CVU - CPI Aerostructures: Don't Buy

2023-08-25 00:30:33 ET

Summary

- CPI Aerostructures has seen a 7.1% return against a 5.9% return for the broader markets.

- CVU's recent results show increased revenues and profits, driven by higher sales and better margins and amortization.

- Analyst estimates for 2023 do not align with the company's guidance, and the stock's upside is limited.

In a previous report , I analyzed CPI Aerostructures ( CVU ) and while the company has a broad array of programs it is active on, I couldn't see a convincing element to build a bullish thesis on. So, in my book, the company was a hold and that has not been a bad call, with a 7.1% return against a 5.9% return for the broader markets.

In this report, I am revisiting CPI Aerostructures with a brief discussion of the most recent results and a valuation using our improved evoX Financial Analytics tool. CPI Aerostructures does not get a lot of coverage from analysts, and I have observed that even some analysts who covered the company misrepresent certain accounting standards as they lack the basic knowledge of the industry.

About CPI Aerostructures

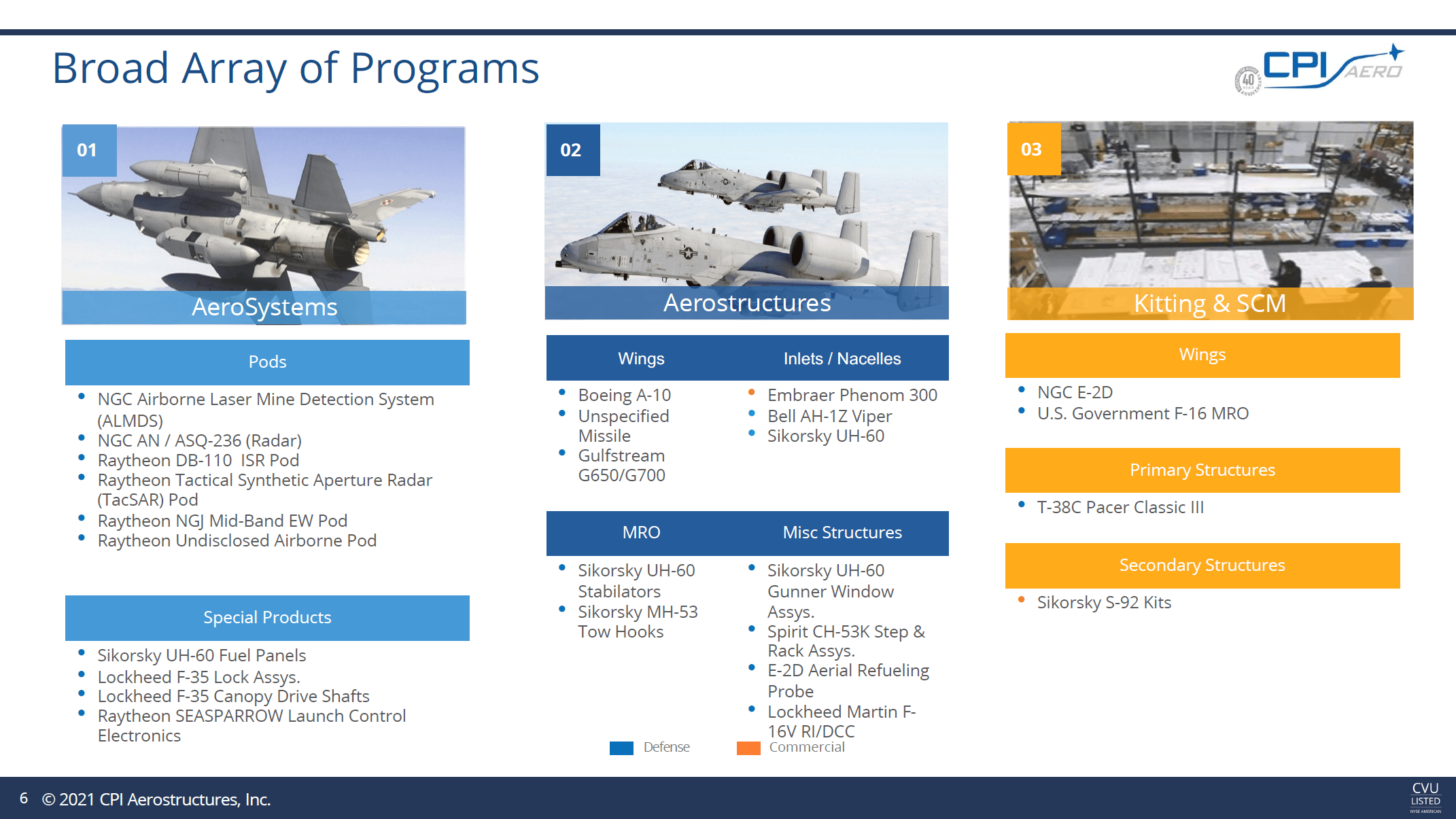

CPI Aerostructures has a market cap of less than $50 million, so it is a rather small name that not everybody will be familiar with. So, a small introduction might be useful. CPI Aerostructures manufactures structural assemblies for Tier 1 and Tier 2 suppliers as well as a prime contractor to the Department of Defense. The company primarily focuses on Defense but has a very small exposure to commercial aerospace.

{kind=link}

CPI Aerostructures is involved in a wide variety of programs. What is somewhat unfortunate is that the last time we were given a timeline for each or many of the programs was two years ago, but we do know that there are some programs that have significant revenue generation potential ahead such as some Lockheed Martin (LMT) programs, namely the F-16, F-35, CH-35K, and UH-60 Black Hawk. With the positive momentum in defense , one could think that CPI Aerostructures has a lot of growth ahead. The reality, however, is that the first big contract flows are expected in 2024 with deliveries in later years. For a company such as CPI Aerostructures that will mostly result in multi-year programs being stretched further and not necessarily in significant rate breaks that provide higher revenues from one day to the other. Apart from that some running programs are offsetting legacy program completion.

With that in mind, it is always good to see contracts such as the recently announced welded assembly valued at $3.6 million and a follow-on order to manufacture pod structures and air management system components for the LRIP phase 3 of NGJ-MB program with a maximum value of $32.6 million.

CPI Aerostructures Results Surge

{kind=link}

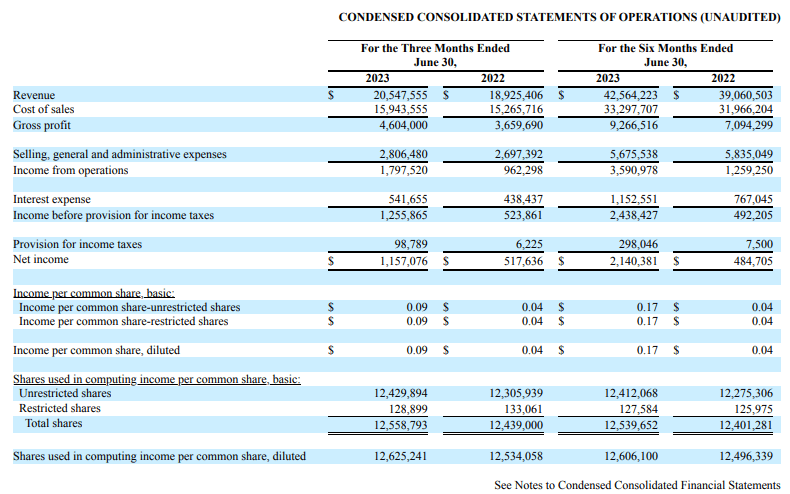

Year-over-year revenues increased by 8.5% to $20.55 million while gross profits increased by more than 25% to $4.6 million. The increase in sales was driven by higher revenues related to the Raytheon NGJ Pods and Raytheon B-52 Radar Racks. Net income more than doubled to $1.16 million. Revenues increased due to higher AeroSystems and Kitting and Supply Chain Management sales. The cost of sales increased by 4.4% driven by higher charges against the cost of sales, higher labor costs offset by lower material procurement and adjustment for the F-16 and Blackhawk.

Overall, the Q2 2023 results showed material improvement in profitability as the company saw favorable growth in revenues as compared to the growth in the cost items.

Outlook For CPI Aerostructures in 2023

For 2023, the company expects slightly higher revenues which doesn't fetch with the $116 million analyst estimate which would indicate a 40% jump in revenues. A recurring element seen in analyst estimates is that at times they do not at all reflect what the business is guiding for, which I think is problematic given the fact that many investors look at these estimates as a starting point when doing due diligence. For the six months ended, CPI has booked revenues of $42.5 million which does not at all indicate the analyst target will be reached. In fact, the Q2 revenues marked the second quarter of declining revenues for CPI.

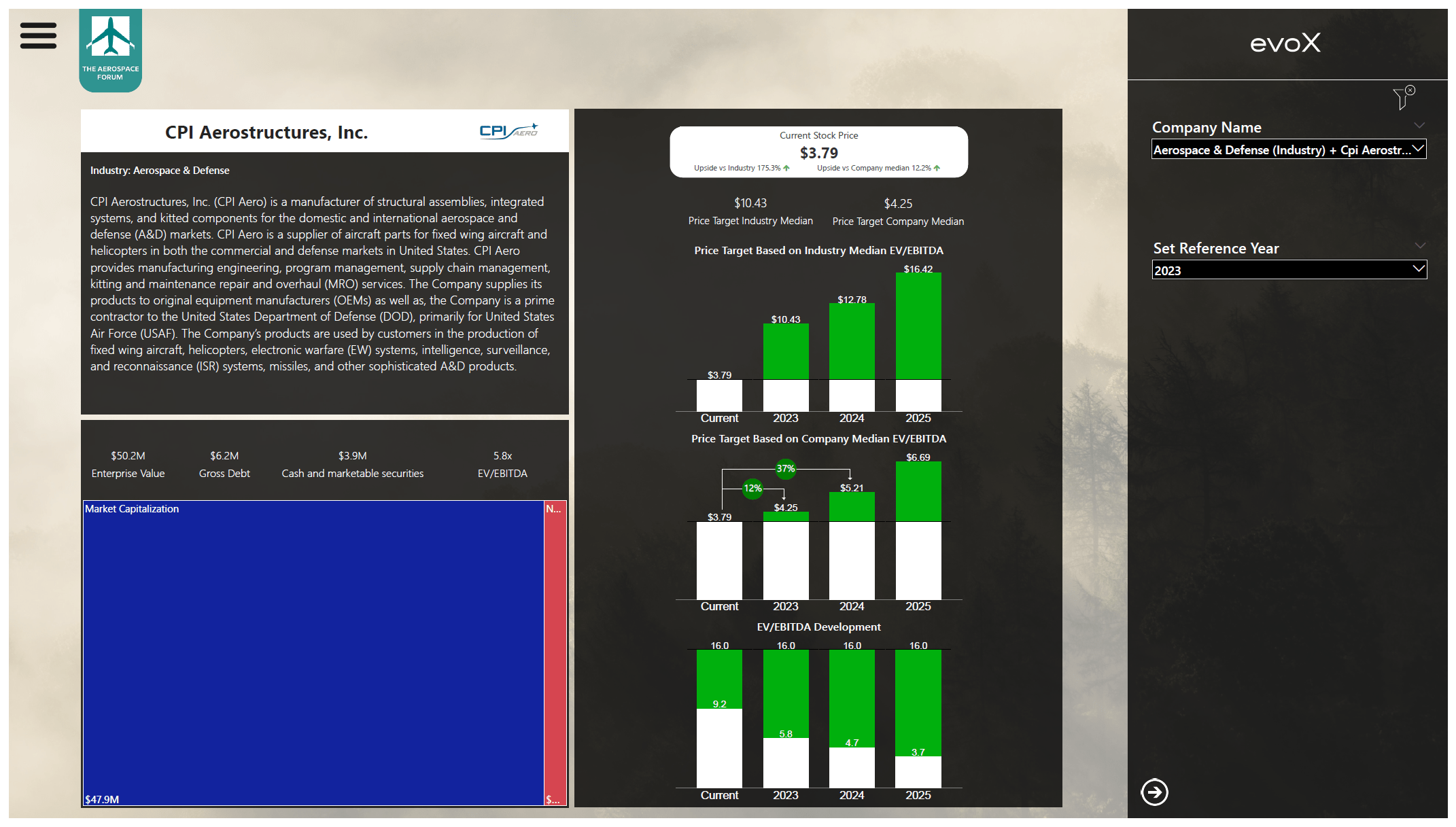

CPI Aerostructures: Hard To See Upside For The Stock

CPI Aerostructures stock price valuation using evoX Financial Analytics (The Aerospace Forum)

{kind=link}

When parsing the numbers for CPI Aerostructures, the upside for 2023 is limited but that is also because the stock has already gained over 15% year-to-date. One would think that it makes for a strong buy case but it should also be pointed out that the markets gained 14% year-to-date, so CPI Aerostructures is not an outperformer. With a market cap of less than $50 million, which is generally considered a higher risk, and the market performance I don't quite find the upside for the aerospace supplier extremely attractive. CPI Aerostructures is a smaller company that has performed in line with the market while I would say being a smaller aerospace supplier they are a higher-risk investment. That risk premium is not visible in the performance.

Separately, the company also identified a material weakness in internal control:

In addition, during the quarter ended June 30, 2023, management identified a deficiency that constituted another material weakness in our internal control over financial reporting as of June 30, 2023 (see Section below entitled "Changes in Internal Control over Financial Reporting". Based on management's evaluation of internal control over financial reporting for the twelve months ended December 31, 2022, and as of June 30, 2023, our disclosure controls and procedures were not effective as of June 30, 2023 due to the materials weaknesses described above.

CPI Aerostructures had issues with internal control before and was even on the verge of being delisted , so that doesn't help build a bullish thesis for the company either.

Conclusion: CPI Aerostructure Stock Is Still Not A Buy

As expected, we are seeing improved margins and nice growth in revenues. In my previous report, I saw 11% upside and the stock is up 7.9% since then. So, one could say that the company is filing the upside, and from current price levels, I see another 12% upside. However, that does not make CPI Aerostructures an extremely attractive name given the small size of the company, which could leave it vulnerable to pressure from big aerospace companies, and the company identified internal control weaknesses. Furthermore, the company provides extremely little information for investors and analysts which does not add to the appeal of the company. So, there is upside but it is not enough given the risk that this name also carries with it.

For further details see:

CPI Aerostructures: Don't Buy