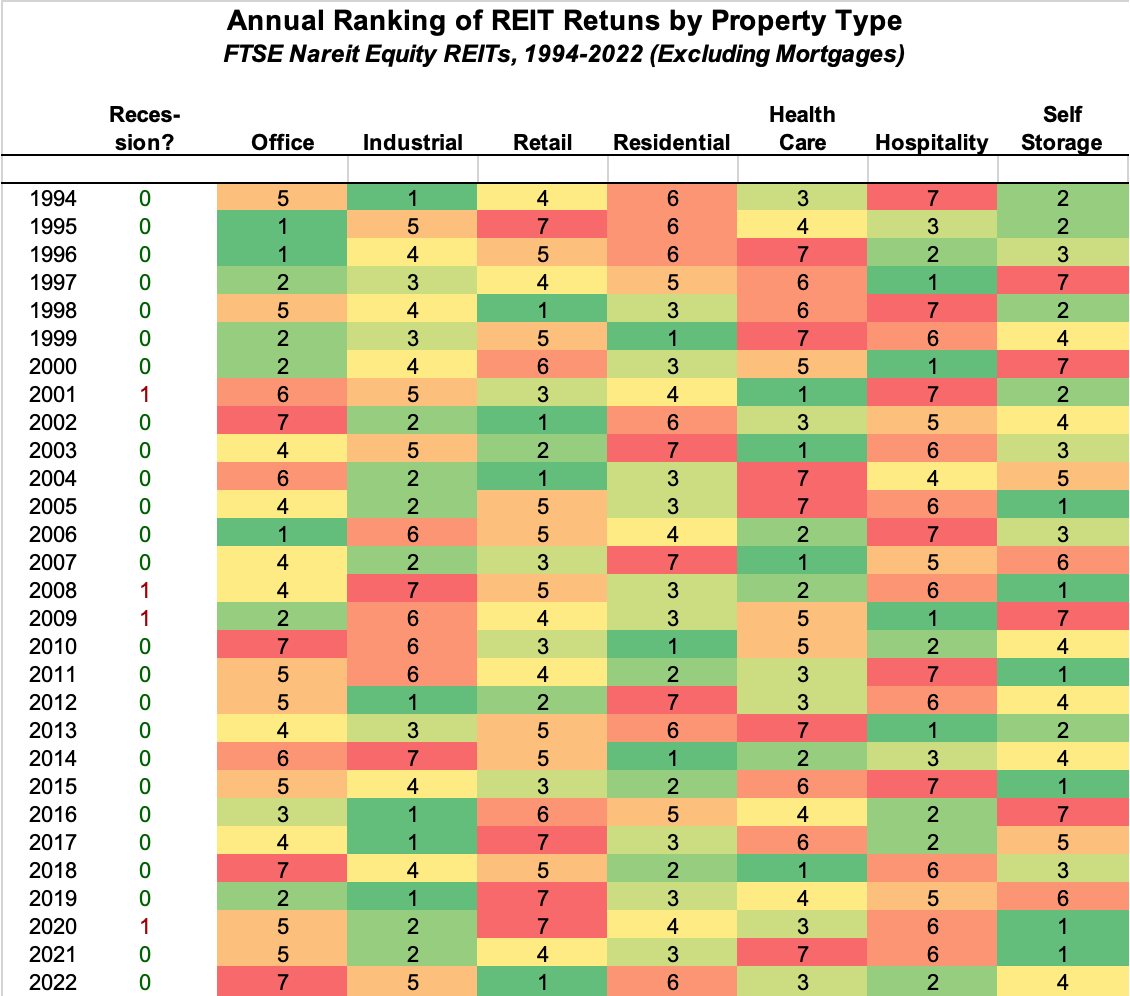

At any given time, different investment types will perform better or worse than others, and these patterns are in constant flux: what's up today may be down tomorrow, and no investments consistently outperform - or underperform. If we sort those asset types from highest to lowest in each period, and then plot those ranks in a chart with each ranking in a different color, what emerges is the multi-colored quilt of returns where the colors for each asset type rarely repeat from one period to the next.

So it is with commercial real estate. The property types delivering the best returns in any particular period - and those providing the worst returns - change frequently. This dynamic process is shown in the following graphic, where dark green represents the highest annual ranking and deep red the lowest, with yellow and orange in between. [Note that this graphic depicts annual ranking to simplify the presentation, but quarterly returns are a more precise measure to compare with GDP growth and are used in the analysis following].

Nelson Economics analysis of Nareit data.

{kind=link}

Some analysts attribute this process to "reversion to the mean," but that explanation doesn't fully capture the underlying dynamics. Property returns are based on both structural and cyclical trends. Structural trends reflect longer-term shifts in the underlying market forces. In recent years, office and retail have fallen out of favor, while industrial and multifamily have become investor darlings. Then, as one sector outperforms, investors pile into that sector, inflating prices and pushing down yields; the opposite occurs in out-of-favor sectors, as is happening now with retail. That's reversion to the mean.

But of particular interest now, as the economy looks to be slowing, is how different property sectors perform at various points in the business cycle: some do relatively better during downturns, and others do worse.

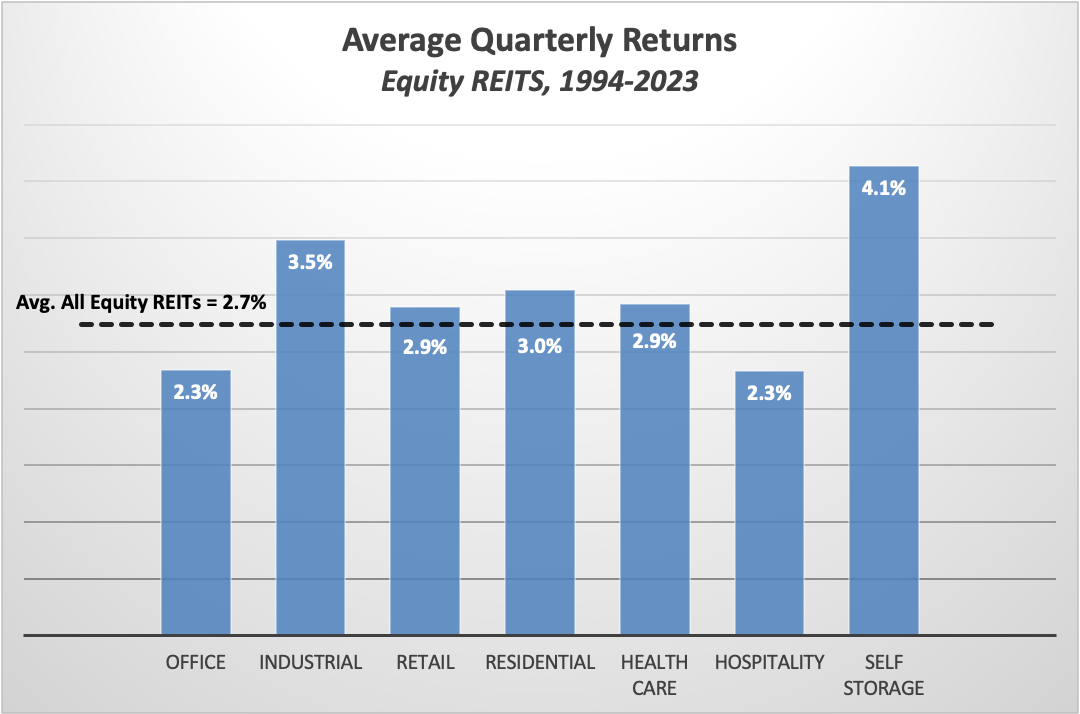

Over the last 30 years, quarterly returns on equity REITs have averaged 2.7%. Among property types, self-storage has been the top dog, with an average return of 4.1%, followed by industrial at 3.5%. Retail, residential, and health care all rank in the middle, with office (2.3%) and hospitality (2.3%) bringing up the rear. [Mortgage REITs are not shown because quarterly returns are available only back to 2000].

Nelson Economics analysis of Nareit data.

{kind=link}

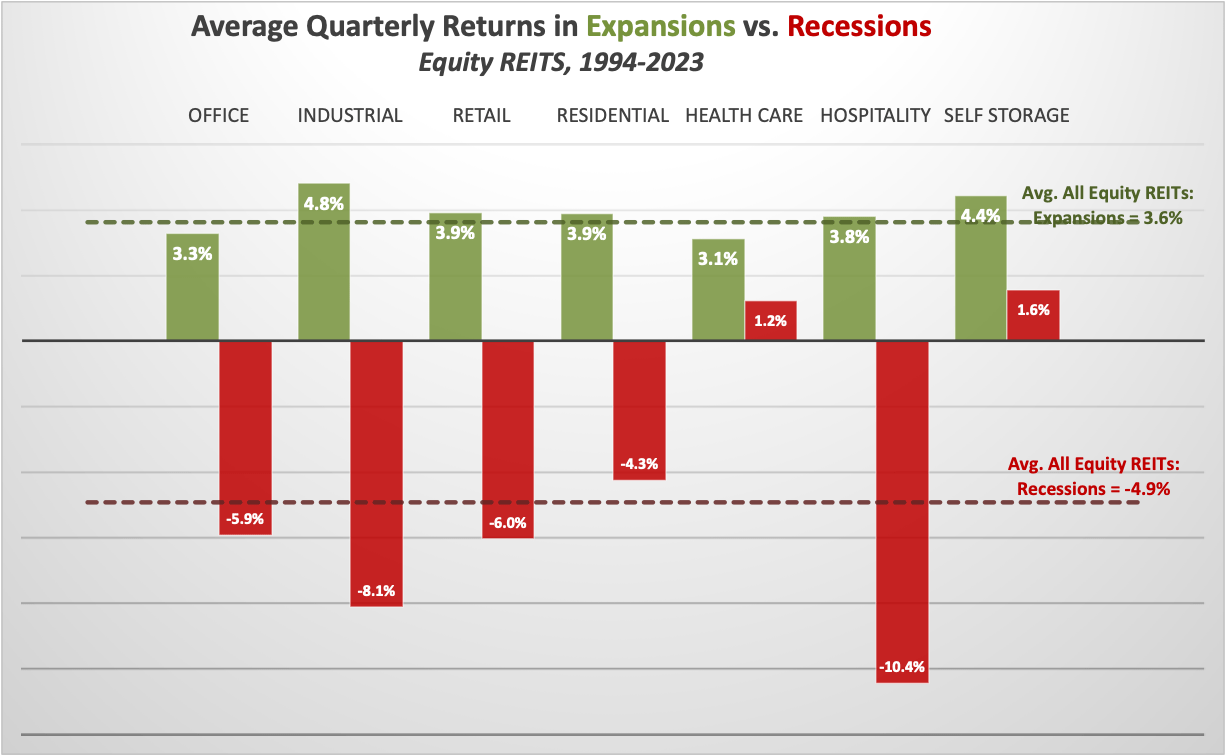

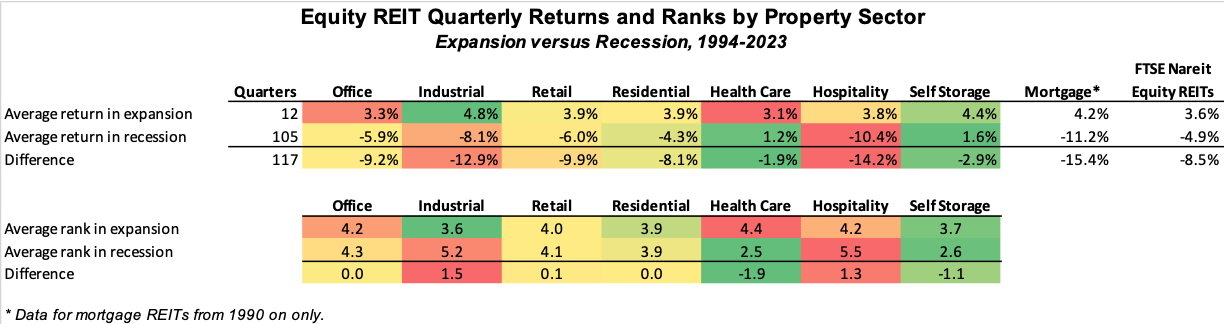

A much different picture emerges when separating the quarterly returns by when the economy is expanding versus when it is contracting, however, as shown in the following graph. Returns in expansion periods - shown in green - look similar to the patterns across all periods indicated above, for the simple reason that the economy is usually expanding. Of the past 117 quarters, the economy has been in recession in just 12 quarters, or 10% of the time. But the returns profiles are noticeably different during recessions. Self-storage remains the top performer, joined by health care as the only two sectors that generate positive returns in recessions. The pro-cyclical sectors that both outperform in expansions and underperform in recessions include retail, industrial, and especially hospitality. The beleaguered office sector underperforms in both up and down cycles, while residential slightly outperforms in both up and down cycles.

Nelson Economics analysis of Nareit data.

{kind=link}

In considering how to position your portfolio as the economy shifts down, another perspective is to consider the difference in returns between the growth and contraction periods within each sector. The hospitality and industrial sectors experience the greatest return declines; the mortgage REITs lose even more, though these figures are based on a more limited time series. While industrial has been on a long bull run and maintains excellent long-term drivers, the next few months may represent a good opportunity to sell to lock in some gains and redeploy later at a lower price point.

On the other hand, healthcare and self-storage stand out as being the most resilient in downturns. Importantly, these relative rankings also hold for slow-growth periods that avoid recessions. Well-regarded players in the healthcare sector include CareTrust REIT ( CTRE ) and Omega Healthcare Investors ( OHI ), while Life Storage ( LSI ) - to merge with Extra Space Storage (EXR) - and CubeSmart ( CUBE ) stand out in self-storage.

{kind=link}

Retail typically underperforms in recessions, but the sector was oversold during the pandemic after struggling under the growing threat of e-commerce for the decade before that, thus presenting value opportunities. Well-run REITs like Kite Realty Group ( KRG ), Regency Centers ( REG ), and Realty Income (O) may represent quality opportunities, along with Federal Realty ( FRT ), which operates best-in-class multi-use centers.

Slow Growth versus Negative Growth

And what happens if the economy slows to a soft landing but doesn't actually fall into a recession? The returns likely would still weaken, but not decline as much as in an outright recession. But the preferred portfolio reallocations would remain very much in line with the recession portfolio. Industrial and hospitality still suffer the greatest return declines and offer the lowest returns in my view, though neither sinks as much as they do in a recession. And self-storage and health care still provide the most resilient return potential. Overall, the rankings barely budge. Thus, investors preparing for a recession would be well positioned for outperformance, even if GDP doesn't ultimately contract.

{kind=link}

The Time to Pivot

These portfolio positionings are appropriate as the economy slows and we enter a recession (or not). But recessions typically last no more than two quarters, and as I highlighted in my last article , the greatest quarterly REIT returns - 15% on average! - are attained in the quarter before the recession ends, as investors anticipate better times ahead and begin to bid up prices. Thus, investors are advised not to get too comfortable in countercyclical portfolio plays. The economy spends vastly more time expanding than contracting, so the prudent investor will want to position for the long haul.

For further details see:

Countercyclical Investment Opportunities For REIT Investors