CUZ - Cousins Properties: A Less Levered Office Operator

2023-04-04 10:27:15 ET

Summary

- Cousins Properties is an owner of premier office properties in quality Sunbelt markets, such as Atlanta, Georgia and Austin, Texas.

- A distinguishing characteristic of the company in relation to other office operators is their lower overall debt load.

- They are also reporting continued leasing strength in their core markets and are still capturing upside in their rents.

- Though shares have been significantly beaten down, I view the stock as well-positioned for an eventual rebound upon any reversal in sector sentiment.

Cousins Properties ( CUZ ) owns a portfolio of premier office properties in the Sunbelt markets of the U.S. Their two largest markets are Atlanta, Georgia and Austin, Texas, who collectively accounted for nearly 70% of their total net operating income (“NOI”) in 2022.

While the company has a diversified representation of industries served, they are more heavily weighted towards the Technology, Financial, and Professional Services sectors. Together, the three industries represent nearly 60% of their total annualized rents.

Among their top tenants are Amazon ( AMZN ) and Meta Platforms ( META ), to name two. At approximately 7% of annualized rents, AMZN is their single largest tenant.

Q4FY22 Investor Supplement - Partial Summary Of Top Tenants

While exposure to the technology sector presents risks, this is offset by their highly accommodative expiration schedule. And this is further supplemented by their conservative debt profile, which skews lower than many of their peers.

Since a prior update on the stock, shares have declined nearly 11%. The S&P 500 ( SPY ) has gained about 7% over that same period. Despite the losses, I maintain a favorable view of the stock, due in part to their most recently released results, which reinforced my convictions of their property class. Their lower degree of risk relating to debt repayment is another positive draw. Though the stock trades at a premium to other Sunbelt-focused office operators, I view shares as attractively priced for new and further initiation.

Recent Results and Current Portfolio Metrics

At year end, the company reported a portfolio-wide leased rate of 91% and a weighted average occupied rate of 87.1%. While occupancy was down, leased rates were up nearly 100 basis points (“bps”) on a sequential basis, due in part to a large signing pertaining to Apache Corporation’s new global headquarters in Houston.

For the quarter, the company signed 632K SF of space at a weighted average term (“WALT”) of 11.6 years. This represented their highest quarterly square footage volume of 2022. And when excluding new development, it was also their highest volume since the third quarter of 2019.

Excluding the Apache signing, the quarterly volume was 296K SF, with a WALT of 8.1 years. And of this total, new/expansion volume represented just under 50% of the total leasing activity. Furthermore, about 83% of their activity, net of Houston, was in the Austin market.

In total, CUZ executed approximately 2M SF of leases for the full year at cash spreads of 9.5%. The average roll-up would have been even higher, but they were offset in part by the dynamics of the Apache signing, which caused a headwind due to concessions provided.

This headwind could be seen by the spreads achieved in Q4 when including and when excluding the signing. Excluding the signing, the company would have reported total spreads of 27.7%. Instead, the roll-up was 7.3%, which, though lower, is in-line with their full year average.

While some would express concern at the concession provided for the signing, it’s worth noting that overall concessions for the quarter were nearly 20% below their weighted average for the first nine months of the year.

Additionally, net effective rents came in at a company record, when excluding the Houston market. And though the Houston market is clearly a laggard, it represents less than 3% of their total NOI.

Looking ahead, CUZ does expect total leasing activity to moderate. In addition, they have just 5.1% of their contractual rent expiring in 2023. While that is a positive in one regard, especially from an office standpoint, it also is a negative in that they will miss out on the mark-to-market opportunity embedded within several of their leases.

Liquidity and Debt Profile

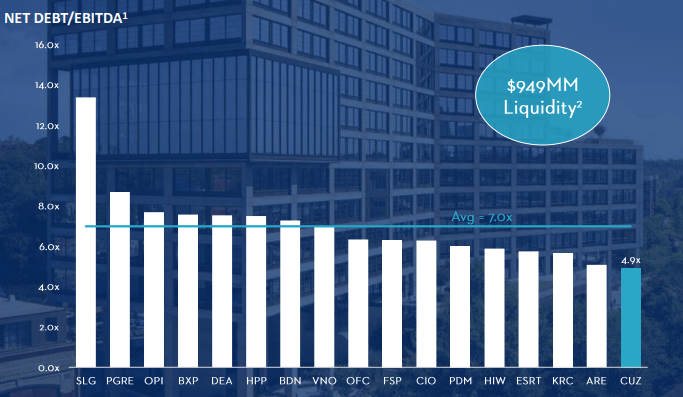

CUZ is strongly positioned from a liquidity standpoint . At year end, just +$56M was drawn on their +$1B credit facility. And their total debt load, as measured by net debt to EBITDA, stood at just 4.9x. This is the lowest among all related peers, including some of the most “high conviction” operators, such as Alexandria Real Estate ( ARE ).

February 2023 Investor Presentation - Debt Profile Of CUZ Compared To Peer Set

{kind=link}

Their debt ladder is also more accommodative, with just 1.3% of their total stack considered near-term maturities. This compares favorably to about 5.6% for their peer set.

While they will have a larger amount due in 2024/2025, I believe the company has ample liquidity and the access to capital to address these obligations when they ultimately come due.

Dividend Safety

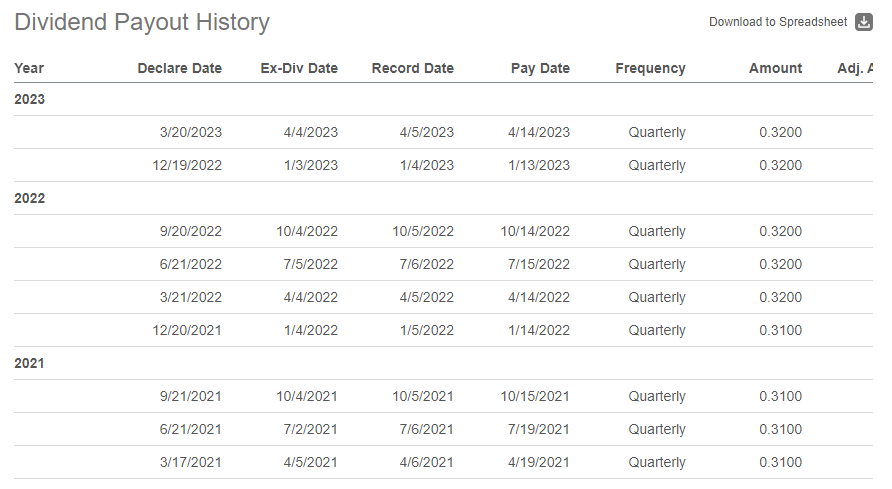

At present, CUZ provides a quarterly payout of $0.32/share. At current pricing, this represents an annualized yield of about 6%.

Seeking Alpha - Recent Dividend Payout History Of CUZ

{kind=link}

Unlike many of their peers, CUZ has a solid track record of growing their payout . Since 2017, for example, the total dividend has grown 33%. For most of the competition, payouts have remained fixed over the same time frame. Some have even cut or suspended their payments in light of current operating conditions.

While the threat of a cut is ever-present in the office sector, CUZ’s payout appears safe in its current form. In 2023, for example, management is expecting a full year midpoint in FFO of $2.52/share.

Based on this, the payout ratio would be just about 50%, well below sector averages. Even from a funds available perspective, the payout is running at approximately 70%, which still represents adequate coverage.

Final Thoughts

While the office sector faces real risks associated with oversupply, waning demand, and an incoming “wall of maturities”, companies such as CUZ continue to reinforce my conviction of the owners of premier space in well-located markets of the country.

The continuing demand for these properties was evident in Cousins’s year end results. Leased rates increased on the back of healthy new and expansion-based signings. In addition, the company realized strong leasing spreads, despite the drag created by one large signing in their weaker Houston market, which represents just a small portion of their overall NOI.

In addition, an accommodative expiration schedule and a conservative debt profile with a lower skew than many of their peers offsets the risks posed by their elevated exposure to the technology sector.

And they are also strongly positioned from a liquidity standpoint, with just $56M drawn on their $1B credit facility at year end, and a total debt load of 4.9x net debt to EBITDA, the lowest among related peers.

CUZ’s dividend payout also appears safe in its current form, as assessed by its payout ratio, which remains below averages. And it's not only safe, but it's also backed by a solid track record of growth since 2017.

Despite the continued decline since my prior update, I remain bullish on CUZ. At 8x forward FFO, shares do trade at a premium to other Sunbelt-focused office operators. Piedmont Office Realty Trust ( PDM ), for example, trades at less than 4x, while Highwoods Properties ( HIW ) trades at about 6x.

In my view, however, the premium is warranted, given their more favorable debt position relative to peers. Consistent with my previous assessment, I see an 11x multiple as a reasonable valuation. At this price point, shares would have implied upside of over 30%. In addition to the returns provided by their current dividend, investors could, therefore, benefit from the possibility of outsized returns on any reversal of sentiment.

For further details see:

Cousins Properties: A Less Levered Office Operator