CPNG - Coupang Q3 Earnings: Overcoming Challenges And Innovating For Growth

2023-11-09 14:53:36 ET

Summary

- Coupang, Inc.'s robust logistics network and diverse product selection drive customer growth to 20 million.

- I now believe that Coupang could see about $2.2 billion of free cash flow in 2023. This leaves Coupang priced at 12 times forward free cash flow.

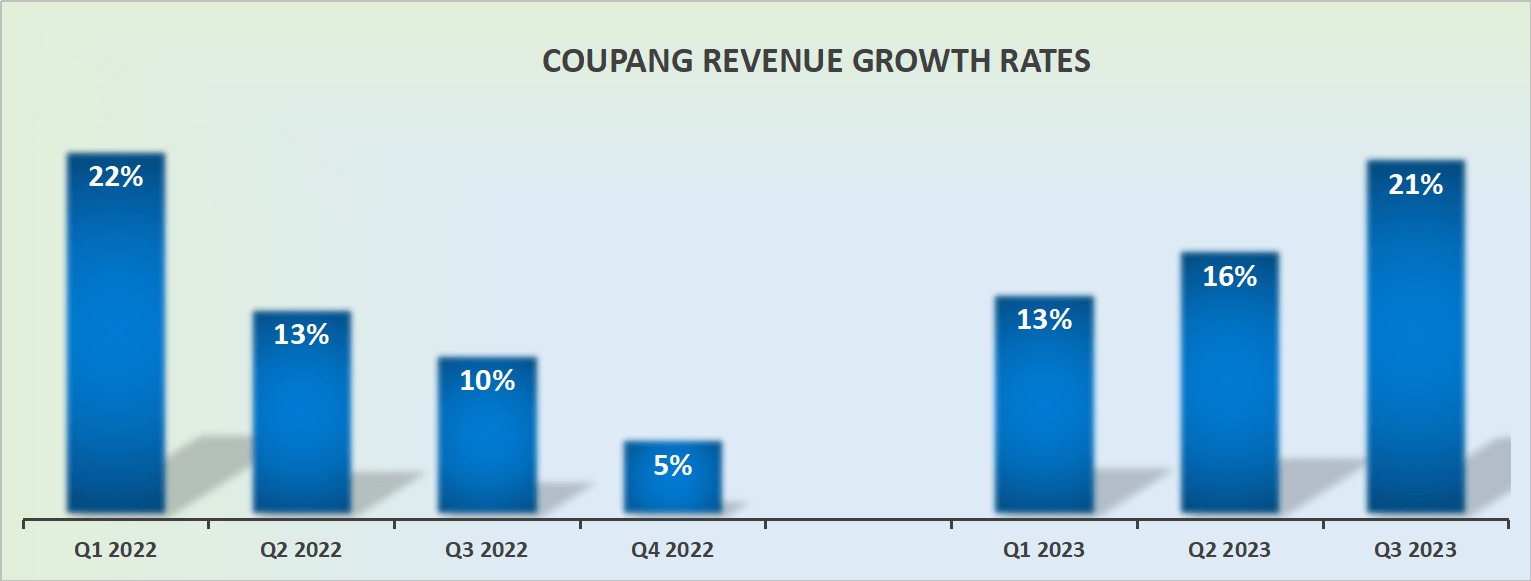

- Coupang's revenue growth rates are promising for future profitability.

Investment Thesis

Coupang, Inc. (CPNG) delivered Q3 results that led to the stock selling off. Indeed, as investors have continued to embrace a risk-off sentiment, anything that is not the magnificent 7 mega caps appears not to be rewarded with any positive traction.

Even though, according to my estimates, Coupang's valuation is now priced at a very attractive 12x forward free cash flows, I won't go so far as to declare that Coupang has any sort of impregnable moat, akin to Amazon (AMZN). However, with 20 million active customers and growing, I believe this stock is unjustifiably cheap.

Quick Recap,

In my previous analysis , I said,

According to my estimates, by the time Coupang exits 2024, this business could be on a path toward $2 billion of free cash flow. This would leave this giant South Korean e-commerce business priced at 15x forward free cash flows.

This multiple looks very reasonable, particularly given that Coupang is likely to be growing at mid-teens to 20% CAGR, as its comparables improve.

Not only do I stand by that prior assessment, but given this latest set of results, I've upgraded my free cash flow estimate, as you'll see.

Coupang's Near-Term Prospects

Coupang is a leading South Korean online marketplace. With an easy-to-use interface, users can effortlessly shop for a variety of items, including electronics, apparel, groceries, and household essentials.

What distinguishes Coupang from its competitors is its pioneering logistics and delivery strategy. In particular, the company has established a comprehensive internal logistics system comprising fulfillment centers, allowing it to offer swift same-day or next-day delivery options to customers throughout South Korea.

Coupang's future prospects appear promising, propelled by its unwavering dedication to enhancing customer experiences and the company's persistent pursuit of innovative solutions. The continued expansion of its logistics network and the diverse product selection have contributed to the solid growth of active customers.

In fact, it should be said that the number of active customers grew by 14 percent y/y, the fastest since the pandemic in 2021. Increasing selection on Rocket leads to higher customer spending on Coupang.

Moreover, the success of the WOW membership program, the equivalent of Amazon Prime, has not only bolstered customer engagement across multiple service sectors but also highlights the potential for continued expansion, particularly within the rapidly growing Eats segment.

Furthermore, Coupang has been striving to diversify from its core Korean market. During the earnings call , we heard that its expansion into Taiwan has yielded encouraging outcomes, with the market displaying a positive reception. Indeed, Coupang noted that its app is on pace to become the most downloaded app in Taiwan for all of 2023.

Given that context, let's discuss some nuanced matters.

Revenue Growth Rates Are Still Attractive

{kind=link}

There are some positive and negative matters to consider. The positive aspects undoubtedly point to its steady and reassuring growth rates. What's more, the next several quarters don't appear to be too challenging compared with the prior year's quarters, meaning that Coupang should easily be able to sustain a mid-10s% percent CAGR for a while.

Meanwhile, Coupang faces challenges too. One notable challenge is the intensifying competitive landscape, particularly from emerging players in the e-commerce space, including new entrants such as TMall and AliExpress, which pose serious threats to Coupang's market share and customer base.

Moreover, the company grapples with the pressure to maintain competitive pricing and promotions while simultaneously ensuring sustainable profitability, which is weighing on its profitability, the topic that we'll discuss next.

Profitability Profile Discussed

Coupang grapples with the continued optimization of its internal logistics network, particularly in managing the growing demands for swift same-day deliveries, as well as continual investments in new merchant acquisition costs, which have exerted temporary strains on the company's margins, requiring careful management and strategic decision-making to strike a balance between growth initiatives and cost efficiency.

Here's a quote from the earnings call that supports this statement,

There are some one-time expenses such as investment in new selection or merchant acquisition that might affect a quarterly snapshot of margins. But the underlying drivers of margin are strong. [...] We remain very confident in our long-term guidance of over 10 percent adjusted EBITDA and corresponding free cash flows.

Furthermore, expanding into new markets such as Taiwan poses operational challenges and necessitates significant investments in infrastructure, demanding strong execution.

Altogether, this has translated into its EBITDA margins not delivering any sort of margin expansion. Indeed, compared with the previous year, Coupang's EBITDA has remained around 4 percent, more than 110 basis compression from Q2 2023.

Put another way, I previously believed that Coupang could exit 2024 delivering $2 billion of free cash flow. However, Coupang is already reporting $1.9 billion of free cash flow on a trailing basis. Naturally, given its strong determination and growth prospects, I believe this figure should be updated by at least 15 percent year-over-year.

Consequently, I now believe that Coupang could see about $2.2 billion of free cash flow in 2023. This leaves Coupang priced at 12 times forward free cash flow, despite clearly achieving at least mid-teen growth rates.

The Bottom Line

Despite the challenges Coupang encounters, including heightened competition from emerging e-commerce players and the ongoing need for strategic pricing and operational efficiency, the stock's valuation remains strikingly appealing.

Trading at 12x its forward free cash flow, Coupang presents a compelling investment proposition given its substantial growth potential, continually expanding customer base and innovative logistics solutions.

With an established track record of solid performance and an anticipated increase in free cash flow, Coupang, Inc.'s current valuation seemingly underestimates its potential to deliver sustained mid-teen growth rates, making it an attractive option for investors.

For further details see:

Coupang Q3 Earnings: Overcoming Challenges And Innovating For Growth