CPNG - Coupang: A Leading E-Commerce Player With Expanding TAM And Improving Profitability

2023-10-19 17:20:45 ET

Summary

- Coupang's advantages in logistics help the company take market share. Competitor Naver is improving its logistics capabilities, but owning a logistics network will let Coupang have more control over its operations.

- International expansion will also expand TAM. Coupang is replicating its success formula in Taiwan: giving out free delivery services. The growth was twice the growth in South Korea post-Rocket launch.

- Lastly, Coupang has turned profitable and generated free cash flow thanks to operational improvements. As more merchants use FLC, Coupang will benefit from economies of scale.

- However, we believe that the growth potential has already been priced into the stock. Our estimates are 12% long-term top-line growth and 11% EBIT margin. Fair value estimate is $18/share.

- Investment risks include shrinking population and already-high online penetration rate in South Korea as well as failure to penetrate international markets.

Summary

We like Coupang's (CPNG) advantages in logistics that have allowed the company to take market share. Additionally, TAM is expanding because of increasing online penetration rate and international expansion, and focusing on operational improvements has improved margins and free cash flow. However, we think the growth potential has already been priced into the stock, hence no significant upside potential.

Business Overview

Founder Bom Kim initially founded Coupang in 2010 as a Groupon-like business, registering the company as a US limited liability corporation. A few years later, Coupang shifted its focus to become an e-commerce marketplace, engaging in first-party (1P) and third-party (3P) relationships. It operates primarily in South Korea and Taiwan after its unsuccessful attempt in Japan. Over two-thirds of Coupang's third-party merchants are small-medium enterprises with less than $2.5 million in annual revenues.

In general, Coupang classifies its business under two segments: Product Commerce and Developing Offerings. 1P and 3P businesses, as well as Rocket Fresh, are categorized under the Product Commerce segment. Coupang's growth initiatives segment, such as Coupang Eats (food delivery), Coupang Play (video streaming), Coupang Pay (digital wallet), and international business, falls under the Developing Offerings segment. This segment makes up about 3% of revenue.

Segment Contribution to Revenue (Vektor Research)

One of Coupang's priorities is to deliver goods to customers more quickly and efficiently. For instance, Coupang introduced Rocket Delivery in 2014, which ships orders within a day, and has since invested billions of dollars in fulfilment centers and last-mile logistics. This enables Coupang to provide Same-Day and Dawn delivery services. For the latter, customers can receive their orders before 7 AM if they order before 12 AM.

Investors have been interested in many called the "Amazon of South Korea." For example, major investments came in from Japanese bank SoftBank with $1 billion in 2015, following Sequoia Capital ($100 million) and new funding by BlackRock ($300 million) a year earlier. But Vision Fund, a fund owned by SoftBank, recently sold over $2.7 billion worth of shares in Coupang, although it remains the largest shareholder.

Nevertheless, with the stock falling over 60% from its all-time high, does the stock offer an attractive buying opportunity? What is the story? How much growth has been baked into the stock?

A Share Taker With Advantages in Logistics

Coupang saw its net revenues grow almost nine-fold from 2017 to 2022. But it was not until last year that Coupang turned profitable and generated positive cash flow since the launch of Rocket Delivery in 2014. In 2Q23, top-line growth was 16%, but currency neutral-wise, revenue grew 21% (Y/Y). In addition, the change in accounting for Fulfillment & Logistics by Coupang ('FLC') revenue, which changed from a gross to a net basis, impacted the year-on-year top-line growth by roughly 300 bps.

Reported vs. currency-neutral revenue growth (Company)

What is the Total Addressable Market ('TAM')? The management said that Coupang is still early in its journey: a single digit market share of ~$550 billion retail market in South Korea. According to data by Statistics Korea, "Total Transaction Value of Online Shopping Mall" from January to August 2023 reached 147 trillion KRW (roughly $110 billion). This makes up about 35% of total retail sales.

Talking about competition in South Korea, we estimate that Coupang has a 24% market share in Gross Merchandise Value (GMV) in 2022, slightly higher than analysts' estimate of 22%. GMV, by definition, is the total sales of merchandise sold on a marketplace platform. Thus, our calculation is based on Coupang's 1P and 3P revenues, assuming a 9% take rate ( fees are roughly between 6% and 11% depending on category) for its 3P revenue.

Meanwhile, our estimate for South Korean top search engine Naver is around 20%. This is based on its impressive 41.7 trillion KRW in commerce GMV ($32 billion) from the last year. Together, both companies made up approximately 44% of the market share.

Naver's Commerce GMV (in KRW) (Naver)

But Coupang has been taking market share from other players. The reason is that Coupang is leading in delivery time thanks to its $4.7 billion investment in more than a decade, building over 100 fulfilment centers around the country. As cited in The Korean Herald , Opensurvey's research suggests that respondents choose Coupang as their preferred e-commerce company because of factors such as "ultrafast delivery, low prices and simple exchange and refund policies."

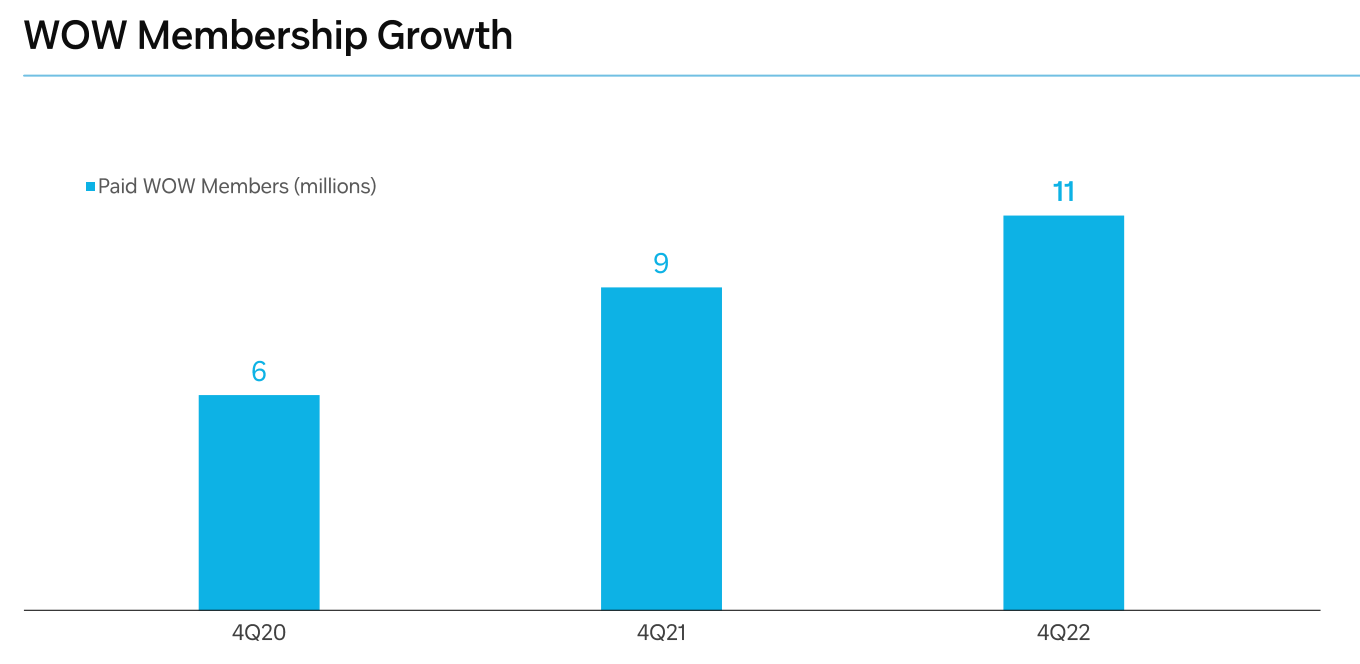

In 2019, Coupang launched Rocket WOW memberships. For 4,990 KRW per month ($3.7 per month), customers can enjoy next-day delivery without minimum purchase and 30-day free returns. Previously, the membership fee was 2,900 KRW per month, but increasing the membership fee did not make customers leave, according to the company, as seen in the figure below. Therefore, we think Coupang has a strong pricing power. On the other hand, Credit Suisse estimated Naver Plus Membership subscribers (priced at 4,900 KRW a month) to be approximately 4 million.

WOW members (million) (Company)

{kind=link}

Additionally, leveraging its extensive logistics network, Coupang offers a Fulfillment & Logistics by Coupang program that enables third-party merchants to put their inventory in Coupang's fulfillment centers. Coupang said merchants saw their sales increase by 65%, on average, after they moved their inventory to FLC. More merchants equals more product selection, which equals more growth. As Bom Kim said on the 4Q22 earnings call:

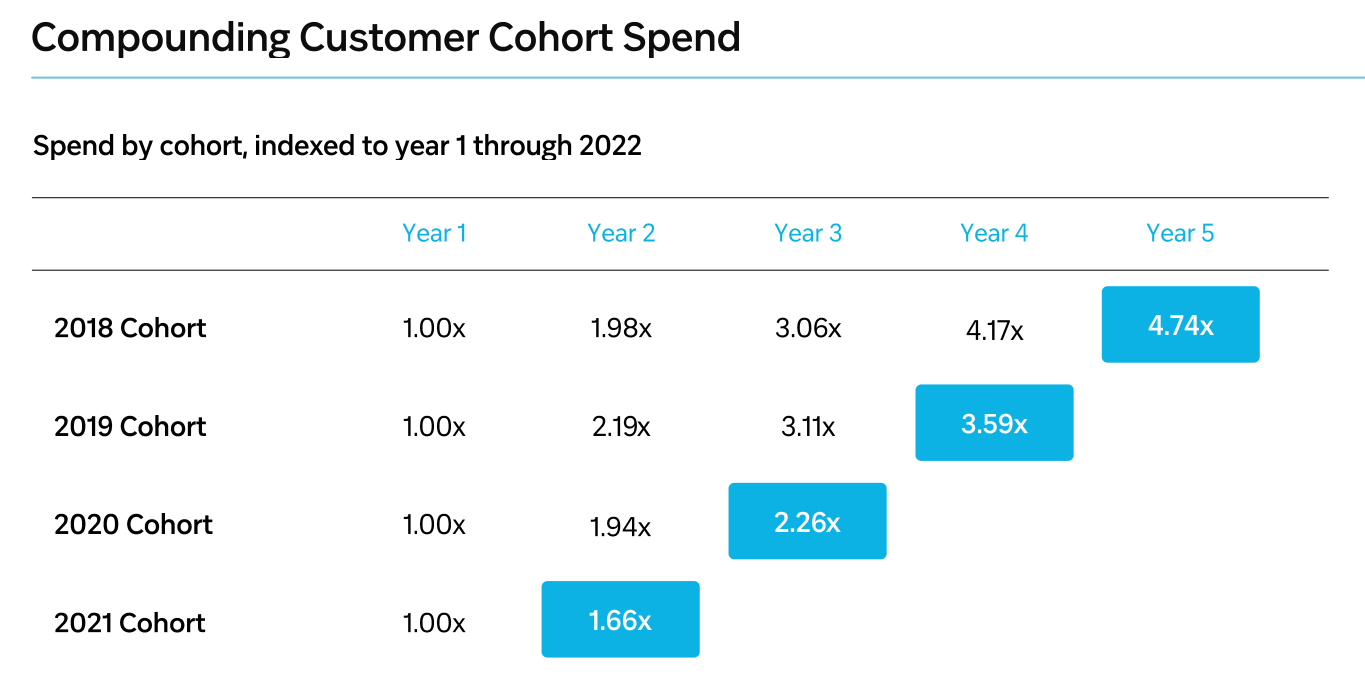

Consequently, we believe selection will be a critical driver going forward of even higher levels of customer engagement and loyalty, which in turn will unlock more growth and profitability over the long term. Currently, only 20% of Active Customers have purchased nine or more of the over 20 categories that we offer. These customers purchased more than two-and-a-half times the amount of the average customer. We expect that engagement within and across categories will accelerate with a wider selection on Rocket. Our oldest cohorts, while spending nearly twice the amount of our newer ones, are still growing in spend each year as they experience new selections and categories on Rocket.

Older Cohorts Are Spending More (Company)

{kind=link}

On the contrary, Naver does not have its own logistics network, but set up the so-called Naver Fulfilment Alliance with logistics companies. For instance, Naver teams up with CJ Logistics following a share-swap deal worth 300 billion KRW. Additionally, Naver Guaranteed Delivery Service program will compensate customers with reward points if their orders do not arrive on time. This prompted Naver to establish a partnership with SK Energy to set up micro fulfilment centers at some 3,000 SK Energy gas stations nationwide.

But will Naver be able to overtake Coupang in logistics? That will be unlikely, in our view.

We think owning its logistics network will let Coupang have greater control over its assets, resulting in more efficient operations and better unit economics. Operating over 100 fulfillment centers also helps reduce delivery time as orders will be much closer to customers. Indeed, CJ Logistics opened more fulfillment centers and claimed that the next-day delivery covers 90% of the country excluding "regions with certain geographical constraints." But there are still some limited logistics capabilities that Naver lacks:

Being at its early stage of fast delivery service, however, its next-day delivery is not available on Sundays and public holidays. Also, the products are mainly limited to processed products.

During the last earnings call , Naver's management said that the company was testing its Sunday delivery service and that the feedback appeared favorable. But the question is whether the cost structure is as efficient as that of those who own fulfillment centers. It is also unclear what percentage of orders do not arrive on time. All in all, thanks to its advantages in logistics, we believe that Coupang is likely to remain a share taker in the e-commerce market.

International Expansion Will Expand TAM

As things stand, Coupang is also expanding its presence internationally. Following its withdrawal from the Japanese market, Coupang is stepping up its investment in Taiwan. This year, the company allocated $400 million for its Developing Offerings segment, although the management did not disclose how much of that allocation was attributable to the international business.

First, we need to look at the potential of Taiwan's e-commerce market. With a total population of roughly 24 million people, slightly less than half of Korea, Taiwan has a low e-commerce penetration rate of about 13-14% , far lower than developed markets such as China and South Korea. According to Statista , total retail e-commerce revenue in 2022 stood at billion ($15 billion).

What about the competition? The biggest players include Shopee, a subsidiary of Sea Limited (NYSE: SE ), Momo, and Ruten. The former was the new kid on the block, entering the market in 2015 while the other two have more than a decade of experience. But Shopee quickly gained prominence thanks to aggressive promotions, including free delivery services, and a user-friendly mobile app, according to some analysts .

Momo said that they have 20% market share in the e-commerce space. No details on Shopee's market share in Taiwan. Indeed, Similarweb suggests that Shopee was the most visited site in the country. But based on revenues generated that are between one-third to one-half of Momo, according to estimates , Shopee might have gained at least 7-10% market share in Taiwan since its inception in 2015, in our view. The figure could be higher depending on the actual take rate.

As things stand, Coupang is replicating what it does in South Korea: leveraging its Rocket Delivery service to gain market share. A trial run of free next-day delivery service for orders or more and a limited 30% off up to for new customers purchasing on Rocket Delivery proved to be successful among Taiwanese customers: the growth is twice as high as the growth in South Korea post-Rocket launch.

Who does not love free delivery and discounts? About two-thirds of respondents, compared to the global average of 51%, chose "Free Delivery" as their online purchase driver, according to research conducted by GWI.com. So, this helps explain why Coupang's strategy is on point.

Your second question on Taiwan. Taiwan, as we mentioned, is growing faster than Korea did over the same time period post the launch of Rocket. Our value proposition is the same as Korea. We've always believed that the transformational customer experience we built in Korea would resonate with customers in other markets.

Bom Kim on 2Q23 Earnings Call.

Additionally, it is likely that Coupang is still looking at expanding its presence to other countries, which will expand TAM. The company has reportedly been hiring in Singapore, although it remains to be seen when they will try to take the pie in the Southeast Asian e-commerce market, which is projected to reach $230 billion in GMV in 2026. Still, we like Coupang's capital allocation strategy, as we have witnessed Coupang's willingness to withdraw from investments it deems to generate lower-than-expected returns.

And five, we are disciplined capital allocators. We start with small investments, then test and iterate rigorously. We invest more capital over time in opportunities that have the best long-term cash flow potential.

In our International initiatives, we shuttered our operations in Japan, where we weren't producing the returns we'd hoped for. In contrast, we like what we've been seeing in Taiwan, which is showing the same signs of transformative potential that we saw in Korea when we launched Rocket Delivery.

Significant Improvement In Margins and Free Cash Flow

Coupang has shown significant profitability improvements, turning profitable at the operating levels in 3Q22 and generating $391 billion post-SBC free cash flow in the following quarter. Adjusted EBITDA margin was 5.1% in 2Q23. Two years ago, the number was over -9%. This suggests the company is on track to achieve its long-term adjusted EBITDA target of 10%+. What is the margin expansion story?

Coupang's adjusted EBITDA and post-SBC FCF margins (%) (Company, Vektor Research)

First, Coupang explained that a significant margin expansion earlier this year was neither from downsizing its workforce nor from raising prices. During the 1Q23 Earnings Call :

The majority of the nearly 600 bps improvement in profit margin this quarter came from operational improvements in Product Commerce, not benefits from advertising, Eats or WOW membership. It was also not driven by one-time cost-cutting measures like layoffs. And more importantly, we achieved these profit improvements without sacrificing the customer experience. In other words, without raising prices to increase margins, rolling back benefits or compromising service levels.

Second, the company is now focusing on AI and machine learning. For instance, Coupang built a $250 million fulfilment center, the largest in Asia, filled with robots and driverless vehicles in Daegu. The company claimed that Automated Guidance Vehicles helped reduce 65% of the workload. Furthermore, automated fulfilment centers are twice as efficient as the non-automated ones.

Lastly, we believe as more merchants put their products on FLC, Coupang will benefit from economies of scale. Shorter delivery time means more products can be delivered. And the company has reiterated that FLC is a margin-accretive business. Despite significant growth, FLC only made up 7% of overall revenue and 4% of total units sold. Looking forward, while the company expects that significant margin expansion is unlikely to be the case, we like where the direction is going: expanding TAM and improving margins.

But What Is Baked Into The Stock?

As of October 17th, Coupang stock trades at $18 per share, with a forward P/E of 35x (using 2024F consensus estimate). Our 10-year reverse DCF model (our base year is 2024) suggests that the market is expecting an average 13% revenue growth and 9.5% EBIT margin in 2034F. Now, the question is whether such expectations are reasonable.

Sensitivity analysis of the market's expectations (Vektor Research)

Putting Estimates Into Numbers

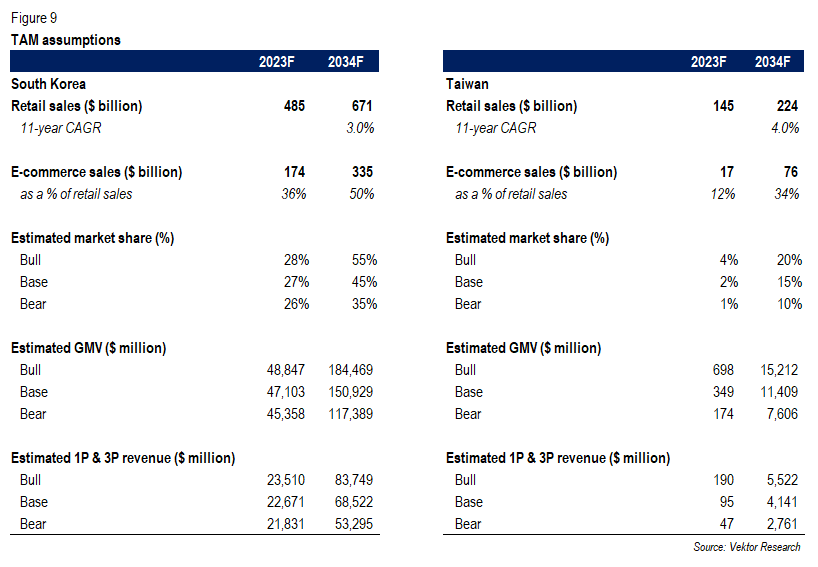

For TAM in South Korea, we estimate e-commerce sales as a percentage of retail sales to increase by 1% per year to 50% in 2034F, given its already high adoption rate. We estimate Coupang's market share to be 27% in 2023F and increase to 45% in 2034F.

Despite lower penetration rate than South Korea, which should provide a higher growth potential, the e-commerce market size in Taiwan is much smaller than in South Korea. As mentioned before, our guess is that Shopee has gained at least 7-10% market share in Taiwan since 2015. And that figure could be higher depending on the actual take rate. Thus, we believe it is reasonable for Coupang to gain a 15% share in 2034F.

TAM Assumptions (Vektor Research)

{kind=link}

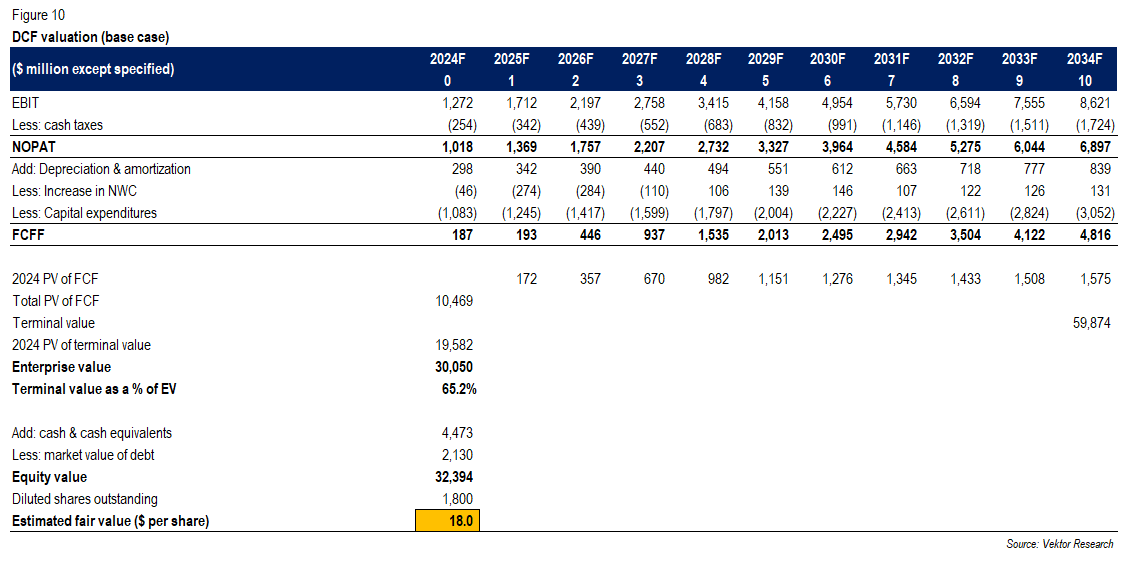

Based on our base case assumptions, Coupang can reach $76 billion in revenue in 2034F (12% long-term average revenue growth) and 11% EBIT margin. Our fair value estimates are between $12 and $25 per share (12% WACC and 3.5% terminal growth). Assigning probabilities to our scenarios (50% to base case and 25% each to bull and bear cases), we arrive at the fair value estimate of $18 per share.

Coupang DCF valuation (Vektor Research) Sensitivity analysis on fair value estimate (base case) (Vektor Research)

{kind=link}

Investment Risks

Shrinking Population and High Online Penetration Rate

The shrinking population and its already-high online penetration rate pose a question on whether South Korea's e-commerce market will grow as expected. Worse, as industry growth decelerates, players will be more aggressive in promotions to acquire customers, leading to margin erosion.

Failing to Expand Internationally

We believe the future growth of Coupang will depend on its international businesses. Successfully expanding presence to, for example, the Southeast Asian market could greatly expand TAM. Should Coupang be successful in its international expansion, the company could exceed our long-term estimates. On the other hand, our estimates could go wrong in case the expansion fails. For example, Coupang withdrew from Japan due to its different customer preferences.

Conclusion

We like Coupang because of its logistics advantages that allow the company to gain market share and establish a well-entrenched competitive position. Furthermore, more efficient operations enable Coupang to give out promotions and free delivery services with competitive membership fees while still producing healthy margins and positive free cash flow.

However, we think the growth potential has been fully priced into the stock, hence no significant upside potential. The company is likely gaining traction in Taiwan, but the market size is much smaller than in South Korea. We could be wrong if Coupang successfully penetrates other international markets with large TAM. In our view, it is important to have conservative yet reasonable estimates and a margin of safety. A 30% margin of safety implies an attractive buying price of $13 per share. Therefore, we rate the stock as a "HOLD." If you have any thoughts, please do not hesitate to comment below.

For further details see:

Coupang: A Leading E-Commerce Player With Expanding TAM And Improving Profitability