CPNG - Coupang: Exceptional Disciplined Capital Allocation

2023-08-31 08:30:00 ET

Summary

- Today, I will discuss Coupang with you through three lenses.

- 1) The substantial impacts currency dynamics have had on the business. 2) Its autonomous, vertically integrated commerce engine. 3) Its digital ad business which is growing at ~50% presently.

- I also discussed valuation considerations for the company in my concluding thoughts.

- In short, with robust free cash flow margins, a long runway for growth ahead, $4.1B in cash, and $500M in long-term debt, I believe Coupang will be a fantastic business to own in the decade ahead.

Currency Dynamics

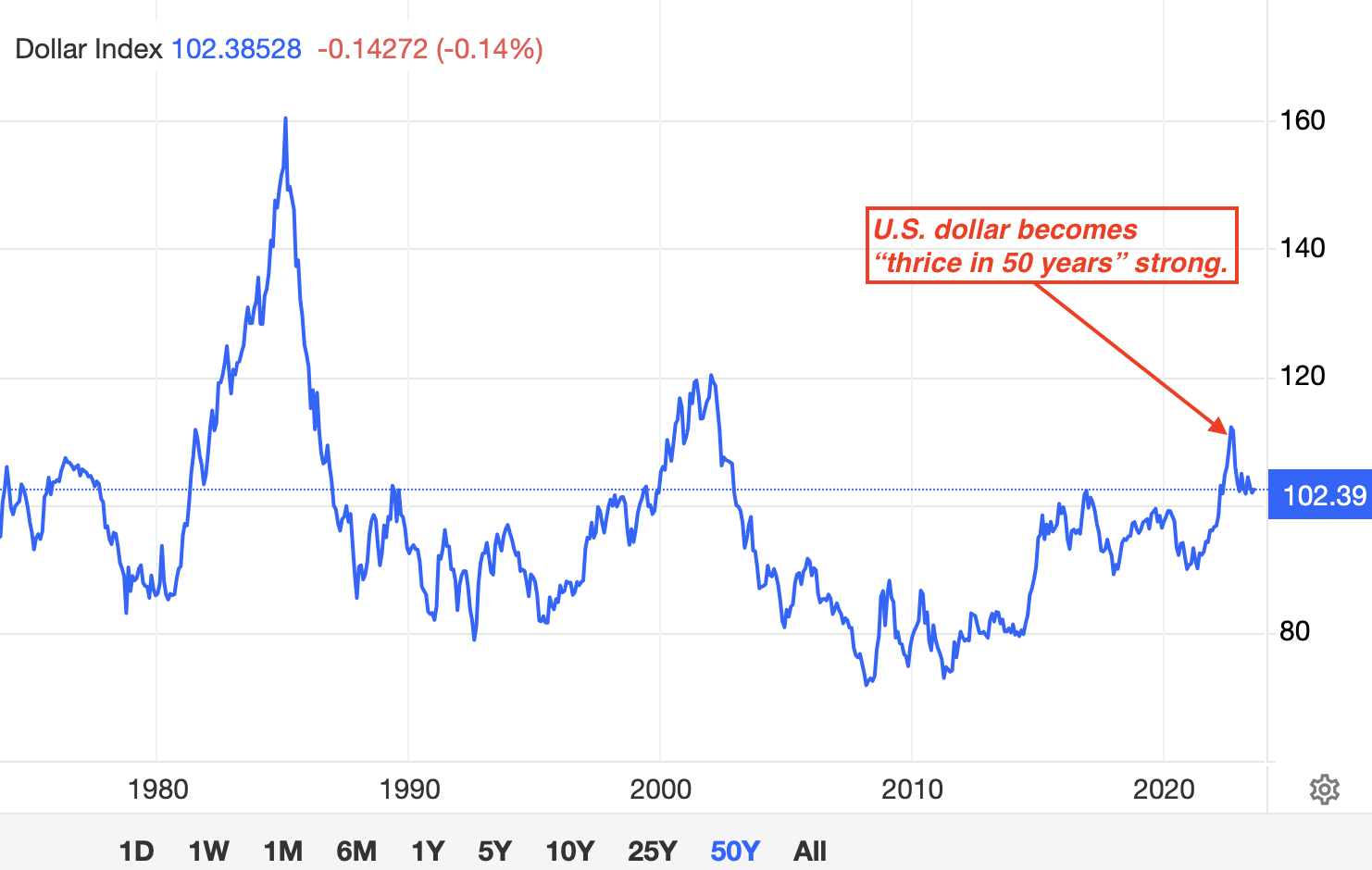

Over the last six months, I've often highlighted the idea that Coupang is, in some sense, a bet on the weakening of the U.S. dollar, at least in the very near term. I've often shared this because, over the last year or so, the U.S. dollar became "thrice in 50 years" strong.

{kind=link}

As we know, Coupang is a company that operates in South Korea; therefore, it generates its revenue and free cash flow in South Korea's native currency, which is then converted into U.S. dollars at the prevailing exchange rate.

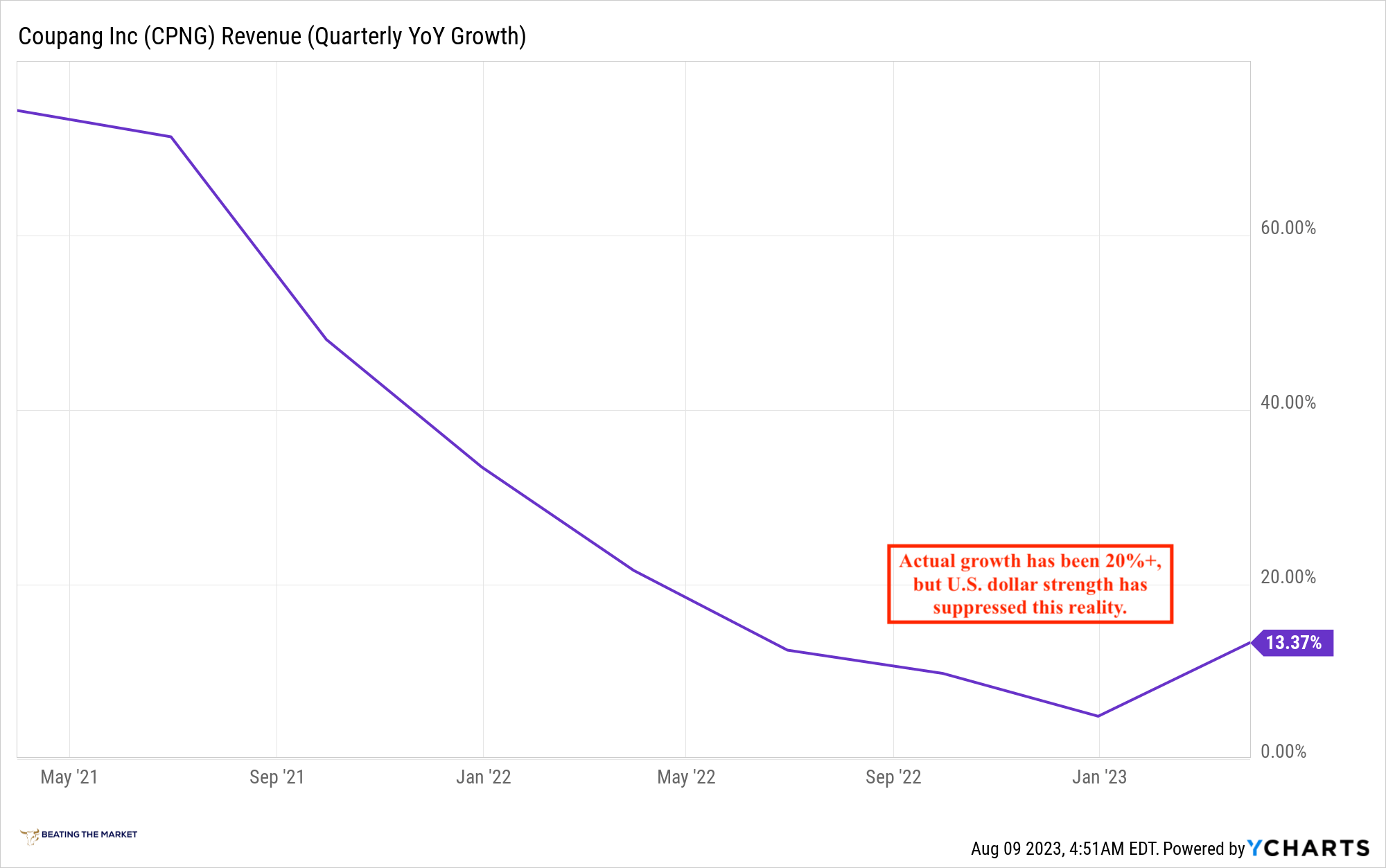

Because the dollar has been so strong, this has created immense drag on Coupang's reported revenue. While the company has grown at 20%+ consistently over the last year on a constant currency, or "FX neutral" basis, its reported revenue growth has cratered into the low teens due in large part to the strength of the dollar relative to South Korea's native currency.

Coupang's Reported Quarterly Revenue Growth In U.S. Dollars

{kind=link}

To put these dynamics concisely, the dollar and Coupang's sales growth have been inversely correlated, meaning that as the dollar strengthens, Coupang's sales growth weakens, and vice versa.

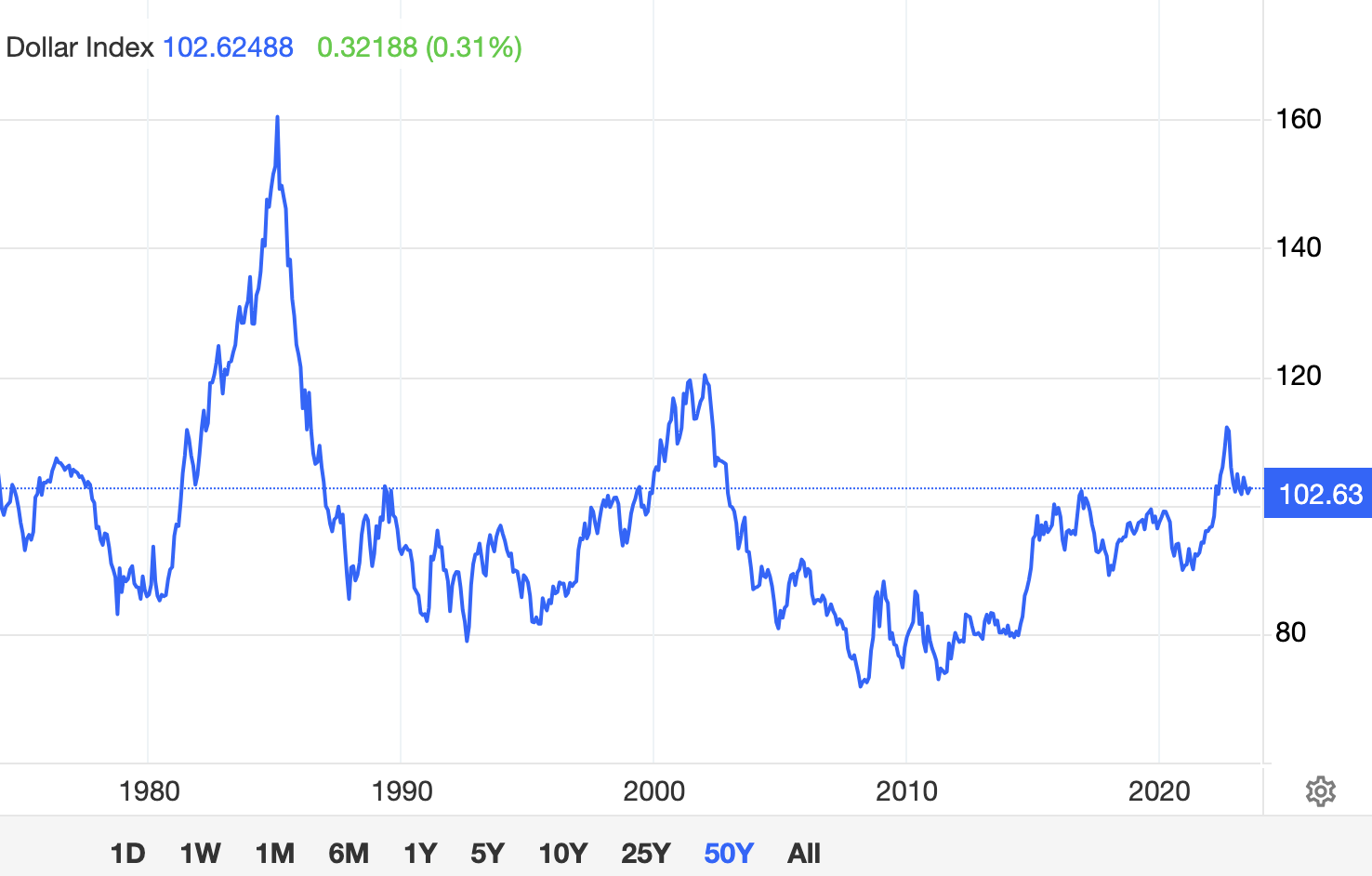

As we saw in the dollar index chart just a moment ago, the dollar has been weakening.

To answer why it's been weakening, I invite you to review these formulas:

- Lower U.S. inflation = lower U.S. interest rates = more U.S. dollars = weaker U.S. dollar

- High U.S. inflation = higher U.S. interest rates = less U.S. dollars = stronger U.S. dollar, due to supply shrinking and demand remaining constant or growing

And the first equation results in strengthening U.S. dollar-reported revenue growth for Coupang. It results in Coupang's actual revenue growth aligning with its U.S. dollar-reported revenue growth, which, in this case, has served to accelerate Coupang's revenue growth in Q2 2023.

On this subject, in a recent note I published entitled, "Acceleration 2," I remarked,

As something of an aside, in the case of Coupang, it's an interesting investment because it has been disproportionately (relative to our other companies) impacted by the strength of the dollar, which, as we've often discussed, has been "thrice in 50 years" strong.

Today, the dollar has weakened materially, but it's still quite strong (contrary to some narratives we may have read over the last couple years):

The USD Remains Very Strong

Trading Economics

Notably, Coupang's growth is actually better than what it recently reported in U.S. dollars for Q1 2023. FX neutral, Coupang grew at over 20% in Q1 2023, despite the incredible rise in interest rates we've experienced over the last 20 or so months.

Coupang's Quarterly Revenue Growth Rate

YCharts

With both a weakening dollar and "anything but the fastest repricing of credit in the history of America, the policy of which gets exported internationally due to the "Trilemma," or "Impossible Trinity," it's likely that Coupang accelerates growth quite substantially in the quarters and years ahead, and it's likely that its valuation re-rates a bit higher, driven by a 10%+ EBITDA margin and accelerating growth.

{kind=link}

{kind=link}

And, in Q2 2023, we, indeed, witnessed accelerating revenue growth.

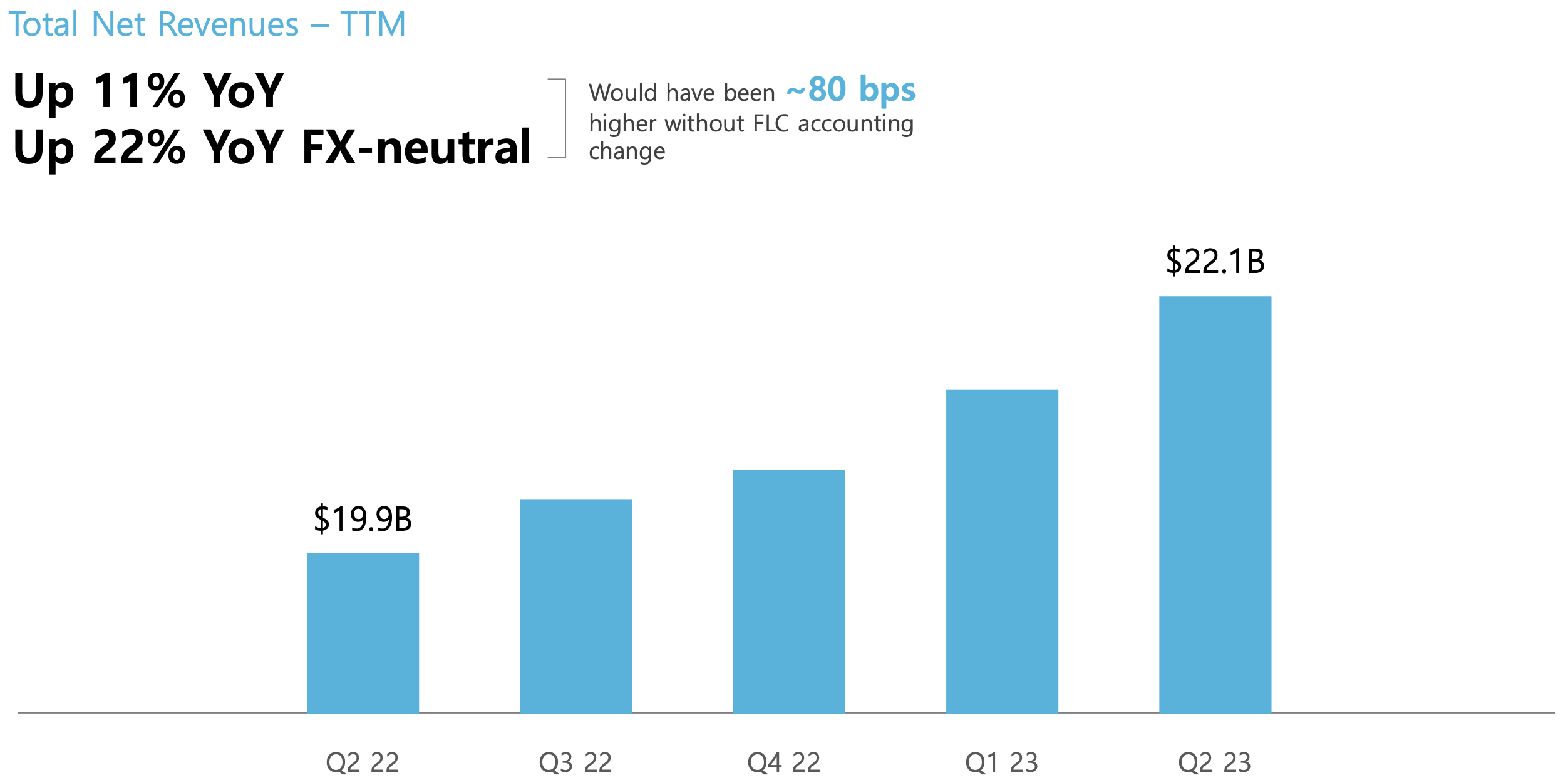

To conclude this brief introduction, my central contention has been that, with a weakening dollar, Coupang's reported sales growth, which has been cratering for the last 18 months, in large part due to the strength of the dollar, would begin to align more closely with its FX-neutral sales growth, and this was the case in Q2 2023, which was the first quarter where we saw a relatively weaker dollar in the last 18 or so months.

We can see this alignment via a comparison of two charts:

In our first chart, we can see that reported revenue growth (in U.S. dollars) has been about half FX neutral revenue growth over the last 12 months, and this is directly attributable to the aforementioned "thrice in 50 years" strong dollar, which has been so over the last 18 months but has begun to weaken in recent quarters.

Coupang's Q2 2023 Investor Presentation

{kind=link}

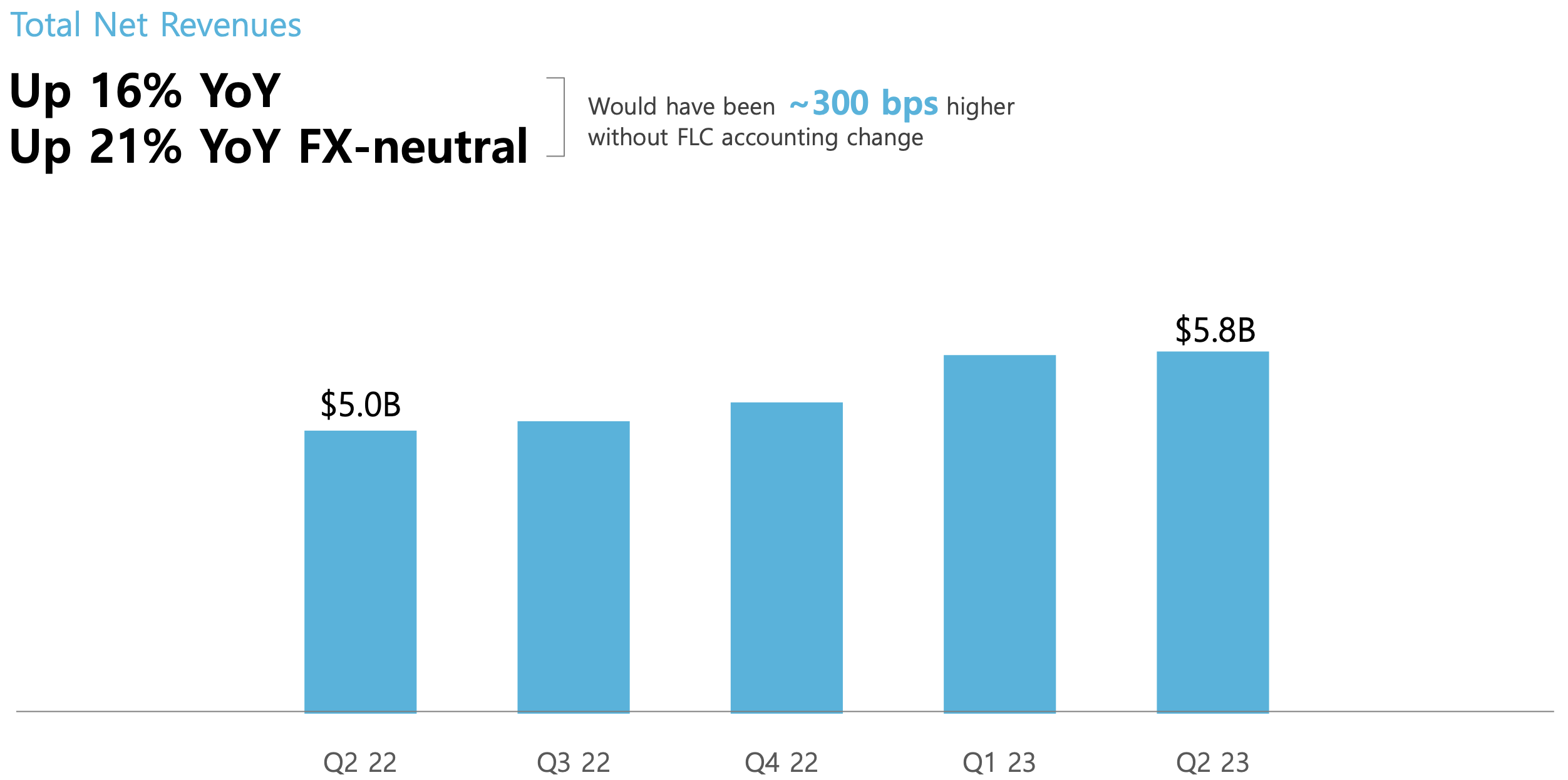

This weakening has caused U.S.-dollar reported revenue growth to move closer to Coupang's true business growth, as was the case in Q2 2023, which we can see in the chart below.

Coupang's Q2 2023 Investor Presentation

{kind=link}

With inflation abating materially , the dollar should continue to weaken as rates begin to ease, and this should continue to push upward on Coupang's sales growth.

Of course, this is just one, more near-term perspective for Coupang.

Over the last year, I've principally written about the attractive nature of the core business and not the currency dynamics which have helped to afford us very attractive entry points in the mid to low teens.

In this vein, let's now turn to two of the most noteworthy components of the Coupang investment thesis.

- Its AI-orchestrated, autonomous delivery network

- Digital ads

Notably, as I highlighted in my recent review of Amazon (AMZN), digital ads could be rebranded as "AI-driven ads," so, in a quite true sense, our bet on Coupang is a bet on AI.

Autonomous Delivery Networks

Our unique end-to-end integrated fulfillment, logistics, and technology network enables Rocket Delivery, which provides free, next-day delivery for orders placed anytime of the day, even seconds before midnight—across millions of products. Our structural advantages from complete end-to-end integration, investments in technology, and scale economies generate higher efficiencies that allow us to pass savings to customers in the form of lower prices. The capabilities we have built provide us with opportunities to expand into other offerings and geographies.

In a recent review of Coupang's business, I detailed the idea that Coupang had created a vertically integrated, autonomous commerce engine that created a substantially better consumer experience (read: created higher consumer surplus than incumbent commerce engines). Using this autonomous commerce engine, it has been gradually capturing giant swaths of the overall commerce TAM in South Korea over the last decade or so.

Put another way, Coupang created a superior product to existing incumbents within a massive, fragmented, highly competitive TAM, and that has allowed the company to gradually consume market share, ultimately achieving tens of billions in sales in a short time.

I’d like to take a moment to frame our Q2 results under five key takeaways.

First, we continue to deliver expanding profitability and sustained high growth, not one at the expense of the other, because of our years of unparalleled investment and an unrelenting focus on both the Customer Experience and Operational excellence.

[The investment has created the differentiated, autonomous commerce engine that's fueling market share capture.]

Second, our flywheel is accelerating, both revenue and active customers increased at a faster pace this quarter. It’s worth highlighting that the growth of Active Customers accelerated from 1% year-over-year in Q4 of last year to 5% in Q1 to 10% this quarter.

Additionally, all of our customer cohorts, even our oldest continue to increase their spend and the number of categories they are purchasing on Coupang. All of these trends underscore how differentiated our value proposition is in a retail market that we believe is defined by high prices and limited selection.

They are also a reflection of our early stage of growth, we have just single-digit share today of a massive retail market expected to reach $550 billion in the next three years. It’s hard to overstate just how early we are on this journey.

Coupang's Differentiated, Autonomous Network

Coupang has used this, as well as other components of its differentiated, vertically integrated commerce engine to consume South Korea's commerce Total Addressable Market.

Customers increasingly come to Coupang for our vast selection, unmatched delivery speed, and low prices. Our next day Rocket delivery experience across millions of 1P and FLC products has no comparison in the market.

Gaurav Anand, CFO, Coupang Q2 2023 Earnings Call

We can graphically understand Coupang as follows:

Q1 2023 Coupang Investor Presentation

{kind=link}

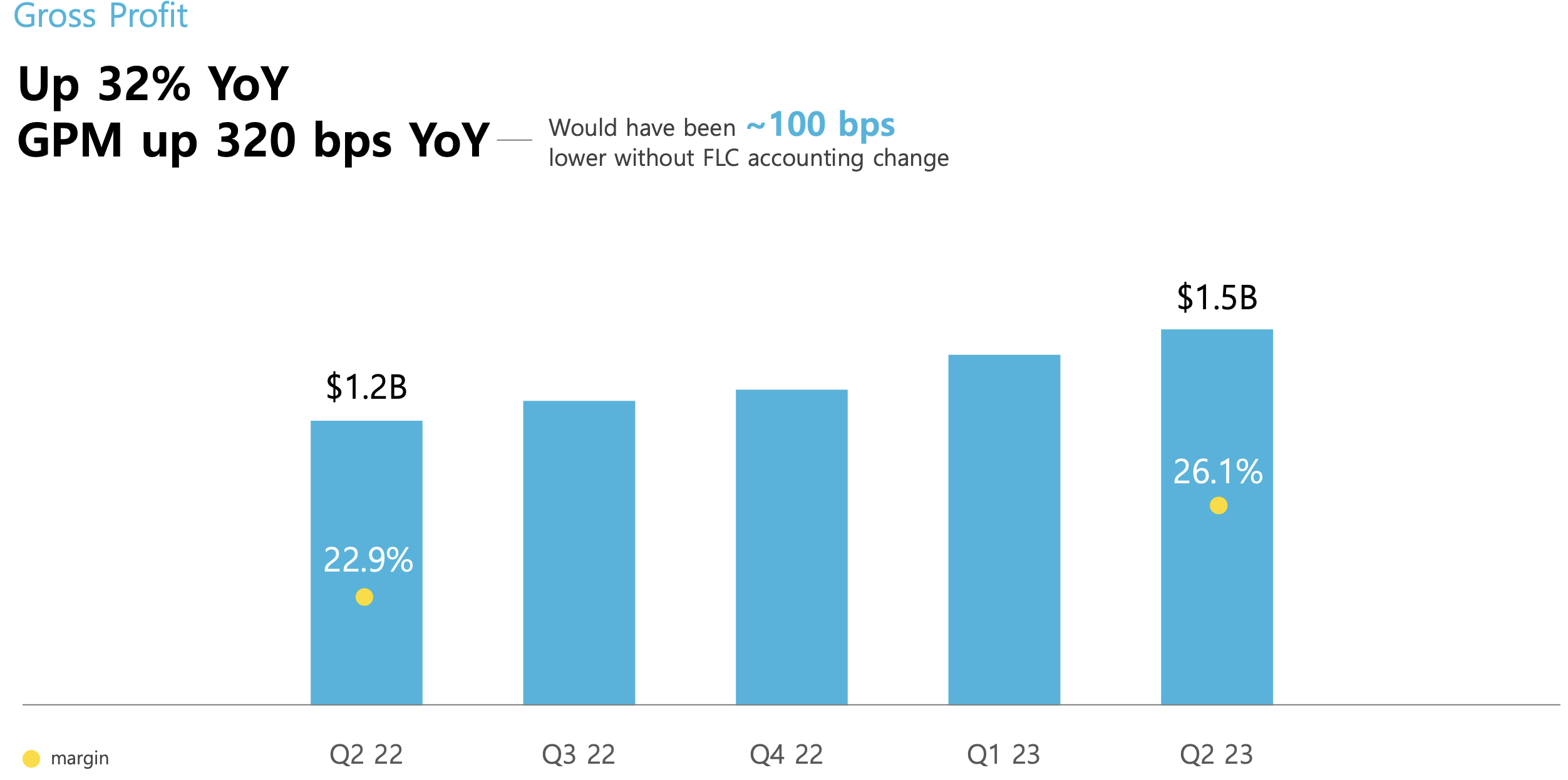

Notably, Coupang's differentiated, autonomous commerce engine affords it exceptional operating leverage, which has been demonstrated in Coupang's ability to grow gross profits at a faster rate than total sales growth.

Coupang Grows Gross Profit At 32% Year Over Year

Coupang's Q2 2023 Investor Presentation

{kind=link}

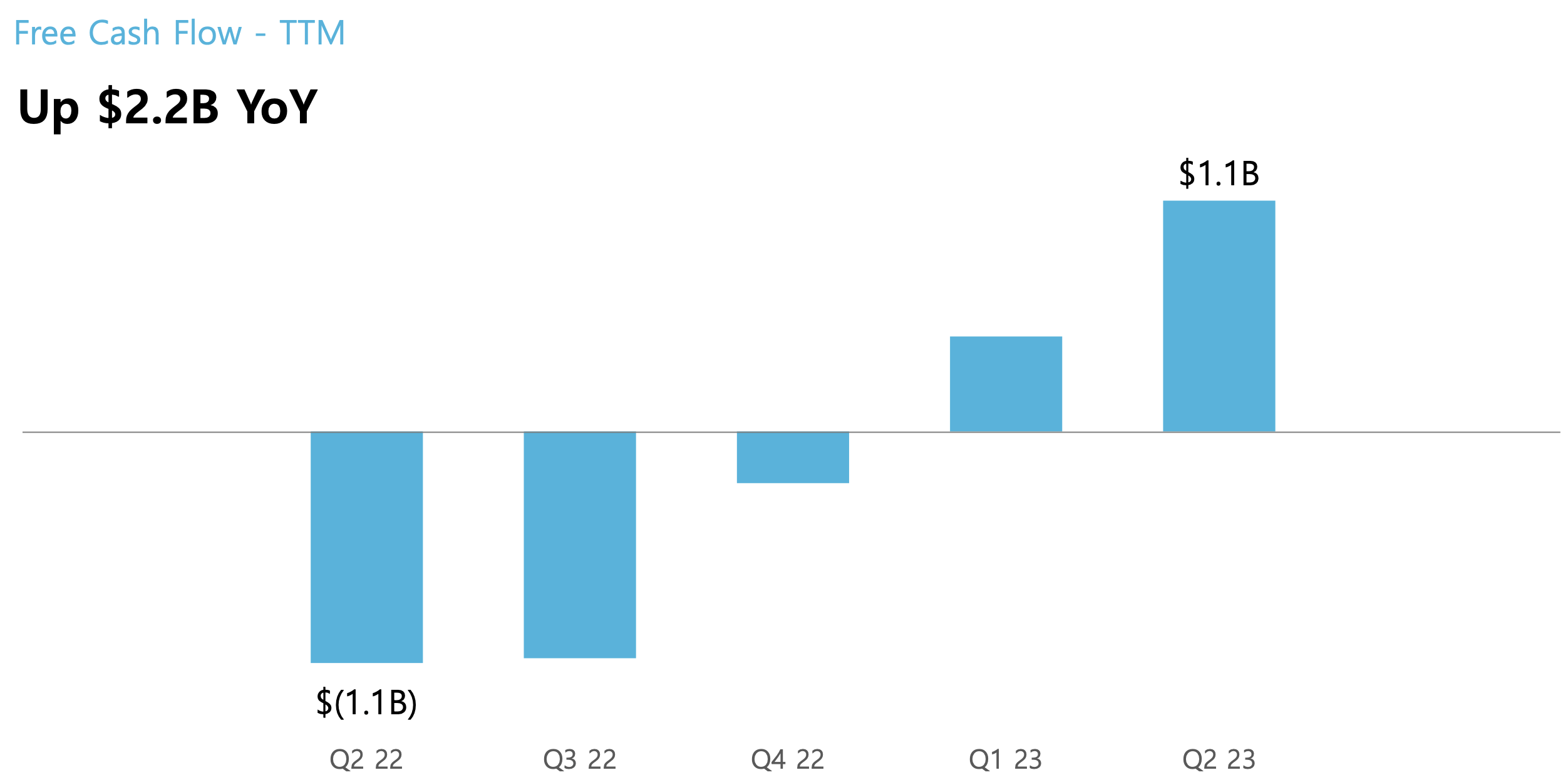

The operating leverage of Coupang's differentiated, autonomous commerce engine has been further demonstrated via its ability to expand its free cash flow margins almost instantly (in the world of business, I would consider the improvements below "almost instant." Most things in business take 5-10 years to really play out in their entirety.).

Coupang's Q2 2023 Investor Presentation

{kind=link}

And I believe autonomous delivery networks are actually still in their early innings.

In the future, warehouses will only be staffed by software and mechanical engineers: robots and automation will be the only "labor capital" being employed by the corporate entity.

This should further serve to enhance the operating leverage of companies like Coupang and Amazon (or, if they pass cost savings on to consumers, market share). On Amazon's Q2 2023 earnings call, the topic of evolving its logistics network/warehouses was discussed quite a bit, and, as I just mentioned, I believe the room for evolution here is quite immense.

And, of course, this is principally a matter of AI engineering.

On this note, let's now turn to another AI-centric component of Coupang's vertically integrated commerce engine.

Digital Ads In Ecommerce

And high growth isn’t limited to our first party offering. Third-party sales in virtually every category, including Fashion and Beauty, are growing at a multiple of the retail market. And our emerging merchant services like advertising and Fulfillment and Logistics by Coupang, or FLC, are growing more than twice as fast as our overall business."

Bom Kim, CEO, Coupang Q2 2023 Earnings Call

In my recent review of Amazon, I shared the following ideas,

As I've often noted, digital ads is actually an AI-revolution at its core. It is the application of machine learning and artificial intelligence to the traditional ads industry.

We recently discussed this attractive industry for investment in a note entitled, "Rapidly Growing Industries."

Within that note, I shared a few TAM charts for the digital ad industry:

eMarketer

As we see, the digital ad industry will continue to grow at healthy rates for the next couple years, and I believe well into the future.

But, in "Rapidly Growing Industries," I specifically highlighted that it's not so much the digital ads industry that's attractive as much as it is the subset digital ad industries within the overall digital ad industry.

Amazon's ads business is comprised principally of its ecommerce digital ads business (the TAM of which is depicted in the first chart just below) and its Connected TV ads business (the TAM of which is depicted in the second chart just below).

Both of these digital ads businesses are growing rapidly within digital ad subset TAMs, which are growing more rapidly than the overall digital ad TAM depicted above.

Ecommerce Digital Ad Spend (Read Description For Precise Definition)

eMarketer

I've not seen many folks discussing this TAM specifically, but I believe it will create a handful of 5x to 10x return businesses in

- Amazon

- Coupang

- Sea,

- and MercadoLibre over the next 10 years or so.

In the past, I've dubbed this cohort "MACS," as an aside.

While Coupang does not currently break out its digital ad sales, we know they're growing rapidly, and we can be reasonably sure that they will, over time, generate $10B+ in very high margin (~70-80% gross margins) sales for the business.

To conclude this section on digital ads, I found this exchange insightful,

Analyst: Our understanding is that ad market environment isn't, wasn't that great in Korea due to macro pressure in second quarter. So, what do you think is driving this performance and where do you think coupon ads are in terms of ad penetration against the GMV and how much runway for growth do you think Coupang still has?

Bom Kim: On advertising, historically, more selection, more suppliers and merchants has led to more customer engagement. That in turn, has led to more opportunities to advertise. We've seen and we expect selection, growth and increase in customer engagement to be key drivers of ad growth in the future. As you point out and as we've mentioned, our advertising business is growing more than twice as fast as our overall business, but we're still very far from our full potential.

Bom Kim, CEO, Coupang Q2 2023 Earnings Call

International Expansion (And Some Thoughts On Sea)

Taiwan is another investment that is thus far exceeding our expectations. We have always believed that the transformational commerce experience we've enabled in Korea could delight customers around the world. We're seeing this play out in Taiwan.

In Q2, Coupang was the most downloaded app in Taiwan. And in the 10 months since we launched Rocket Delivery, Taiwan has scaled faster than Rocket Delivery in Korea did in its first 10 months post launch.

Bom Kim, CEO, Coupang Q2 2023 Earnings Call

I recently shared a bullish note on Sea Ltd. (SE) with you, and I remain quite confident that Sea will do well in the years and decades ahead as a business and as a stock. (As an aside, I believe we're paying about 30x EV/*only Garena's annualized cash flows.* We're getting FinTech, ecommerce, shipping & logistics, and future products for free as of today. But I digress.)

While I do believe Sea will perform well, over the last few years, I took substantial issue with Mr. Li's (Sea's CEO and Founder) decision to basically light shareholder capital on fire by trying to build 3P marketplaces around the world during 2020 and 2021. While he was doing this, I would often remark that Sea would have to withdraw from regions like Europe and Latin America, where MercadoLibre (MELI) and Amazon had already built established, defensible moats/businesses.

Ultimately, this thinking was proven correct, and Sea withdrew from these regions.

Further, I believed that Sea should be spending virtually all of its excess capital on building "superintelligent logistics networks" and "cloud computing data centers" specifically focused and tailored to the SE Asian region, whereby it would solidify its dominance in the region for decades to come.

While I believe Sea will ultimately do these things in the future, there's some chance it's too late in places like Taiwan (for total, monopolistic dominance), where Coupang appears to be gaining real traction by way of its expertise in building aforementioned superintelligent, autonomous logistics networks.

But, while Coupang's success is a negative for Sea, it's unequivocally a positive for Coupang. I believe Mr. Kim has demonstrated that he's an adroit and disciplined capital allocator.

Our bar for new initiatives is high. We've exited investments that didn't meet our internal thresholds and deferred countless others that rank below our most attractive opportunities. So far, Taiwan is leaping over that bar.

In view of that progress, we will invest at a higher level in Taiwan this year. As always, we'll remain disciplined capital allocators, investing more only if the underlying metrics continue to validate our convictions.

Bom Kim, CEO, Coupang Q2 2023 Earnings Call

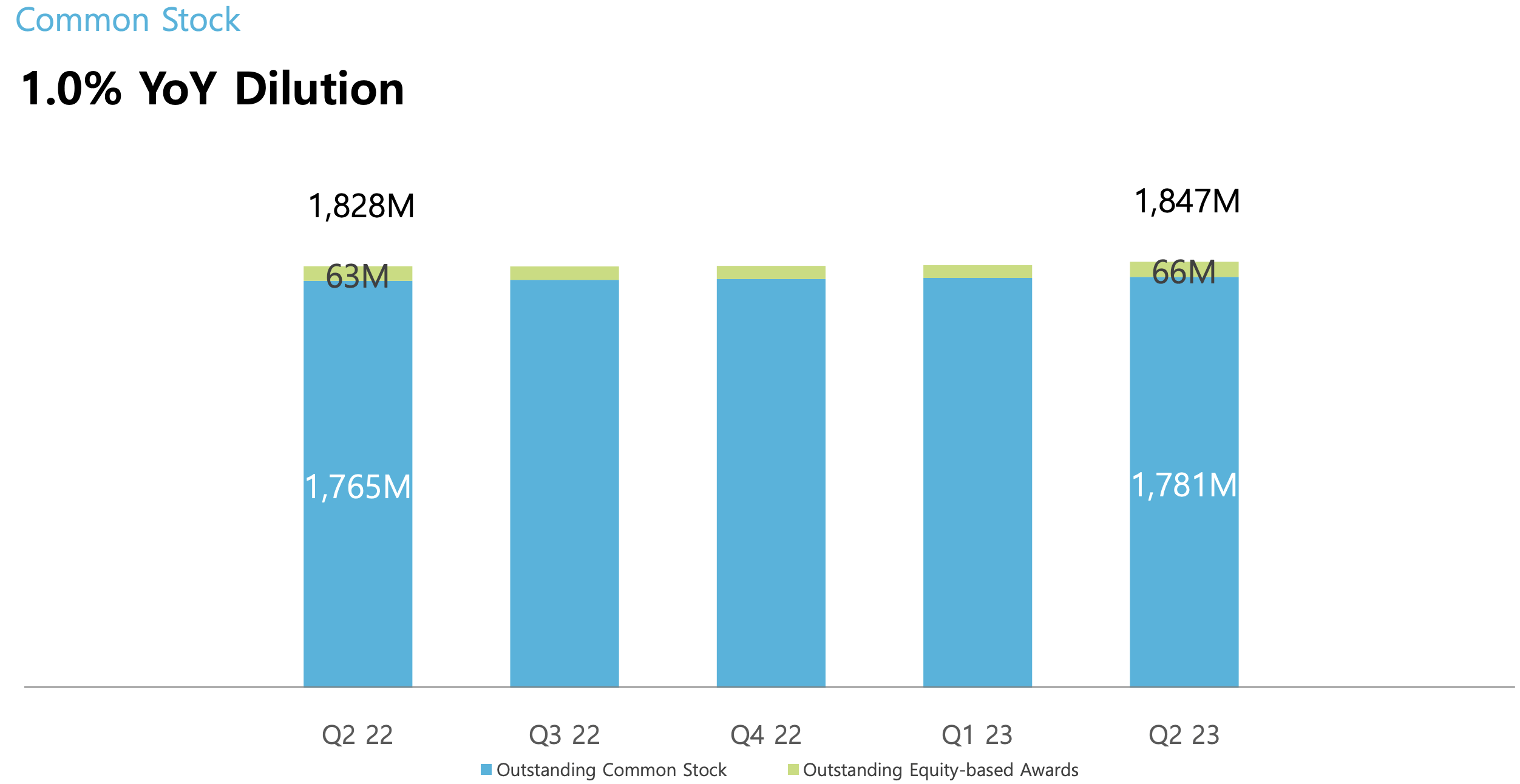

I believe Coupang's dilution dynamics also lend to the idea that the company is exceptionally disciplined in its operations and capital allocation (SBC is effectively capital allocation to "labor.").

Coupang's Q2 2023 Investor Presentation

{kind=link}

Concluding Thoughts: A Long Runway Ahead

On product commerce, it is important to note that we just have a single digit share in the overall retail market opportunity.

Active customers are only about half of the total active shoppers available.

Our active customer growth is accelerating again this quarter. Tens of millions of customers have yet to join wow.

We continue to grow at a multiple of the market, and our active customer growth is accelerating because we've made unparalleled investments and infrastructure and technology that have enabled us to deliver unmatched customer experience and operational excellence that applies to our 1P or FLC, and even our third-party offerings are also growing at a multiple of the overall market.

We're still a tiny share of a retail market that is projected to reach $550 billion in just the next three years. And as we've demonstrated quarter after quarter, we're confident that in any scenario, we'll continue to grow at a multiple of the market.

Bom Kim, CEO, Coupang Q2 2023 Earnings Call

While TAM may be limited relative to Amazon in America and Europe, I do believe Coupang still has a long runway for growth ahead.

Within just South Korea, over the next 10-20 years, I believe it could achieve $100B to $200B in total sales via a mix of total commerce market share capture and launching new product offerings atop its existing business models/product offerings.

Should Coupang successfully gain footholds for its various products in markets like Japan and Taiwan, then I believe this would become an even safer bet to make.

At any rate, the business will likely produce ~10% free cash flow margins based on management's long-maintained guidance for 10%+ EBITDA margins, on which it's been delivering over the last 24 months.

With 10% free cash flow margins on $100B in sales, Coupang could generate robust, defensible cash flows of $10B for shareholders. At 20-30x EV/fcf, the company would trade at between $200B and $300B in enterprise value, and it currently trades at $28B in enterprise value.

And we've not even touched on the free cash flow per share-accelerating impacts of the likely robust share repurchase programs Coupang will execute in the future, which could serve to further accelerate share price appreciation.

Thank you for reading and have a great day.

For further details see:

Coupang: Exceptional, Disciplined Capital Allocation