AQUA - Crane Holdings Still Offers Upside

- Crane Holdings Co. has performed really well lately, driven by continued sales growth and rising net income.

- Some issues do exist, namely centered around other profitability metrics, but this doesn't change the investment thesis.

- On the whole, shares still look attractively priced and the company is worth some consideration.

Some investments take quite a while to pay off if they pay off at all. Others, meanwhile, can pay off rather quickly. One company that has performed incredibly well over the past couple of months, even compared to the broader market, has been Crane Holdings, Co. ( CR ). This firm, which focuses on the production of components and systems for the commercial aerospace, military aerospace, defense, and space markets, as well as producing high technology payment acceptance and dispensing products, bank notes, and other related offerings, has, in the light of mixed fundamental performance, fared surprisingly well. Shares of the company don't look quite as cheap as they were previously, they do look to be rather cheap on an absolute basis and relative to other firms. As such, I've decided to retain my ‘buy’ rating on the company for now.

Performance has been mixed but encouraging

Back in early June of this year, I wrote an article that took a bullish stance on Crane Holdings. In that article, I lauded the company for holding up well in what had been a volatile market. Its stability came at a time when revenue continued to grow but as its bottom line had been somewhat mixed. This was also coming off of a solid 2021 fiscal year and was in light of some major changes being made by management. On the whole, I had concluded then that the company made for an attractive ‘buy’ prospect based on its performance at the time. And since then, things have gone quite well. While the S&P 500 has risen by 3.1%, shares of Crane Holdings have generated a return for investors of 10.3%.

{kind=link}

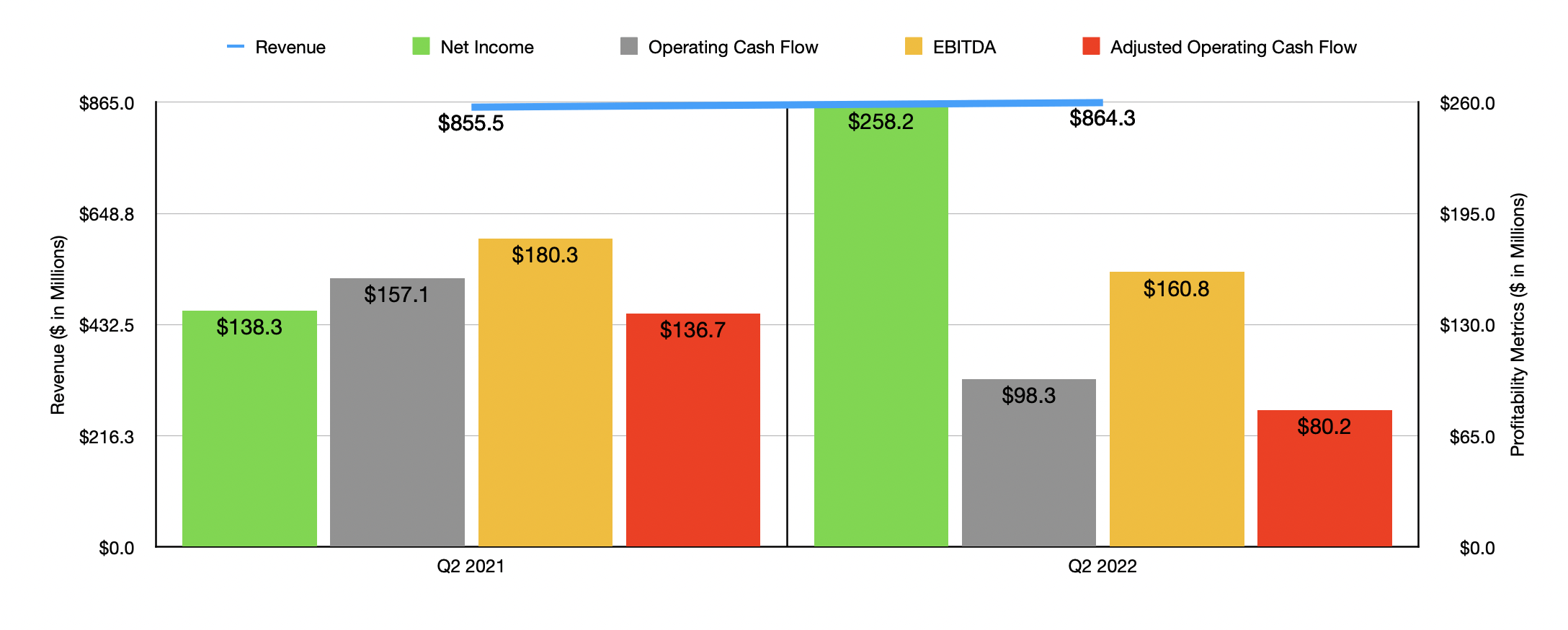

There is no denying that we are currently in precarious times. High inflation, rising interest rates, and the fear of a recession, have all impacted how individuals and companies alike spend their money. Even so, Crane Holdings has done quite well. To see what I mean, we need only look at the most recent financial performance provided by the business. This is the second quarter of its 2022 fiscal year. This is the only quarter for which I did not have information on when I last wrote about the company. During that latest quarter, revenue came in at $864.3 million. That's 1% higher than the $855.5 million generated the same quarter last year.

{kind=link}

Though this may not sound impressive, it is worth noting that management beat expectations set by analysts to the tune of $43.2 million. No matter how you stack it, that's a nice victory. Management attributed this increase in revenue to a 60.3% rise in core sales for the business. It's incredibly important to point out that not only did the company suffer from a $21.8 million hole associated with its sale of Crane Supply, it also has hit to the tune of $29.7 million as a result of foreign currency translation. Analysts certainly would have factored in the divestiture. So when you consider how the company did on a constant currency basis, it could be argued that performance was very strong.

Profitability, meanwhile, was somewhat more mixed. Net income in the quarter came in at $258.2 million. That's nearly double the $138.3 million generated the same time one year earlier. Of course, it should be said that the business benefited to the tune of $228.7 million for may gain on the sale of Crane Supply. So without that, profitability would have been lower. For instance, excluding that and restructuring gains, operating profit actually fell from $144.8 million to $124.4 million. This came in part from a 2.3% increase in the cost of goods sold. Meanwhile, selling, general, and administrative expenses grew by 8.8%. Management attributed these increases mainly to higher material, labor, and manufacturing costs, as well as to higher selling costs and transaction-related expenses. Despite this weakness, adjusted earnings per share of $1.90 beat analysts' expectations by $0.09. This pain on the bottom line also extended into other profitability metrics. Operating cash flow fell from $157.1 million to $98.3 million. If we adjust for changes in working capital, it would have fallen from $136.7 million to $80.2 million. Meanwhile, EBITDA declined from $180.3 million to $160.8 million.

When it comes to the 2022 fiscal year as a whole, management expects earnings per share of between $9.80 and $10.20. This compares to the $6.80 to $7.20 previously anticipated. But if we adjust for one-time items, the guidance has remained flat at between $7.45 and $7.85. Based on the company's current share count, achieving the midpoint of this range would imply net income of $429.2 million. That's only marginally lower than the $435.4 million the company generated in 2021. No guidance was given when it came to other profitability metrics. But if we assume that they will change to the same rate that net earnings should, then we should anticipate adjusted operating cash flow of $430.8 million and EBITDA of $620.4 million.

{kind=link}

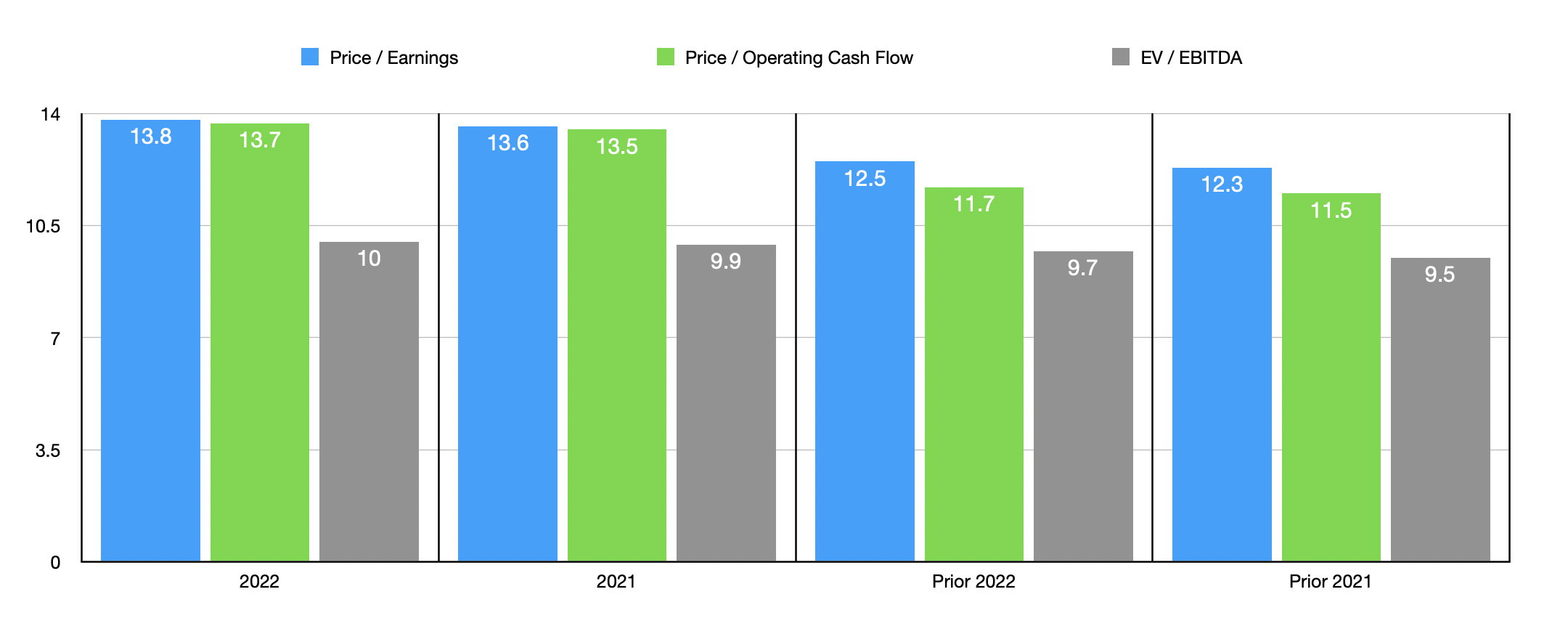

When it comes to valuing the company, the process is fairly straightforward. On a price-to-earnings basis, the firm is trading at a forward multiple of 13.8. This compares to the 13.6 reading that we get using 2021 results. The price to adjusted operating cash flow multiple should increase from 13.5 to 13.7. And the EV to EBITDA multiple should rise from 9.9 to 10. This pricing is, as you can see from the chart above, slightly higher than when I last wrote about the firm. But to put this all-in perspective, I also compared the company to five similar firms. On a price-to-earnings basis, these companies ranged from a low of 13.8 to a high of 86.3. Using the price to operating cash flow approach, the range is from 17.5 to 30.1. In both cases, Crane Holdings was the cheapest of the group. Meanwhile, using the EV to EBITDA approach, the range is from 9 to 23.4. Only one of the five firms was cheaper than our prospect.

| Company |

| Price / Earnings |

| Price / Operating Cash Flow |

| EV / EBITDA |

| Crane Holdings Co. |

| 13.6 |

| 13.5 |

| 9.9 |

| Watts Water Technologies ( WTS ) |

| 24.8 |

| 33.6 |

| 14.7 |

| The Timken Company ( TKR ) |

| 13.8 |

| 17.5 |

| 9.0 |

| ITT ( ITT ) |

| 20.8 |

| 24.8 |

| 13.2 |

| Evoqua Water Technologies ( AQUA ) |

| 86.3 |

| 30.1 |

| 23.4 |

| Donaldson Company ( DCI ) |

| 22.7 |

| 29.1 |

| 14.4 |

Takeaway

Based on all the data provided, it seems to me as though Crane Holdings is still doing well, especially considering that it is taking some hits on the bottom line. This is to be expected in the current environment. But it is still great to see revenue rise and shares were trading at low enough levels on both an absolute basis and relative to similar firms that the risk for investors moving forward looks fairly low. For all of these reasons, I've decided to retain my ‘buy’ rating on the company for now.

For further details see:

Crane Holdings Still Offers Upside