CUZ - Cousins Properties: Stronger After Q3 Despite Struggling Sector

2023-11-26 04:29:35 ET

Summary

- Cousins Properties has a high-quality portfolio of office buildings in vibrant locations, backed by a strong balance sheet and conservative FFO distributions.

- The company has performed well compared to the office REIT segment, with improving NOI and occupancy rates.

- CUZ has the strongest balance sheet in the industry, ample liquidity, and low debt maturing over the next few years, positioning it well for future opportunities.

- Despite the inherent resiliency stemming from the trophy-like properties and fortress capital structure, CUZ is only 8% more expensive than the rest of peers in a struggling sector.

- 6.5% dividend yield provides an attractive motivation for investors, while waiting for a more proper recalibration by the market.

Back on April 13th, 2023, I wrote an article on Cousins Properties (CUZ) recommending a buy despite some notable headwinds on a sector level.

The essence of the thesis lied in the combination of the following factors:

- High quality portfolio consisting of mostly trophy-type office buildings located in vibrant location s.

- Robust financials , which are backed by one of the safest balance sheets in the sector and conservative FFO distributions leaving ample cash flows to further reduce leverage of secure accretive investments.

- Appealing growth pipeline , which is based on CUZ's 4.6 MM square feet of land bank in class A Sun Belt locations.

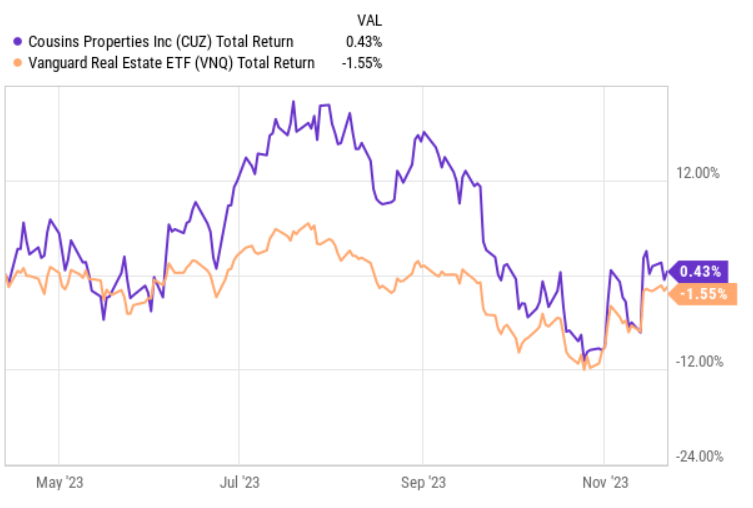

Since then, CUZ has performed more or less in line with the overall REIT market (on a total return basis).

{kind=link}

While this might sound not that solid, if we compare CUZ to the office REIT segment, we would notice a presence of a significant alpha (ca. ~13% based on the NAREIT average).

Now, roughly a month ago CUZ published its Q3, 2023 results , which revealed some rather interesting dynamics that should be considered by long-term investors, who have longed CUZ.

Q3 in a nutshell and key takeaways

All in all, CUZ managed to register very decent operational results in almost all fronts of the financials.

The overall like-for-like NOI increased by 4.6% (on a cash-basis) and the second generation (related to renewals) NOI grew by 9.8%. While the FFO per share landed slightly below the Q3, 2022 level, in terms of the rate of change effects and adjusted for the extraordinary items, the FFO was flat.

The total office portfolio occupancy rate and end-of-period lease percentage both increased by 0.3% during the Q3 to 88% and 91.1%, respectively. These results mark the strongest performance (or levels) since 2021.

Interestingly, that CUZ has delivered this in quarter, which was rather busy with new leases and the expiries of existing ones. In total CUZ signed 32 office leasings at a weighted average lease term of 8.6 years.

As you can see, the overall picture looks solid. While there are some painful headwinds blowing in the office sector and many of the office REITs are on a constant decline with a meaningful probability of potential default, CUZ seems to be unaffected. If there were major struggles for CUZ to attract tenants, we would not see improving like-for-like NOI or strengthened occupancy ratio.

Furthermore, because of no new acquisitions, major investments and thanks to ~50% FFO payout, CUZ's balance sheet has continued to improve.

{kind=link}

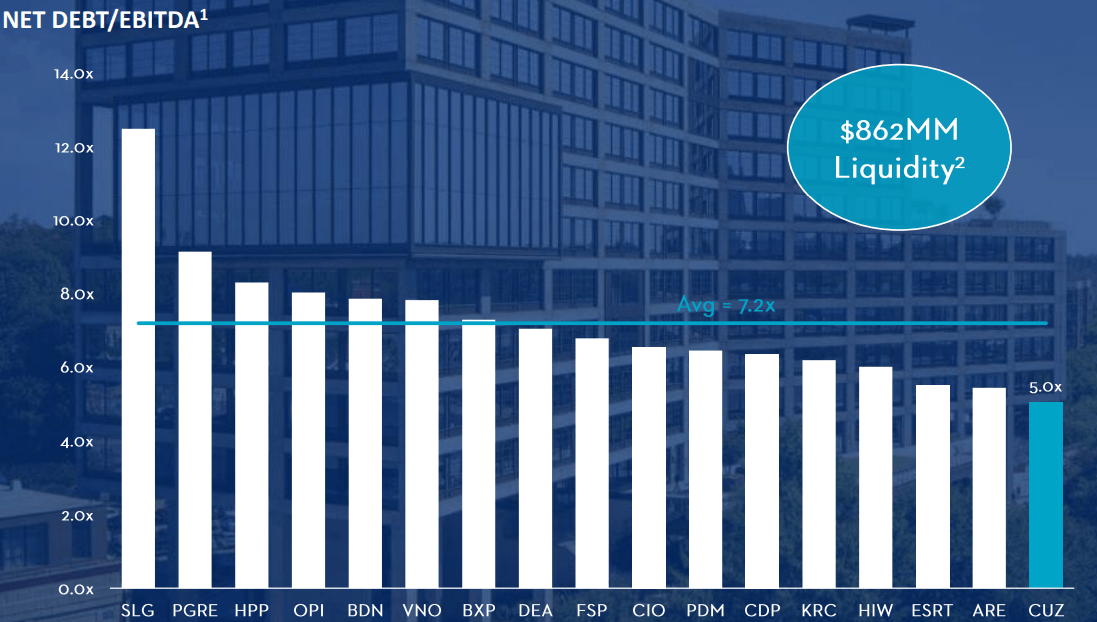

As of Q3, 2023, CUZ has the strongest balance sheet in the industry if measured on a net debt to EBITDA basis. Plus, it also hold ~$850 million in liquidity, which accounts for roughly 28% of the current market cap level.

From the debt maturity perspective CUZ is also well-positioned; in fact, having one of the lowest portions of debt maturing over the remaining 2023 and 2024 period. While the sector on average has to refinance ~12% of the borrowing over 2024, in CUZ's case we are talking just about ~3%.

Another layer of safety on top of that which stems from the fortress balance sheet is the underlying structure of leases. Currently, CUZ has only 15.1% of total leases expiring through the end of 2025 (and only 6% in 2024).

With all of this being said, it is clear that CUZ does not only continue to perform well and deliver attractive results, but it also carries an embedded financial buffer making the Company resilient and able to capitalize on the new opportunities.

As mentioned earlier, CUZ has access to a sizeable amount of immediate liquidity and considering the prevailing position of its balance sheet, there is definitely incremental financial capacity to assume more debt in case that is necessary. Lastly, 50% FFO payout warrants additional ~$200 million of proceeds that could be put at work from internal cash generation.

This means that CUZ is well-equipped and positioned to act opportunistically when attractive deals emerge.

In my opinion, this is one the most important catalysts that should eventually compensate investors for going long CUZ. Just looking at how other peers are experiencing difficulties to access financing (both debt and equity due to depressed valuations) and the fact that in most cases these balance sheets are to a large extent already exhausted, CUZ's liquidity should be viewed as a competitive edge.

According to Colin Connolly - President and Chief Executive Officer, there are some early signs of accretive opportunities, but for the heavy lifting to take place it still needs a bit of time:

But we are starting to see an uptick in opportunities that we are tracking. I think in many cases, it's still a bit early to insert ourselves in those opportunities because there are I'd say capital structure dynamics that are still playing out between, in many cases, owner and lenders. But we are tracking a number of situations that are going to require outside capital. And I think it could be interesting opportunities, but we need to be patient and wait for the right time.

For CUZ investors being patient and waiting for the right opportunities is not that difficult. Although the FFO payout level is very conservative, because of the depressed share price, CUZ is able to offer a rather attractive dividend yield (i.e., ~6.5%).

The bottom line

In my humble opinion, CUZ is underappreciated by the market. In the past 3-year period, the share price has dropped by ~40% even though the fundamentals have remained stable and the operational performance has been improving.

Currently, CUZ is 8% more expensive than its closest peers if we base that on projected P/FFO multiple in 2024. To me this is unjustified and considering the fact of the safest balance sheet in the sector, ample liquidity reserves and great organic growth on a same property level, it seems that long-term investors have an attractive opportunity to enter CUZ.

The key catalysts here are:

- Emergence of attractive enough deal opportunities, where CUZ can put its liquidity at work to capture appealing spreads between the cost of financing and expected property IRR.

- Normalization of interest rates, which should per definition provide a notable tailwind for the overall equity valuations, especially across the sectors that have been struggling a lot due to a more restrictive financing.

For further details see:

Cousins Properties: Stronger After Q3 Despite Struggling Sector