UDMY - Coursera: Good Growth Prospects But Loss Making And High Valuation

2023-04-18 14:15:05 ET

Summary

- Revenue should benefit from growing demand for entry-level professional certifications, higher attention towards reskilling and upskilling, and new branded micro-credential course additions.

- Margins are expected to remain under pressure in the coming year due to incremental costs associated with a large contract renewal.

- The stock is trading at a premium to Udemy.

Investment Thesis

Coursera Inc. ( COUR ) is expected to benefit from the increasing demand for entry-level professional certifications and the growing need for reskilling and upskilling, as low-skilled jobs are constantly being overtaken by artificial intelligence. The transition from traditional higher education systems to affordable online modes of learning and the company’s efforts to expand its course catalog by adding new programs and branded micro-credential courses are also expected to contribute to revenue growth.

However, the company is yet to turn a profit, and margins are expected to remain under pressure in the near term due to incremental costs from a contract renewal with the company’s largest industry partner. The company is also trading at a premium to its peer Udemy ( UDMY ) on EV/Sales basis despite Udemy's higher expected revenue growth in the near term. Hence, I have a neutral rating on COUR stock.

Revenue Outlook

During the pandemic, there was a significant increase in demand for online education and training worldwide, which benefited Coursera's revenue growth, and its revenue grew by 41.49% Y/Y in FY21 and 59.16% Y/Y growth in FY20. However, in the fourth quarter of 2022, the revenue growth slowed to 23.68% Y/Y as the enterprise segment growth slowed due to tight budget spending in response to a weakening economy. Additionally, the growth was impacted by lower-than-anticipated enrollments in the degree segment.

{kind=link}

COUR’s Revenue (Company Data, GS Analytics Research)

Looking ahead, I believe that Coursera should be able to continue its revenue growth trajectory in the coming years. The company is well-positioned to benefit from the increasing demand for affordable online education, particularly from prestigious institutions, as well as the need for reskilling and upskilling to ensure career progression as low-skilled jobs are increasingly being replaced by artificial intelligence.

During the pandemic, it became clear that remote learning could be successful on a global scale. However, the traditional higher education system has been slower to adapt to this mode of learning. Coursera's degree segment offers higher education institutions an ideal platform to expand their global reach and make education more accessible to learners regardless of their location or financial means. As a result, the company has been partnering with a growing number of higher education institutions and introducing new master's programs on its platform. In 2022, Coursera added 14 new degree programs, including a liberal studies degree from Georgetown University and a master's of science in software engineering from West Virginia University. These affordable degree programs should attract more learners in the second half of 2023 as they seek to earn their master's degrees online and advance their careers.

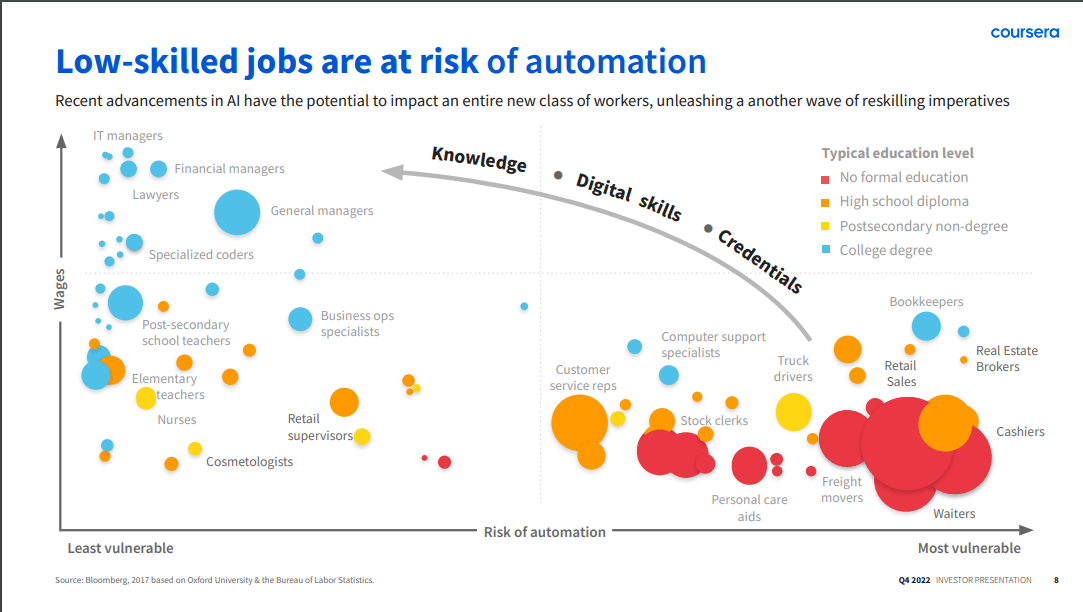

Furthermore, as we move toward greater digitization, work processes are becoming more automated, and low-skilled jobs are being replaced by AI. This is driving increased interest in reskilling and upskilling among employees to ensure their career paths are secure. Coursera is well-positioned to benefit from this trend as it offers a wide range of courses and programs to help individuals acquire new skills and advance their careers.

{kind=link}

Job category and risk of automation (Coursera Q4’22 earning call presentation slide)

I believe we should see a significant demand for upskilling as artificial intelligence increasingly replaces routine actively. It might take some time for traditional universities to upgrade their curriculum to address these changes and online education companies like Coursera are much better placed to quickly fill this gap with relevant course offerings.

Furthermore, remote work has enabled employers to hire talent from anywhere, and job-seekers want to ensure they have the necessary skills to take advantage of these opportunities. This is driving demand for skill enhancement courses, and I expect these trends to continue driving demand for Coursera's B2B and B2C channels, offsetting some of the softness in the enterprise segment and supporting revenue growth in the coming years.

In addition, Coursera is continuously expanding its branded micro-credential course offerings. Recently, the company received American Council on Education (ACE) credit recommendations for two entry-level professional certificates, bringing the total number of recognized certificates to fourteen. Learners can earn academic credit toward a degree program at a lower cost, and universities are considering offering credit for these industry micro-credentials to complement traditional curricula with job-relevant skills. These branded micro-credentials and the demand for entry-level professional certificates should support revenue growth in the longer term.

Coursera's data-driven marketing should also support revenue growth in the years ahead. The company's platform collects a good amount of student information regarding their preferences and career goals, which it uses to target potential learners with guidance for their career paths and personalized skill set recommendations. This aids in new paid customer acquisitions.

These secular demand trends and Coursera's data-driven marketing are expected to drive revenue growth in the long run. Management has guided for a 15% revenue growth (mid-point) in FY2023, and I believe the company can easily generate mid-teen annual revenue growth for the next few years.

Margin Outlook

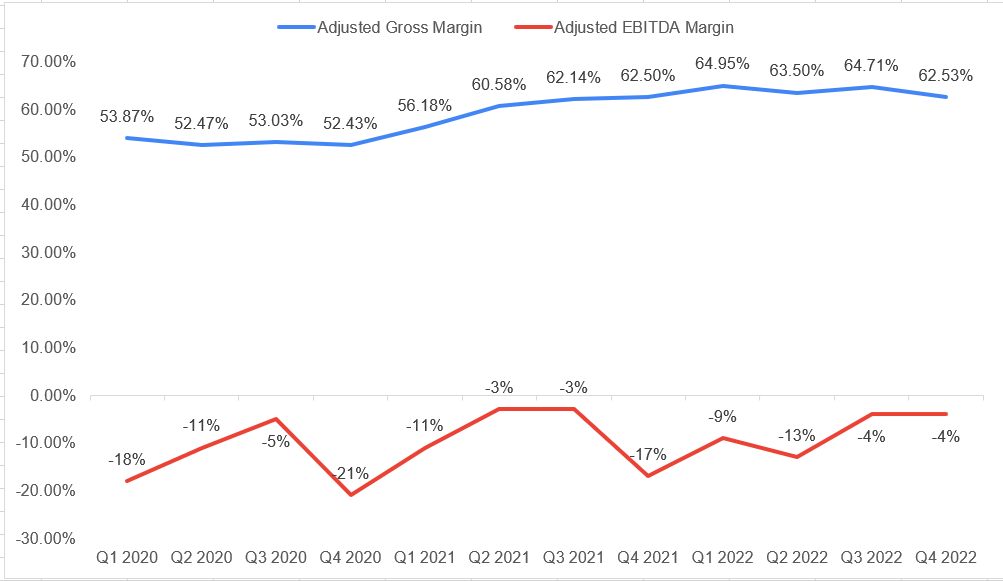

Since its IPO, COUR’s adjusted gross margin has benefited from a favorable product mix across its segments and relatively low fees given to its partners as a percentage of revenue share on their course materials. These lower fee partnerships enable COUR to invest in marketing, advertising, and research and development for its platform while saving on content creation costs, as COUR’s partners make the majority of the course content. However, heavy investments in advertising and marketing to expand its content offering have led to losses in adjusted EBITDA margin.

In the fourth quarter of 2022, the company was able to post growth in margins as a result of improving leverage from revenue growth and cost structure adjustments, including reducing the global workforce and lowering sales and marketing costs as a percentage of revenue. This resulted in a gross margin of 63.5%, in line with the prior period, and a 1300 bps YoY increase in adjusted EBITDA margin to -4%.

{kind=link}

COUR’s Adjusted Gross Margin and Adjusted EBITDA Margin (Company Data, GS Analytics Research)

Looking ahead, COUR’s margin is expected to be negatively impacted in FY23 due to a renegotiated contract renewal with one of its largest industry partners, which now stipulates a larger percentage of revenue share to the partner. Additionally, the contract renewal will result in a one-time incremental cost of ~$25 million in operating expenses spread evenly across the four quarters of 2023, which should adversely impact the adjusted EBITDA margin. While the contract renewal was necessary for the company's long-term growth, it will delay improvements in profitability in the near term and management has provided guidance for a negative 5% adjusted EBITDA margin in 2023.

The recent renegotiation of the contract has also exposed some vulnerabilities in Coursera’s business model which is overly reliant on its content partners which are big universities with substantial bargaining power. What if these universities try to further flex their muscles in the future to get a bigger piece of the revenue pie? I would like to see the company’s execution and contract negotiation in the future to get a better sense of its path to profitability, but the margin outlook doesn't look great at least for the first half of this year.

Valuation and Conclusion

COUR is trading at EV/Sales ((TTM)) of 1.60x and EV/Sales ((FWD)) of 1.39x. This is a premium compared to its largest peer Udemy which is trading at EV/Sales ((TTM)) of 1.35x and EV/Sales ((FWD)) of 1.17x despite UDMY’s higher revenue growth forecast. According to consensus estimates, Coursera's revenue is expected to grow by 14.71% in FY23 and 16.33% in FY24 while Udemy's revenue is expected to grow by 15.22% in FY23 and 22.10% in FY24. I like Coursera’s revenue growth prospects, but its high valuation compared to Udemy and cost headwinds after the recent contract negotiation keeps me on the sideline. Hence I have a neutral rating on the stock.

For further details see:

Coursera: Good Growth Prospects But Loss Making And High Valuation