ETSY - Coupang: Ongoing Business Strategy Should Further Strengthen Competitive Position

2023-07-19 01:02:22 ET

Summary

- I reiterate my buy rating for Coupang, as I expect the Eats 'discount' strategy and international expansion will continue to drive success.

- CPNG expanding scale advantage, combined with its logistical lines and efforts to increase WOW membership, gives it a competitive edge in the market.

- Despite its current lack of profitability, I believe the business is on the right track to become much more profitable.

Investment action

I recommended a buy rating for Coupang ( CPNG ) when I wrote about it the last time as I expected Coupang Eats and Fulfilment & Logistics to further strengthen its competitive position. Based on my current outlook and analysis on CPNG, I reiterate a buy rating as I expect CPNG to continue driving success via the Eats 'discount' strategy and its international strategy to start yielding results.

Business

CPNG is an e-commerce business. The Company offers dynamic end-to-end e-commerce and logistic solutions. By investing heavily in mobile app development and creating its own end-to-end logistical operations, CPNG has quickly risen to become one of the leading e-commerce companies in Korea. It is thanks to this strategy that the firm has been able to expand at such a rapid rate and give its clients a safe, secure, and hassle-free online purchasing experience.

Industry & Peers

Research and Markets estimates that by 2026, the South Korean e-commerce market would be valued $390 billion, up from its current level of roughly $189 billion. This represents a staggering CAGR of 19.9% over 4 years. It's hardly unexpected that the industry is developing at such a clip, given the increasing number of people who have access to the internet, the advent of artificial intelligence in retail, the spread of cities, the popularity of online advertising, and the proliferation of smartphones. CPNG, eBay, Lotte Shopping, Naver Corp, SK Telecom, and SSG.com are among the top companies in this sector.

Qualitative review

I still have faith in CPNG Eats' 'discount' approach since I believe it is a part of larger efforts to increase WOW membership, which in turn brings in more consistent revenue and data, as opposed to simply increasing market share. In particular, I anticipate that CPNG's expanding scale advantage will be propelled by the combination of the WOW members cohort and the Coupang Eats cohort as the density of its logistical lines increases. The larger the total number of members, the more of an edge CPNG has in the market.

However, I anticipate that CPNG will enhance the unit economics of EATS and eventually discover a method to connect the ecosystem more closely together, such as providing discounts that only a scaled player can afford to offer. This would leave the smaller player with little choice but to burn funds for an extremely extended period of time, which is not a desirable strategy given the current state of the market.

In addition, I have faith in CPNG's overseas strategy, which is not limited to penetrating large markets and increasing market share, but rather involves actively seeking out new areas that CPNG believes are ready for disruption and can be leveraged with the company's current offerings (3Q22 earnings call). I think Taiwan is a promising market because of the many parallels it has with Korea (1Q23 earnings call). Moreover, the e-commerce market in Taiwan is substantial, with an expected valuation of $23 billion in FY26 .

Quantitative analysis and Valuation

{kind=link}

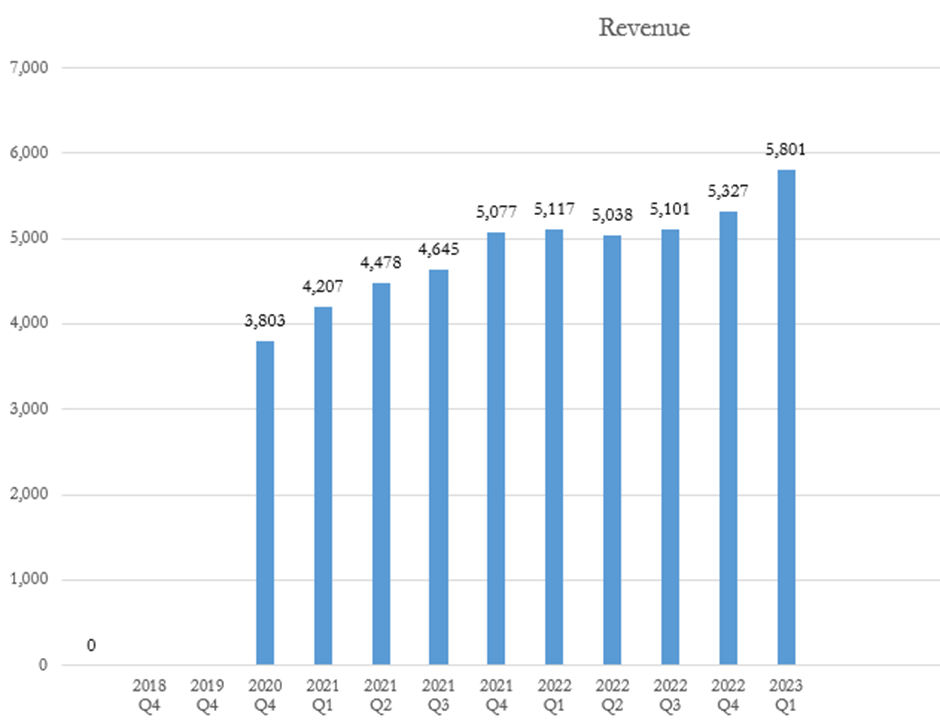

In the most recent quarter, CPNG increased revenue by 20% in constant currency, which I believe demonstrates CPNG's ecommerce superiority as compared to industry growth. CPNG is also rapidly expanding its Fulfilment by Coupang [FLC] at a pace of 90%. In my opinion, the faster FLC grows, the stronger its competitive position gets, as it CPNG further cements its route density strength.

{kind=link}

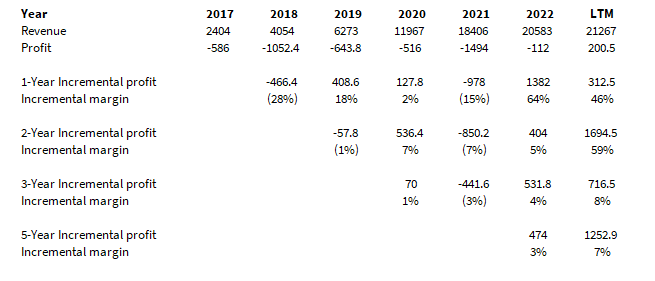

One analysis that I like to do for all companies is incremental margin analysis. As the market focuses more on profitability, it is encouraging to see CPNG becoming profitable, and the incremental margin signals more margin expansion potential.

{kind=link}

{kind=link}

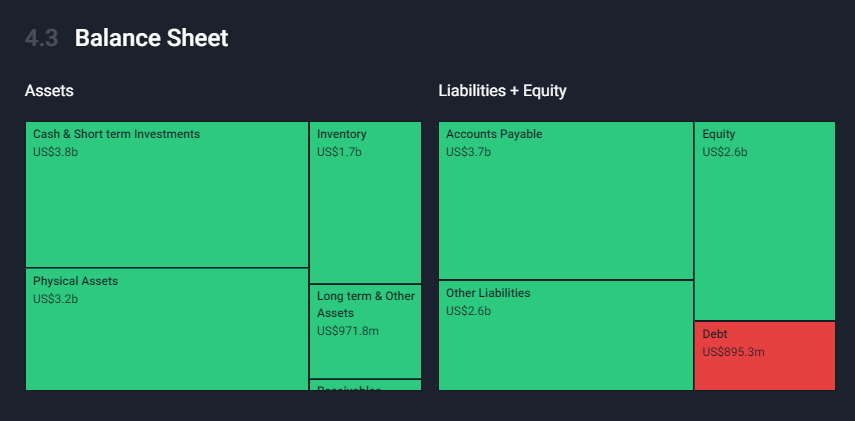

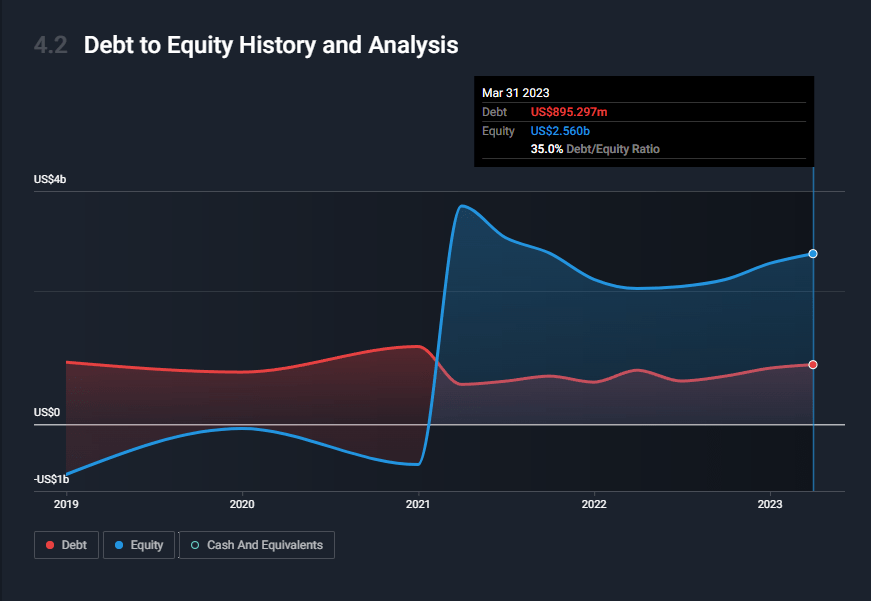

CPNG has a secure balance sheet because it has $1.4 billion in net cash. With $1.4 billion, I believe it is plenty for the company to reinvest aggressively in order to stay far ahead of competition. Particularly now that the company is profitable, I anticipate that the balance sheet will improve in the future.

{kind=link}

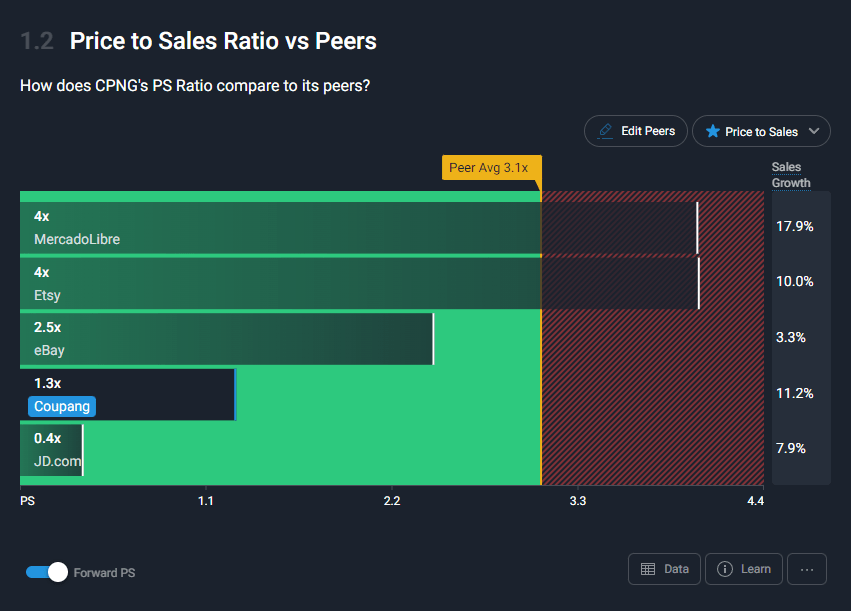

CPNG is not generating meaningful profits at the moment, so P/S is a better valuation metric.

CPNG is now valued at 1.3x ahead PS, however I believe this is excessive considering the expected growth pace. When comparing CPNG to ETSY, the valuation discount is unusual, despite the fact that the two stocks have identical growth rates. While I agree that Etsy ( ETSY ) is much more profitable, therefore the premium, I believe the value difference will eventually decrease given that CPNG is on its way to become far more profitable today.

Based on my expectations, CPNG should be able to grow faster than the industry given its strong competitive position. I modelled a slowdown in FY23 due the macro-economic situation, followed by a 25% growth rate until FY25 (growing faster than the industry as it continues to capture share). Attaching the same multiple as what ETSY is trading at (2.5x forward P/S) based on my expectation for CPNG FY25 revenue would suggest a share price of $52 in FY24, a 190% upside.

Author's work

Risk and final thoughts

Since the market is fixated on CPNG's profitability improving, underwhelming performance will damage the story's credibility. As a result, profitability may be harmed if the pace at which FLC is adopted is lower than anticipated, as implementing FLC necessitates initial investments that inflate the fixed cost.

In conclusion, I have faith in CPNG Eats 'discount' approach and its efforts to increase WOW membership, which can generate consistent revenue and data. The company's expanding scale advantage, combined with the density of its logistical lines, gives it a market edge. Additionally, Coupang's overseas strategy, particularly in Taiwan, shows promise for further expansion.

While CPNG profitability is not yet significant, its improving financials and secure balance sheet provide confidence for future growth. The current valuation discount seems too much, considering the growth and my expectation that it is going to be much more profitable than toady. Hence, I anticipate a closure in the valuation gap compared to similar companies like ETSY.

For further details see:

Coupang: Ongoing Business Strategy Should Further Strengthen Competitive Position