CPNG - Coupang: Strong Moat But Overpriced

2023-03-16 09:09:53 ET

Summary

- Coupang's revenue growth is decreasing, but its profitability is rising.

- The company has a competitive edge through its logistics infrastructure and 11 million WOW subscribers.

- However, leveraging these strengths outside of South Korea may not be viable.

- Based on my DCF valuation, Coupang's intrinsic value per share is $11, indicating that the current stock is slightly overpriced.

Editor's note: Seeking Alpha is proud to welcome Value Compounder as a new contributor. It's easy to become a Seeking Alpha contributor and earn money for your best investment ideas. Active contributors also get free access to SA Premium. Click here to find out more »

Editor's note: Seeking Alpha is proud to welcome Value Compounder as a new contributor. It's easy to become a Seeking Alpha contributor and earn money for your best investment ideas. Active contributors also get free access to SA Premium. Click here to find out more »

Investment Thesis

Coupang's ( CPNG ) recent success in achieving net profitability over the last two quarters can be attributed to its exceptional logistics infrastructure and the increasing number of WOW members. These factors demonstrate the company's strengths and lead me to believe that Coupang will continue to thrive, with an estimated operating margin of 7% in 10 years.

However, I believe that these strengths may also limit the company's potential for growth outside of Korea, as expanding into international markets would require significant investment. Additionally, other e-commerce players in Korea are likely to remain competitive even if Coupang continues to expand its market share. Therefore, I estimate that Coupang's market share will not exceed 30%.

Based on these assumptions, my DCF model calculates an intrinsic value of $11 per share. Given that the current stock price is slightly higher than this estimated intrinsic value, I recommend a "hold" position on the stock.

Review of 2022 Q4 and Annual Earnings

Coupang reported Q4 2022 results on February 28th, marking the second consecutive quarter of net profitability. While revenue increased by 21% QOQ and 26% YOY in constant currency, growth decelerated due to the pandemic and sluggish consumer sentiment. However, the company's gross margins improved, rising to 23% YOY in 2022. Coupang's WOW membership base also grew by 20% YOY, reaching 11 million subscribers.

Overall, the company's revenue growth is slowing, but profitability is improving.

Key Strengths and Weaknesses of the Business

Strengths

Coupang's key strength is its superior logistics infrastructure, with 70% of South Korea's population living within 10 minutes of its fulfillment centers. Despite experiencing around $6 billion in losses building this infrastructure, it has paid off in accurate inventory management and same-day delivery. Coupang has already won the competition with other Korean retailers, as there are no shareholders in other retail companies who would accept such losses to build infrastructure and supply management systems.

Additionally, Coupang's 11 million WOW membership subscribers provide another strength. As the number of subscribers increases, the company can offer more competitive prices and accumulate more reviews, giving it a network effect and bargaining power against suppliers.

Weaknesses

Coupang's logistics infrastructure, while a key strength, presents a challenge for expansion outside of Korea, as heavy investment would be required to replicate the infrastructure in another country. As a result, success in expanding beyond Korea may be unrealistic.

Furthermore, Coupang's operating costs structure presents another challenge, with most of its warehouses and fulfillment centers still relying on a labor-intensive model, despite implementing an automated logistics system in one center. As a result, the company may not fully benefit from operating leverage when revenue increases.

Intrinsic Valuation - Discounted Cash Flow Model

Factors of Discounted Cash Flow Valuation

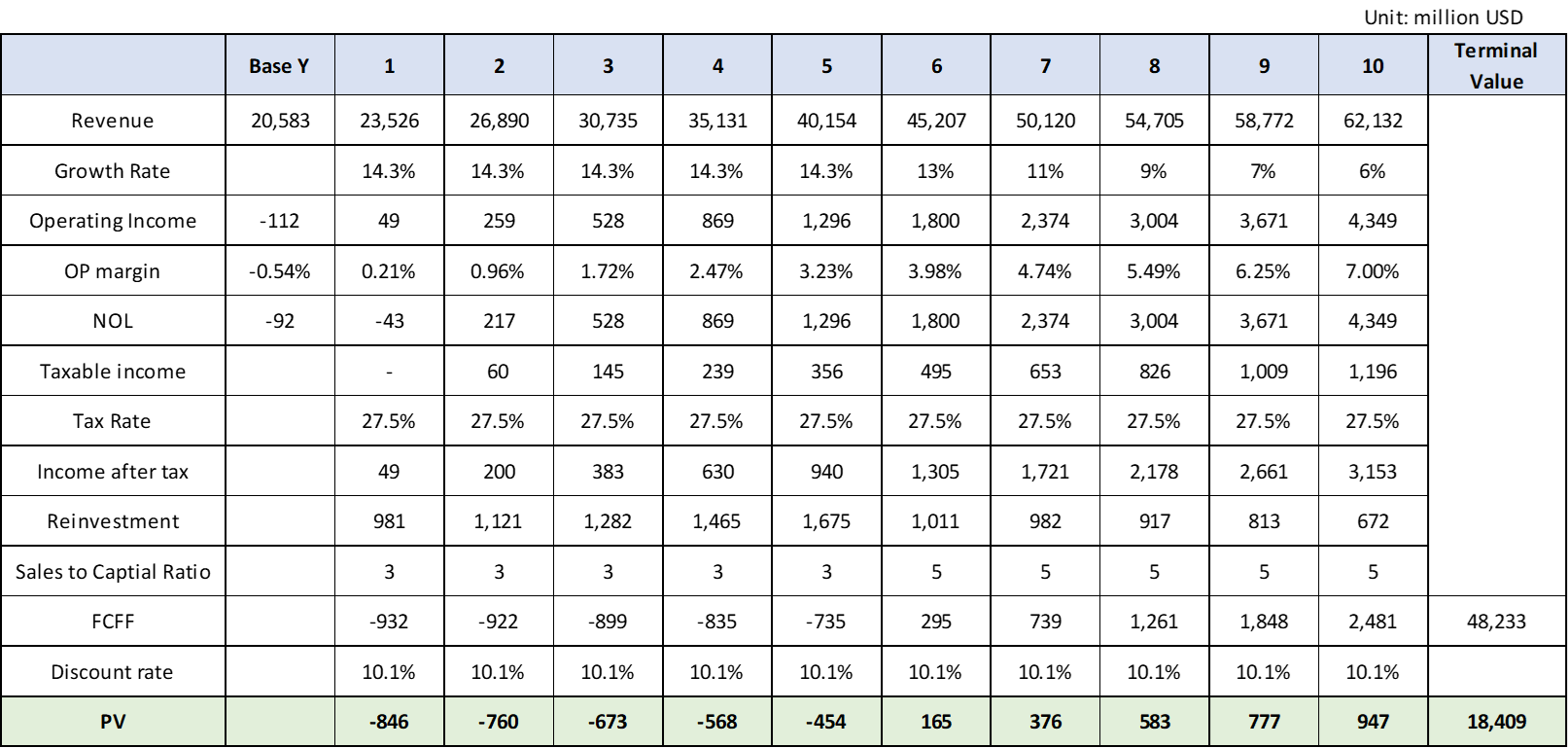

To perform a discounted cash flow valuation ((DCF)) for Coupang, it is necessary to determine the timeframe for projecting the company's free cash flow. As Coupang's revenue growth exceeds 10%, a 10-year projection is appropriate.

In my DCF model, four key factors influence the intrinsic value: revenue in 10 years, operating margin in 10 years, reinvestment, and discount rate. I will outline the specifics of my projection below.

Revenue in Year 10

While Coupang's revenue growth is decreasing, it remains high. Predicting their exact revenue growth for the next decade is unrealistic. It's more reliable to project its revenue in 10 years and estimate the growth rate through reverse engineering.

Business Model and Total Addressable Market

To estimate Coupang's revenue in 10 years, I should define its business model and total addressable market. Coupang's revenue is primarily from product commerce in Korea, and its logistics infrastructure competitive edge may not translate to expansion outside of Korea. Therefore, assuming Coupang remains a Korean e-commerce player, its total addressable market in 10 years will be the size of the Korean e-commerce market.

Coupang's investor presentation indicates that the Korean commerce market was worth $446 billion in 2022 and is expected to grow to $547 billion by 2026. Assuming a 4% of economic growth after the period, I estimate the market will reach $689 billion in 10 years.

To estimate Coupang's revenue in 10 years, I need to determine the e-commerce penetration rate. Currently, the rate in Korea is 37% , but I anticipate it will reach 50% in a decade due to the changing perception of online buying and selling (e.g. buying perishable items such as vegetables online). Thus, I project the Korean e-commerce market size to be $346 billion, which is Coupang's total addressable market in 10 years.

Estimating Revenue per Gross Merchandise Value

To estimate revenue based on market share, I should know how much GMV is converted to revenue. Although Coupang doesn't disclose its GMV, I estimate that the revenue per GMV is around 60% based on external sources and the company's reported revenue. As I project Coupang's business model remains the same, I expect the revenue per GMV to remain at 60%.

Market Share and Revenue in 10 Years

According to my calculation, Coupang's current market share is estimated to be 21% (market share = revenue / revenue per GMV / total size of the e-commerce market).

Although the company's revenue growth is high, it is unlikely that Coupang's market share will exceed 30% in the next decade. This projection is based on the fact that Amazon, which operates in the US, has less than 40% of the e-commerce market share despite having no comparable competitors in the US. In Korea, there are still several viable players, including Naver (KRX: 035420), a leading search and advertisement platform, SSG.com, an online shopping platform operated by the biggest retail company in Korea Shinsegae Inc (KRX: 004170), and E-mart (KRX: 139480), which will affect Coupang's market share growth.

Based on my projection of a 30% market share, Coupang's estimated revenue in ten years is approximately $62.3 billion (revenue = market size x market share x revenue per GMV).

Operating Margin and Income After Tax

Operating Margin in Year 10

Coupang uses adjusted EBITDA margin instead of operating margin to report profitability. During the 2022 4Q earnings call , the company provided a long-term guidance of 10% or higher for EBITDA margin.

Coupang generates Product commerce revenue through two models, direct product sales, and commission from its marketplace and fulfillment solution. The former model is similar to retailers such as E-mart, which had an operating margin of 5% prior to Coupang’s rise. The latter model is similar to other marketplaces with operating margins over 10%. Based on the mix of revenue recognition models, the company's guidance appears reasonable. Factoring in depreciation and amortization, I estimate Coupang's operating margin to be around 7% in 10 years.

Tax Rate

In my DCF valuation of Coupang, I used a US marginal tax rate of 27.5% (25% + 2.5%) for the company's operating income after tax. However, based on Coupang's 2022 10-K report , the company had net operating losses of $92 billion. As a result, the company will not be subject to any income tax until its operating income offsets this accumulated deficit.

Reinvestment

To facilitate its growth, a company must allocate resources to reinvestment. Coupang's sales to capital ratio for the past two years has been around 3. Given the company's expansion plans, it is my projection that Coupang should continue to reinvest at a similar pace. Then a sales to capital ratio of 5 will be reasonable estimation once it achieves its objective of covering 90% of the population with Rocket delivery.

Discount Rate

Even though Coupang primarily operates in Korea, the company reports earnings and trades stocks in US dollars. Therefore, I calculated the cost of capital in US dollars.

For the cost of equity calculation, I used a risk-free rate of 4%, based on the US 10-year treasury yield. Additionally, I factored in a Beta of 1.07 and an equity risk premium of 5.11%. Since the majority of Coupang's business is in South Korea, I included a country risk premium of 0.85%. These inputs resulted in a cost of equity of 9.82%.

In terms of the cost of debt, I used a risk-free rate of 4%. As per the company's 10-K filing, around 65% of Coupang's interest-bearing debt is in lease form with a mid-6% discount rate for lease payments. I added a company-specific default risk of 7%, leading to a cost of debt of 11%.

After considering the equity and interest-bearing debt ratio, I determined the cost of capital to be 10.11%

Terminal Value

Looking ahead 10 years, I anticipate that Coupang will continue to leverage its strong logistics infrastructure and WOW membership to maintain its competitive advantage. As a result, I predict that the company's return on invested capital will remain robust, at 15% in the final year of my projections. To determine the growth rate, I used the US 10-year Treasury yield (4%) as a proxy. Using these assumptions, I calculated the reinvestment rate to be 26.7%.

DCF Valuation Model

Coupang DCF valuation (Author calculations)

{kind=link}

Based on my DCF analysis, I estimated that the present value of Coupang's future cash flows is $17.9 billion. To calculate the intrinsic value, I added the company's $3.5 billion cash and cash equivalents and then subtracted its $2.4 billion in interest-bearing debt. This led me to a total intrinsic value of $19.2 billion for Coupang.

Coupang Intrinsic Value (Author calculation)

Given that Coupang has a total of 1,770,298,228 class A and class B shares outstanding, I calculated the intrinsic value per share to be $11.

Investment Risk

Government regulation : The current Korean government is advocating for self-regulation in the digital platform industry. Nevertheless, public concern is rising over the potential monopolistic and oligopolistic practices of platform providers. A 2012 regulation , which required hypermarkets to shut down their stores for two days every month, could potentially serve as a reference for regulating the platform industry.

In the event that the government changes its policy direction, there is a chance that Coupang may face headwinds. Therefore, it is vital for the company to closely monitor any changes in government regulations

Recession : Korea is one of the countries with a high household debt to GDP ratio, which was 108.5% as of September 2022 , primarily due to inflated housing prices. In the US and Japan, a high level of household debt has been known to cause a recession. If a similar scenario were to occur in Korea, it could have a negative impact on the growth rate of e-commerce in the country, which, in turn, could affect Coupang's revenue growth.

Conclusion

Coupang's impressive logistics infrastructure and a rapidly expanding WOW member base are undoubtedly its core competencies. Given these advantages, coupled with the company's revenue recognition model, I believe that Coupang will be able to achieve a 7% operating margin in 10 years.

Nevertheless, Coupang's logistics infrastructure also poses a challenge for its international expansion, as it may not be feasible to duplicate its successful formula in other countries. Furthermore, I anticipate that Coupang's competitors will continue to be competitive, hindering the company's market share growth beyond 30%.

Based on my DCF valuation, I have arrived at an estimated intrinsic value of $11 per share for Coupang. Given that the current stock price is slightly above this valuation, my recommendation would be to maintain a "hold" position for the time being.

For further details see:

Coupang: Strong Moat But Overpriced