CUZ - Cousins Properties Looks Safer Than Others In This Distressed Sector

2023-04-13 13:52:25 ET

Summary

- Cousins Properties holds a diversified portfolio of Class A offices that are spread across the prime locations in the Sun Belt.

- Over the past couple of years, its valuation has plunged opening up a significant discount relative to the peers and historical levels.

- In the meantime, FFO has decreased only marginally and given the secular trends in the Sun Belt, favourable leasing schedule and recent investments, the future FFO is expected to remain stable.

- The magnitude of the valuation discount is not justified as CUZ carries one of the safest balance sheets in the industry and has only 1.3% of total debt falling due this year.

- The conservative FFO payout level, recent investments coming online, and largely absorbed interest rate impact will inevitably contribute to a mean reversion in the valuations.

Since the outbreak of COVID-19, the office segment has been one of the most severely hit areas in the entire commercial real estate space. While retail and hotel properties faced the sharpest drop in rents, in the subsequent periods these segments have experienced gradual reversion to the pre pandemic levels. For offices it has been a bit different. First , the period of most aggressive restrictions in the economy was not that painful as most tenants kept paying rents despite the actual (physical) occupancy levels being very minimal. The underlying lease contracts and a belief that after the pandemic people will return to the office justified continued payments of rent. Second , as opposed to the retail and hotels, office segment has been subject to a notable shift in paradigm. Namely, during the pandemic many tenants (companies) realized that work-from-home policy is doable, more cost efficient and strengthens the offering for current and prospective employees. This has removed a significant chunk of demand from the office segment, while the supply has remained constants. So, there is a negative supply and demand dynamic both at the present moment and structurally in the long-run. Third , the combination of negative supply and demand dynamic, higher interest rates, expensive property repurposing and generally high indebtedness in the sector have considerably impaired the current valuations and long-term prospects of many offices.

However, each systematic drawdown usually introduces some new buying opportunities, where the healthy and well-managed constituencies are unfairly punished together with the rest and subpar players.

In my opinion, Cousins Properties (CUZ) presents such case. Below you can find three main reasons why CUZ entails a relatively high probability of outperforming the sector and generating predictable dividends going forward.

1. Durable portfolio and diversified across favourable geographies

CUZ owns only class A office properties, where all of them are located in the Sun Belt area. The average year built of CUZ properties is 2004, 19.1 MM SF large and 91% occupied.

{kind=link}

Currently, one of the biggest issues for owners of office buildings is the negative rate of change in the demand. The worry is not only bound by the short-term hiccups, but also related to the long-term development.

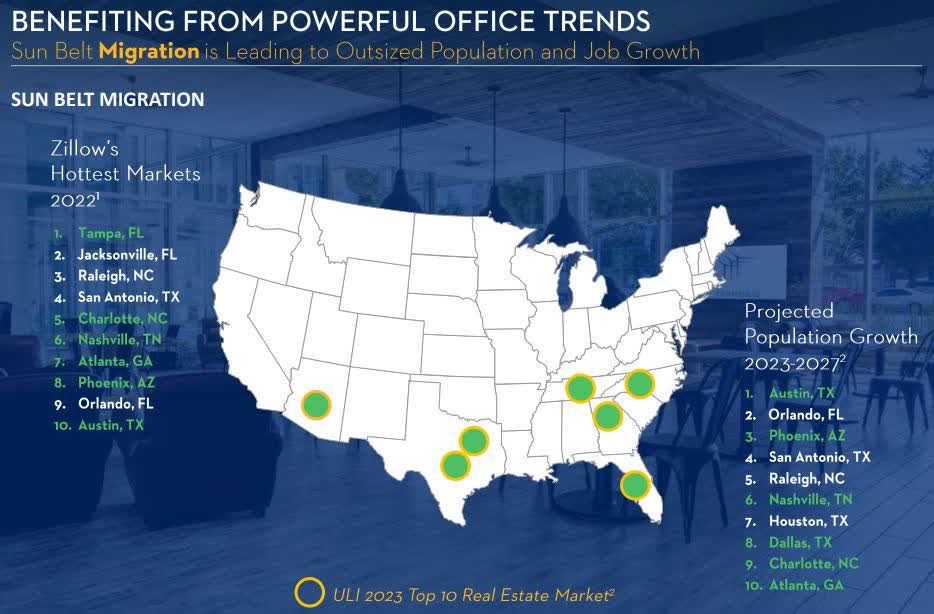

In general, the Sun Belt provides secular tailwinds for the overall growth, business activity and real estate. The historical trend and future projections indicate an outsized population and job growth.

According to the Avison Young research Atlanta office market continuous to perform well and still enjoys favourable momentum for the office sector. For instance, the direct asking rents have remained stable and even increased a bit from $30.9 psf in 3Q 2022, to $31.4 psf in 1Q 2023.

Since 3Q 2020, there has been an uptick in the vacancy rate (from 16% in 2020 to 21% in 1Q 2023), but this is mostly relevant for class B buildings.

Austin is projected to face similar dynamics. As per Avison Young research "Austin office market insights, Q1, 2023":

The long-term outlook remains positive, given the area's strong economic and labor market fundamentals that will help tackle the near-term softening macroeconomic landscape. The city's rapid population growth, competitive quality of life, and growing clout as a tech hub will continue attracting companies and driving the highest return to office rates in the nation.

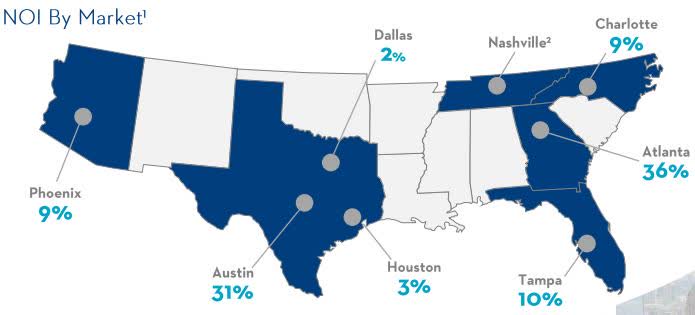

Tampa, Phoenix and Charlotte, which are also rather notable geographies in CUZ's portfolio from the NOI perspective, entail similar characteristics and future growth patterns.

It is clear that office owners that have solid class A portfolio with attractive locations will manage to weather the storm better and eventually benefit from the structural demand dynamics. CUZ fulfills both of these elements - premium offices and favourable locations.

{kind=link}

The following facts capture the essence of underlying quality in CUZ's portfolio:

- CUZ asking rents are 9% higher than pre-COVID levels and 24% higher than for average class A in the Sun Belt.

- 34% of portfolio is less than 5 years old or recently developed.

- Historically, CUZ has been a leader in driving NAV growth of 6% per year since 2017.

At the same time, CUZ's lease expiration schedule allows to mitigate the near-term risks of elevated vacancy levels that might be driven by an overall economic uncertainty and possible tech layoffs, which in turn might lead to temporary gaps in the occupancy.

{kind=link}

CUZ has the lowest percentage of lease expiries in 2023 and 2024 relative to the other office peers. Only ~10% of the total leases fall due over this and next year. This is extremely helpful for pre-emptively steering the capital in right direction (e.g., avoiding considerable investment commitments when there is a risk in the coming years to suffer short-term pain in occupancy levels).

2. Fortress balance sheet supporting growth in a prudent manner

CUZ carries the lowest financial leverage profile in the industry. As of year-end 2022, CUZ's Net debt/EBITDA stood at 4.9x, while the sector average was 7.0x.

CUZ is also one of the leading office owners in the context of near-term debt maturities. For instance, this year CUZ will have to refinance or pay off only 1.3% of the total outstanding liabilities. In 2024, there will be much higher portion to refinance (~15%). Yet, given that CUZ holds $949 million of fresh liquidity in credit lines and that lion's share of the liabilities maturing in 2024 are based on variable rate there should not be a material impact on the CUZ's average cost of debt and ability to successfully rollover the maturing portion.

Currently, CUZ's weighted average interest rate is 4.48%, which is just ~150 basis points below the recent financing it managed to secure from commercial banks. This indicates that the incremental financings, assuming that the current interest rates remain constant, should not have a material impact on the FFO figures. The most recent (Q4, 2022) fixed charges coverage ratio was 4.7x, which is considerably above the norm.

3. Depressed valuation levels and a reasonable probability of mean reversion

Looking back at the past three year period, CUZ has significantly underperformed the broader REIT market, which itself has lagged behind the S&P 500.

{kind=link}

As of now, CUZ trades at a price to FFO of 7.9x, which is ~52% below the year-end 2019 level. Over the same period, the FFO per share has decreased only by ~$0.06, corresponding to a negative movement of 2.5%. So, already here from the historical perspective and given where the current FFO numbers are, there is a huge divergence.

Compared to the other players in the office segment and their prevailing valuation levels, there is also a notable difference. Namely, as per latest NAREIT report (March, 2023) the average price to FFO is 9.1x, which implies a ~ 15% discount. In December, 2019, the relative valuation discount to the other peers was just ~ 5%.

From the statistics above, we can conclude that CUZ trades drastically below its historical average and meaningfully below its competitors, even though historically the difference was much smaller.

Now, the question is whether the discount is justified and what could be the possible catalysts for an upward push in the multiple.

Here is my reasoning for why I think CUZ will manage to deliver abnormal returns in the long-run without suffering too much until the uncertainty in the sector abates:

- Portfolio exposure - as described above, CUZ holds relatively fresh class A offices in geographies that embody positive secular demand dynamics.

- Lease expiries - CUZ has the luxury to avoid negotiations over notable portfolio areas in the coming two years, when the bargaining power is structurally in favour of the tenants.

- Strong balance sheet - the fact that CUZ has the lowest gearing in the industry and almost no debt maturities this year bodes well for keeping the financial risk in balance.

- Absorbed interest costs - the prevailing average cost of debt level is very close to the one, which can be currently found and negotiated in the financing market. Given the current interest rates remain where they are now, there is relatively immaterial impact on the FFO from future increase in CUZ's interest expense component.

- Conservative FFO payout - on average CUZ pays ~47% of its annual FFO in dividends. This means that there is roughly $200 million of cash kept at company to either strengthen the balance sheet or fund growth opportunities. Considering that CUZ's balance sheet is already robust, my expectation is that most of the retained funds will be channeled towards new investments as there is no need to overcapitalize the company.

- Attractive development pipeline - over the next two years, two new properties are expected to come online with a total of ~ 770`000 square feet. Approximately, 94% of the total costs are already incurred and reflected in the 2021 and 2022 financial statements. Initial revenue recognition is projected to take place in late 2023 or early 2024. While, the incremental impact on the FFO will not be significant, it will still help offset some near term downward pressure on the NOI stemming from potentially decreased occupancy rate. Lastly, CUZ holds 4.6 MM square feet of land bank in prime Sun Belt areas that provide future opportunities to expand the portfolio.

Key risks to the buy thesis

The main risks associated with CUZ's overall financial performance are mostly of a systematic nature as the underlying company specific factors (i.e., idiosyncratic risks) are well managed.

The leverage profile of CUZ mitigates financial risk and neutralizes refinancing risk in the foreseeable future. Similarly, the asset quality and the fact that majority of the buildings are still relatively fresh, mitigates the risk of obsolesce, especially considering the structural tailwinds for the Sun Belt area.

However, the systematic or beta risks are still present and might lead to a more deeper drawdowns and depressed valuations multiples for long period of time. There are two potential drivers that could impair the prospects of CUZ and consequently weaken the investment thesis.

An uptick in interest rates could put a downward pressure on the future FFO and CUZ's ability to capture positive spread between WACC and property cap rates. Higher interest rates might also constrain the NOI trajectory as a significant chunk of CUZ's tenants are technology companies for which an unfavourable change in rates can seriously impact their financial profiles. We can already now observe how many technology companies, even that are already well established, are devising aggressive cost cutting strategies to offset the inflationary factors including the surging interest costs.

Lastly, if the economy does not recover any time soon and technology companies as well as banks, which also constitute a material part of CUZ's tenant portfolio, continue to suffer, there could be depressing consequences on the occupancy levels.

However, I strongly believe that what matters the most is the secular dynamics in the Sun Belt (i.e., CUZ's locations) in conjunction with the high asset quality. These elements should justify the long-term thesis of capturing both capital appreciation and continued dividend gains. In the short-term, one could expect further downside volatility via increased occupancy rates - mostly, from partially extended leases or completely renegotiated yet at lower price levels. Yet, CUZ's financial profile is strong enough to weather these challenges without sacrificing dividends.

The bottom line

There is a notable disconnect between the magnitude of drop in CUZ's valuations and the state of CUZ's underlying fundamentals.

Given the above, my expectations would be that CUZ will safely service its current 6.3% dividend yield and at the same time deliver capital appreciation gains from a partial closure in the valuation discount relative to its peers.

CUZ fundamentals are strong enough to explain at least similar valuation levels as in the sector. This implies ~ 19% of share price gain on top of the ~6% dividend income.

For further details see:

Cousins Properties Looks Safer Than Others In This Distressed Sector