CPNG - Coupang: Increasing Consumer Surplus Through Autonomy

2023-11-22 08:30:00 ET

Summary

- Today, I will comprehensively walk you through my investment thesis for Coupang, including the underlying mechanisms that have resulted in its market share capture/gains.

- In just 10 years, Coupang has grown from $0 in sales to $24B, and it's continued to grow at about 20% for the last eight quarters.

- Interestingly, the market has priced it such that this growth will stop in perpetuity, but my belief is that Coupang is just getting started.

- In short, I believe Coupang, like Sea Ltd., will prove to be a fairly easy 10x return from these levels. The market agreed from 2015 to 2022! Only recently has it suddenly lost this narrative in its mind, which I believe is our opportunity.

Fast Growers And Inverse Bubbles

As I've mentioned a few times recently, I've been re-reading the Great Peter Lynch's One Up On Wall Street, and I've been having a blast reading it.

While reading it, I came across an excerpt that reminded me that our Four Foundational Investment Frameworks, as well as our tools for investment broadly, are, indeed, timeless methodologies for quality, profitable investment selection.

Let's read the brief excerpt from One Up All Wall Street, then I will interpret it and extrapolate its wisdom to Coupang (CPNG), as well as our entire MACS acronym.

The Fast Growers

These are among my favorite investments: small, aggressive new enterprises that grow at 20 to 25 percent a year. If you choose wisely, this is the land of the 10- to 40-baggers, and even the 200-baggers. With a small portfolio, one or two of these can make a career.

A fast-growing company doesn't necessarily have to belong to a fast-growing industry. As a matter of fact, I'd rather it didn't, as you'll see in Chapter 8. All it needs is the room to expand within a slow-growing industry. Beer is a slow-growing industry, but Anheuser-Busch has been a fast grower by taking over market share, and enticing drinkers of rival brands to switch to theirs. The hotel business grows at only 2 percent a year, but Marriott was able to grow 20 percent by capturing a larger segment of that market over the last decade.

The same thing happened to Taco Bell in the fast-food business, Wal-Mart in the general store business, and The Gap in the retail clothing business. These upstart enterprises learned to succeed in one place, then to duplicate the winning formula over and over, mall by mall, city by city. The expansion into new markets results in the phenomenal acceleration in earnings that drives the stock price to giddy heights.

- One Up On Wall Street by Peter Lynch (Must Read if you're taking this investing journey with me)

For those of you really paying attention to my work, you will likely have already drawn the many parallels captured in the quote between our investments and the great investments of Mr. Lynch's era (e.g., Taco Bell = Chipotle and MACS = Wal-Mart, among others).

Specifically, Coupang possesses the precise characteristics Mr. Lynch looked for in purchasing his "Fast Growers" (which was one out of six categories into which he placed stocks he owned or was considering to own).

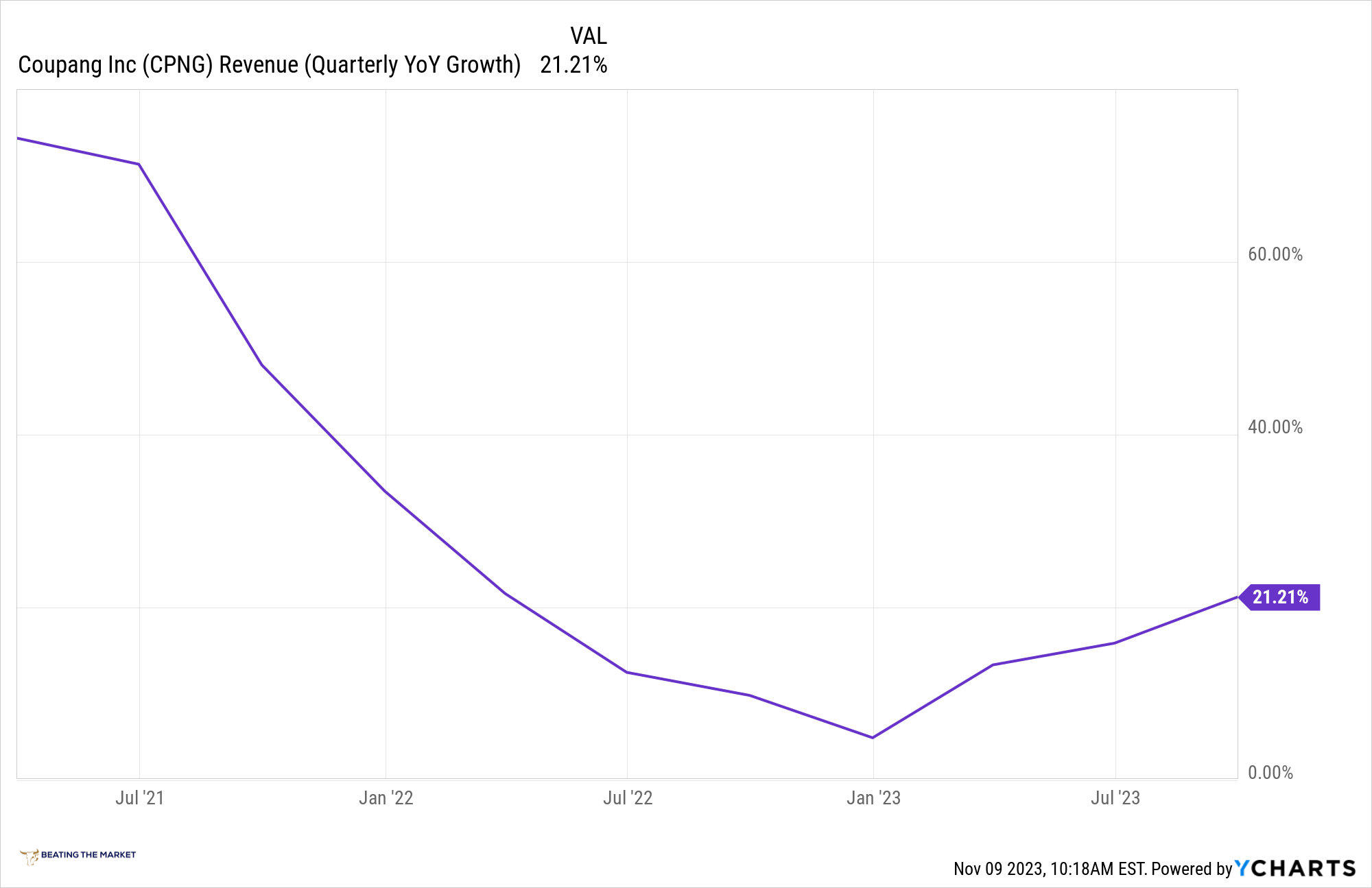

- Coupang has grown at 20%+ consistently since going public.

- Coupang is growing within the stagnant, mature, and boring old retail industry, in which it's rapidly capturing share.

Coupang Grows At 20%+ (FX-Neutral) In Each Quarter Since Going Public

{kind=link}

A fast-growing company doesn't necessarily have to belong to a fast-growing industry. As a matter of fact, I'd rather it didn't, as you'll see in Chapter 8.

All it needs is the room to expand within a slow-growing industry. Beer is a slow-growing industry, but Anheuser-Busch has been a fast grower by taking over market share, and enticing drinkers of rival brands to switch to theirs.

The hotel business grows at only 2 percent a year, but Marriott was able to grow 20 percent by capturing a larger segment of that market over the last decade.

Coupang is, indeed, the quintessential Lynch-style Fast Grower, growing at 20%+ in a stagnant, mature industry, in which Coupang has fielded a considerably differentiated product that continues to capture market share at an incredible clip.

With the overall retail market in Korea growing an estimated 1.3% year-over-year, this quarter continued our years-long trend of growing at a high multiple of the overall retail market. We see that customers increasingly come to the Coupang for the best prices, broadest assortment and fastest delivery experience. Fueled by the strong topline growth across our business this quarter, we generated record gross profit of $1.6 billion, growing 27% over the last year.

This is a sufficient point at which to conclude that Coupang will likely be a good investment in the years and decades ahead; however, I believe it's worth employing my Tools for Investment to more granularly and intimately understand the underlying mechanisms that are driving Coupang's market share capture.

Inevitability

Its market share capture is not mysterious: Coupang's product (ecommerce platform) isn't just "better."

It's differentiated in such a way that it inevitably drives human behavior. It's differentiated in such a way that it creates greater consumer surplus than commerce engines that preceded it, e.g., a gas station or convenience store from which a consumer historically might have purchased a charging cable. Today, that same consumer likely uses Coupang's Dawn, because it offers better price and convenience.

Wall Street Mojo

- Better price = more money saved = more energy saved = greater chance for survival as a living being

- Better convenience = more time saved, and time = money so more time saved = more money saved = more energy saved = greater chance for survival as a living being

This is what I mean by products that create greater consumer surplus are inevitable. Humans are constantly working towards enhancing their likelihood of survival, and products that create greater consumer surplus essentially just increase chances of survival and, as such, achieve adoption rapidly.

Purveyors of the product, by extension, are rewarded by this innate tendency of our reality (and its inhabitants) to work towards survival and replication, and, as a result, they're rewarded with more energy (money in the form of revenue/free cash flow/appreciating stock value).

With this in mind, let's further analyze Coupang's capture of market share within its stagnant, mature Korean retail industry. This process is what I've termed capturing market share within "Inverse Bubbles."

We will look at the Coupang-specific, tangible mechanisms underlying the above-illustrated consumer surplus dynamics, which result in market share capture for Coupang, which results in rapid growth and rapidly appreciating share prices, as Mr. Lynch would have appreciated.

Growing Within Its Inverse Bubble

- It's "Inverse" because Coupang's value (Market Cap) is small relative to the industry/TAM in which it's growing; therefore, Coupang collapses the bubble into itself by consumer market share and, commensurately, expands as the bubble collapses into Coupang's revenue and profits.

Coupang Investor Relations

- Conversely, in a regular bubble, Coupang's market cap would dwarf the industry in which it consumes market share, making the entire situation an unsustainable bubble where the business' value is set to collapse down to the size of the actual market.

As I noted above, Coupang is not just a "better product" capturing market share.

There's more to it. It's more nuanced than this.

We've already discussed the idea that Coupang creates greater consumer surplus which essentially forces human behavior. Let's now consider the operational mechanisms within Coupang's business (as well as the businesses of Amazon (AMZN), MercadoLibre (MELI), and Sea Ltd. (SE), as an aside) that create this consumer surplus.

A Vertically Integrated, Highly Autonomous Commerce Engine (I Shared At The Specific Relevant Timestamp)

Here is the video from which the following quote was taken.

Journalist: How important is it that Coupang is end to end? So you have the ecommerce, you have the fulfillment, you have the logistics, the delivery?

Coupang Executive: You know what, that's our differentiator with our competitors, because we own and operate the entire process.

Coupang's vertical integration, governed largely by artificial intelligence and machine learning, creates a meta-structure commerce engine that intertwines the physical world with the digital world.

Coupang's Digital Marketplace Is A Meta-Structure Atop The Physical World That Allows Consumers To Shop Anywhere Instantly

PC Mag

It affords consumers the ability to have virtually infinite selection alongside unprecedented shopping convenience in a way that legacy commerce engines simply cannot match.

First, we continue to deliver durable growth and expanding profitability, not one at the expense of the other, because of our years of unparalleled investment and an unrelenting focus on both the customer experience and operational excellence.

Second, our flywheel is accelerating . Our selection advantage is a critical component of that accelerating flywheel. In Q3, we expanded selection across both first and third-party. Both active customer and revenue grew even faster than last quarter. Active customers grew 14% year-over-year, faster than the rate of any quarter since the pandemic levels of 2021. We've observed that increasing selection on Rocket leads generally to increasing customer spend on Coupang.

Bom Kim, CEO, Q3 2023 Coupang Earnings Call

This vertical integration of both the digital and physical worlds, governed by AI, is what has driven Coupang's rapid market share growth within the stagnant, mature, existing retail industry in Korea and, hopefully, over time, Taiwan, and it's what will continue to create rapid revenue growth for Coupang in the years and decades ahead.

We continue to see an accelerating growth rate in our active customers, growing at 5% in Q1, 10% in Q2 and 14% in Q3. We now have 20.4 million active customers, adding 2.3 million customers so far this year.

Gaurav Anand, CFO, Q3 2023 Coupang Earnings Call

Of course, this isn't exactly novel: Amazon and MELI have been at this game for the last 20-30 years, creating unprecedented feats of business growth in the process.

Coupang, to a very large degree, is just replicating Amazon's playbook, but, I must say, the company is doing it exceptionally; perhaps better than Amazon itself!

Likening Coupang to Amazon is a perfect segue to our next point of consideration for Coupang: its valuation.

Valuation Analysis: Competent Capital Allocators

One of the most striking aspects of working with the Coupang management team has been their ability to articulate their quantitative investment thesis.

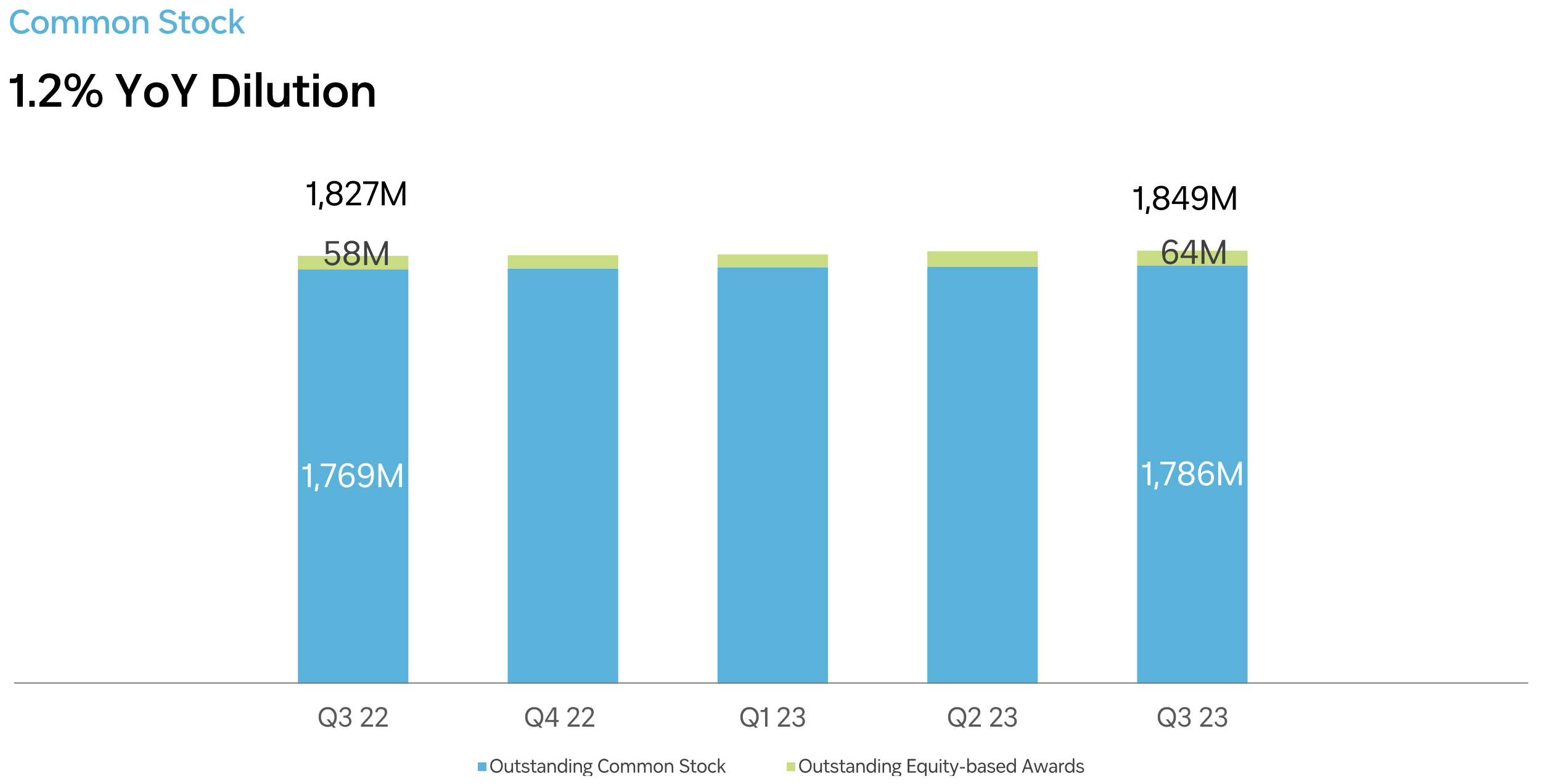

Coupang Scantly Dilutes Despite Being So Young

{kind=link}

Prominently featured at the start of Coupang's Q3 2023 earnings presentation was the above slide in which the company's share dilution is illustrated.

Throughout Coupang's earnings call, it specifically discussed free cash flow margins often, as opposed to adjusted operating margins this or adjusted EBITDA margins that.

The company often incisively conveys what truly creates shareholder value... to its shareholders! Astoundingly, this has become something of a novel concept in modern technology investing.

The Drivers Of Equity Value Creation

- Sales and gross profit growth (as a proxy for free cash flow growth)

- Share dynamics

- Free cash flow generation and free cash flow margins

Combined, these three variables result in the fundamental basis of all equity value:

- Free cash flow per share

To our shareholders:

Our ultimate financial measure, and the one we most want to drive over the long-term, is free cash flow per share.

Jeff Bezos, Executive Chairman, Amazon 2004 Shareholder Letter

I mean Coupang does an even better job than Amazon at articulating its investment thesis through this essential and immutable lens of value creation.

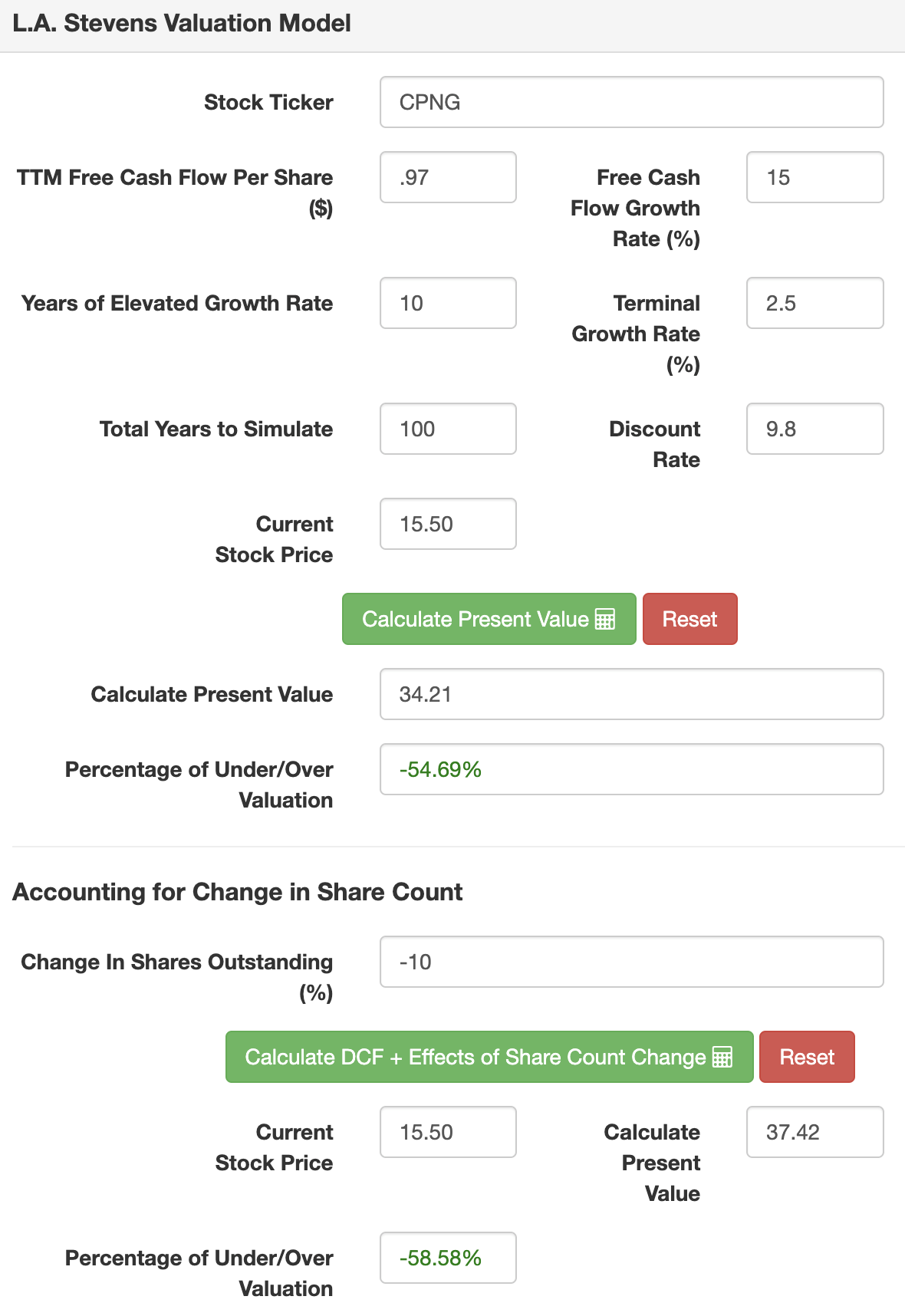

With these ideas in mind, I believe we can trust management's projections for free cash flow margins long term. I will reference these projections, as well as my own assumptions, in the next section in which I will share my conservative valuation for Coupang.

Valuing Coupang

Below, you will read my key assumptions for valuing Coupang based on the growth of free cash flow per share.

Because Coupang is very aggressively reinvesting for growth, I must assume long run free cash flow margins whereby I accurately appraise the value of the business. Essentially every truly great investment I've ever made, e.g., Tesla (TSLA), Amazon, Nvidia (NVDA), Chipotle (CMG), Apple (AAPL), and others, has been as a result of investing in this fashion, and, granted we start by assessing the key economic moats of the business, whereby we determine its ability to generate free cash flow and deliver on the projections management has set forth, I believe it's prudent to continue doing so.

To this end, the valuation below relies on one key assumption:

- Free cash flow margin will hit 7.5% by year 10 of the model.

Considering management has guided for "10%+ adjusted EBITDA," and has stated:

Generally, we expect that free cash flow on a TTM basis will be closer to the levels of adjusted EBITDA generated. As we continue to achieve even higher levels of cash flow generation, we remain committed to prioritize our capital allocation to those opportunities we believe will generate the highest level of long-term shareholder value.

Gaurav Anand, CFO, Q3 2023 Coupang Earnings Call

I believe this free cash flow margin is achievable.

Notably, we will not use 10% free cash flow margins, as the above language and projections would suggest we should use. Instead, we will bake in conservatism in both long run free cash flow margin and next 10 years worth of revenue growth rates in our model below.

But the underlying drivers of margin are strong. The underlying trends in margin are strong and have a lot of room for expansion. We remain very confident in our long-term guidance of over 10% adjusted EBITDA and corresponding free cash flows.

Gaurav Anand, CFO, Q3 2023 Coupang Earnings Call

Assumptions:

| TTM Sales [A] |

| $24 billion |

| Potential Free Cash Flow Margin [B] |

| 7.5% |

| Average diluted shares outstanding [C] |

| ~1.849 billion |

| Free cash flow per share [ D = (A * B) / C ] |

| $.97 |

| Free cash flow per share growth rate (conservative) |

| 15% |

| Terminal growth rate |

| 2.5% |

| Years of elevated growth |

| 10 |

| Total years to stimulate |

| 100 |

| Discount Rate (Our "Next Best Alternative") |

| 9.8% |

Using these assumptions, we can calculate Coupang's fair value and projected returns.

{kind=link}

Notably, I assumed a 10% reduction in total shares outstanding.

Considering how exceptionally efficient Coupang has been from a dilution perspective, I believe either 1) it will reduce shares by this much by 2034 and/or 2) it will have accumulated such a massive cash hoard as to easily be able to do this.

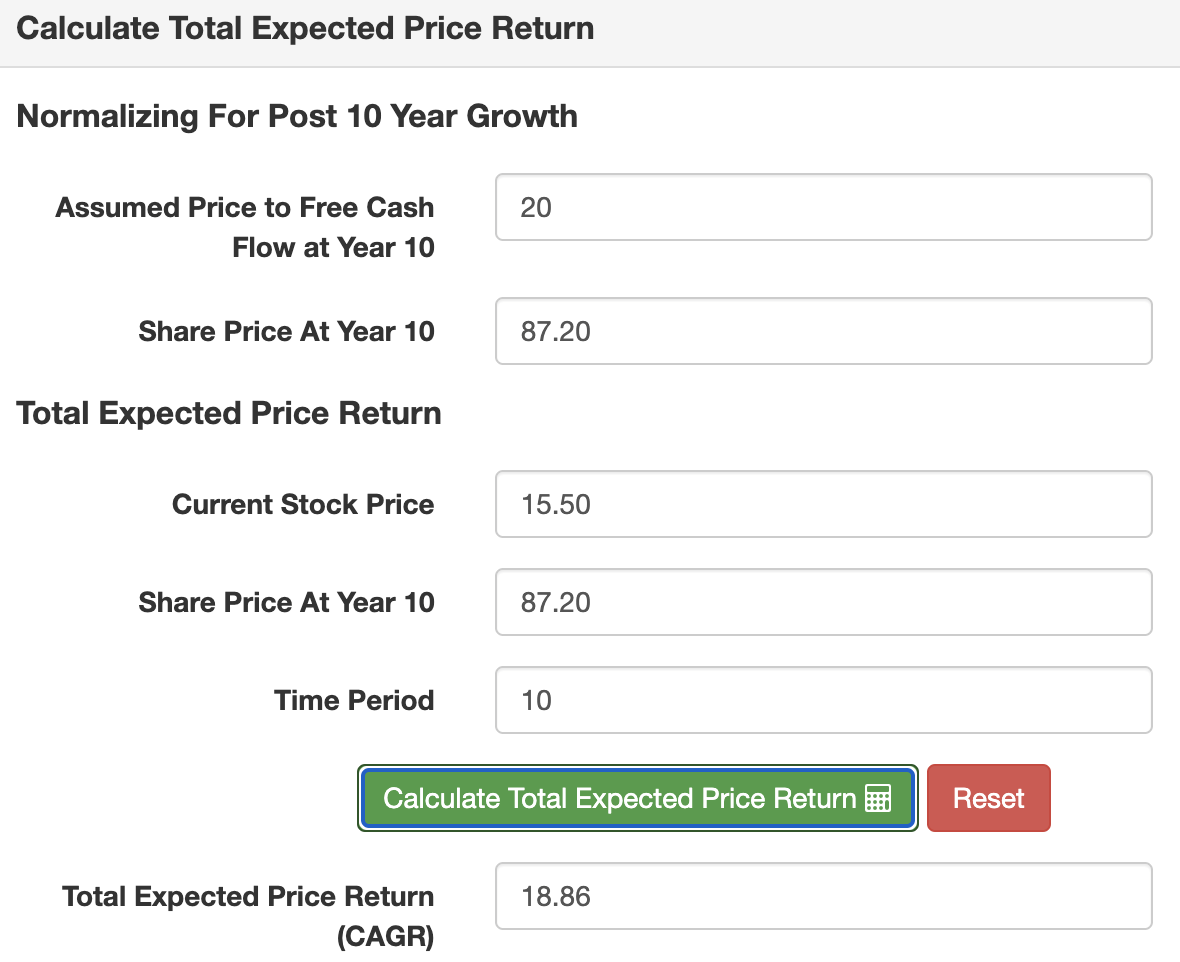

Turning to projected returns:

{kind=link}

As you can see, I used what I believe to be a conservative 15% growth rate, a conservative 7.5% long run free cash flow margin, and a conservative exit multiple by year 10 (because Coupang will likely be growing at 10%+, if not more, by that time).

And we're still getting ~19% annualized returns.

I think, from these levels, there's a solid chance we get closer to 30% annualized returns, especially as the capital return programs begin to kick in over the next one to two decades.

Concluding Thoughts: Digital Ads & TAM Expansion

I've been almost endlessly discussing the idea that MACS (an acronym for MercadoLibre, Amazon, Coupang, and Sea Ltd.) is experiencing a genuine "GOOG-like search engine ads scaling" event, which will drive their share prices for years and decades to come.

I've also noted that the market appears to be totally asleep at the wheel as to the significance of this source of revenue for these companies, and this is certainly the case for Coupang.

Within our Product Commerce segment, gross profit margin improved 250 basis points year-over-year where we continue to generate further improvements through supply chain optimization, operational efficiencies and scaling of newer offerings like ads.

Gaurav Anand, CFO, Q3 2023 Coupang Earnings Call

Amazon generates about 4-5% of GMV in 40-60% free cash flow margin digital ads sales.

Coupang will very likely generate similar levels of digital ad sales over time, suggesting that, as it reaches $100B in GMV and beyond by the late 2020s/early 2030s, it will generates billions in very high margin digital ad revenues, which buttresses the case for a 7.5% long run free cash flow margin.

To close this note, it would not be a Coupang review without touching on the company's central bear thesis: its TAM.

Coupang expanded into Japan in recent years, but recently quit that expansion and withdrew from the region, much to my disappoint I will note.

Today, Coupang is expanding in the 24M person Taiwan, and this expansion appears to be going well so far.

Finally, our conviction about the long-term potential in Taiwan continues to strengthen. We launched Rocket Delivery in Taiwan in October of 2022, and the offering in Taiwan has scaled much faster in its first year of operation than it did in its first year in Korea. And our app is on pace to be the most downloaded app in the market for all of 2023. We are off to a promising start.

Bom Kim, CEO, Q3 2023 Coupang Earnings Call

Mr. Kim went on to say,

As we've noted, we are seeing strong momentum in both Taiwan and Eats. I'll start with Taiwan. It's only been a year in Taiwan since we've launched Rocket Delivery. But our growth in that first year has been faster in Taiwan than it was in Korea. And as you know, we remain very confident in the overall model of Rocket Delivery. We've been delighted by the customer response so far. We still have a lot of work to do to not only build the kind of customer experience we want there, but also the operational experience, the excellence, that we've set our sights on. And as you continue to see us improve customer experience and improve operational excellence, you should see us able to capture growth and profits, not one at the expense of each other, as we've demonstrated in our first market, Korea.

Bom Kim, CEO, Q3 2023 Coupang Earnings Call

It's heartening that Coupang is winning in Taiwan, and, should Coupang develop a permanent and profitable foothold in the region, especially with its WOW membership program, then my previously shared valuation assumptions will be far too conservative.

So Taiwan is not necessary to the thesis, but it's certainly worth noting and a victory in Taiwan would substantially shift our annualized returns upward.

We believe we still have significant opportunity ahead [in Korea alone] in both number of active customers and spend per customer. Our active customer count is just 20 million and our single-digit share of the total retail market indicates a low share of wallet today. We believe the continued expansion of selection on Rocket via our first-party offering and FLC will help drive a higher share of both active customers and total retail spend.

Bom Kim, CEO, Q3 2023 Coupang Earnings Call

In short, I believe Coupang will be a 10x return from these levels. As such, the risk = return equation is way, way out of whack, giving us far more in the way of returns relative to the risk we assume in purchasing Coupang today.

For further details see:

Coupang: Increasing Consumer Surplus Through Autonomy