BAP - Credicorp: Looking Through The Near-Term Headwinds

2023-11-30 07:52:33 ET

Summary

- Credicorp is going through a bad patch right now, no thanks to a worse-than-expected El Nino.

- While near-term results will be impacted, the mid to long-term earnings growth potential remains intact.

- There's also plenty of capital buffer to withstand any asset quality issues ahead.

- At the currently discounted valuation, Credicorp stock is worth a look.

It's been a series of mixed quarters for Credicorp ( BAP ), the Peruvian holding company for some of the country's largest financial institutions, including Banco de Crédito del Perú (commercial bank), Grupo Pacífico (insurance company), and Prima AFP (asset management), among others. While the near-term outlook has materially worsened since I last covered the name, the key culprit is transitory weather headwinds underpinned by a worse-than-expected El Nino rather than anything structural. Still, the stock has sold off on the news, pricing in quite a bit of pessimism - despite the company remaining adequately capitalized to weather a downcycle.

More fundamentally, however, not a lot has changed for Credicorp – as the dominant financial player in Peru, the company is as well-positioned as ever to capitalize on an attractive long-term growth runway in its core businesses. There's optionality here as well, supported by management's track record of accretive capital deployment into fast-growing digital initiatives with clear paths to profitability (e.g., payment services platform Yape's 2024 breakeven target). Hence, the path is clear to sustaining more region-leading returns on equity going forward. Even weighed against some net interest margin compression from a Peruvian rate cut cycle, there's more than enough growth potential here to justify a re-rate from the current high-single-digits % earnings multiple (~1.2x book).

Searching for Silver Linings in the Latest Quarterly Reset

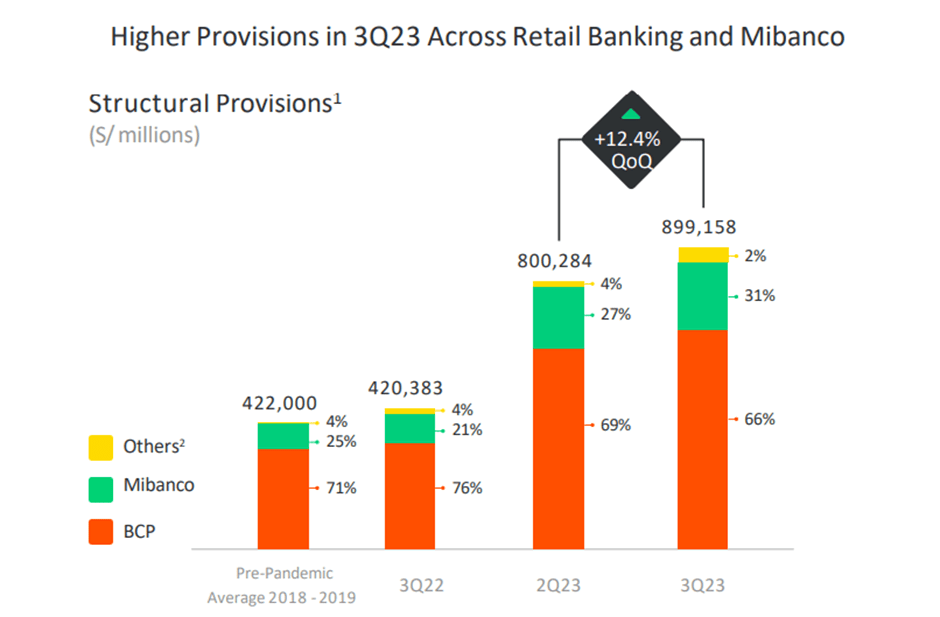

Credicorp's Q3 wasn't as bad as Q2, with investment income boosting the P&L despite higher funding costs weighing on net interest income. The pace of sequential provision growth, on the other hand, was a negative surprise amid weather-driven macro headwinds and notable defaults across the company's banking client base. As a result, management has increased its credit cost guidance to 2.6-2.9% (up from 2.1-2.5% previously), levels last seen during the worst of the COVID-impacted years. Similarly, Credicorp's all-important ROE metric was revised lower following a slight dip in Q3 (slightly below historical levels at ~16%). The lower 15.5% to 17.5% range implies a steeper dip in ROEs to 9-10% next quarter, though the delta is down to weather-related provisioning one-offs and a seasonal peak in expenses rather than anything structural.

{kind=link}

Credicorp

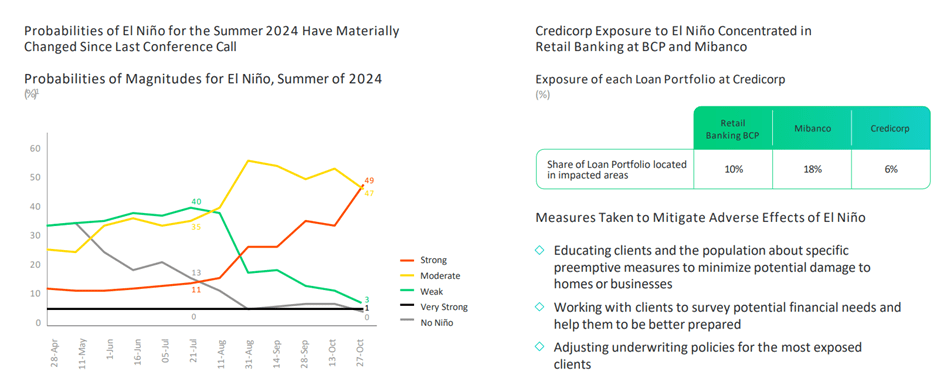

The qualitative readthrough from Credicorp's post-Q3 earnings call was surprisingly even more bearish, with management sounding more cautious than before on the severity of El Nino and its near-term impact on provisions and ROE. Per current forecasts, the timing of the weather headwind means earnings will be hit hardest in the back half of Q4 this year through Q1 2024, in line with management expectations for a flat GDP growth outcome this year. For investors with a longer-term horizon, on the other hand, the silver lining is that the bank now sees a path to stabilization and improvement in H2 2024. With the economic and loan growth bar (1-4% ex-Reactiva portfolio) also set fairly low, there's ample room for outperformance. Incremental growth optionality from new initiatives like Yape, now on track to break even by 2024, also poses additional upside from here.

{kind=link}

Credicorp

Resilient Capital Position; Allocation Strategy Intact

Even through this difficult period, Credicorp should have no issues maintaining its profitability and funding advantages; hence, management remains committed to its current pace of digital transformation investments. These include Peru's digital payment leader Yape (~9m active users), digital banks Tenpo and IO, as well as digital insurance platform Monokera, all of which add compelling new capabilities to the existing Credicorp platform. While many of these projects are cash burners today, the accelerated path to profitability, particularly for Yape, which is now on track to achieve cash breakeven by the end of 2024, is encouraging. Recent moves to break out these units and their key performance indicators, as well as specific disclosure of their spending requirements (currently up to $175m/year), also represent steps in the right direction.

{kind=link}

Credicorp

For now, though, management is erring on the side of caution by pausing capital returns to maintain a buffer. Hence, investors won't be getting an additional dividend this year – a disappointment, but not all that bad, given the company already paid out 43% of earnings earlier this year (equivalent to a ~5% dividend yield). To be clear, Credicorp's capital position is rock solid, evidenced by a healthy tier-1 ratio %; hence, I wouldn't be concerned about an adverse economic cycle or capital allocation constraints over the mid to long-term. Further helping are ongoing asset quality mitigation measures like more stringent loan origination for higher-risk segments, as well as efforts to work with clients to manage repayment risks ahead of the upcoming El Nino.

{kind=link}

Credicorp

Looking Through the Near-Term Headwinds

Credicorp may have posted another guidance downgrade in Q3, but the outperformance since then indicates the bad news is already in the price. Yes, weather-related headwinds from El Niño will weigh on asset quality and earnings for a few months, as reflected in the rebased ROE expectations for 2023 and H2 dividend pause. Yet, this ignores the many mitigations management has implemented over the last few months, as well as the group's strong capital buffers.

Over the long run, Credicorp is still the dominant player in a concentrated Peruvian financial system and boasts a funding cost advantage, as well as a strong track record of capital management, all of which underpin its best-in-class returns on equity. As the best-positioned platform to track not only a fast-growing conventional financial market but also digital services (Yape being a case in point), there's ample long-term earnings potential here. For a company capable of sustaining high-teens % ROE through the cycles, the current ~1.2x book valuation presents good value.

For further details see:

Credicorp: Looking Through The Near-Term Headwinds