COVTY - Covestro: Darkest Hours Have Passed

2023-05-03 06:21:43 ET

Summary

- The company starts to be on the road back to mid-cycle earnings estimate.

- €500 million buyback resumed with a third tranche of €75m starting in May.

- EBITDA was well above the guidance range of €100-150 million.

After having commented on BASF's latest results with a publication called ' We See Light And Shadow In Q1 ', it is now Covestro's (CVVTF)(COVTY) turn. As a reminder, we were cautious about the company's short-term horizon and anticipated the dividend suspension already in Q3 last year . Despite that and in line with the other chemical players, we are starting to see the light at the end of the tunnel . Why?

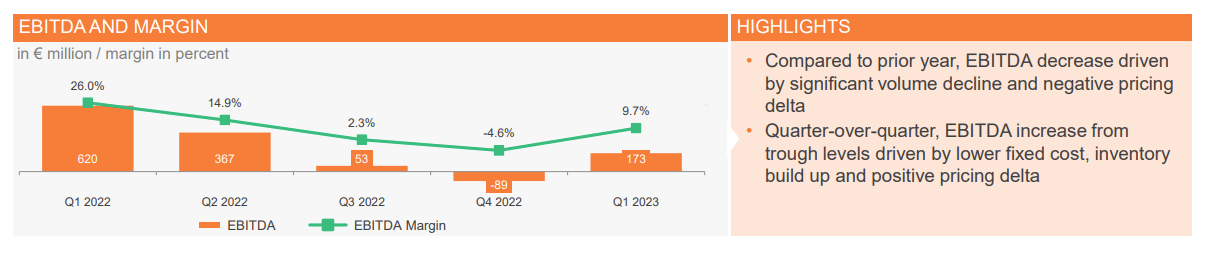

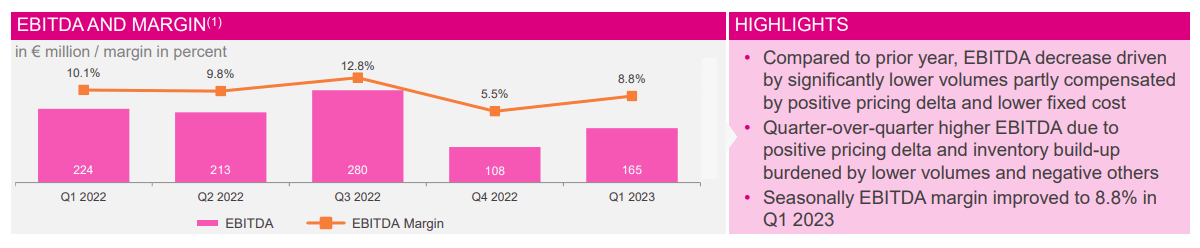

- Looking at the Q1 results, there is a continuous volume decline on a yearly basis which is due to client destocking mainly and the EU economic slowdown. Here at the Lab, we are confident that Covestro has now passed its darkest hour and we are anticipating a positive earnings momentum thanks to 1) gradual facilities utilization rates backed by competitor shutdowns announcements, 2) lower energy prices costs, and 3) volume recovery in the 2023 second half with a rebound from the Chinese reopening and Europe. Looking at Figures 1 (Performance Materials EBITDA evolution) and 2 (Solutions & Specialties EBITDA evolution), Covestro is returning to a positive EBITDA contribution. Fixed cost reductions as well as a positive pricing delta were not able to offset volume decline and higher energy prices;

- The company is currently addressing its cash flow evolution. Covestro-guided spot spreads and CAPEX investment that lead to a negligible free cash flow in Fiscal Year 2023. Here at the Lab, we are forecasting ~€400 million improvement in output and better spread through the year. This positive guidance is also backed by 1) better-working capital management, and 2) cost-saving initiatives estimated at €100 million. Despite these headwinds, we are confident that Covestro's cash flow generation has been restored with the difficult decision to suspend its dividend payment , curtail its CAPEX, and halt the buyback;

- At the operational level, we estimate that the company's key product spreads will improve. In detail and by-product, we see the MDI markets well balanced with a supportive demand in line with supply. On the TDI market, we expect a better utilization of approximately 300 basis points by 2024. This is driven by a lack of supply. In detail, BASF announced a 300kt closure in the EU market. With competitors that are exiting the EU markets and BASF which will close the TDI plant in Ludwigshafen, we are anticipating a higher utilization rate for Covestro (86%) - Fig 4. While Polycarbonates utilization rates should slightly increase after a long period of weakness;

- To support Covestro chemical spreads improvements, it is important to report the Jaideep Pandya question from Onfield Research. In the Q&A call , management is guiding flat volumes for Q2 but lower energy costs. March spread improvement back our forward-thinking for a better year. Our primary earning increase is a function of better product spreads;

- Related to points 1) and 3), here at the Lab, we are forecasting a higher EBITDA of 6.5% at the EBITDA level for the next two years. Implicitly, we are anticipating a return toward the mid-cycle level over the forecast period;

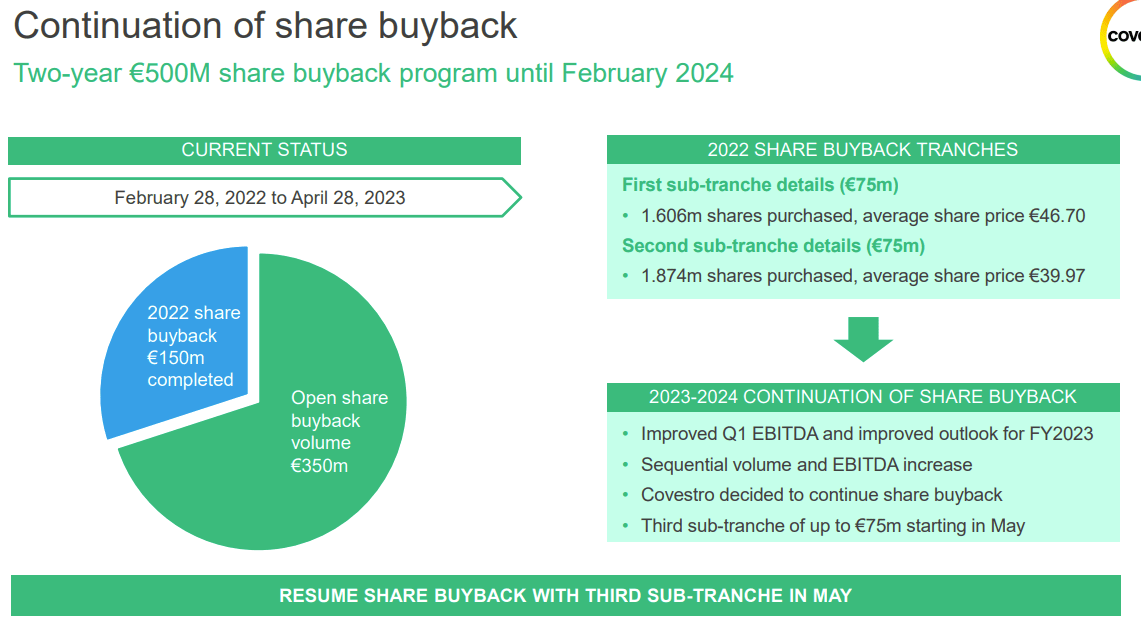

- On a positive note, the company is back to buy its own shares. The third sub-tranche in May has been announced. This has a value of approximately €75 million (Fig 3).

Performance Materials EBITDA evolution

{kind=link}

Source: Covestro Q1 results presentation - Fig 1

Solutions & Specialties EBITDA evolution

{kind=link}

Fig 2

{kind=link}

Fig 3

BASF TDI capacity in EU

Fig 4

Conclusion and Valuation

Last time, we forecasted a Q1 EBITDA between €100 million and €150 million. Covestro delivered €286 million in results, very much above our internal estimates as well as Wall Street average consensus. We might conclude that the company starts to be on the road back to mid-cycle earnings estimate. Here at the Lab, we decided to slightly increase Covestro's EBITDA, and based on a 5.5 EV/EBITDA target multiple in 2024, we derived a buy target at €48/share ( from €47 ). However, on 12-month forward EV/EBITDA, we believe that Covestro is fairly priced in. In detail, it is currently trading at ~7.9x in line with peers. For this reason, as already mentioned last time, we decided to maintain a neutral view and we still prefer BASF . Our risks section includes: 1) slower industrial activities (especially in the coating, construction, and automotive), 2) cyclical downturn, 3) FX evolution, 4) production overcapacity, and 5) higher energy costs.

For further details see:

Covestro: Darkest Hours Have Passed