CUZ - Cousins Properties Continues To Deliver In A Resilient Fashion

2023-07-31 17:15:54 ET

Summary

- Cousins Properties (CUZ) has a strong portfolio of office buildings in Sun Belt markets, with favorable growth dynamics and office-crisis resilient characteristics.

- CUZ also has a well-distributed lease expiry schedule and a strong balance sheet with the lowest leverage in the sector and no debt maturities in 2023.

- Q2 2023 earnings for CUZ were impressive, with increasing NOI and a resilient occupancy rate, supporting the bullish thesis on the stock.

- The recent price run-up is still immaterial relative to the historical valuation levels, and leaves ample room for CUZ's share price to revert closer back to more meaningful price territory.

Back on April 13th, 2023, I issued an article on Cousins Properties ( CUZ ) indicating a clear buy. There were six aspects, which together substantiated my confidence in the stock:

- Portfolio exposure , where all the office buildings held by CUZ are at either A or trophy status located in Sun Belt markets, which exhibit favourable secular growth dynamics.

- Lease expiries that are well-distributed in the future allowing CUZ to avoid negotiations over sizeable portfolio areas in the coming years, when the bargaining power is in favour of the tenants.

- Strong balance sheet with the lowest leverage ratio in the sector and close to no debt maturities in 2023.

- Absorbed interest costs , where the prevailing average cost of debt of CUZ has already converged closer to the market level, implying less of an unfavourable impact from the increasing interest costs on the FFO going forward.

- Conservative FFO payout of ~50% , which allows CUZ to retain ~ $200 million at the balance sheet level to deleverage even further or make accretive M&A moves.

- Attractive development pipeline , which primarily stems from CUZ's 4.6 MM square feet of land bank in prime Sun Belt areas providing future opportunities to expand the portfolio.

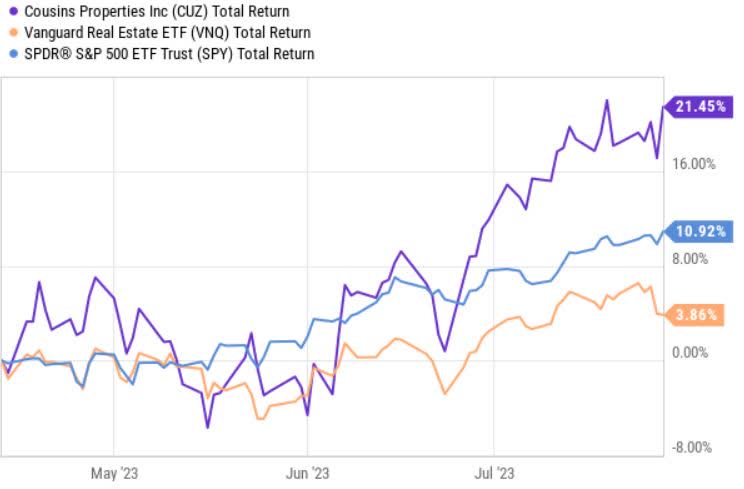

Since the article was circulated, CUZ has strongly outperformed the market.

{kind=link}

It seems that the market has slowly but surely realizing the underlying strength and competitive advantage of CUZ's portfolio.

{kind=link}

Yet, if we take a look at the relationship between CUZ and the broader REIT market, it is evident that CUZ has still a lot of room for convergence.

On July 27th, 2023, CUZ revealed its Q2 earnings, which, in my opinion, support the bull thesis of the stock and confirm the merits of the six elements described above.

Q2 results

Q2, 2023 figures delivered by CUZ were remarkable to me, registering improving financial results despite the prevailing pessimism in the office REIT space.

The same property performance was strong, where the NOI increased 6.3% relative to the 2022 comp. On a YTD basis this translated to a 7.3% increase in the like-for-like NOI.

The weighted average occupancy rate also remained resilient at 87.3%, which is by 30 basis points above the Q1, 2023 level.

As a result of this, CUZ updated its FFO guidance to a range of $2.57 to $2.65 per share, up from previous guidance between $2.55 and $2.65 per share.

The key underlying driver of these positive dynamics is the leasing activity. According to Richard Hickson (Executive Vice President of Operations) per Q2, earnings call, new and expansion leasing were the main sources of enhanced NOI:

In the second quarter we executed a solid 40 office leases totaling 435,000 square feet, with a weighted average lease term of seven years. This quarter's volume was a significant increase compared to the first quarter. Also notable, is that new and expansion leasing volume this quarter accounted for 79% of our total activity, a level not seen since 2021.

A noteworthy point here is also the duration of the newly stipulated leases, which on average extend to seven years. Currently, it is rather difficult to negotiate leases longer than a 3-year period for the office space as the tenants still possess stronger bargaining power due to structurally lowered demand for the conventional offices. However, I think CUZ has once again proved that the quality of office stock plays a significant role in securing stable and growing cash flows even in a sector that is currently out of vogue.

An additional proof that CUZ is a different office REIT is the fact that Q2, 2023 ended with an average net rent at $38.65, which is the second-highest quarterly level in a company's history.

{kind=link}

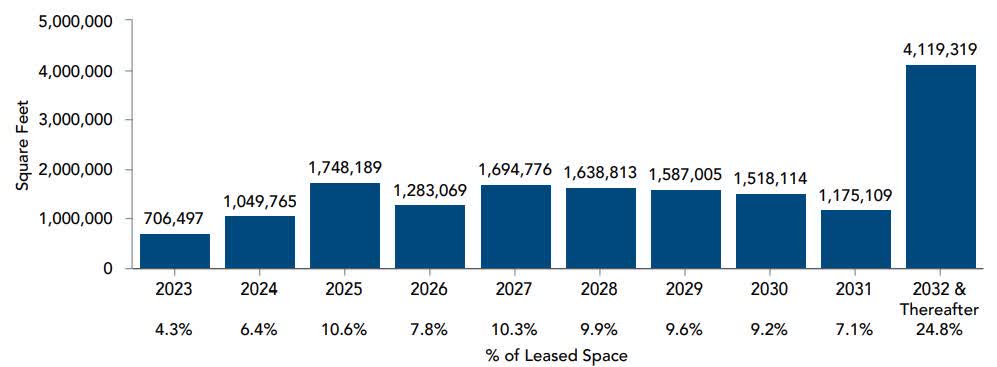

While it is rather obvious by now that CUZ is not exposed to the same challenges in the lease front as a typical REIT operating in the office segment, a well-laddered lease expiry profile still comes in handy in these market (sector) conditions. Namely, the near-term lease exploration profile of CUZ indicates that only 18.6% of annual contractual rents expire through the end of 2025.

Now, since early 2022, the key driver of FFO growth that has largely helped offset the growing interest cost burden has been the expiring lease contracts. Through new tenants or renegotiations with existing ones, CUZ has managed to secure favourable NOI spreads. There has not been any other major source of incremental cash besides the embedded rent escalators and rising parking fees.

So, in this context having distant lease maturities may limit material improvements in the earnings (FFO).

Colin Connolly (President, Chief Executive Officer) also provided commentary that growth via M&A program does not look promising in this particular moment:

Importantly, we have significant liquidity and capacity to pursue compelling new investments in a dislocated market when many peers now lack capital to compete. However, the downward re-pricing of assets in the private market is still playing out, thus we will remain patient, disciplined and continue to prioritize driving cash flow and maintaining a strong balance sheet. We are watching closely for new opportunities though and we will be ready when it is time.

Although CUZ has sufficient liquidity and fortress balance sheet to make accretive M&A moves, the sellers are not yet willing to accept market clearing pricing unless they absolutely have to. This is not something CUZ or office specific, but rather common across the board in REIT space.

Hence, we should expect CUZ to maintain or even further strengthen its best balance sheet in the industry and deliver moderate levels of continued like-for-like NOI growth.

Bottom line

After seeing the most recent quarterly figures I have become even more confident in my bull thesis on CUZ. And this is even despite the recent uptick in the share price.

{kind=link}

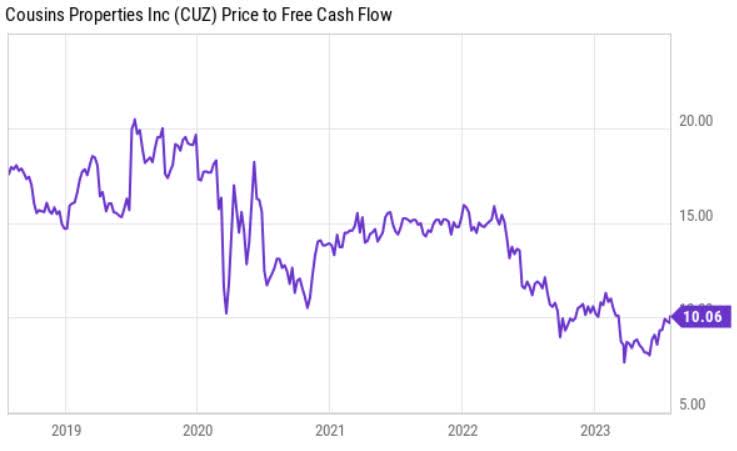

As of now, CUZ trades at P/FFO of 9.4x (or P/FCF of 10x), which is significantly below the historical average. At the same time, the dividend remains at a relatively juicy level of 5.4% that is backed with a safe FFO payout of 50%.

In my humble opinion, CUZ is a solid play for contrarian investors, who believe that sooner or later there will be a normalization in the office segment. When that happens, CUZ should rebound much closer to the historical average price level. While waiting for this thesis to play out, the risk of experiencing a notable drop in the share price seems limited.

For further details see:

Cousins Properties Continues To Deliver In A Resilient Fashion