CPNG - Coupang: The Power Of Operating Leverage

2023-03-30 05:04:56 ET

Summary

- Coupang is down nearly 70% since going public in 2021.

- The company's heavy emphasis on profitability should reap great rewards in the long run.

- The latest earnings continued to demonstrate strong operating leverage with the bottom line improving substantially.

- The current valuation remains discounted compared to peers.

- I rate the company as a buy.

Investment Thesis

Coupang ( CPNG ) is up over 40% since my last coverage in June , but still down nearly 70% since its IPO in early 2021. I remain convicted that the company presents one of the more compelling buying opportunities in the market. Despite facing tough macro headwinds, the company continued to execute and the latest earnings showed substantial improvement in its bottom line. The current valuation is also very attractive with multiples below most e-commerce peers, not to mention the opportunity for margin expansion that could further compress the multiple. I believe the company still has meaningful upside potential and I rate it as a buy.

Relentless Focus On Profitability

I discussed a lot about Coupang's market opportunities and offerings in the last article. This time, I want to talk a bit more about profitability and operating leverage, as I believe it is one of the company's greatest strengths that should be hugely accretive in the long run.

Most tech companies that went public in the past few years solely focus on top-line growth, with little emphasis on the bottom line. Some even adopt a growth-at-all-cost strategy and totally ignore profitability. While revenue growth is certainly important for companies at early stages, the improvement in profitability is also critical as it demonstrates how much operating leverage the company has. There is no point in running a business if it has to spend $1 just to make $1. After all, the ability to generate an income is what matters the most to a company. Unlike other newer companies, Coupang has been focusing on profitability since day one. It does spend money but everything it does is calculated, disciplined, and focused on operating leverage.

For example, the company recognized the importance of logistics and supply chain therefore they took it all in-house. They have been building out their own infrastructure over the years and now have one of the largest infrastructure footprints in Korea with 47 million square feet. This is extremely costly initially, but the benefits are increasingly evident as the company continues to scale rapidly. They now control the whole delivery experience which gives them much better pricing power and they are also able to keep logistics costs down with no impact from third-party companies. It is also investing in other areas such as warehouse automation , which allows the company to further reduce headcount expenses.

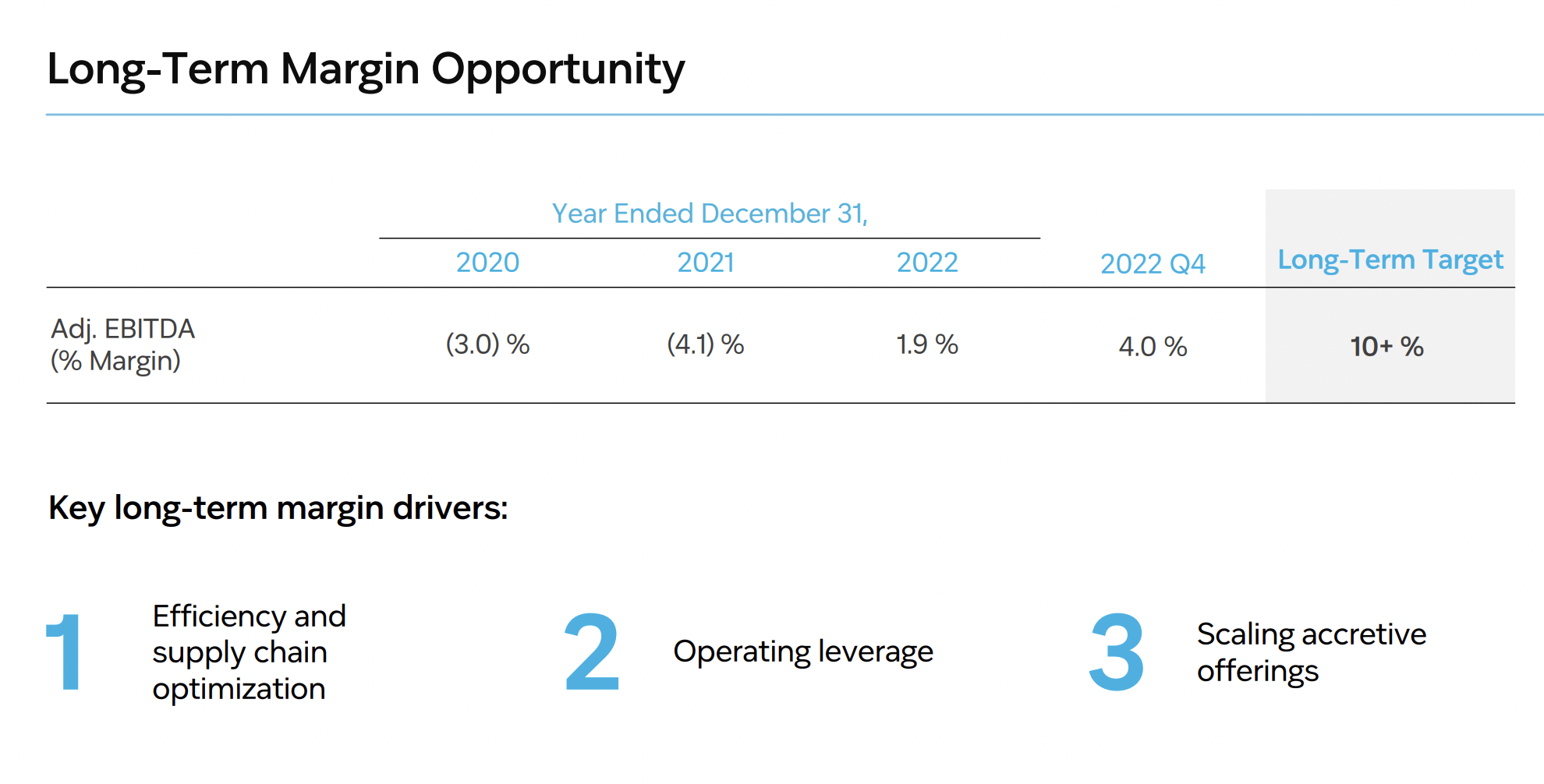

Thanks to these efforts, the company's profitability has been improving rapidly, with the gross margin increasing from 5% in FY18 to 22% in FY22. In the latest quarter, they also raised their long-term guidance for adjusted EBITDA margins to 10%+. I believe the company's outstanding management and relentless focus on profitability are why it will succeed in the long run.

{kind=link}

Financials

Coupang reported its fourth-quarter earnings last month and the results are impressive, especially the bottom line which improved significantly once again. The company reported revenue of $5.3 billion, up 5% YoY (year over year) compared to $5.08 billion. Growth rates appear to be low but this is mainly due to the won weakening against the dollar. On a constant currency basis, revenue growth was actually much higher at 21%. The number of active customers edged up 1% YoY from 17.9 million to 18.1 million. The average revenue per customer grew 4% YoY from $283 to $294 (the growth was 19% on a constant currency basis). Its WOW membership ended the year with 11 million paid members, up 20% YoY.

The top line was a bit underwhelming but the bottom line was definitely the highlight with substantial improvement. Thanks to cost optimization through investments in technologies, infrastructure, supply chain, and automation, costs of sales actually went down 5.2% YoY from $4.27 billion to $4.05 billion. This resulted in gross profit jumping 59% YoY from $805.6 million to $1.28 billion. The gross profit margin was 24% compared to 15.9%, up 810 basis points YoY. Spending also moderated as OG&A (operating, general, and administrative) expenses remained flat at roughly $1.2 billion. This resulted in the adjusted EBITDA flipping from negative $(285.1) million to positive $211 million, or 4% of revenue. It also went from a net loss of $(405) million to a net income of $102.1 million. The EPS was $0.06 compared to $(0.23).

Compelling Valuation

Despite being up 40% since June last year, Coupang's valuation remains compelling in my opinion. According to Seeking Alpha's consensus , the company is estimated to generate $24.1 billion in revenue for FY23. Using its long-term adjusted EBITDA margin guidance of 10%+, this translates to a fwd EV/EBITDA ratio of just 10.7x, which is meaningfully below e-commerce peers. For context, Sea Ltd ( SE ) and MercadoLibre ( MELI ) are trading at a fwd EV/EBITDA ratio of 28.8x and 34.2x respectively, as shown in the chart below. This represents a significant premium of 62.8% and 68.7% compared to Coupang. I believe the discount is unjustified as Coupang continues to demonstrate strong bottom-line growth. Revenue growth was weaker, but this is only because of the headwind from unfavorable foreign exchange rates, which should moderate over time.

Investors Takeaway

I believe Coupang has strong fundamentals and is well-positioned for long-term success. The company's emphasis on operating leverage is now paying off as profitability continues to improve rapidly in the past few quarters. Despite soft revenue growth due to currency headwinds, gross profit still increased 59% YoY in the latest quarter, while the gross profit margin also expanded substantially. As currency headwinds ease, I expect growth to further accelerate. The current valuation also remains heavily discounted compared to peers, despite the recent progress shown in the bottom line. I believe the company will see meaningful multiples expansion as the market starts to acknowledge its ongoing improvement in profitability, which should present decent upside potential. Therefore, I rate Coupang as a buy.

For further details see:

Coupang: The Power Of Operating Leverage