WEX - Crane NXT: Banking On A Fantastic Business Focused On Strong Growth

2023-04-09 08:52:52 ET

Summary

- Crane NXT was recently spun off from its parent company, Crane Company, as a standalone cash/payments business.

- Although growth wasn't the best in recent years, management has fuel to grow the company moving forward.

- Add on top of this, certain catalysts and a low share price, and it definitely warrants consideration.

April 3rd was a big day for shareholders of Crane Company ( CR ). This is because, after more than a year of working toward it, the company finally shed off its industrial technology operations into a separate company called Crane NXT ( CXT ). This tax-free spinoff of stock to shareholders of Crane Company might be confusing to some investors. But at the end of the day, the ultimate goal here is to create additional value for shareholders in the long run. Based on the plans currently laid out by the management team at Crane NXT, value creation moving forward could be significant. Shares of the enterprise look to be quite cheap at this moment, and the growth potential and capacity of the business over the next few years can create significant upside. All things considered, I do believe that Crane NXT warrants a ‘strong buy' rating at this time.

A niche business

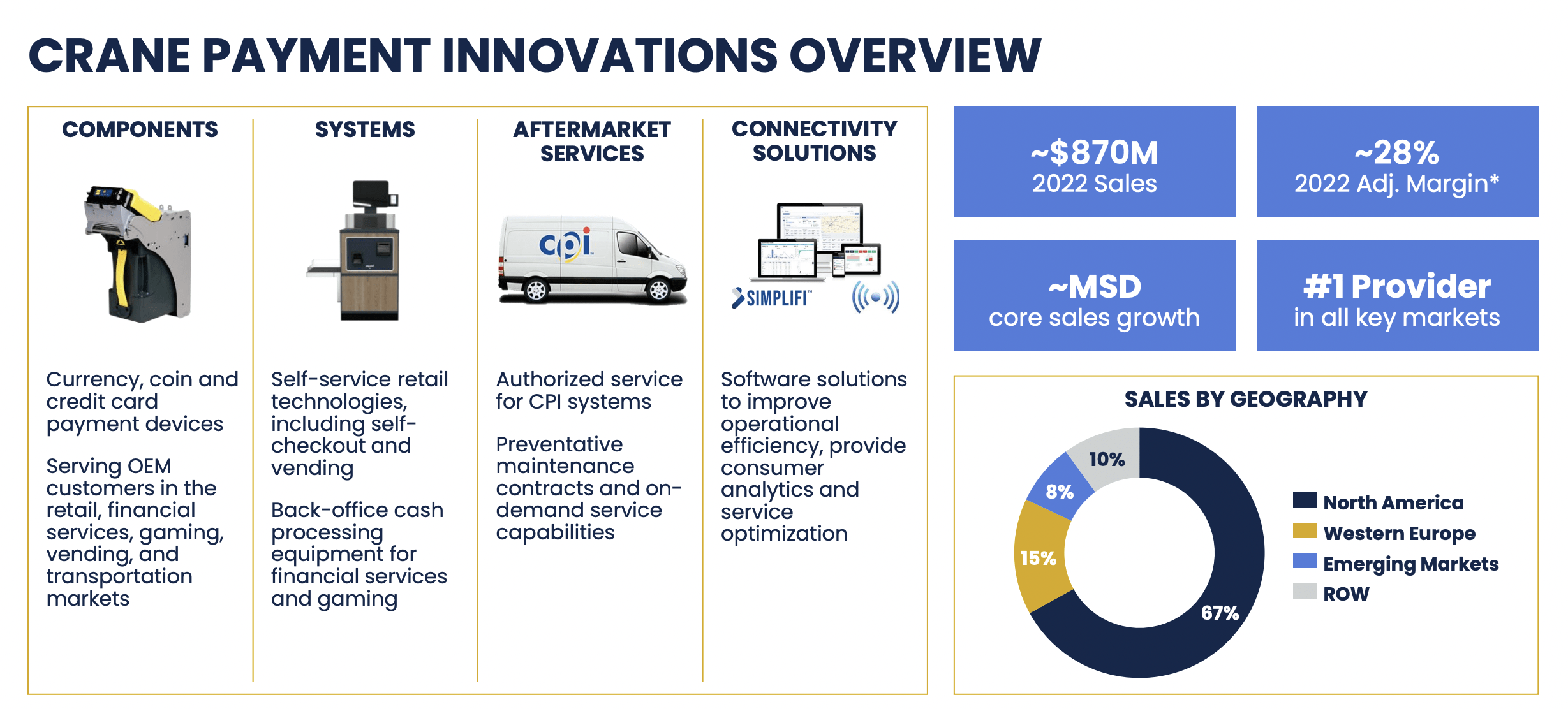

Back in March of last year, news broke that Crane Company was splitting up into two separate companies. The smaller and, to me, more interesting, of the businesses was Crane NXT. To truly understand the company, it would be wise to break it up into its individual operations. Operationally speaking , the firm has two different segments. The first of these is Crane Payment Innovations, which makes up around 65% of the firm's revenue. Through this unit, the company provides technology solutions that aid in Detecting and authenticating payment transactions.

{kind=link}

Examples of the products that the company provides include currency, coin, and credit card payment devices. The firm sells these directly to OEM customers across all sorts of industries from gaming, to financial services, to retail, and more. The firm is also responsible for producing and selling self-service retail technologies like self-checkout and vending devices. It produces back-office cash processing equipment as well. Outside of the device and systems categories, the firm also offers customers aftermarket services like preventative maintenance contracts and on-demand repairs. There also exists a software component of this that includes solutions like consumer analytics and service optimization features.

In terms of customer concentration, it's worth noting that about 30% of sales come from the vending category. A close second is gaming at 26%, followed by retail at 20%. The customers the company serves have often been with it for a long time. In fact, the average tenure of its 20 largest customers for this segment is 28 years. As you might expect, this unit is largely focused on sales across North America. 67% of its overall revenue comes from here at home. Western Europe, meanwhile, accounts for another 15% of sales, while emerging markets comprise 8%. Although this is a global market, the addressable market’s size is not as large as you might expect. Management pegged the space as being worth about $4 billion in 2022. By 2027, it should grow to about $4.7 billion, implying an annualized growth rate of 3.3%.

{kind=link}

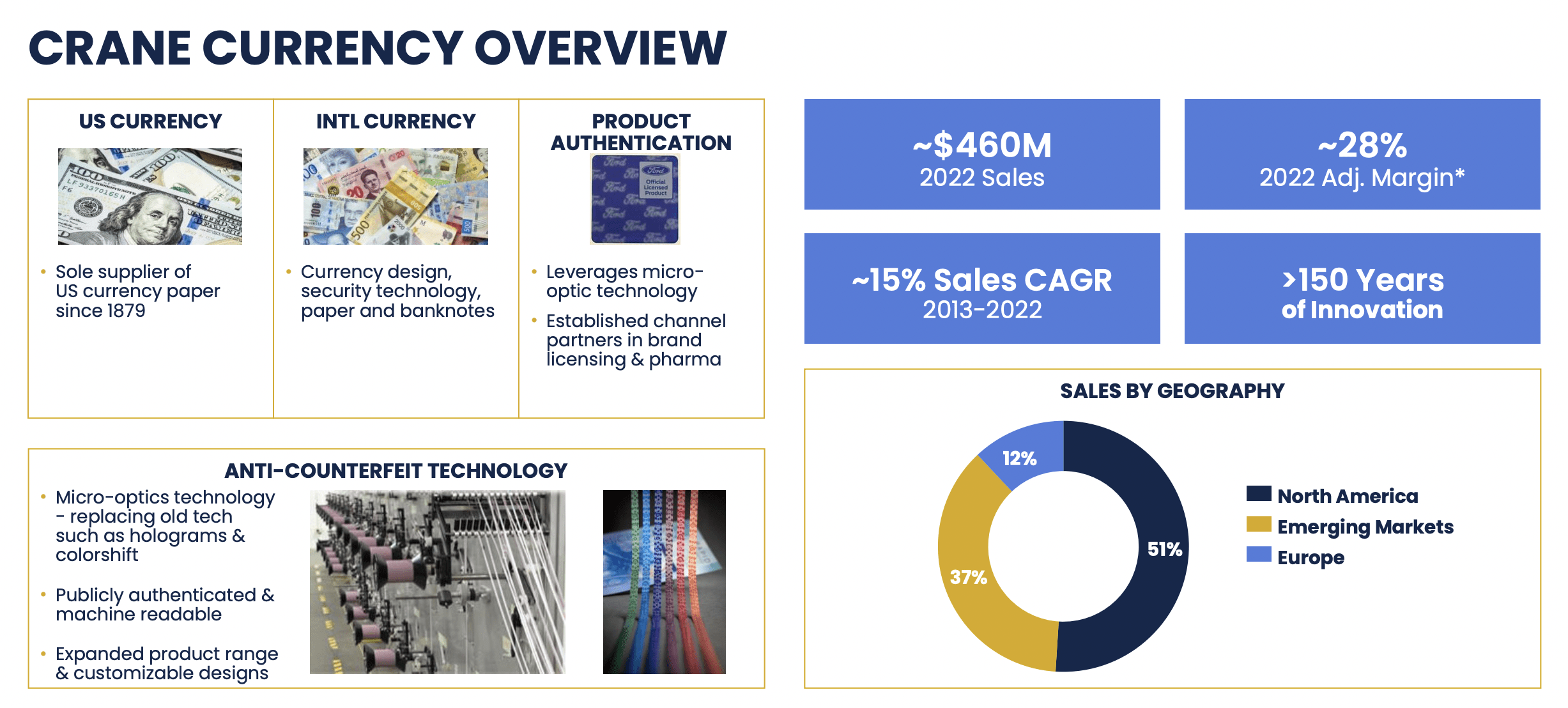

The more interesting side of the business, to me at least, is what management calls Crane Currency. This makes up the other 35% of revenue for the enterprise and it involves the use of technology in securing and authenticating banknotes. The company has had a very loyal customer base. In fact, it has served as the sole supplier of US currency paper since 1879. When working with international clients, it aids in currency design, as well as its other core services. And some of this technology even includes things like micro-optic solutions that the company has also expanded into other categories like brand licensing and pharmaceuticals. Naturally, the company's micro-optics technology is incredibly useful when it comes to anti-counterfeiting activities.

Using data from the 2022 fiscal year, about 51% of the $460 million that this unit generated came from customers throughout North America. Surprisingly, Europe made up only 12% of sales. The remaining 37%, which I believe is an impressively high number, came from emerging markets. Though this does make sense when you consider that emerging markets would be more likely to rely on paper money and that counterfeiting would be more achievable when governments lack the resources to combat it or address it.

{kind=link}

{kind=link}

{kind=link}

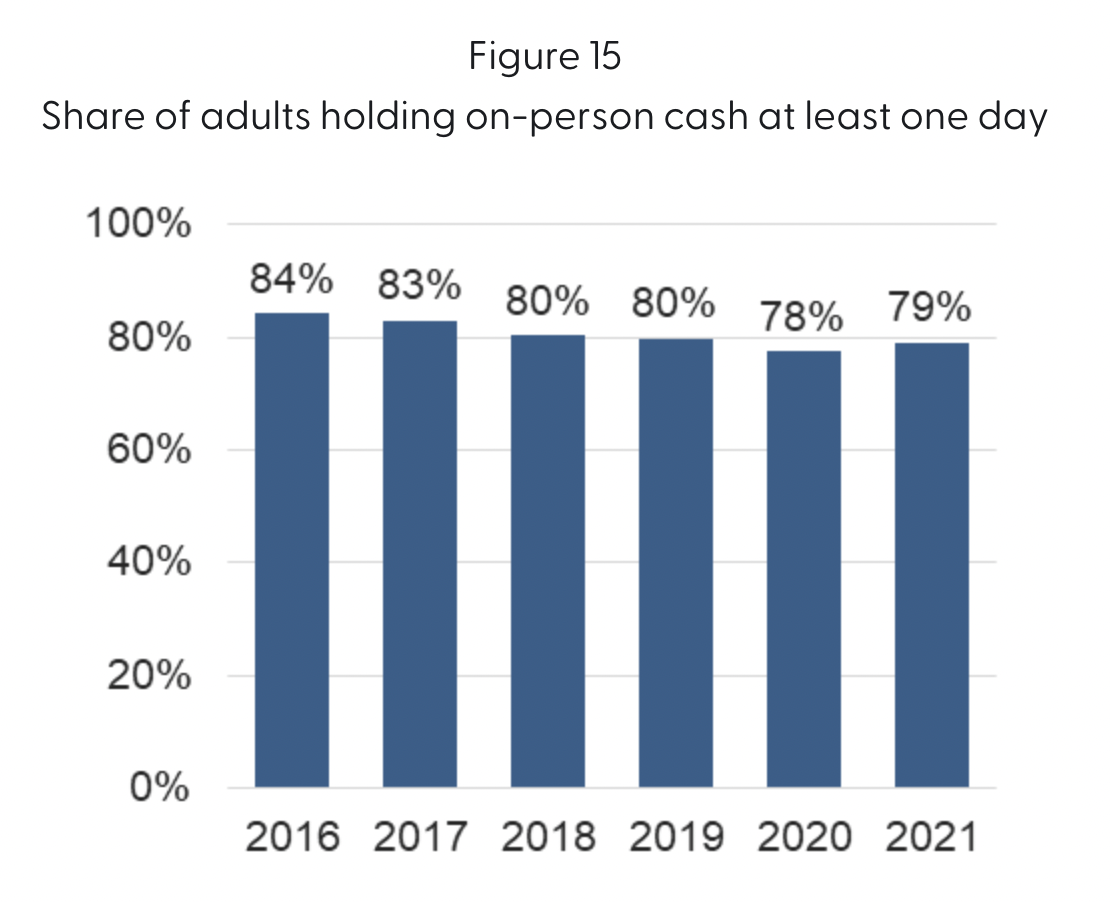

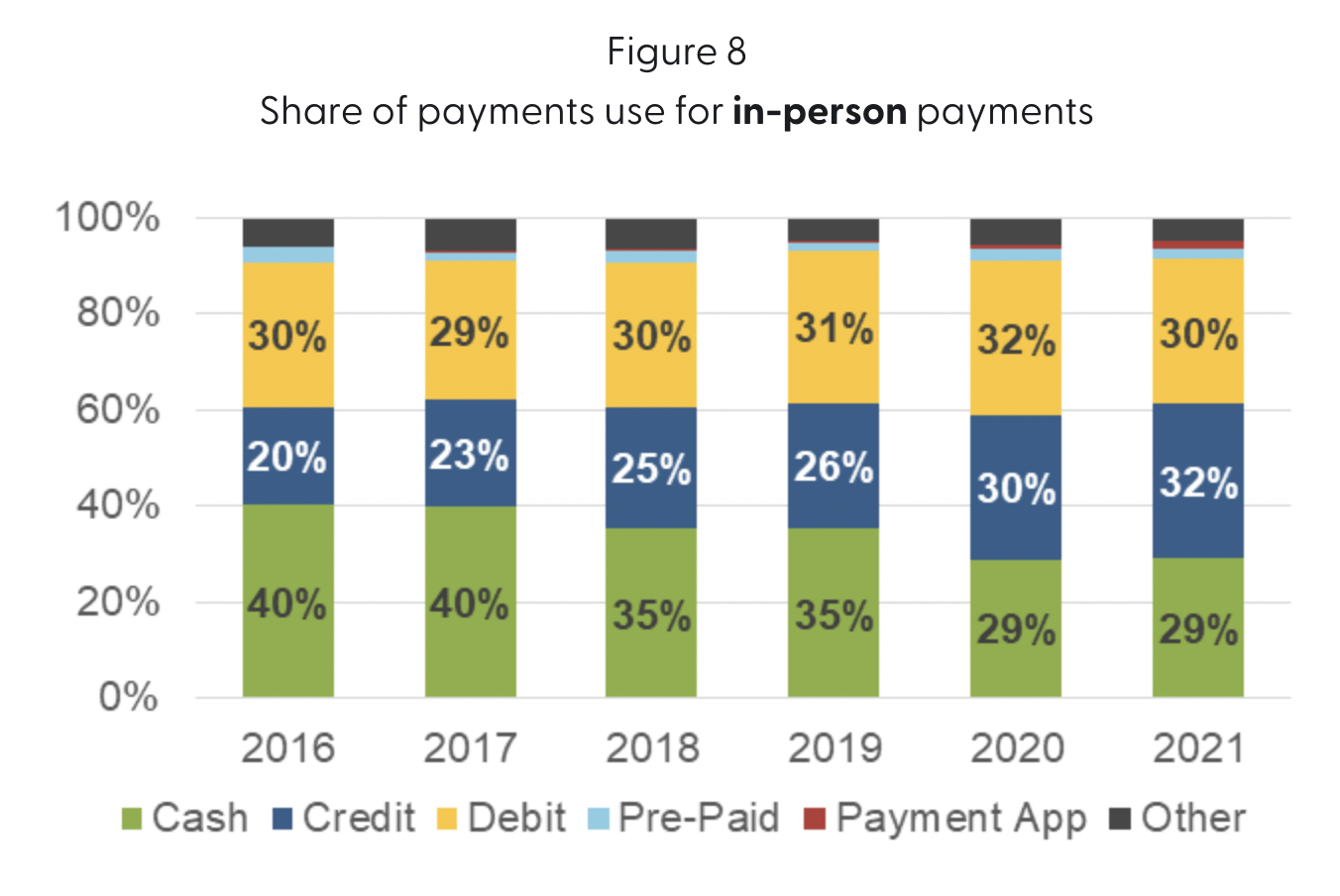

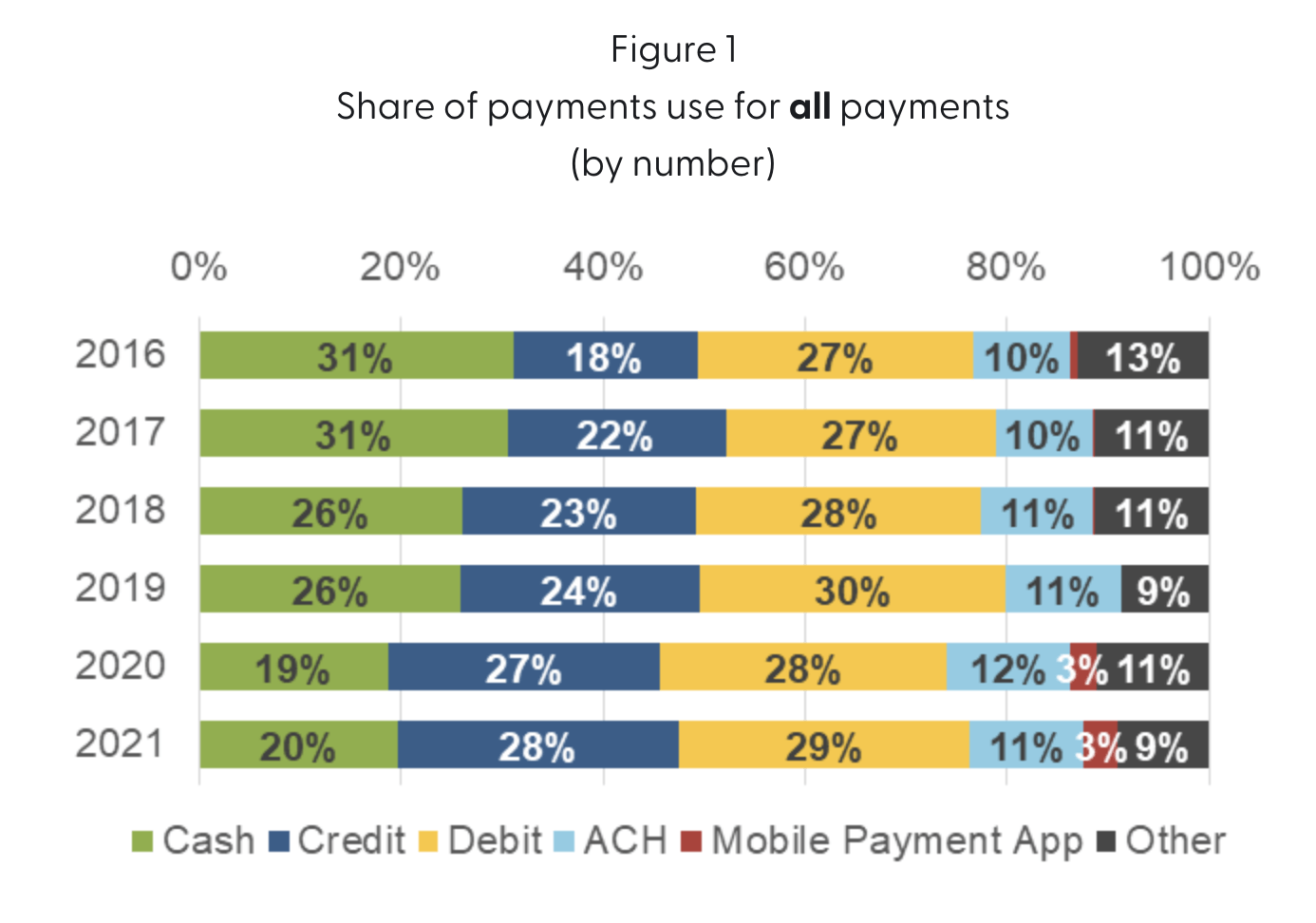

Those who don't like a company like this may point out the cash seems to be dying. There is some truth to this when you look at it from a per capita basis. For starters, back in 2016, 84% of adults in the US carried cash on them. That number fell to 79% by 2021. From 2019 through 2021, we saw cash go from accounting for 61% of the value of all in-person payments down to 49%. It is very likely that the COVID-19 pandemic played some role in this decline. But with mobile apps growing from 11% to 29%, and such apps likely to stick around because of the convenience they offer, it's possible that the effects of the pandemic were permanent. For all payments, by the way, we went from seeing 26% market share, by number of payments, not payment share, being in the form of cash in 2019, down to 20% in 2021.

{kind=link}

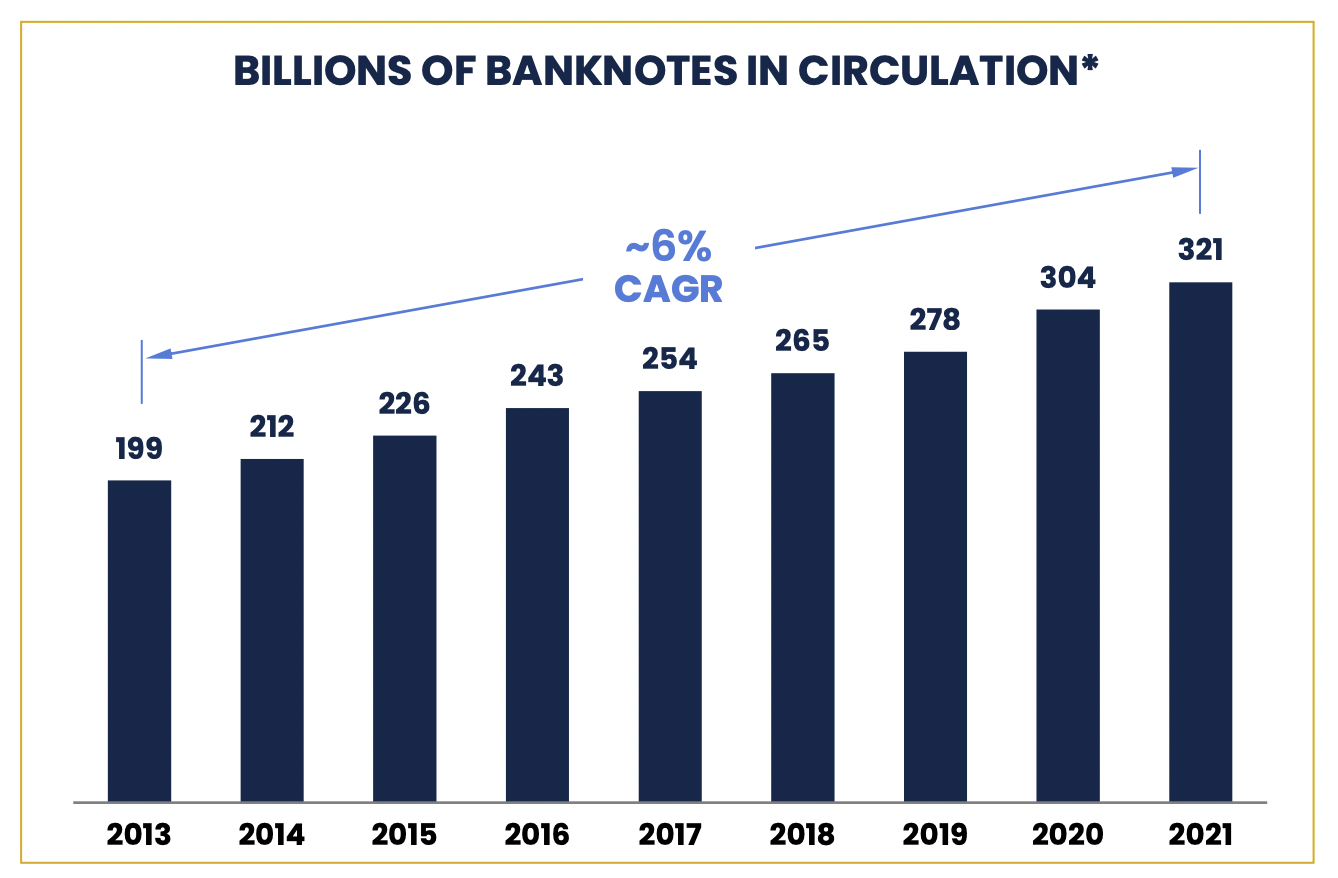

This may seem like a major turn-off for prospective investors. But when you look at the overall number of banknotes in circulation, it's clear that cash is not going away anytime soon. About 321 billion banknotes were in circulation in 2021. That's up from 199 billion in 2013 and it translates to an annualized growth rate of around 6%. Even from 2020 to 2021, the growth was nearly 6%. In addition to this, management believes that the continued evolution of paper money will further guarantee demand for its services. For instance, in 2026, the new series for the $10 bill in the US is expected to launch. This would be followed up by the $50 bill two years later, the $20 bill two years after that, the $5 bill two years later, and the $100 bill in 2034.

{kind=link}

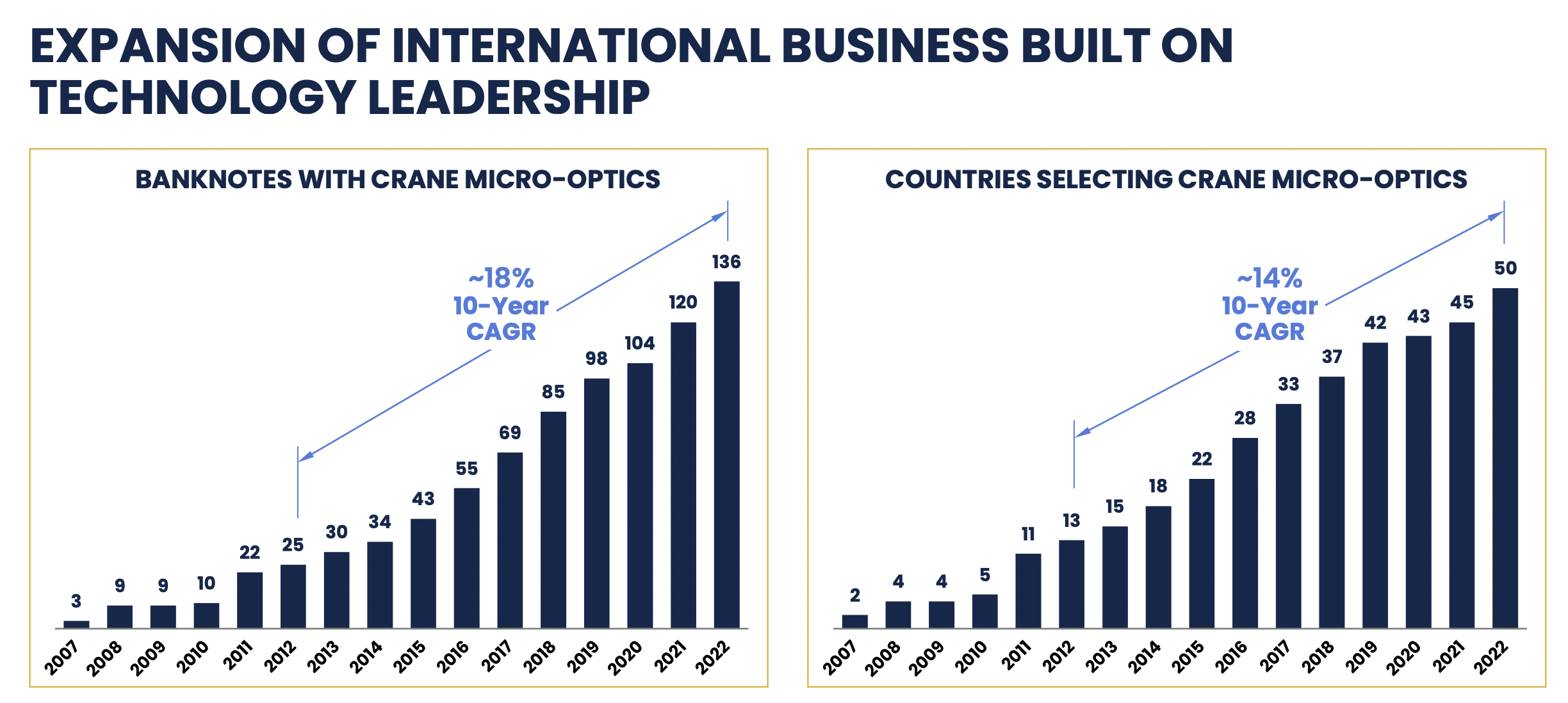

In addition to providing its customers with its traditional offerings such as motion surface polymer and other offerings, the firm will be stressing the use of its micro-optic technologies to further reduce the risk of counterfeiting. This has become very valuable on the international stage. From 2012 through 2022, the number of banknotes globally that had Crane’s micro-optics offerings in them jumped from 25 billion to 136 billion, translating to an 18% annualized growth rate. As of 2022, 50 different countries were using this offering, up from 13 a decade earlier.

{kind=link}

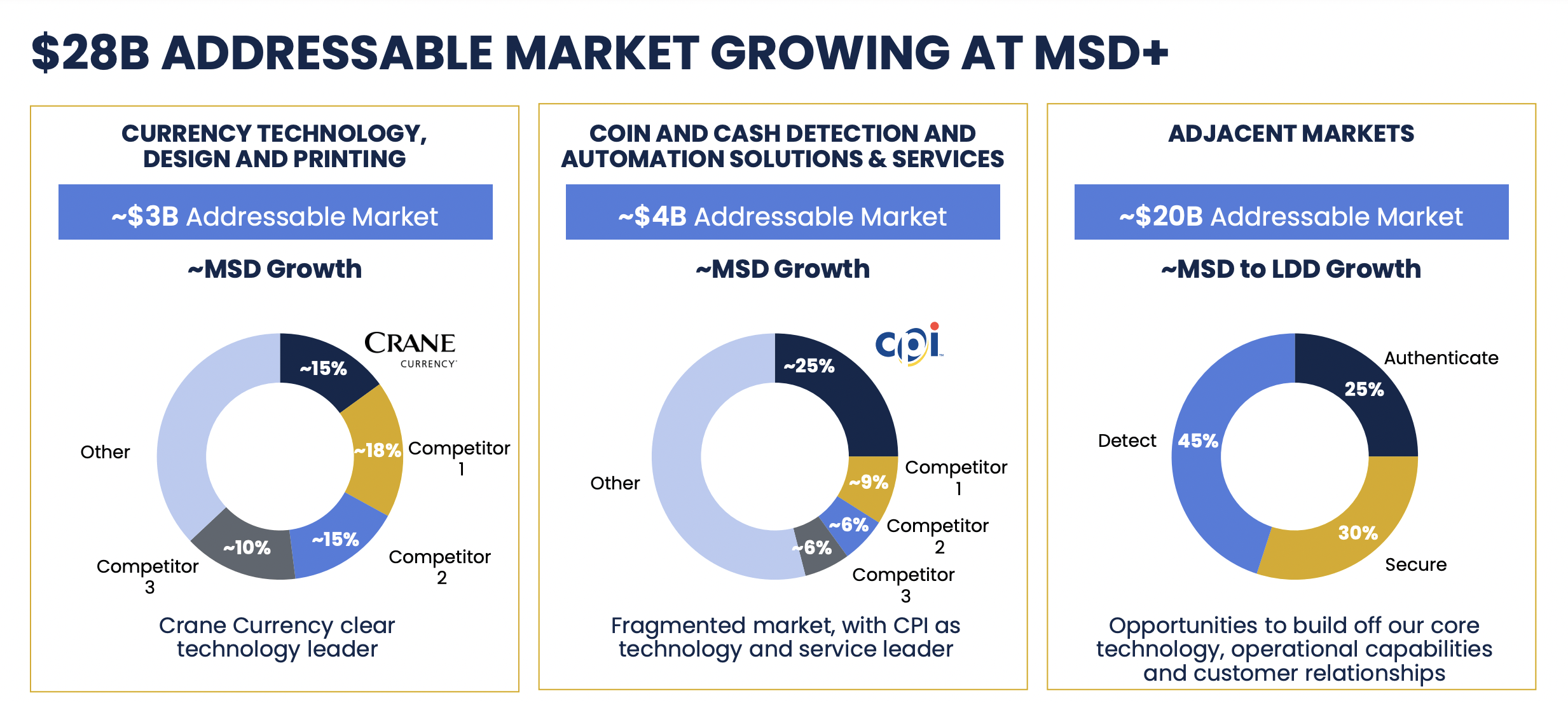

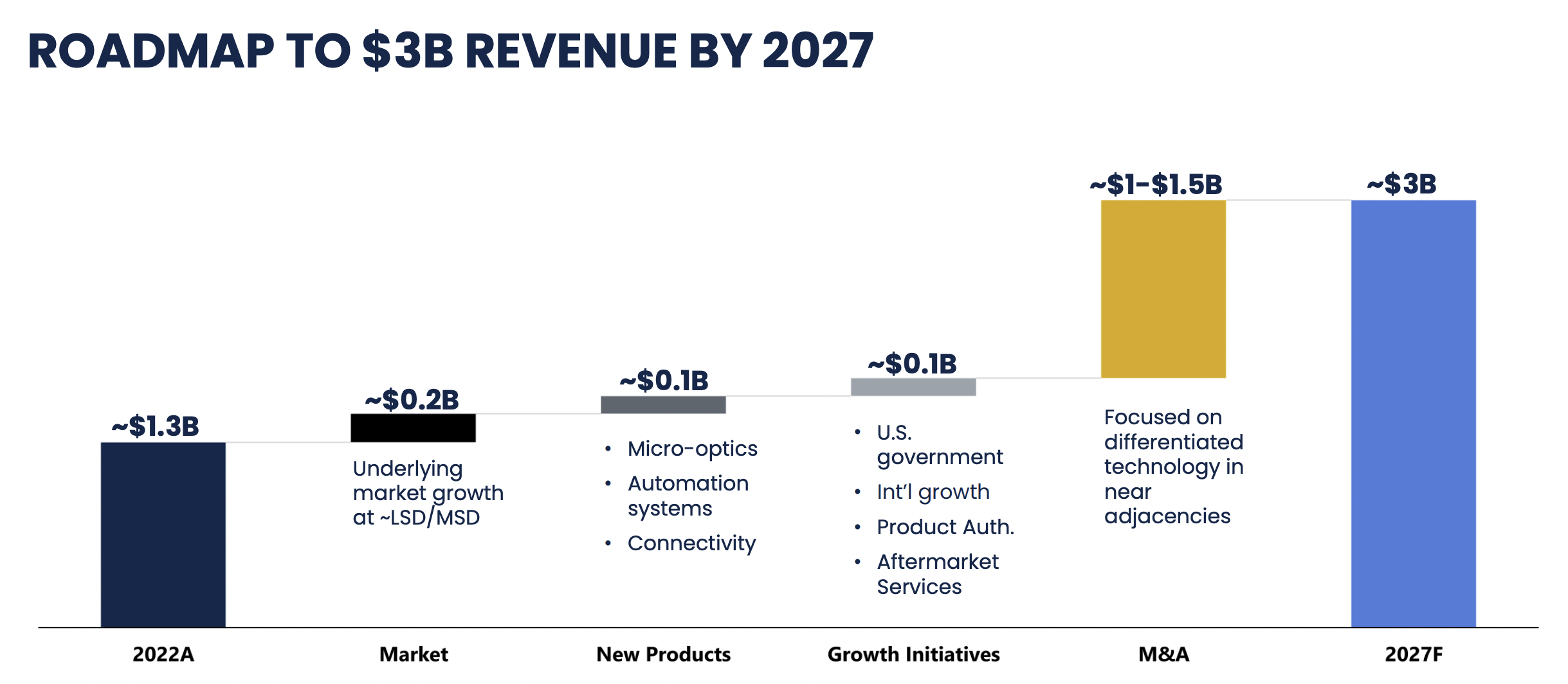

Management also wants to use the technologies that the company owns and continues to innovate on to grow into other markets. For instance, the product authentication market is estimated to be worth around $1 billion. This is a nice additional market to the $7 billion core market opportunities that the company is already focused on. However, the company is focusing on other spaces as well. There's a roughly $6 billion market opportunity that management has classified as ‘secure’. This includes access controls and payment verification, including things like biometrics. There's a $10 billion ‘detect’ market that consists of industrial detection and sensing systems. And there's a $5 billion ‘authentication’ market that involves physical security technology and online authentication such as track and trace features. From 2023 through 2027, management hopes to allocate up to $3.4 billion between growth initiatives and rewarding shareholders. 89% of this, for roughly $3 billion, is likely to go into mergers and acquisitions activities. The ultimate goal here is to grow revenue from the $1.34 billion that the business generated in 2022 to roughly $3 billion by 2027. Between $1 billion and $1.5 billion of growth is expected to come from the aforementioned mergers and acquisitions activities that the company is interested in pursuing.

{kind=link}

In terms of overall financial health, the picture for the business is quite solid. As part of the separation from Crane Company, the firm received a $275 million dividend from its parent and allocated that toward debt reduction. Overall debt right now, on a net basis, is about $650 million. When it comes to the 2023 fiscal year, management expects revenue to increase slightly to $1.36 billion. They are forecasting net income of about $218 million, operating cash flow of $263 million, and EBITDA of $364 million.

Author - SEC EDGAR Data

{kind=link}

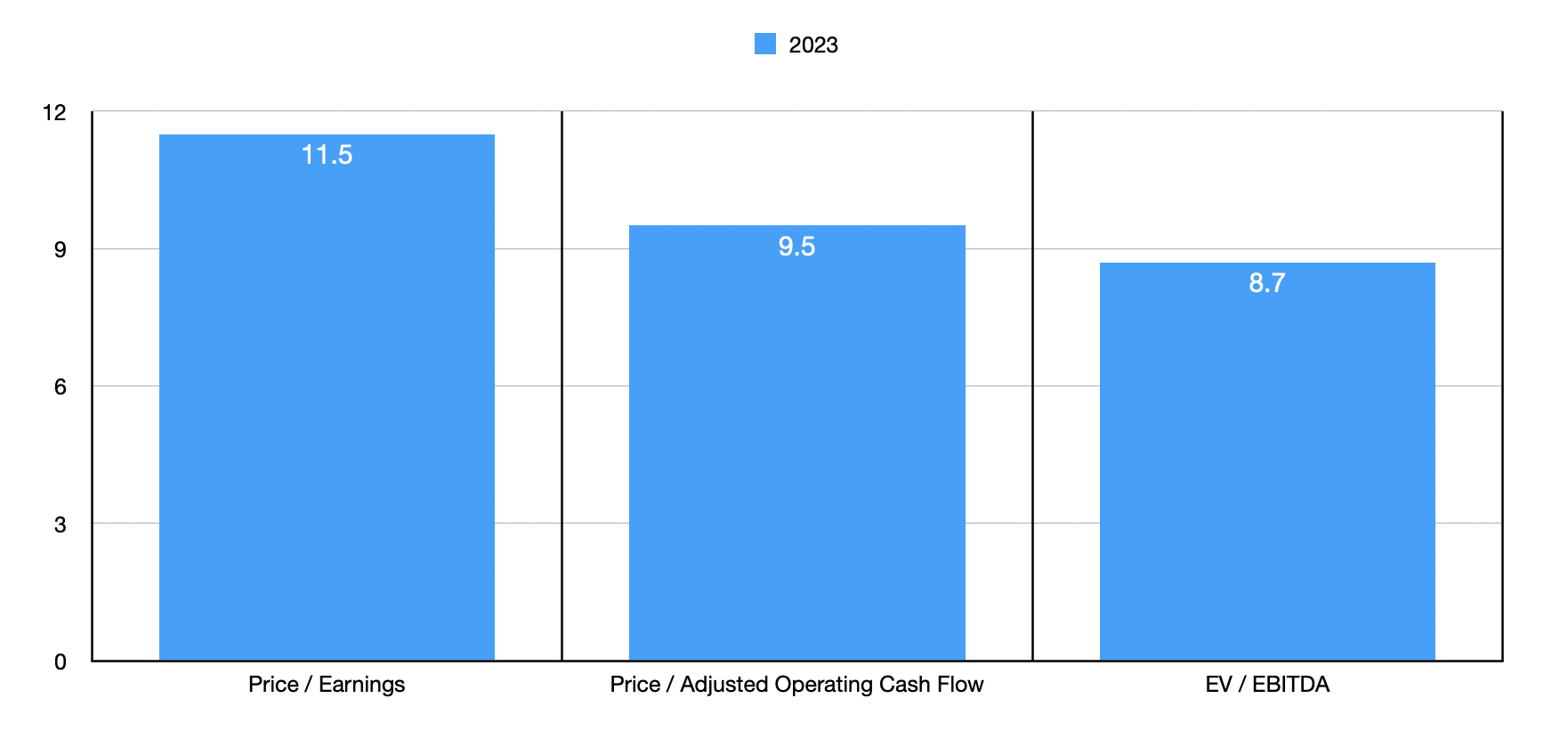

Based on these figures, and where shares are at the moment, the company is trading at a forward price-to-earnings multiple of 11.5. The price to adjust and operating cash flow multiple is 9.5, while the EV to EBITDA multiple is even lower at 8.7. These numbers are quite low on an absolute basis. In terms of competitors, it really is difficult to find a good spot for the business. In an investor presentation that the company gave shortly before the separation was finalized, it compared itself to these small and medium industrial technology space. The EV to EBITDA multiple of these companies came out to about 12.7. That would indicate a great deal of upside. Although certainly not a perfect comparable by any means, it might be the best that we have to work with. Although I did decide, as part of my analysis, to compare the company to other payment services firms. These results can be seen in the table below. Using both the price-to-earnings approach and the EV to EBITDA approach, we can see that Crane NXT is the cheapest of the group. Meanwhile, using the price to operating cash flow approach, only one of the five firms was cheaper than our target. But just like how I am hesitant to agree with management that the company belongs in the industrial technology space, I am also hesitant to say that it belongs comfortably in this niche.

| Company |

| Price / Earnings |

| Price / Operating Cash Flow |

| EV / EBITDA |

| Crane NXT |

| 11.5 |

| 9.5 |

| 8.7 |

| Global Payments ( GPN ) |

| 238.9 |

| 12.9 |

| 17.2 |

| WEX Inc. ( WEX ) |

| 40.0 |

| 11.8 |

| 12.5 |

| Fidelity National Information Services ( FIS ) |

| 44.4 |

| 8.5 |

| 10.5 |

| Jack Henry & Associates ( JKHY ) |

| 30.8 |

| 21.8 |

| 17.1 |

| Toast ( TOST ) |

| 65.2 |

| 19.6 |

| 19.2 |

Takeaway

All things considered right now, Crane NXT is doing quite well for itself. Although the company has only just separated from its prior parent, it seems to be starting off on solid footing. It has a tremendous capacity for growth and the desire to achieve that growth. Shares are trading on the cheap at this moment, both on an absolute basis and relative to other companies that have similarities to it. And it has a history of working with long-tenured customers that are unlikely to leave it anytime soon. Given all of these factors, I do believe that the company makes for a ‘strong buy’ prospect at this time.

For further details see:

Crane NXT: Banking On A Fantastic Business Focused On Strong Growth