CPNG - Coupang: Value When Farfetch Is Unlocked

2024-01-16 10:23:19 ET

Summary

- Coupang's acquisition of Farfetch has faced criticism, with doubts about the suitability of Farfetch's luxury marketplace model.

- In an optimistic scenario, if Coupang can turn Farfetch profitable, the value of Farfetch could be $2.7 billion.

- My Coupang's revised market share projection is 35%, taking into account competition and the number of Korean households.

- If Coupang unlocks the value of Farfetch, Coupang's intrinsic value is $15.4 per share.

Investment Thesis

Coupang (CPNG) announced on December 18, 2023 , that it would acquire Farfetch Limited (FTCHF) and give $500 million capital with Greenoaks Capital to Farfetch. Farfetch reported that It would not have been able to continue as a going concern. Coupang and Farfetch both expressed their optimistic outlook for the acquisition.

However, some critics of Coupang may discover that this acquisition would be a loser because the online marketplace business model is unsuitable for luxury brands. In addition, some suspect that the acquisition was made due to pressure from financial investors who wanted to exit from the investment through revenue increase.

Since the only available information is Coupang's announcement, I cannot judge whose view is more persuasive. Accordingly, I need to conduct a valuation of Coupang, considering both optimistic and pessimistic scenarios.

In addition, I revisited my previous valuation of Coupang and revised my projection based on recent information.

Two Scenarios of Coupang X Farfetch

Overview of Farfetch

Based on Farfetch's second quarter 2023 results , I deduced two significant issues contributing to negative operating income.

Firstly, Farfetch is selling 'non-luxury goods.' Farfetch's revenue streams come from transaction fees from the third-party seller in their marketplace (Digital Platform Services third-party revenue), selling its products in their marketplace (Digital Platform Services first-party revenue), fulfillment service fee (Digital Platform Fulfillment Revenue), on and offline sales of their product (Brand Platform Revenue and In-Store Revenue).

Because fulfillment revenue is a pass-through cost with no economic benefit, most of Farfetch's revenue comes from Digital platform service revenue. Within Digital Platform revenue, selling their products shows a meager gross profit margin compared to the gross profit margin of a typical luxury business. From a productivity perspective, Farfetch's products (i.e., New Guards) are 'wannabe' luxury rather than 'true' luxury.

Farfetch's filling, the author

Secondly, Farfetch has not enjoyed the economies of scale since SG&A cost increased at a similar pace to revenue growth. The primary reason for this increase is the increase in headcounts resulting from the continuous acquisition. Coupang should find a way to increase efficiency to benefit from revenue growth.

Farfetch Revenue, SG&A, and SG&A/Revenue (Farfetch's filling, the author)

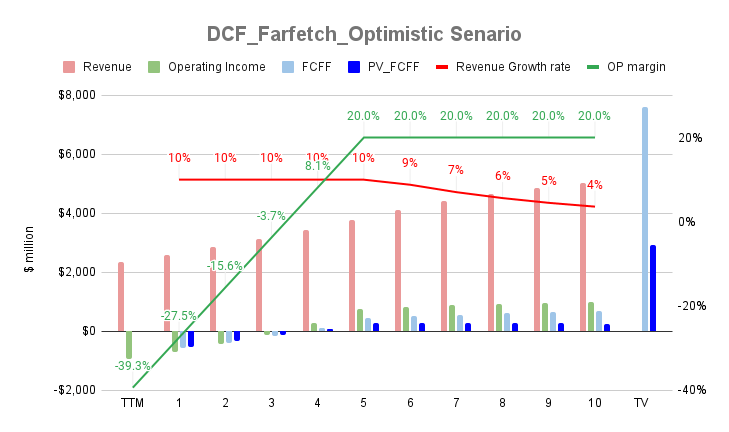

Optimistic Scenario

Coupang's announcement shows that the company would create value by combining Coupang's ability in operating and logistics with Farfetch's business. Based on this statement, it is probable that Coupang will reduce the segment of selling and producing Farfetch's products to focus on what Coupang is good at (i.e., e-commerce).

In this case, Farfetch's revenue might decrease as the total GMV of Farfetch's product is recognized as revenue. However, Coupang can offset this revenue decrease by creating a revenue stream in the Korean market by combining Coupang's logistic system and Farfetch's brand-sourcing ability.

If this optimistic scenario materializes, it's probable that Farfetch's revenue will increase by 10% for five years, considering Bain & Company for the luxury market , then linearly decrease to the economy's growth rate. Farfetch's operating margin could reach 20%, considering companies in the marketplace sector like Etsy (ETSY) and eBay (EBAY). In this scenario, my simplistic estimation of Farfetch's value, as illustrated in the chart below, is $2.7 billion (Present value of FCFF ($3.75 bn) less interest-bearing debt ($1.05 bn))

{kind=link}

Pessimistic Scenario

Coupang would fail to turn Farfetch into a profitable company in a pessimistic scenario. If so, the value of Farfetch could be zero because the business has no positive free cash flow stream. And Coupang would lose 80% of the $500 million that Coupang spent on the acquisition.

Coupang's Core Business

Total Addressable Market

In my March 2023 valuation , I viewed that Coupang would not show any remarkable performance outside of Korea because Coupang could not replicate its strength in the Korean market in other countries. Even if Coupang tried to venture into Taiwan , the primary business model is cross-border e-commerce from Korea to Taiwan . I wonder whether Coupang will create meaningful revenue in Taiwan in the near future. Thus, I maintain my previous view regarding Coupang's total addressable market.

Based on Statistics Korea's data on the retail and online commerce market size, the U.S. 10-year Treasury Rate (around 4%), and my projection of the e-commerce penetration rate, I estimated that the Korean e-commerce market size would be $363 billion.

the author

Revenue Growth

According to Statistics Korea's data , the GMV of online shopping in the 3rd quarter of 2023 was $43 billion (equivalent to KRW 56.9 trillion). Considering Coupang's revenue in the 3rd quarter of 2023 ($6.2 billion) and revenue to GMV ratio of Coupang (60% according to my previous estimate), I estimate that Coupang's market share in Korea will increase to 24% in 2023.

Coupang's progress is impressive, so I revised my projection for Coupang's market share in 10 years from 30% to 35%. The reasons why I limit my projection to 35% are as follows.

Firstly, Coupang was not the only company that increased its market share. Naver (KRX: 035420), the biggest competitor in the Korean e-commerce business, also shows a similar extent of market share increase (22% calculated based on Naver's GMV in Q3 2023).

Secondly, there is little room for the growth of active customers. Coupang reported that the number of active customers in the 3rd quarter of 2023 reached 20.4 million. Considering the number of Korean households, which was 23.9 million in December 2023 , most Koreans are using Coupang to purchase goods for their households.

Thirdly, Chinese players like AliExpress and Temu are aggressively penetrating the Korean e-commerce market.

Based on my estimate of the size of the total addressable market, market share, and revenue per GMV, my projection for Coupang's revenue in 10 years will reach $65.4 billion (revenue = market size (363bn) x market share (30%) x revenue per GMV (60%)).

Operating Margin

During the earnings call , Coupang continuously expressed that " we are confident in our ability to achieve our entitlement adjusted EBITDA margins of over 10%. " In line with my previous view , Coupang's long-term guidance is attainable. Coupang's long-term guidance is achievable. Thus, my operating margin projection remained unchanged at 7% in ten years, considering depreciation and amortization.

Tax Rate, Reinvestment Rate, and Discount Rate

Regarding tax rate, I used a U.S. marginal tax rate of 27.5% and considered Coupang's net operating loss carry forward of $3,320 million based on Coupang's 2022 10-K filing .

Regarding the reinvestment rate, I applied a sales-to-capital ratio of 5, considering Coupang's coverage of Rocket delivery in Korea and the recent sales-to-capital ratio.

I applied 10% for the discount rate, considering the U.S. 10-year Treasury Rate and equity risk premium.

Intrinsic Value

Based on my projections and assumptions, the intrinsic value of Coupang's core business is $24.8 billion (equivalent to $13.9 of value per share), which is equivalent to Coupang's overall intrinsic value in the pessimistic scenario of Farfetch.

In the optimistic scenario (Farfetch is worth $2.7 billion), Coupang's overall intrinsic value is $27.5 billion (equivalent to $15.4 of value per share).

(in thousands, except Intrinsic value per share)

| TTM |

| 1 |

| 2 |

| 3 |

| 4 |

| 5 |

| 6 |

| 7 |

| 8 |

| 9 |

| 10 |

| TV |

| Revenue |

| $23,149 |

| $26,968 |

| $31,418 |

| $36,602 |

| $42,641 |

| $49,677 |

| $56,632 |

| $62,975 |

| $68,617 |

| $73,536 |

| $77,753 |

| Revenue growth |

| 17% |

| 17% |

| 17% |

| 17% |

| 17% |

| 14% |

| 11% |

| 9% |

| 7% |

| 6% |

| 4.0% |

| Operating income |

| $425 |

| $774 |

| $1,226 |

| $1,806 |

| $2,545 |

| $3,477 |

| $3,964 |

| $4,408 |

| $4,803 |

| $5,148 |

| $5,443 |

| OP margin |

| 1.8% |

| 2.9% |

| 3.9% |

| 4.9% |

| 6.0% |

| 7.0% |

| 7.0% |

| 7.0% |

| 7.0% |

| 7.0% |

| 7.0% |

| NOL |

| $3,320 |

| $2,546 |

| $1,320 |

| After-tax income |

| $774 |

| $1,226 |

| $1,310 |

| $1,845 |

| $2,521 |

| $2,874 |

| $3,196 |

| $3,482 |

| $3,732 |

| $3,946 |

| $4,104 |

| Reinvestment |

| $764 |

| $890 |

| $1,037 |

| $1,208 |

| $1,407 |

| $1,391 |

| $1,269 |

| $1,129 |

| $984 |

| $843 |

| FCFF |

| $10 |

| $336 |

| $273 |

| $637 |

| $1,114 |

| $1,483 |

| $1,927 |

| $2,354 |

| $2,748 |

| $3,103 |

| $41,038 |

| PV_FCFF |

| $9 |

| $278 |

| $205 |

| $435 |

| $692 |

| $837 |

| $989 |

| $1,098 |

| $1,166 |

| $1,196 |

| $15,822 |

| PV Total |

| $22,726 |

| - Interest-bearing debt |

| -$2,788 |

| + Cash and Cash equivalent |

| $5,261 |

| - Cash out for acquisition |

| -$400 |

| Intrinsic value (except Farfetch) |

| $24,799 |

| Farfetch's intrinsic value (optimistic scenario) |

| $2,700 |

| Total intrinsic value |

| $27,499 |

| Intrinsic value per share |

| $15.38 |

Risk

Last December, the Korean Fair Trade Commission announced its decision to introduce new regulations targeting market-dominant platform operators . As Coupang is one of the companies expected to be targeted by the regulations, Coupang's bargaining power against sellers could be weaker if the regulations take effect. If so, my projection on Coupang's operating margin may not be achievable.

Conclusion

Coupang's acquisition of Farfetch has generated both optimism and skepticism. In the optimistic scenario, Coupang aims to leverage its strengths to enhance Farfetch's revenue streams, particularly in the Korean luxury goods market. If successful, I estimated that Farfetch's value is $2.7 billion. However, in a pessimistic scenario, if Coupang fails to turn Farfetch profitable, its value could drop to zero.

In terms of Coupang's core business, I revised my projection of Coupang's potential market share in the Korean e-commerce business to 35%. Based on my estimation, the intrinsic value of Coupang's core business is $24.8 billion, equivalent to $13.9 per share. In the optimistic scenario, including Farfetch, Coupang's overall intrinsic value could reach $27.5 billion, or $15.4 per share.

For further details see:

Coupang: Value When Farfetch Is Unlocked