CACC - Credit Acceptance: Subprime Trouble Ahead

Summary

- Credit Acceptance has shown strong performance in the past decade but with worsening economic conditions, its business model is under threat.

- The subprime lending industry as a whole may suffer as US consumer credit reaches all-time highs alongside lower savings rates.

- In the short term, Credit Acceptance might struggle to sustain earnings as consumers struggle with rising interest rates and inflation.

- A heavy debt burden may cause the stock to fall as interest expenses rise and cash flow fails to keep up.

In the event of a recession, credit underperforms as default rates rise with subprime lenders being the most vulnerable. Credit Acceptance ( CACC ) is one stock which we believe will suffer in worsening economic conditions after years of increasing leverage combined with riskier and riskier loans. In the short term, we anticipate a repricing to the downside, with a potential for a much larger decline or even the risk of bankruptcy over longer time horizons, depending on the state of the US economy.

Lender of last resort

Credit Acceptance provides loan services for a large network of auto dealers across the US, enabling them to offer financing to customers with low or no credit score. As compensation for the elevated risk of default inherent in subprime lending, CACC charges an average 22% rate on loans.

Their novel lending model consists of two main segments: the Portfolio Program and the Purchase Program, the former accounting for 65% of company revenue. In the Portfolio Program, dealers receive a down payment from the customer and a cash advance from CACC, ensuring that the dealer makes a minimum profit on a sale. Loans are bundled into pools for each dealer and CACC will collect on these pools until advances have been recovered, after which time remaining payments will go to the dealer, minus collection costs and service fees charged by CACC. The Purchase Program is different in that the dealer receives a one-time payment from CACC to purchase the loan at origination.

At first look, the financials look solid with growing revenues (8 year CAGR of 13.4%), healthy stable margins (8-year average gross margin of 76.7%) and a consistently high ROIC in the double digits. Not only that but management has signaled to the market that they think the stock is undervalued, with almost $2B in share repurchases in 2021 and 2022.

Cracks begin to show

Dig a little deeper and several red flags become apparent. Firstly, the vast majority of assets (92%) are made up of loans receivable, which makes sense due to nature of the business mode but creates a concentrated risk if there is a significant shock to the ability to collect on these loans. Debt has also been trending higher, growing from just $1B in 2013 to $4.63B in Q3 2022, with the interest rates increasing rapidly in past year, making the variable portion of debt more expensive. This is a key concern with respect to the solvency of the stock and in Q4 2022, CACC took measures to address this risk by wrapping loans in SPEs and selling them for a fraction of the value, raising $390M at a cost of 8.5% and a further $200M at SOFR + 2.35% (currently 6.35%), in order to keep on top of debt repayments. According to Moody's, CACC carries a credit rating of Ba3 indicating "substantial credit risk" and only one notch away from "high credit risk," so this strategy is a cheaper alternative to issuing bonds. However, it is clearly unsustainable in the long term unless economic conditions drastically improve.

Looking at the income statement, we can see that net income has been negatively impacted by large increases in credit loss provisions under CECL since 2020 when the new accounting rules came into effect. This will continue to hurt reported profitability going forward and FY22 is looking to be another down year comparable to FY20. We can also see that revenue growth appears to have stalled for the first time in the last decade going into earnings on Tuesday. This is most likely due to rapidly rising car prices discouraging new purchases and after enjoying a decade of rapid growth, CACC may be approaching market saturation as highlighted by the need to make their loans more affordable over time in order to sustain growth.

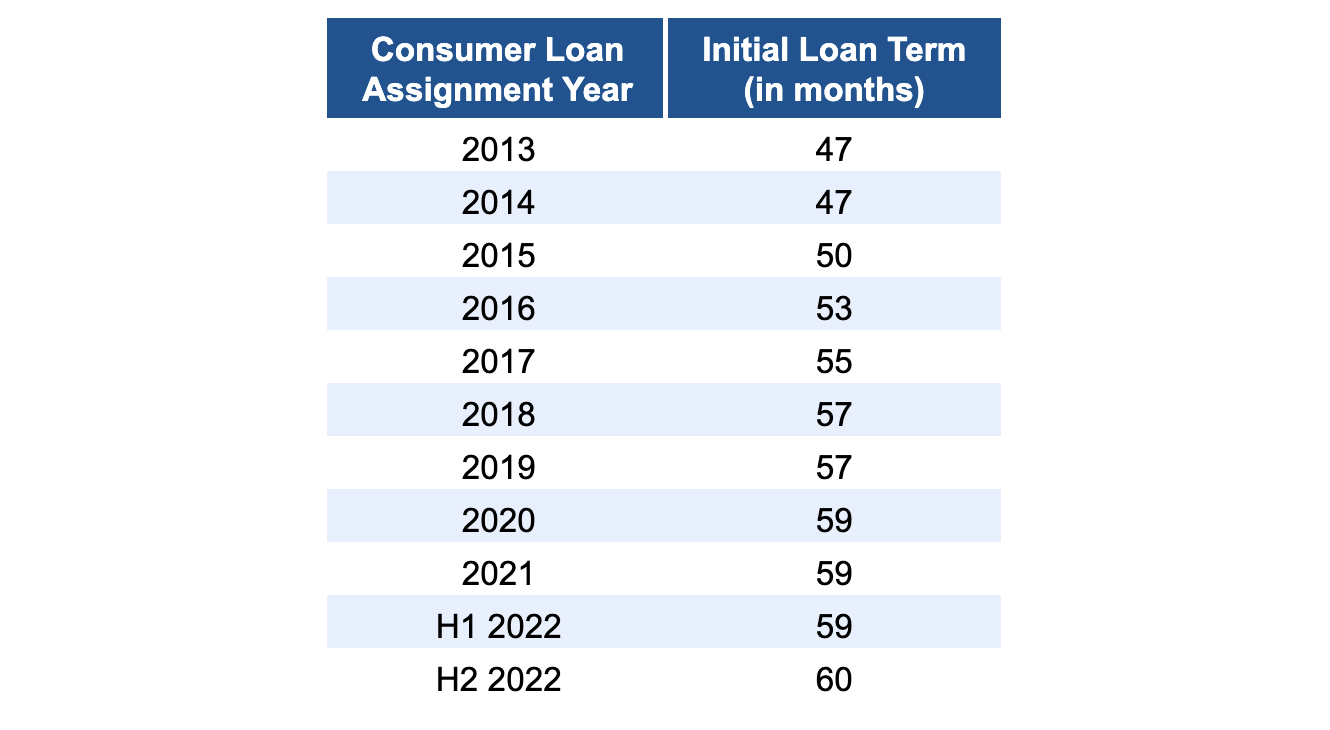

For accounting purposes, both the Portfolio Program and the Purchase Program are technically loans to dealers. This means that CACC is not required to disclose useful customer metrics such as FICO scores, default rates, salvage value of repossessions, etc. Initial loan terms and forecast collection rates are, however, disclosed and show a worrying trend. The initial loan term has increased from an average of 47 months in 2014 to 60 in H2 2022. This allows borrowers to take out larger loans while maintaining lower monthly payments but also means that it will take longer for them to build up significant equity in their vehicle. Delinquencies are more likely during the early stages of a loan if borrowers are struggling to make their monthly payments as there is more incentive for them to default sooner rather than later. Longer initial loan terms increase this higher risk period and therefore the likelihood of default.

{kind=link}

Increasing initial loan terms. (Author - data from Q3 2022 earnings, Credit Acceptance)

Forecast collection rates have also declined from 73.4% for loans assigned in 2013 to 66.5% in the most recent quarterly report with the initial forecast having been revised lower for 2022 after a record year of loan assignments.

Underestimating the risk

Despite the grim outlook for the stock and an already notable drop from highs of $687 in late December 2021 to $472 today, valuations still look generous. The stock currently trades at a relatively high TTM P/E of 10.54 when compared to other lenders with the majority of their book consisting of auto loans such as Ally ( ALLY ) and Capital One ( COF ) with P/E ratios of 6.42 and 6.57, respectively. Ally reported poor performance and outlook in their auto financing segment in their most recent earnings report, with higher than expected delinquencies. While firms such as ALLY and COF have a diversified portfolio of loan types and credit quality, CACC is entirely exposed to the subprime auto loan segment. Back in September 2022, the Consumer Finance Protection Board (CFPB) highlighted the rising trend in the rate at which lenders defaulted on their recent auto purchases through 2021. A trend which was increasing more rapidly for subprime borrowers. This mainly due to an increase in average monthly payments resulting from rising vehicle prices. Since this post was published, conditions have only gotten worse with soaring inflation (11.8% for new cars by the end of 2021 and a further 5.9% in 2022) and last year’s interest rate hikes. More recently, many firms have been announcing layoffs which further contribute to increased default risk woes.

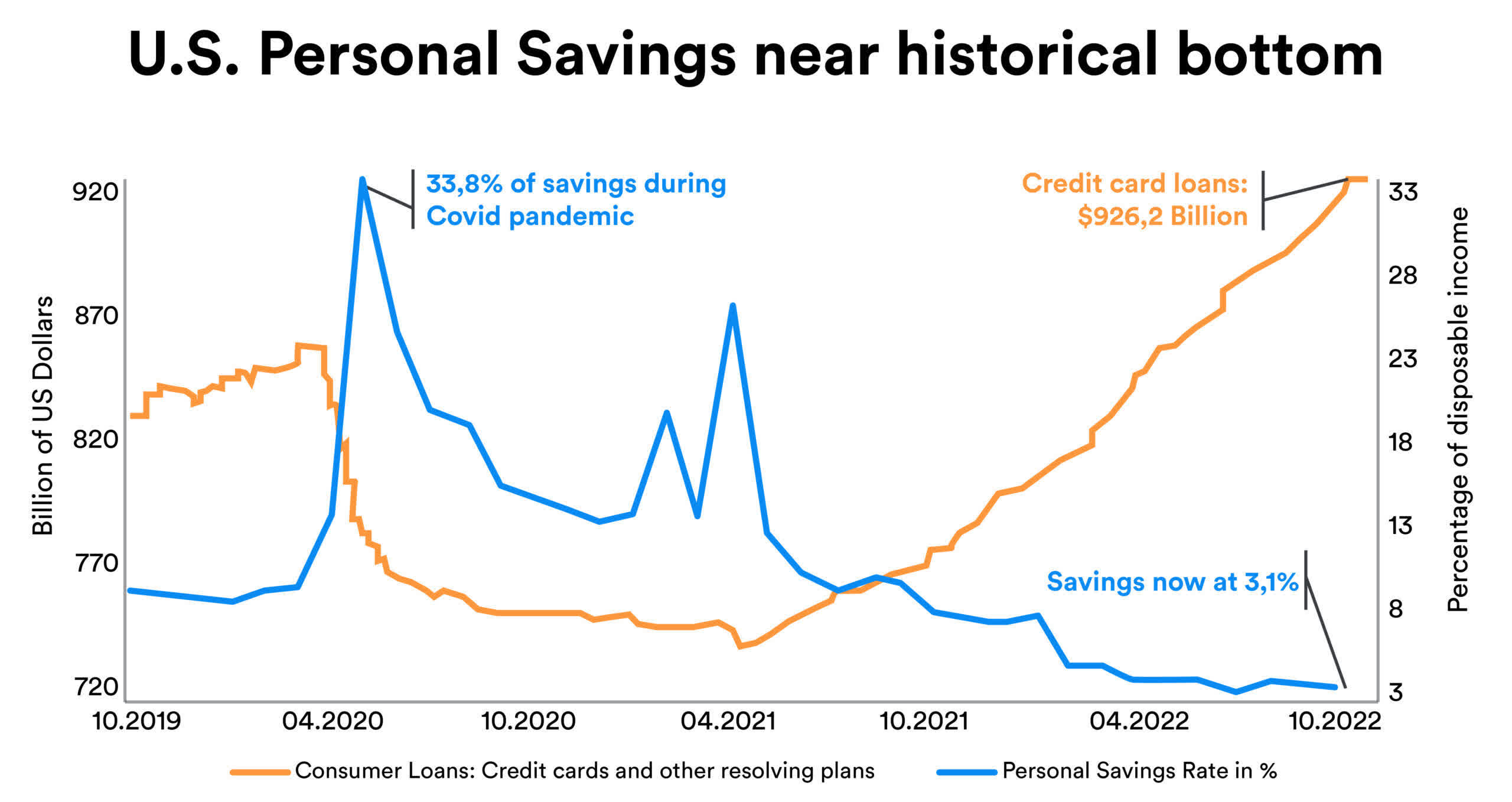

Not only that, but economic indicators are signaling a widespread debt crisis with US consumer credit recently reaching an all-time high while savings are at their lows. It is not clear at which point things will break but the trend looks to be unsustainable in the short term.

{kind=link}

US Personal Savings Rate vs. Consumer Loans (Bloomberg, Lombard Odier)

We believe that investors are underestimating the impact these conditions could have on future performance and financial stability of the company. Not only could it cause a depression in earnings, the company may be forced underwater as it struggles to keep up with debt repayments. While its high ROIC may look good initially, the deterioration of the balance sheet cannot be ignored. Market conditions over the last 12 years or so have presented an exceptional environment for subprime lending, with a long period of economic growth and high employment rates. Simply extrapolating out past performance, the company looks like a reliable compounder, but this point in time appears to be a pivotal moment in the US economy and for CACC especially.

Value in a crisis

To put a value on the stock price in recessionary conditions, we can look back at the most recent recessions in history to see how it might perform, given earnings remain stable. In 2008, the P/E multiple bottomed around 5.9x while during March 2020 lows reached a low of 7.5x, bearing in mind that during those periods the balance sheet was not as leveraged as it is now, with a record high debt to equity of 3.3x currently, and both crises were very different. Based on average analyst estimates of FY22 EPS at $36.77 giving a forward P/E of 12.84x, we obtain a price target of around $217 ((GFC)) to $276 (COVID-19), or a drawdown of 42-54% from the current market price. However, should earnings continue to decline as the recent quarter on quarter results indicate, the price will be forced to fall in line with earnings, regardless of the macro conditions. If cash flow becomes insufficient to cover debt repayments, which is looking increasingly likely, this floor will fall out and bankruptcy risk will become a real concern. Ill-timed buybacks will not support the stock price in the long term.

Key catalysts to look out for will be unfavorable earnings, news from the company regarding more debt raises or worsening economic conditions. Anything but an enormous surprise print in net income this week will render FY22 the first year of negative growth since the 35.8% decline in FY20 driven by increased provisions for credit losses. CACC is on track to experience a comparable decline on an annual basis once again. Any further negativity surrounding collection rates, free cash flow or forecasted yields may also have a material impact on the stock price. In addition, more announcements of refinancing in the form of loans wrapped in SPEs, i.e. continuing to eat into future profitability in order to reduce the overhanging debt burden, will not be popular with analysts. Should any of the US economic indicators such as the unemployment number or GDP growth show an inflection in line with recent layoffs and pessimistic EPS forecasts by many companies, betting on subprime default could become a key strategy to capitalise on new trends. Within the auto loan industry specifically, persistent inflation in new vehicle prices, a decline in industry wide vehicle sales or increasing delinquency rates could all act to depress CACC’s market value. Finally, the company currently faces regulatory issues with a recent lawsuit filed by the CFPB against CACC for predatory lending practices. A negative outcome in this case will also put pressure on the stock price.

The main risk to the thesis is that CACC somehow manages to navigate through troubled economic waters, as they have indeed done in past financial crises, but this time come out on the other side unscathed. If consumer credit is not tapped out as it appears to be and borrowers remain comfortably employed, possibly with higher wages, enabling them to continue paying their record high monthly car payments, CACC will do well. An interest rate reversal and an elusive ‘soft landing’ by the FED will also benefit the company’s ability to refinance or pay down debt, originate new loans and keep collecting on their loan portfolio with a favorable yield. Taking a short position in a stock costs investors money over time and there is no cap on losses. It’s hard to gauge just how long the can-kicking can continue and therefore, poor timing of a CACC short is a key risk. It could be a long time before there is a significant enough shock to break the current business model, but the longer initial loan terms are stretched, the market approaches saturation and debt keeps piling up, the bigger the eventual explosion.

In conclusion, due to poor expected earnings and solvency risk as a result of its large debt burden in a worsening economic environment, a short position in CACC seems like a solid bet on underperformance in the subprime lending industry.

For further details see:

Credit Acceptance: Subprime Trouble Ahead