BAP - Credicorp: Still Cheaply Priced Relative To Its Fundamentals

2023-08-02 11:17:23 ET

Summary

- Having successfully climbed a wall of worry this year, Credicorp’s management outlined a bullish mid-term outlook at its investor day.

- In addition to the strong core business fundamentals, digital initiatives like Yape are also set to contribute to the P&L.

- Owning Credicorp into a normalizing rate environment has its risks, but long-term investors willing to brave out the transition period could still come out ahead.

The political turbulence in Peru appears to have calmed down since I last covered Credicorp ( BAP ), supporting renewed optimism at its investor day event . On the agenda this year was a plan to ‘decouple from macro’ by investing in disruptive initiatives outside of the BAP core business, most notably its Yape digital payments platform. And with Yape already establishing a clear lead in Peruvian digital payments, monetization isn’t far away. In the near-term, operating leverage is poised to get Yape to its break-even target, while over the mid to long-term, incremental revenues from financial and non-financial products support significant growth optionality.

There are near-term hurdles to clear, though, with the core business set to be impacted by normalizing interest rates and inflation levels. Still, the strength of BAP’s domestic retail franchise should underpin a high-teens ROE through the cycles (low-20% mid-term ROE target for the core business). Hence, the current 1.3x fwd P/B valuation (~1.6x trailing P/B) seems reasonable, particularly after factoring in the optionality from BAP’s rich innovation pipeline.

New Mid to Long-Term Targets Highlight the Credicorp Ambition

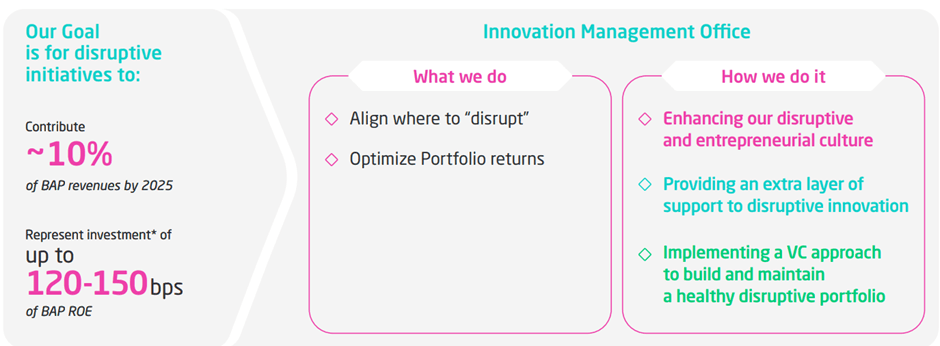

The Peruvian banking environment has improved significantly since the start of the year, and the renewed optimism was reflected in this year’s BAP investor day presentation. Chief among management’s priorities is to ‘decouple from macro’ – this means building a sustainably profitable business through the cycles with good visibility. One of the key levers here is investing in digital (Yape) and other disruptive initiatives - not surprising, given it has been a management focus area for a while now (recall last year's Digital Day ). What was a positive surprise, however, was the ~10% ‘disruptive’ revenue contribution target by 2025, as well as the scale of reinvestments at up to 300bps of cost-to-income and 150bps of ROE.

{kind=link}

Credicorp

As optimistic as the ‘disruptive’ target might seem, management has rightly added a big caveat to near-term results, guiding toward lower ROEs this year in line with the lowered GDP forecast due to El Niño. Management also referred to 2024 as a ‘transition year’ amid normalizing rates and inflation levels. So ahead of Q2 results next week, downside revisions may well be on the cards, particularly around GDP-linked assumptions like bad debt provisions and loan growth. The scale of the potential downside will depend on management’s updated interest rate assumptions – ‘higher for longer’ rate expectations, for instance, will provide some cushion to the near-term guidance (and vice versa).

{kind=link}

Credicorp

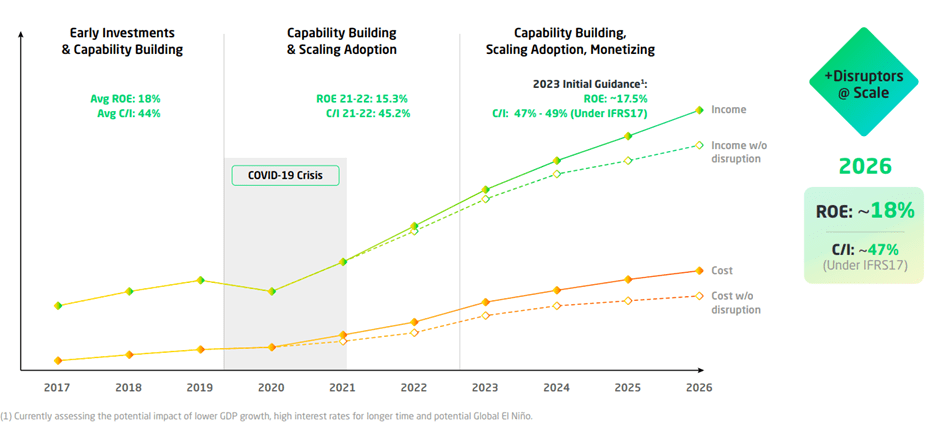

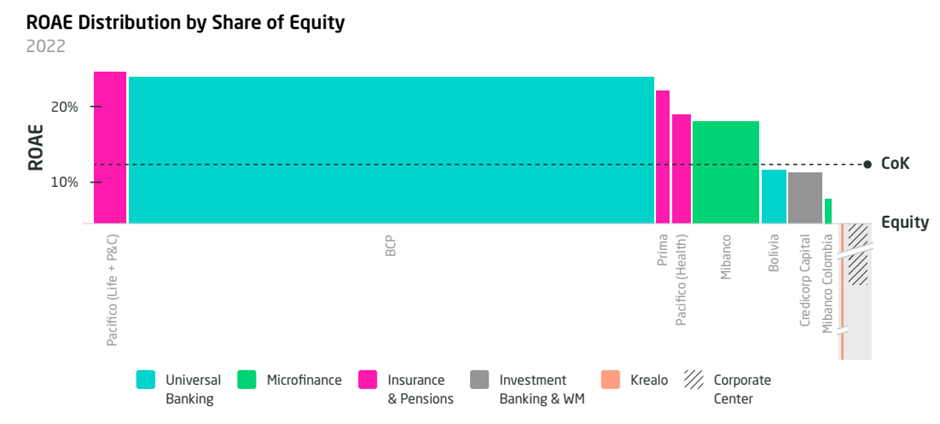

But over the mid-term, BAP has called for stable net interest margins (NIMs) at its core banking business (Banco de Crédito del Perú or ‘BCP’). While lower rates will pressure NIMs in the wrong direction, a mix shift towards retail and steady loan growth will provide more than enough tailwinds to offset the ROE impact, underpinning a solid low 20s target. On the microfinance side, MiBanco is also guided to contribute significantly to overall ROEs. The investment unit, Credicorp Capital, is set to generate solid ROEs in the high teens (in line with the group) - a testament to management’s shift in focus toward recurring businesses like wealth over the more volatile investment banking and capital markets divisions. Including Yape, this nets out to an 18% consolidated ROE for Credicorp by 2026 – impressive when you consider rates will be lower by then.

{kind=link}

Credicorp

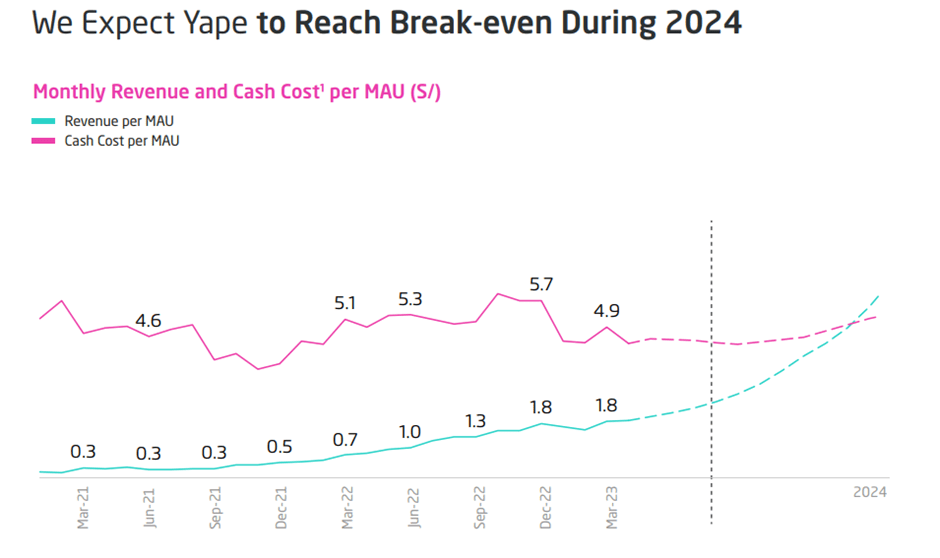

Yape Monetization Progressing Well, Inching Closer to Break-even

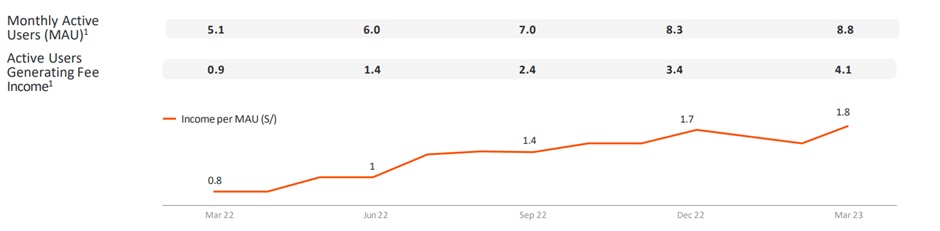

Zooming in, this year’s investor day presentation emphasized the potential of Yape as BAP’s next big growth driver. In an environment crowded with payment solutions, Yape stands out, given its already established active user base at ~9m (the largest by far in Peru) and with transactions in Q1 also running well above peers at 178m. Of the total user number, over 30% (or 3-3.5m users) are also new to the Credicorp ecosystem (i.e., no account at BCP), signaling Yape’s role in driving market share gains as well. And given the high unbanked population in Peru, the long-term goal of onboarding 6m users by 2025 seems well within reach (vs. the current 2.6m in the ‘financial inclusion’ category).

{kind=link}

Credicorp

Alongside growth, management is leaning on monetization levers as well. Firstly, via the Yape payment network’s operating leverage benefits from transaction volume (more than doubling every year) and the even faster-growing revenue-generating portion (triple the growth rate of total payment volumes). And following the successful rollouts of ‘proof of concepts’ like Yape promos (an in-app marketplace for products and services) and nano loans, Yape looks to be well on track to hit its 2024 break-even target. Importantly, incremental revenue per user will mean higher margins (even before accounting for efficiency opportunities), given ~50% of the cost base is already ‘semi-fixed.’ So with over ten products set to roll out in the next twelve months, the current break-even estimate (unchanged since last year’s digital-focused investor day) could even prove conservative. Key cross-selling opportunities to look out for include increased product sales from other business lines, such as wealth management (Credicorp Capital) and insurance (Pacifico).

{kind=link}

Credicorp

Still Cheaply Priced Relative to its Fundamentals

This year’s investor day reaffirmed the mid to long-term Credicorp path, as management looks to create a less cyclical business by leveraging its digital pipeline. Its most notable product is digital payments leader, Yape, which looks poised to transition into a ‘super-app’ platform offering both financial and non-financial services and products; success here bodes well for future revisions to BAP’s relatively conservative long-term estimates. That said, the H2 2023/2024 transition period, when Peru will inevitably see a normalization of peak interest rates, poses downside to near-term ROEs. Given its industry-leading funding advantage via a highly ‘sticky’ retail deposit base, though, BAP could surprise to the upside here.

While some of the positives have been priced in at the current ~1.3x fwd P/B (~1.6x trailing), the valuation remains undemanding relative to the low 20s ROE potential for the core businesses (high teens including digital). And with compelling growth optionality from its Yape-led innovation pipeline, there’s still plenty to like here for long-term-oriented investors.

For further details see:

Credicorp: Still Cheaply Priced Relative To Its Fundamentals