CPNG - Coupang: 2 Reasons For An Upside Revaluation In 2024

2023-12-28 11:07:28 ET

Summary

- Coupang's shares have disappointed in 2023.

- The acquisition of luxury goods retailer Farfetch Holdings could drive further revenue, EBITDA, and free cash flow growth for Coupang in FY 2024.

- The South Korean firm is seeing double-digit Y/Y revenue and customer growth. The Korean e-Commerce market is expanding rapidly as well.

- Coupang's shares are cheap relative to Amazon and have revaluation potential.

South Korean e-Commerce company Coupang (CPNG) has not met my return expectations in FY 2023 as the company's share price languished, despite improving operating fundamentals. The biggest drivers for a potential revaluation to the upside in FY 2024 are improvements in EBITDA margins as well as growth in free cash flow. Secondly, the e-Commerce company just announced the acquisition of online marketplace Farfetch Holdings, which could boost the company's positioning in the luxury goods market. I believe the acquisition could help drive further growth at Coupang in the coming year and shares of the South Korean e-Commerce company are cheap relative to Amazon's!

Previous coverage

I rated shares of Coupang a buy in June 2023 -- Coupang: A Top E-Commerce Growth Stock -- as I believed the company made rapid progress in terms of growing its customer base and revenues. Coupang did indeed show strong revenue momentum in the third-quarter, but investors have not yet been ready to reward the company's clear financial progress. I believe the recent acquisition of Farfetch Holdings could put Coupang back on the map with investors and together with solid execution in the core e-Commerce business, I believe Coupang has a good chance for an upside revaluation in 2024.

Growing core e-Commerce business

South Korea is not exactly the first e-Commerce market that comes to mind when investment opportunities in the space are discussed. The country is relatively small and has a population of only about 52M. However, Coupang, South-Korea's Amazon (AMZN) which is building a massive fulfillment center network and which is the country's largest online retailer, is growing rapidly… and it is showing in the company's financials.

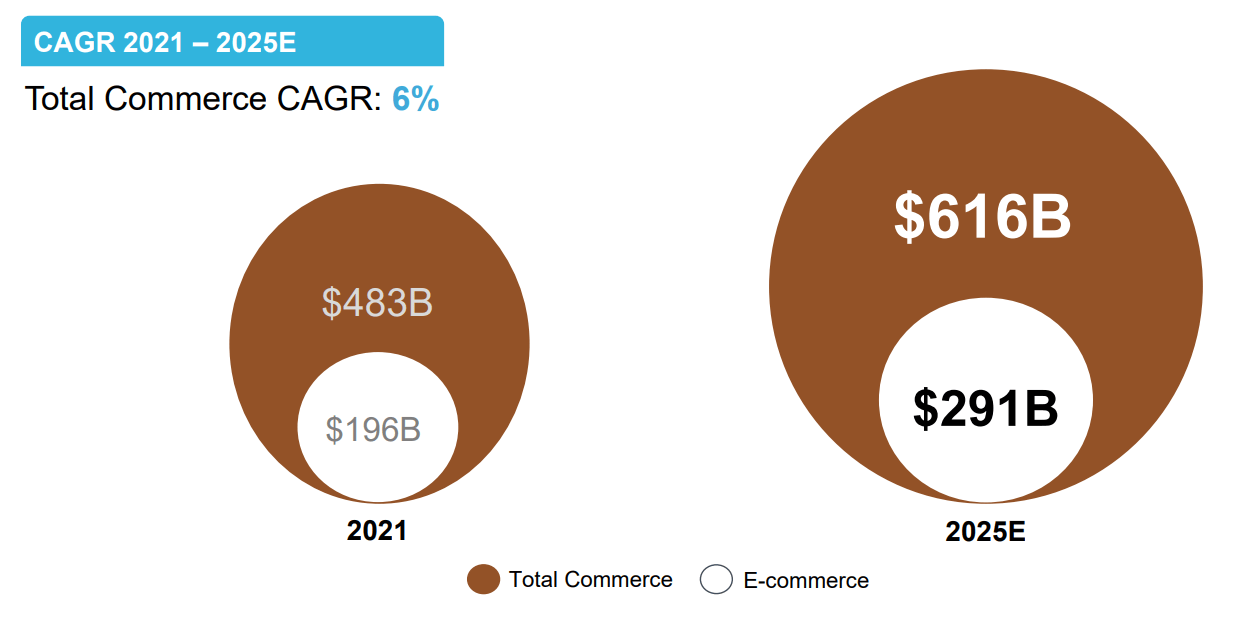

The South Korean e-Commerce market is expected to grow from $196B in 2021 to $291B in 2025, implying an annual growth rate of 10%. The share of South Korean e-Commerce sales in relation to total commerce sales is expected to rise from 41% in 2021 to 47% by the end of 2025. The e-Commerce market is still expected to grow a lot faster than the overall South Korean economy. Based off of Statista Market Insights projections , the South Korean economy is poised to grow at an average annual rate of 2% in the next five years. Therefore, Coupang's core market is growing three times as fast as the overall economy.

{kind=link}

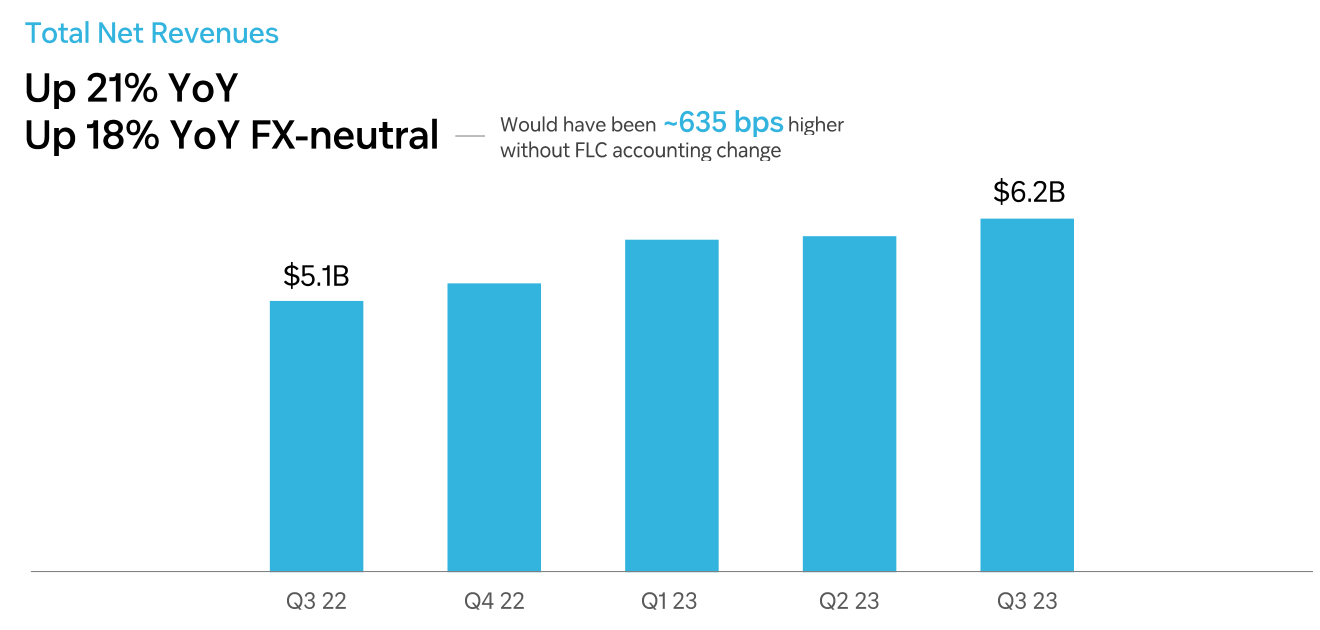

Online e-Commerce adoption and increasing spending are key drivers for Coupang's growth and the company's most recent financial results look very good. In the last year alone, Coupang's revenues soared 21% to $6.2B as its customer base expanded to 20M, showing a year-over-year increase of 14%. The majority of Coupang's revenues come from e-Commerce product sales: in the third-quarter these revenues amounted to $6.0B or 97% of consolidated revenues.

{kind=link}

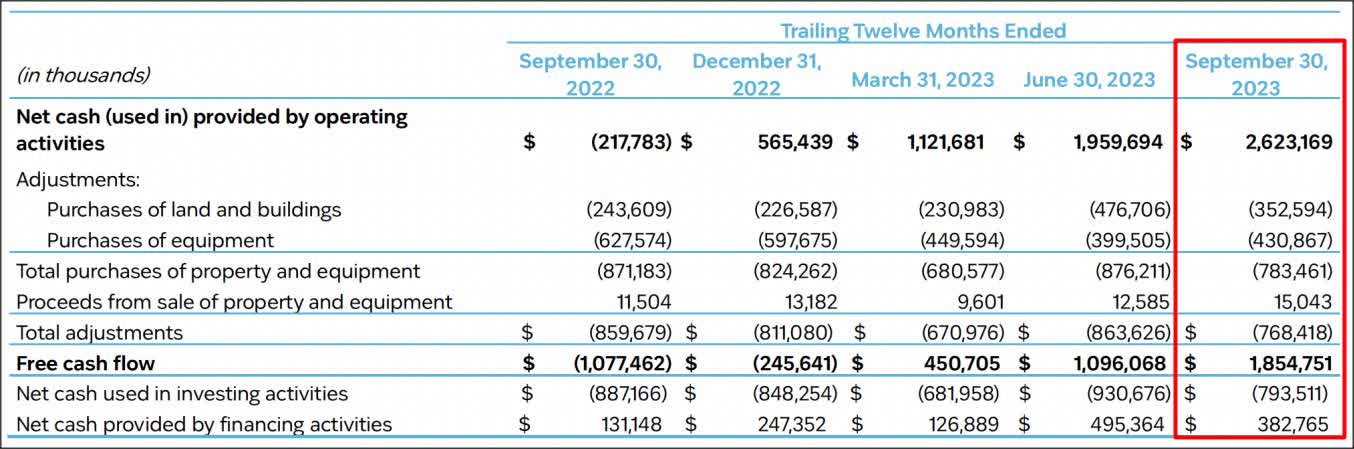

What makes Coupang stand out from the e-Commerce crowd is that the South Korean online retailer is already profitable in terms of free cash flow which not many e-Commerce companies can claim about themselves. Coupang generated $1.85B in free cash flow in the last twelve months on revenues of $23.15B which calculates to a rather impressive free cash flow margin of 8%. Amazon, for comparison, achieved a free cash flow margin of only 4% in the last twelve months ( Source ). Continual growth in free cash flow and margins, potentially related to the company's last acquisition may be a catalyst for a share price revaluation to the upside.

{kind=link}

Impressive EBITDA margin trend

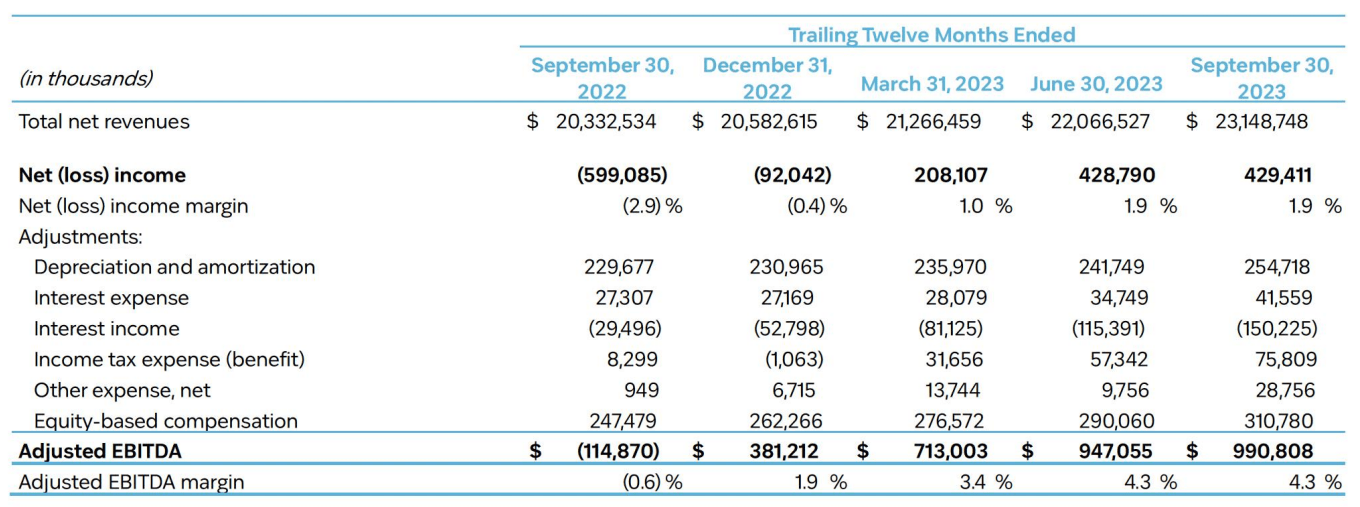

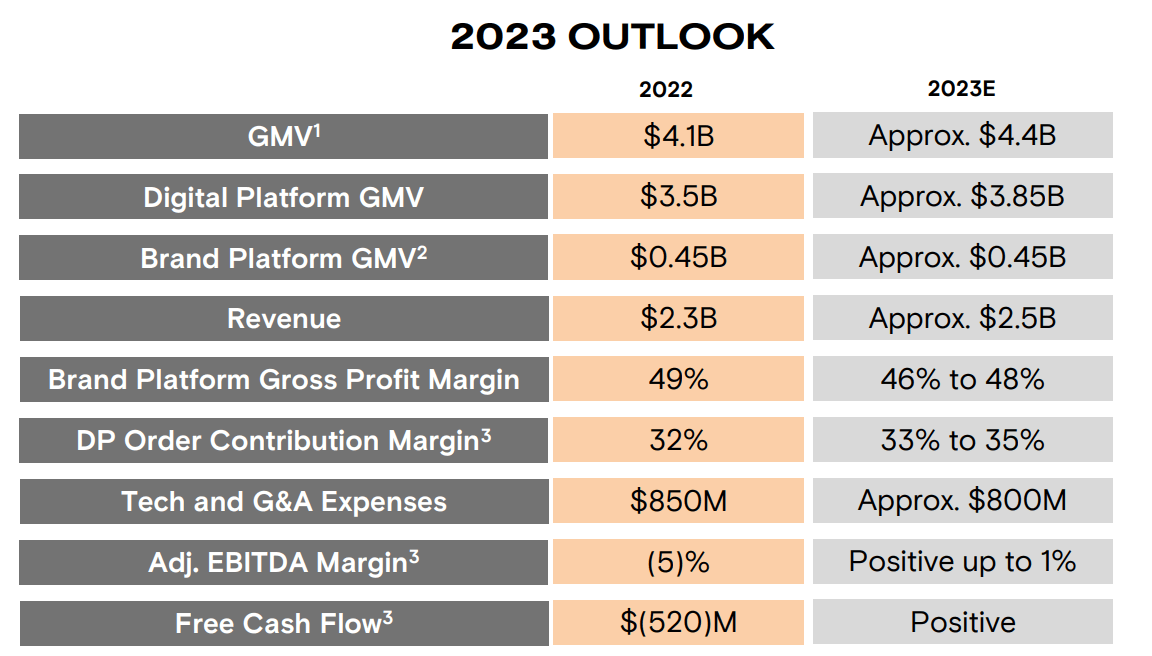

Coupang's EBITDA trend is also improving, chiefly due to more customers transacting on the e-Commerce platform. Coupang achieved an EBITDA margin of 4.3% in Q3'23 (on a twelve-month basis) compared to a negative margin of 0.6% in the year-earlier period. The company now has reached a scale at which it consistently reports profitability on both an EBITDA and net income basis.

{kind=link}

Acquisition of Farfetch Holdings

To accelerate its e-Commerce growth, Coupang announced the acquisition of U.K.-based retail firm Farfetch Holdings recently. Farfetch Holdings operates a global marketplace for the high-margin luxury fashion industry and therefore is a good strategic fit for Coupang to accelerate its growth and maybe even add incrementally to its free cash flow and EBITDA margins going forward (details have not yet been provided).

Farfetch Holdings expected, as of the end of the June quarter, to generate approximately $2.5B in revenues this year and projects positive EBITDA and free cash flow as well. Farfetch Holdings will receive $500M in emergency capital as the company has struggled to secure financing from other sources.

{kind=link}

The price paid is obviously a good deal for Coupang as Farfetch Holdings was valued at $23B as recently as in FY 2021. Farfetch Holdings fell on hard times as the Chinese luxury good markets slowed during the pandemic and the marketplace also pulled off expensive acquisitions that didn't meet the company's expectations, resulting in a major drop-off in market value. Since Farfetch is a restructuring play with high operating costs, Coupang paid only 0.2X revenues for the marketplace which likely means that the South Korean e-Commerce did not overpay for its acquisition.

Valuation of Coupang vs. Amazon

Coupang is following the same blueprint as Amazon, with a core focus on South Korea. The company has seen significant growth in the last couple of years, but U.S. investors are chiefly focused on U.S. companies, simply because they are more familiar with them.

However, I believe Coupang is also interesting for U.S. investors as a growth play. Coupang is expected to grow its top line from $24.1B in FY 2023 to $30.8B in FY 2025, implying an average annual growth rate of approximately 13% annually. For comparison, Amazon is expected to achieve 12% growth in the next two years, meaning Coupang has a slight growth advantage relative to Amazon.

Coupang is currently trading at 1.07X FY 2024 revenues which makes it a bargain compared to Amazon whose shares trade for 2.5X forward revenues. Considering that Coupang also generates a ton of free cash flow from its e-Commerce operations, I believe Coupang deserves a higher valuation. If Coupang's shares were to revalue just to their 3-year average P/S ratio, which in my opinion is totally possible, shares of Coupang would have 59% upside potential... and then would still be significantly cheaper than Amazon's.

Risks with Coupang

Coupang's revenue growth may slow if the South Korean economy dips into recession territory which I would consider to be the firm's greatest risk factor. Coupang is already profitable, so the online retailer has already proven that it can translate its customer and revenue growth into tangible earnings for shareholders. A slowdown in consumer spending and a deteriorating willingness to spend on e-Commerce products would obviously be potential concerns for any Coupang investor. A decline in free cash flow margins and a weaker EBITDA margin trend would likely cause me to change my opinion on the growth company.

Closing thoughts

Coupang is a promising growth play for FY 2024, in my opinion, because the company just announced a major acquisition in the luxury good market which is set to boost the company's revenues, EBITDA and free cash flow. Additionally, Coupang is already profitable in terms of EBITDA margins and FCF and the e-Commerce company is seeing solid revenue/customer momentum as well. Shares of Coupang are also fundamentally more attractive as a growth investment when compared to Amazon as Coupang trades at a significantly lower revenue multiplier factor. I believe the risk profile is favorable and Coupang may benefit from two key growth drivers in FY 2024: 1) EBITDA/FCF margin expansion and 2) Acquisition-driven revenue, EBITDA and free cash flow growth. With Coupang being much cheaper than Amazon (while also growing slightly faster), it is currently my favored e-Commerce growth play!

For further details see:

Coupang: 2 Reasons For An Upside Revaluation In 2024