CUZ - Cousins Properties: Major Signs Of Resiliency In The Q1 Figures

2023-05-06 11:22:43 ET

Summary

- Recently, Cousins Properties issued a Q1 report which overdelivered on both top and bottom-line estimates.

- In mid-April, I articulated the strengths of Cousins Properties office portfolio and balance sheet, and in the context of depressed valuations, I issued a buy rating.

- Since the date of buy rating, the stock has delivered some excess returns relative to the market, yet the multiple, in conjunction with the recent financials, still seems rather low.

- In my opinion, Cousins Properties is still a clear buy with a great potential to resist the near-term shock and deliver superior returns via both capital appreciation and juicy dividends.

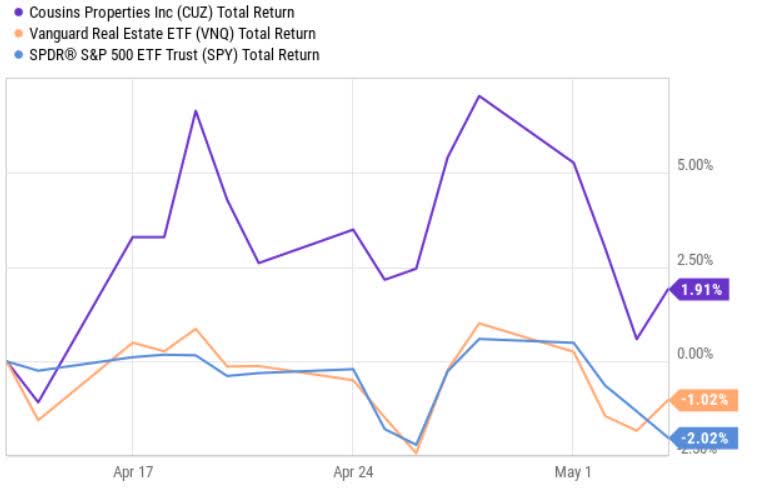

Since the date of a buy recommendation, Cousins Properties ( CUZ ) share price has performed slightly better than the S&P 500 and the broader REIT market.

{kind=link}

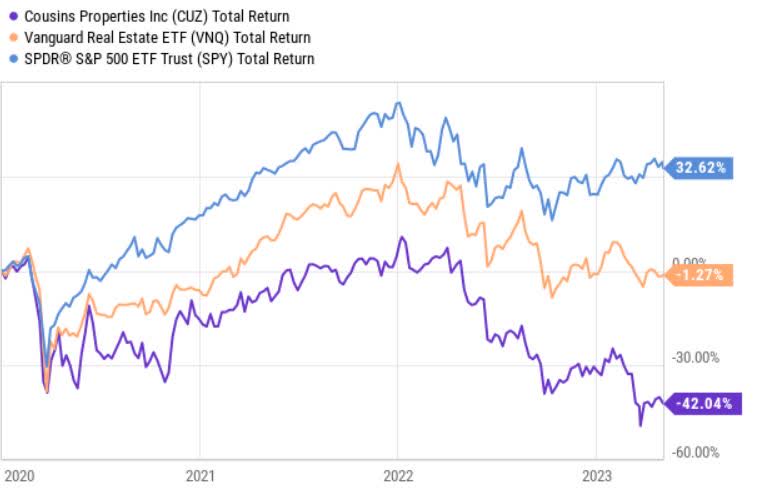

While this obviously is something positive, if we zoom back to the early beginnings of the COVID-19 and the FED's shift in its monetary stance, CUZ trades still at relatively (and historically) depressed levels.

{kind=link}

It is interesting to notice the gap in price performance between the Vanguard Real Estate Index Fund ( VNQ ) and CUZ. The most important reason why the overall REIT market has underperformed the S&P 500 is the high sensitivity to rate of change in interest rates as REITs are treated and to some extent also valued as bond-like investments given the predictability and duration profile of the underlying cash flows. As we know, whenever there is an uptick in the interest rates, bond prices tend to respond in a notable and negative fashion.

Now, I am not arguing that the REITs should not be down, but what I am trying to say is that CUZ has been punished by an extra 41% relative to the VNQ due to a non-interest rate-related factor. Namely, there is no reason to consider a more pronounced impact from the change in FED's policy given the state of CUZ's balance sheet (i.e., one of the healthiest balance sheets among its peers; with net-debt-to-EBITDA of 4.9x).

The non-interest rate-related factor is the sector-specific risks pertaining to the office stock and all of the knock-off effects stemming from the COVID-19 and work-from-home policies.

In my humble opinion, CUZ is uniquely positioned to not only weather the approaching storm in the office space, but also capitalize on the surging cap rates via accretive M&A, while making no sacrifices on the dividends payments.

Before synthesizing Q1 earnings, let me quickly remind the key drivers of my bull thesis for CUZ:

- Durable portfolio and diversified across favourable geographies. The portfolio consists of class A offices with 35% of less than 5 years old or recently developed. All of CUZ's properties are located in structurally growing and favourable locations. The fact that CUZ's asking rents are 9% higher than pre-COVID levels and 24% higher than for average class A in the Sun Belt is a clear testament of that.

- Fortress balance sheet supporting growth in a prudent manner. CUZ carries a considerably stronger balance sheet compared to the rest of the U.S. office equity REITs. The net-debt-to-EBITDA stands at 4.9x compared to the benchmark average of 7.0x. CUZ also has a well-structured debt financing profile, where less than 1.5% of outstanding borrowings fall due this year. At the same time, the current average cost of debt for CUZ is not that far below the rate, which can be obtained in the market. We are talking about ~200 basis points. While the convergence to the market rates will take place and will have a negative effect on the future FFO, the impact will not be so large that dividends and/or accretive M&A transactions get sacrificed.

- Depressed valuation levels and a reasonable probability of mean reversion. The forward P/FFO multiple at which CUZ trades is ~52% below the year-end 2019 level, while over the same period, the FFO has decreased only by 2.5%. At the same time, CUZ trades at a ~15% discount relative to the other U.S. office equity REIT peers.

Synthesis of Q1 earnings

The recently published Q1 earnings by CUZ confirmed the underlying resiliency of the portfolio and proved how important healthy balance sheet is.

CUZ recorded strong like-for-like development where the NOI figure increased by 4.9% compared to the Q1, 2022. The key driver of an improved NOI result was the combination of rent escalators and favourable leasing activity stemming from the expiries of previous leases (renegotiations). On a quarter-on-quarter basis, the occupancy rate also remained at a healthy level and even slightly increased by 0.4% to a total of 90.6%. This marked a fourth straight quarter of an increased occupancy rate for CUZ.

On the cost side, there are some obvious headwinds attributable to the notable cost inflation factors. The SG&A increased to 0.37% of total undepreciated assets, which is 7 basis points higher than in the prior quarter. Another major factor offsetting the benefits from improved like-for-like figures was higher interest costs that grew by 13% compared to the Q4, 2022. If compared to the Q1, 2022, the rate of change in interest costs lands at 66%.

As a result, the FFO per share landed at $0.65 - almost the same level where it was in Q4, 2022 ($0.66 per share).

On a go-forward basis (until year-end 2023), the FFO is expected to remain stable due to the following reasons:

- There are immaterial debt maturities in 2023 (less than 1% of the total outstanding debt) as a result no additional headwinds are expected from the interest cost component (except from the slight uptick in SOFR associated with the floating rate debt due to the recent FED's decision).

- Less than 5% of leases are expected to expire this year, from which a part has already been renewed at more attractive pricing for CUZ. While remaining leases will provide an opportunity to increase rents, these effects will be likely offset by higher operating expenses (mostly related to labour input factors).

- While CUZ still holds a fortress balance sheet (at net-debt-to-EBITDA of 5.1x), which allows the Management to devise accretive M&A strategy, we should not expect incremental cash flows from new acquisitions.

CEO during conference call on April 28:

Importantly, we have significant liquidity and capacity to pursue compelling new investments in a dislocated market when many peers now lack the capital to compete. However, the downward repricing of assets in the private market is still playing out. Thus, we remain patient, disciplined and continue to prioritize our strong balance sheet.

The bottom line

The Q1 earnings proved that CUZ has the ability to weather the volatility in the office segment as, even during these rather unfavourable times when there is a structural oversupply of office buildings. CUZ has managed to both renew and increase rents on the expiring leases. Also, the FFO figure came in at a stable level despite surging interest rates and inflationary pressures from the OpEx side.

The forward P/FFO multiple of 8.1x is still very low and at a ~15% discount compared to the benchmark level. At the same time, the dividend yield of 6.1% is attractive and safe given the FFO payout ratio of just 49%.

In my opinion, my previous bull thesis remains intact. CUZ should be able to withstand the shocks in the office segment and in the financing markets, and act opportunistically once cap rates are sufficiently attractive. Ultimately, this will help the stock to close the valuation gap in the office equity REIT segment and provide solid returns for investors, who while waiting for this to play out can count on stable streams of current income.

For further details see:

Cousins Properties: Major Signs Of Resiliency In The Q1 Figures