NHNCF - Coupang: The Future Of Retail Thanks To AI

2023-08-09 10:24:59 ET

Summary

- Coupang, the South Korean e-commerce giant, has the potential for long-term growth due to positive demand dynamics and a defendable competitive position.

- The company's efficient logistic network and use of AI and machine learning set it apart from competitors in the Korean market.

- Coupang is on track to be profitable in FY23 and has addressed previous concerns about dilution, making it an attractive investment option.

Introduction

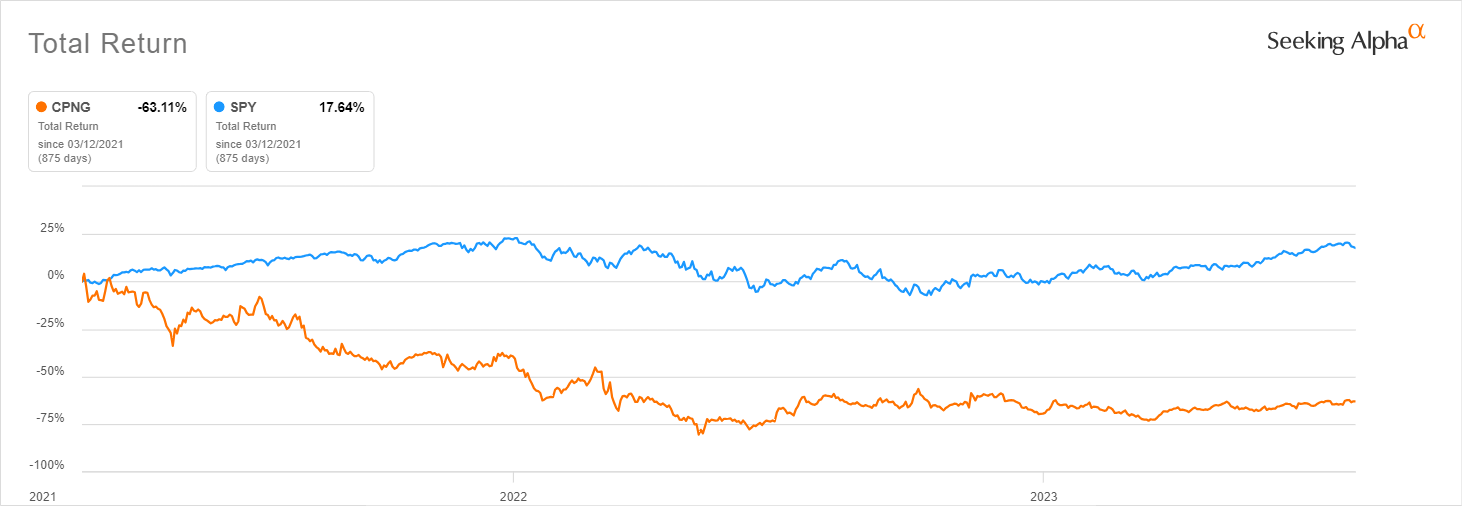

While I have followed South Korean e-commerce giant Coupang ( CPNG ) since its IPO in March 2021, I have been a long-time bear and advised against investment in CPNG several times in the past. I have lived in South Korea for the better part of the last decade and consider myself knowledgeable about the local market. I have used Coupang services for many years, and while I recognize its vast potential as a business, I have always had concerns about CPNG share structure and price. There was a huge hype surrounding CPNG at its IPO, with shares briefly shooting above $60 per share, giving the company a $109 billion valuation on its first trading day. Class A shares available for trading carry limited voting rights compared to the Class B shares (1:1 vs. 1:29). Class B shares, held by Coupang’s founder, Bom Kim, ensure his stable control of the company. Until 2022, CPNG remained a business in high cash-burn mode, using its inflated valuation to issue stock. Even though dilution was an excellent financing option from the company’s perspective, as an investor, it made me feel uneasy about purchasing CPNG shares. Despite the natural short-term fluctuations, I believe I got the story right, as the stock’s performance has been far from great. Nevertheless, narratives can change, which I think is the case with Coupang.

{kind=link}

My change of heart about the potential of investing in CPNG has been a long time coming. And with Coupang still capitalizing over $30 billion and sporting a forward P/E above 70, shares still do not appear cheap. Nonetheless, I finally came around, and I think investors should seriously consider starting to accumulate shares for the long haul. The future of Coupang undoubtedly looks bright.

Investment Thesis

If I had to summarize the reasons for investing in Coupang in a single sentence, I believe it could be appropriate to paraphrase the company’s investor relations choice. Korean people (and foreigners living in Korea!) can’t live without it any longer.

{kind=link}

But necessity alone doesn’t make Coupang a good investment. The attractiveness of Coupang’s business proposition is significantly enhanced by the following:

- Positive long-term demand dynamics, with a continuous shift in consumer preference towards e-commerce (secular growth).

- A defendable competitive position. Like Amazon ( AMZN ) in the US, CPNG is now deeply entrenched in the Korean market. Its efficient logistic network scale allows Coupang to promise same-day delivery (on most purchases) to its members. Over the years, Coupang has built over 100 fulfillment centers, covering over 47 million square feet and housing millions of products. The company estimates 70% of Koreans live within 7 miles of a logistics center (wide moat).

- The continuous use of AI and machine learning to improve the company processes sets the company apart from the competition. Coupang has long been using machine learning to increase i nbound efficiency , predicting order volume, and improve the algorithms on its main app. AI already runs Coupang’s fulfillment centers with minimal human involvement (IT leadership).

- Now that Coupang has scale, it finally shifted gears, focusing on productivity and profitability. Even if the company continues to invest and expand its top line, it has taken a more balanced approach, using the cash generated from operations to self-fund itself. The business has a clear path to profit, and it is pushing toward its 10% EBITDA long-term goal (improving margins)

Favorable long-term trends

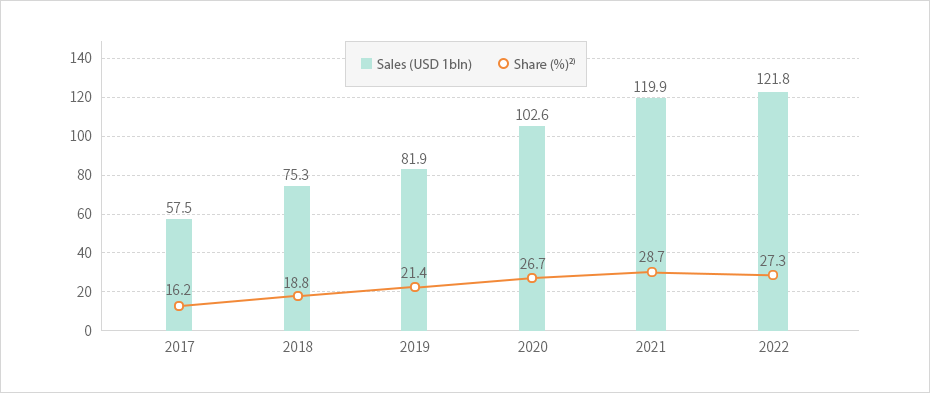

Koreans are tech-savvy customers, and even if screen usage time isn’t among the highest globally, Koreans are well-versed in using their devices for everything from payments to online shopping. Also fueled by the pandemic, South Korean e-commerce has experienced explosive growth. E-commerce sales expanded from $57.5 billion in 2017 to $121.8 billion in 2022, a 2.12x increase in just five years, representing a 16.2% CAGR. Despite moderately increasing overall market share from 16.2% in 2017 to 27.3% in 2022, online sales still represent just about 1/4 of the total retail market size of $446 billion. While other sources online may provide different data, these are official figures from InvestKorea (part of KOTRA, a government agency), so I believe they offer the best reliability.

{kind=link}

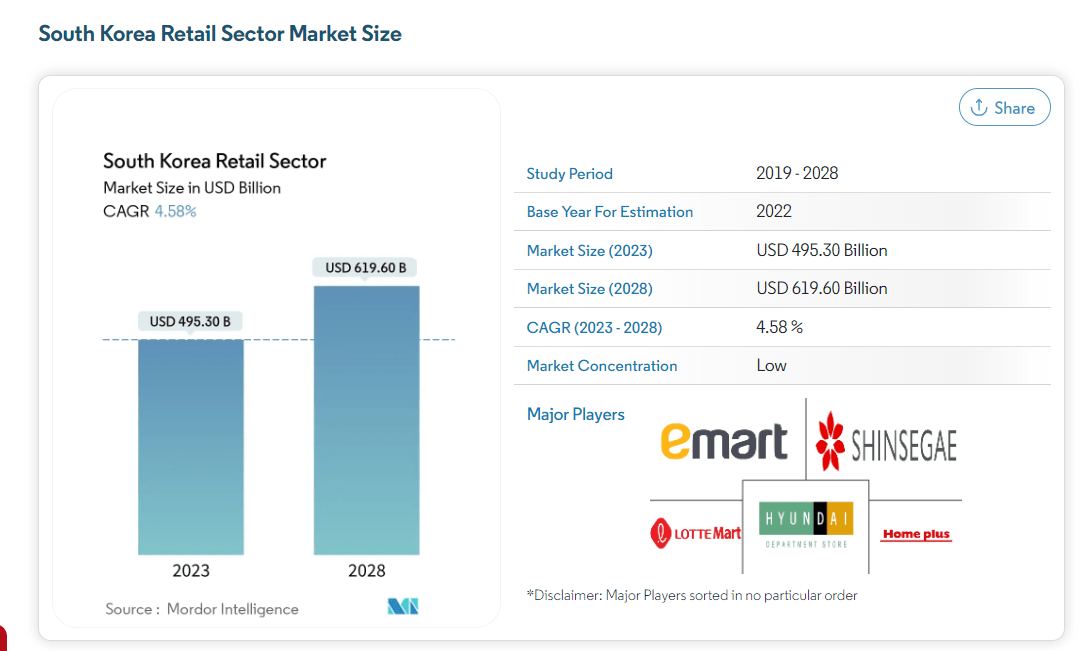

Regarding the 2023-2028 period, I rely on this Mordor Intelligence data as a starting point to project CPNG’s 2028 estimated market. The 11% YoY jump to $495 billion seems believable, considering the high level of inflation the country has experienced over the past 12 months, and I am OK with the subsequent 4.6% CAGR. So, Coupang’s TAM points at $620 billion in 2028.

{kind=link}

I estimate that, after a pause in 2022 due to the country’s post-COVID reopening, e-commerce will return to command an increasing share of the total retail sales and reach at least 30% by 2028. A new driving force shifting consumer preference toward online shopping from offline could be the public shock caused by the recent mass stabbings in Seoul. One of these stabbings happened at a department store, and local chains remain on high alert amid copycat crime threats .

Defendable competitive position

Coupang sales in 2022 totaled $20.6 billion, giving the company a 16.9% market share as a leading e-commerce platform in Korea. Coupang operates in Korea through its integrated app that offers:

- A traditional online marketplace (Coupang), with main competitors being Naver ( NHNCF ), Gmarket Global (Gmarket, Auction & G9, owned by the Shinsegae Group), and 11ST (30% owned by Amazon).

- F&B delivery (Coupang Fresh), with the strongest competitors in the segment being Shinsegae Group’s SSG.com, Market Kurly, and GS Fresh (GS Retail)

- Food Services delivery (Coupang Eats), here, mainly competing with BaeMin, owned by Delivery Hero ( DHERO ). DHERO, in turn, divested its ownership of No. 3 player Yogiyo in 2021 to GS Retail as a condition imposed by the Korean FTC related to the BaeMin acquisition.

- Entertainment (Coupang Play). The company competes here with both international Subscription-Video-on-Demand (SVoD) providers Netflix ( NFLX ) and Disney ( DIS ) with Disney+ as well as local Tving (CJ E&M and Naver JV) and Wavve ( SKM ).

The first critical point emerging from this analysis is that Coupang, through its WOW membership, offers the most comprehensive and enticing online shopping experience. There is no competitor with an equally broad offering, an end-to-end value chain ownership, so Coupang can achieve higher margins by creating more value for its members and taking advantage of cross-selling opportunities.

Despite the scale of its operations, Coupang still has a long growth runway. As highlighted during the most recent earnings call, the company has limited market share in a massive total retail sales TAM. Bom Kim mentioned in the 2Q23 call an expected $550 billion by 2026, which is about on pace with the earlier estimate of this article for $620 billion in 2028.

F&B accounts for over 35% of the retail market ( 2022 data ), but the online part is below this share, underscoring that e-commerce is still underpenetrated and Coupang Fresh has incredible potential. Competitors are nowhere near Coupang regarding fulfillment capabilities or offering width. Even if competitors have experienced robust top-line growth, they struggle to show progress in turning profits, despite starting similar pivoting efforts in 2022.

And Value For All

A 2021 plan to proceed with SSG IPO the following year has yet to come to fruition, and Kurly has similarly scrapped its 2023 IPO plans . Coupang’s vertically integrated end-to-end logistic network is unique, and its massive scale provides the company with critical advantages in delivery lead times and the sheer size of available SKUs over competitors.

Unsurprisingly, Coupang’s founder Bom Kim has his eyes on the prominent (and profitable) Korean incumbent retail players instead when talking about the next phase of growth and Coupang’s main competitive arena:

We’re still in the single-digit share of the overall market. The overwhelming majority of the retail market is offline, with high prices and limited selection. We’re excited about the opportunity to wow customers with a wider selection, lower prices, and exceptional service to continue to capture significant growth. (Bom Kim, 1Q23 earnings call)

Then again, Coupang has a unique selling proposition and distinct advantages over offline players. While initiatives such as Coupang Play may remain accessories with an internal goal only of breaking even while adding overall value to customers, I expect the company’s core e-commerce offering (Coupang, Fresh, and Eats) to maintain its trajectory and grow market share further. In particular, I am becoming more constructive on Eats. Despite the local market still being dominated by BaeMin, the company is progressing by leveraging its WOW membership base and offering cross-benefits.

In the regions where we’ve launched our Eats benefit, we’ve already seen an 80% increase in total WOW members participating in Eats and a 20% increase in average WOW member spend on Eats. (Bom Kim, 2Q23 earnings call)

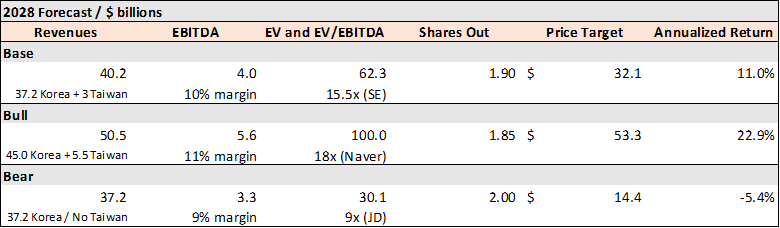

With asymmetric growth coming from the F&B e-commerce expansion, Coupang’s total turnover in Korea could increase to $45 billion by 2028, a 14% CAGR. Still, even at $45 billion, revenues would represent only 7.25% of the 2028 South Korea retail TAM. Within e-commerce, I see Coupang gaining at least a 20% share, possibly even 22% or above, mainly as Coupang Fresh continues to gain ground. The table below recaps my assumptions.

{kind=link}

These figures are achievable without adding any optionality from international expansion, which deserves some clarification.

International expansion flounders?

Another reason that kept me away from CPNG in the past was that, with the IPO, bulls claimed that Coupang could use the proceedings to expand into new markets successfully. But bulls were dreaming with their eyes open, thinking that Coupang could easily replicate its successful domestic model everywhere outside Korea.

The overseas markets targeted in 2021, Japan and Taiwan, made sense from a theoretical standpoint. Coupang core strength is in operating an end-to-end logistic model and, to do so effectively and efficiently, developed markets with a mature infrastructure are preferable vs. developing countries. Still, this is not the only thing to consider. An expansion in Japan was bound to face multiple hurdles, from cultural to political ones. The potential market is enormous, with a population of over 100 million. Yet, the country is also almost 4x the size of Korea, and Coupang needed to build another logistic network from scratch. Fast forward two years and CPNG decided to pull the plug .

Conversely, I believe the company’s new focus on Taiwan goes in the right direction. The country is relatively small (1/3 of Korea) but has an even higher population density than Korea. Logistic investments are relatively affordable, with fewer cultural hurdles to overcome. The main problem is that deep-pocketed competitors Shopee ( SE ) Taobao ( BABA ), and Amazon are already contending the market. Yet, e-commerce market penetration is still way lower than in Korea at about 10% of total retail sales, suggesting potential for a long future runway.

If successful, CPNG could carve out a 9-13% position within the Taiwanese e-commerce space, generating $3-$5.5 billion in sales over the medium term. A 10% market share would imply that Coupang is a top-5 platform in the country but not the likely leader. I do not see CPNG accepting a marginal – and unprofitable – side role over the long term, which means the likely downside scenario here is a withdrawal from the market.

{kind=link}

The company has also been hiring for months in Singapore ahead of a potential launch that has yet to happen.

After clarifying international markets’ expansion, it is time to focus on how Coupang can generate all this top line and why the company will increasingly command positive operating margins when its competitors struggle to keep up with mounting losses and failing IPOs.

At the core of Coupang’s advantage – AI

Coupang has long been dubbed “the Amazon of Korea” as both companies are large e-commerce operators. Yet, substantial differences exist, first and foremost, because most of Amazon’s profits come from the AWS division. But business models aside, Coupang shares with Amazon an incredible focus on efficiency that has led CPNG to invest hundreds of millions and incorporate the latest technologies in its logistic processes, redesigned to achieve maximum productivity.

At Coupang’s fulfillment center in Daegu, Asia’s largest , cutting-edge automation technology based on artificial intelligence ((AI)) on-site is pervasive. The 3.5 million square feet, 12-story building features an army of robots, from heavy hauler merchandise movers to sorters and unmanned forklifts, that navigate the entire perimeter using QR codes on the floor and pillars. AI automation manages all processes at the center, from collecting ordered items to packaging and classifying them before delivery.

The result? It potentially takes 10 minutes for a placed order to become a packaged item loaded onto a delivery vehicle. You can check the videos shot by Bloomberg TV at the site [ here for 3min version ] and [ here for the 6min version ] on YouTube.

{kind=link}

Coupang also organizes shelves in its centers in a seemingly puzzling way, mixing different types of products. This combination, called the Random Stow method, is the same way Amazon sets up its warehouses for maximum efficiency. These random products are placed together because of technology: an AI solution that predicts sales rate, sales period, and the product groups likely to be ordered together. By analyzing big data, such an arrangement improves efficiency.

Anyone can buy a truck, anyone can buy a fulfillment center, but not everyone can be Coupang – (William Wang, Head of FC Systems).

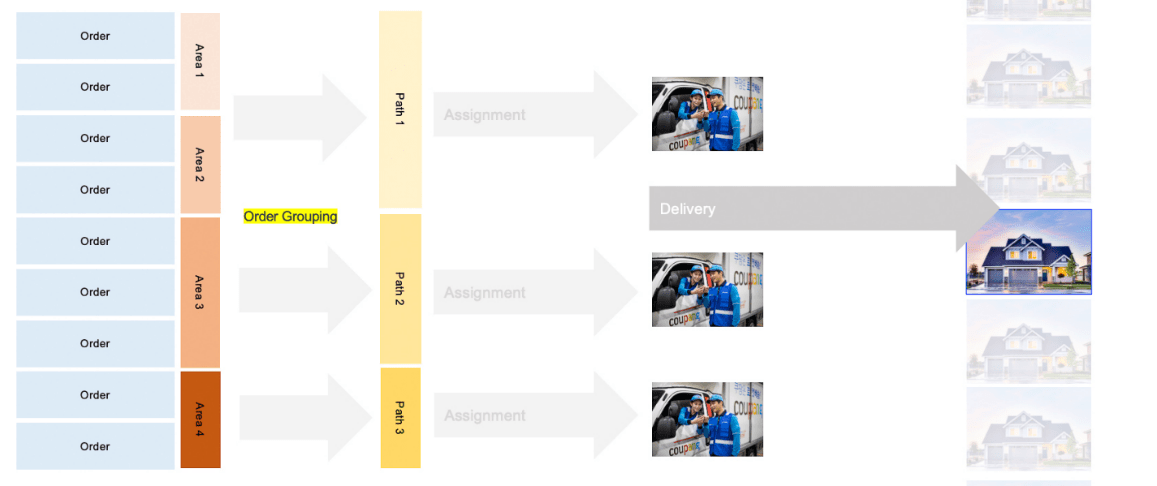

Mastering data science is the critical piece of the puzzle that sets Coupang apart from competitors like SSG.com. When I order from Coupang, I know my products will arrive the next day. When I try to shop on SSG, most of the time, some products I’d want to buy are unavailable at my location because they are out of stock at the specific fulfillment center tied to my house. Unavailability is , instead, a rare occasion with Coupang. AI considers multiple factors and then efficiently proceeds with order grouping, but it doesn’t end there. AI also estimates delivery times and determines the order of delivery. It automatically selects the best delivery routes, which staff to send, and to which locations.

{kind=link}

Diagram of Coupang’s shipping solution

The company also uses AI to apply dynamic pricing on its app, which is a massive advantage over offline competitors. AI is pervasive in Coupang’s business, and the company takes advantage of it in every possible aspect. At the same time, the company has taken “a quiet approach” toward AI, like Apple ( AAPL ). Even if the company thoroughly employs AI to drive the future of retail, it does not like to mention it in its prepared remarks. When asked (the same question twice in the last two calls) this is what Bom Kim had to say (emphasis added):

AI has been a powerful technology that we’ve deployed across virtually every facet of our business from Rocket-related operations to search to ads, customer service, and supply chain management, just to name a few.

I view in a very positive way that Coupang refrains from launching bold, unsubstantiated claims to appease analysts and fascinate speculators. While being at the forefront of AI implementation, Coupang remains focused on execution and the creation of long-term value.

The path to profitability – Coupang’s Valuation

The sheer amount of progress made during the last year is impressive. Coupang is now firmly on track to be profitable in FY23, with $950 billion in adjusted EBITDA generated over the trailing twelve months. Adjusted EBITDA for the core product commerce segment came at 7.2% in 2Q23, and the consolidated adjusted EBITDA margin was 5.1%. The company also achieved profitability on a quarterly GAAP EPS basis beating consensus by $0.03 ($0.08 vs. $0.05).

The improvements were pretty much everywhere across the board, with gross margin expansion (+320 bps) and OG&A expenses down (-66 bps), which prompted management to re-affirm that the goal of 10% adjusted EBITDA is within reach (at least, initially, for the product commerce segment). The company also generated $2 billion in operating cash flow and $1.1 billion in free cash flow on a trailing 12-month basis, which is huge. Most importantly, FCF is now converging toward adj. EBITDA levels.

Seeking Alpha

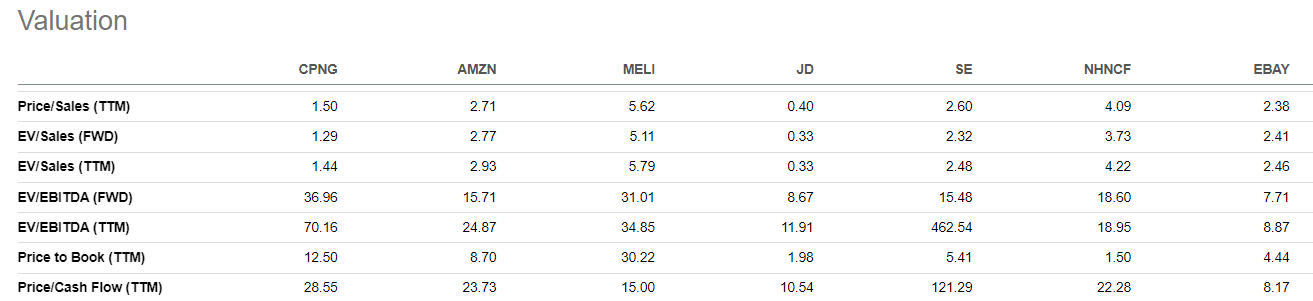

Considering these improvements in the financial metrics, investors finally have the chance to evaluate CPNG on realistic EBITDA and Free Cash Flow future targets. Evaluating Coupang from an EV/EBITDA standpoint is not easy. Peer valuations in this space diverge considerably, as businesses operating in the e-commerce space are never perfectly overlapping. Amazon trades at almost 25x EV/EBITDA, yet the valuation could be wildly different without AWS. I pulled data from several peers, and valuations can go from nearly 31x fwd EV/EBITDA for MercadoLibre ( MELI ) to as low as 8x for eBay ( EBAY ).

{kind=link}

While I think the peers’ average of 16x (fwd basis) could be somewhat appropriate, it is also evident that growth expectations play a significant role in determining the multiple. Coupang in 2028 won’t likely trade even close to 30x anymore. Yet, I wouldn’t rule out CPNG growing revenues at 5-10% CAGR even after 2030, with margins and profits increasing at an even faster clip. As Coupang expands into contingent segments, international markets and consumers continue to shift towards e-commerce, the possibilities are real. In my base case, I assign a 15.5x multiple to CPNG, in line with Sea Limited ((SE)), which by assuming FCF to be roughly in line with EBITDA, translates into a 6.5% FCF yield for Coupang. For my upside (bull) scenario, I aligned the multiple to the 18x of Naver and the 9x of JD.com ( JD ) for the bearish one.

{kind=link}

Based on my forecasts and a starting price of $19 (as of August 9 following the Q2 earnings call), I expect investment in CPNG to generate a 5-year annualized return of about 11%. The upside potential is quite huge, and see, under my most bullish hypothesis, Coupang’s enterprise value to reach $100 billion in 2028, powered up by an 11% EBITDA margin and 18x EV/EBITDA multiple on over $50 billion of revenues. The downside scenario sees CPNG trading at just 9x EV/EBITDA multiple, withdrawing from Taiwan after an unsuccessful forage in the market, and only modest margin expansion toward 9%, below the management’s target. While the 11% return may not appear enticing enough to some investors, I am prone to assign a BUY rating and suggest share accumulation, as I expect CPNG to outperform the broad market over the next five years. Market volatility, however, could provide better entry points over the following months.

Dilution problem solved

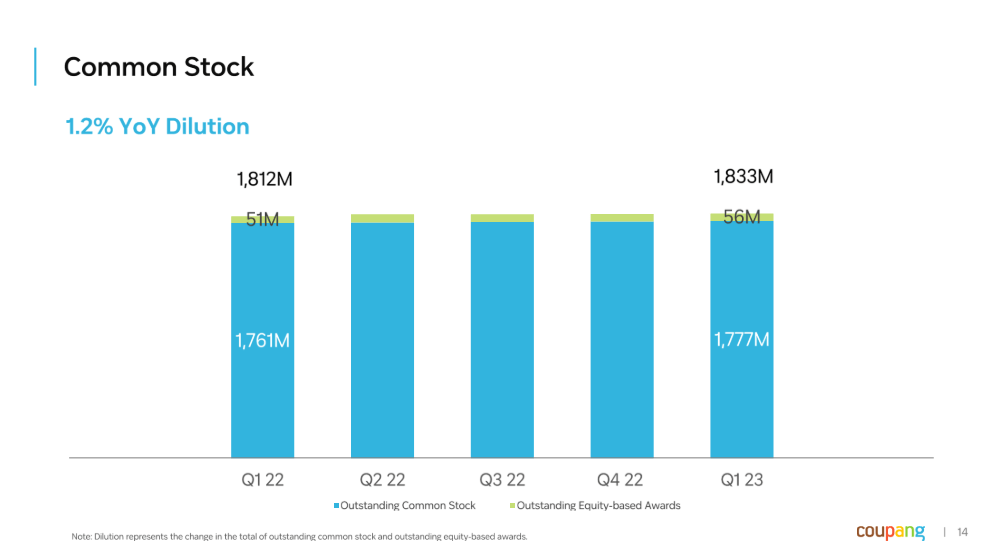

Another concern that I had with Coupang in the past was dilution. Common stock ballooned 24% between 2021 and 2022, and CPNG common shares increased from 1.42 billion to 1.76 billion. The problem was not related to equity-based awards (which are disclosed and therefore quantifiable) but rather the potential use of an inflated equity valuation to finance bold growth projects with uncertain ROI.

However, the picture has radically turned around. Dilution rate has decreased considerably to just a 1.2% YoY change. With the company focusing on profitable growth and margin expansion, the earnings multiple has the potential to come down quickly. I forecasted an average dilution between 1% and 2% for my valuation model vs. the current weighted outstanding total.

{kind=link}

Risks to the thesis

Although I like the idea of accumulating CPNG shares here, significant risks persist in this space.

First, the valuation I assigned to Coupang is not cheap and somewhat foresees better-than-average growth throughout the forecast period and beyond that. While I have little doubt that CPNG can eventually surpass the $50 billion sales mark, my forecast for 2028 expects market share gain and an overall expansion of the retail TAM in South Korea and other Asian markets.

A long and severe recessionary period would inevitably affect the presented valuation. In times of hardship, customers intensify bargain hunting to higher levels, and in turn, it could become difficult for Coupang to achieve such stated targets within 2028.

Offline and online local competitors such as Shinsegae, Lotte, and GS Retail are large and deep-pocketed, backed by the country’s largest chaebols (conglomerates) and the families of the post-war South Korean elites. If threatened, they won’t go down without a fight. As said, my forecast assumes that Coupang will “only” command about 7.3% of the total retail sales for 2028 in Korea, obviously leaving plenty of space for the competition. Nevertheless, from a foreigner’s perspective, I find the current retail landscape in South Korea lax, with extensive price gouging by retailers. I commonly see packaged products with very long-dated expirations (e.g., sauces, baked goods) at 3x the price I see the same products in Europe. I can’t determine whether such a landscape can last indefinitely or a more aggressive competition will kick in soon, eroding every player’s margins. On a more positive note, Coupang already seems to offer better-than-average value on a wide range of products.

Besides incumbent players, there is always a moderate risk that deep-pocketed foreign competitors could enter the market. As stated, Amazon operates in the country only through its 30% minority partnership in SK Telecom’s 11ST platform. Though improbable, bold moves by AMZN cannot be completely ruled out, as well as more aggressive competitive stances by Netflix or BaeMin to eat market share away from CPNG.

Conclusion

Following the Q2 earnings release on August 8, Coupang shares have shot up and are now changing hands at about $19 per share. Despite the gain, I see CPNG shares still offering a good entry point for long-term investors looking to gain exposure to a wide-moat e-commerce player poised to continue revolutionizing the retail landscape of South Korea through the use of AI and data science.

Now that efficient scale has been reached, the AI-powered end-to-end logistic network of Coupang is showing its full force in the domestic market, with CPNG potentially set to dominate the F&B delivery market (Coupang Fresh) by the end of the decade. While more skeptical about developing offerings (Eats and Play), I recognize that these services add significant value to the general Coupang customer experience when bundled within the WOW membership. With scenario analysis, I finally tried to weigh the probabilities of the different cases I have illustrated in my valuation paragraph, which resulted in a final risk-adjusted potential rate of return (ROR) of 12%

{kind=link}

I recommend slowly accumulating CPNG as long as shares trade below $20.

Editor’s Note : This article was submitted as part of Seeking Alpha’s Best AI Ideas investment competition , which runs through August 15. With cash prizes, this competition -- open to all contributors -- is one you don’t want to miss. If you are interested in becoming a contributor and taking part in the competition, click here to find out more and submit your article today!

For further details see:

Coupang: The Future Of Retail, Thanks To AI