CPNG - Coupang: A Top E-Commerce Growth Stock

2023-06-14 07:28:04 ET

Summary

- Coupang is an attractive e-Commerce stock to own for investors that want to focus on e-Commerce markets outside the U.S. and China.

- Coupang achieved free cash flow profitability in Q1'23, on a trailing twelve months basis.

- Shares of Coupang are undervalued, based off of revenues, when compared to Amazon and Alibaba.

Coupang ( CPNG ) is a fast-growing South Korean e-Commerce company that has achieved free cash flow profitability in the first quarter and is on a good path to growing its margins. Coupang has seen double-digit net revenue growth in the first-quarter and reported a $91M in earnings. With strong revenue momentum, a growing customer base, expanding margins and positive free cash flow, I believe shares of Coupang deserve to trade at a higher valuation!

Strong momentum in core e-Commerce business

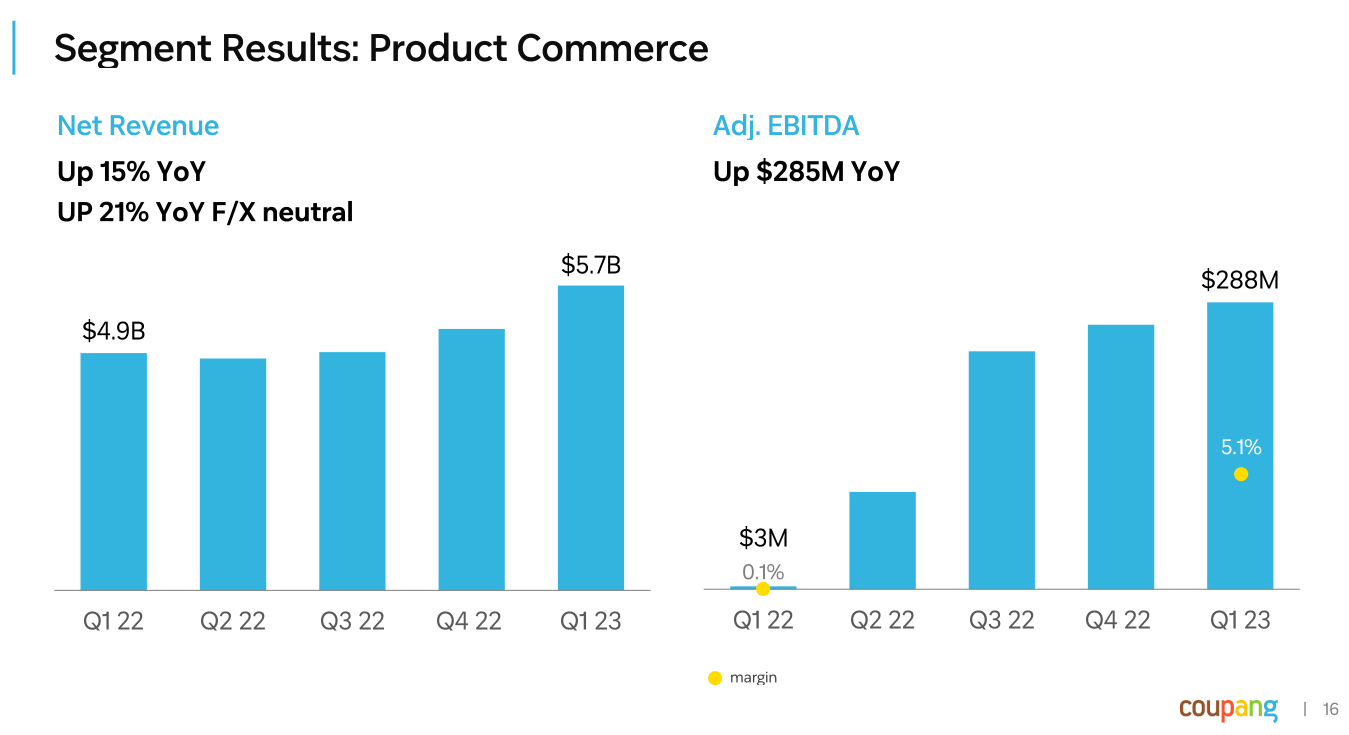

Coupang is a South Korean e-Commerce platform, which was founded in FY 2010 and has received investment capital from Sequoia Capital. Coupang chiefly focuses on its e-Commerce marketplace, but also launched its own private label business and developed Coupang Play, a subscription-based video streaming service. The private label business has been a major success for the company as it achieved $1.0B in annual revenues just three years after its inception. The core business, however, is e-Commerce which is seeing strong momentum and which posted 15% year over year revenue growth in the first-quarter (21% in currency-neutral terms).

In total, Coupang generated $5.7B in core segment revenues which makes the South Korean e-Commerce segment a $23-24B annual revenue business. Due to Coupang's heavy investments into its e-Commerce infrastructure and new product launches, the firm has seen a strong improvement in its profitability picture in the last few quarters: in the first-quarter, Coupang reported $288M in adjusted EBITDA and a positive adjusted EBITDA margin of 5.1%. In the year-earlier period, Coupang achieved only $3M in adjusted EBITDA and a margin of 0.1%.

{kind=link}

Source: Coupang

Coupang's other segment -- which groups together its investments in Coupang Eats, International, Play and Fintech -- is seeing less stability in its revenues so far and significant operating losses. As Coupang grows these businesses to profitability over time, I believe the e-Commerce company will more and more look like a South Korean version of Amazon ( AMZN ): a company that uses its strength in e-Commerce to push into other areas such as delivery services, financial services and streaming.

Source: Coupang

Coupang's revenues are in an uptrend and the company's margins are improving as well. Coupang achieved a first-quarter profit of $91M, showing an improvement of $300M year over year.

Free cash flow profitable

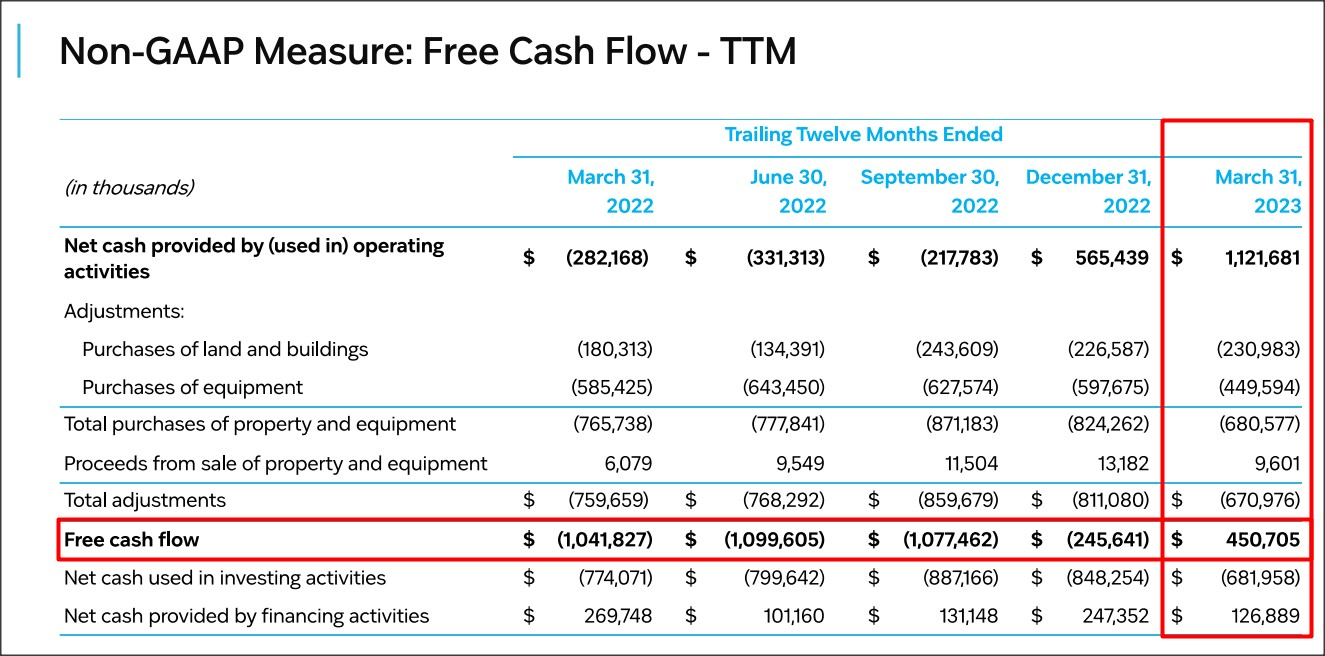

Coupang achieved a critical milestone in the first-quarter which is that the e-Commerce company posted its first positive free cash flow on a trailing twelve months basis.

Coupang reported free cash flows of $450.7M in Q1’23 (ttm) compared to negative free cash flow of more than $1.0B in the year-earlier period. The key reason for this improvement is that the company has expanded its customer base from 18M in last year's first-quarter to 19M in Q1'23.

{kind=link}

Source: Coupang

Coupang's valuation compared to international e-Commerce rivals

Coupang has valuation upside, in my opinion, largely because the company has proven to investors that it can run a profitable e-Commerce enterprise and is now free cash flow profitable. Coupang is expected to see 100% EPS growth next year widely outmatching EPS growth rates of Amazon (65%) and Alibaba ( BABA ) (11%). As a result, Coupang has a relatively high P/E ratio of 29X which reflects the firm's strong EPS growth prospects. On the other hand, Coupang is trading at only 1.1X forward revenues compared to price-to-revenue multiples of 2.07X for Amazon and 1.54X for Alibaba. Based off of sales, Coupang appears to be greatly undervalued, in my opinion.

Risks with Coupang

The two biggest commercial risks for Coupang are moderating top line growth as well as growing pressure on the e-Commerce company’s profit margins. The e-Commerce business is notoriously competitive and Coupang competes in the global marketplace with companies such as Amazon or Alibaba. What would change my mind about Coupang is if the company saw declining free cash flow as well as contracting adjusted EBITDA margins going forward.

Final thoughts

Investors don't always have to buy Amazon or Alibaba in order to get exposure to the e-Commerce industry: in my opinion, Coupang is an attractive e-Commerce stock to own for investors that like to add international exposure to their portfolios. There are also very solid and fundamental reasons to own Coupang stock as well: Coupang is seeing double-digit top line growth, improving margins and is now free cash flow profitable. Additionally, Coupang's growth in the e-Commerce market is discounted when compared to Amazon and Alibaba, based off of sales. Since Coupang is attractively valued and has momentum on its side, I believe the risk profile is skewed to the upside and I recommend Coupang's shares!

For further details see:

Coupang: A Top E-Commerce Growth Stock