CACC - Credit Acceptance: There Are Better Opportunities

2023-11-16 16:50:10 ET

Summary

- Economic indicators provide a mixed perspective: consumer confidence is declining, and interest rates are high.

- On the flip side, we observe growth catalysts: decreased used car prices and the expected decline in interest rates next year.

- However, when considering the decision to invest in Credit Acceptance or its industry peers, I lean towards choosing the latter.

Introduction

The end of interest rate increases is in sight, after inflation figures came out better than expected. The Federal Reserve recently paused interest rate increases at 5.3%, and a slight rate cut is expected next year. This makes the economic prospects interesting again, especially for subprime auto lenders. Many hope that a soft landing will occur.

Credit Acceptance ( CACC ) has boomed in recent years. The stock price has risen sharply since the 2008 financial crisis but fell precipitously during the coronavirus crisis in 2020. After the government intervened and provided financial support to US citizens, Credit Acceptance's stock rose sharply from $200 to over $700 at the end of 2021. Yet the trend quickly ended as there was a sharp increase in inflation during the end of 2021. The Fed intervened and raised interest rates. A high interest rate is beneficial for Credit Acceptance's income, but credit delinquencies could increase.

Despite the positive news reports, subprime auto lenders are still attractively valued in the stock market. They also return a significant portion of their profits to their shareholders. In my article I compare Credit Acceptance, Ally Financial and Synchrony Financial from the investor's perspective.

Credit Acceptance's Financial Landscape and Market Sentiments

Credit Acceptance is a subprime auto lender, extending loans to consumers who fall just outside the criteria for a regular car loan. However, this comes with a higher interest rate because of the increased risks for the company. The large exposure to subprime loans makes it particularly susceptible to economic downturns. Low-income consumers are more severely impacted than other consumers. Which could lead to a significant increase in delinquency rates.

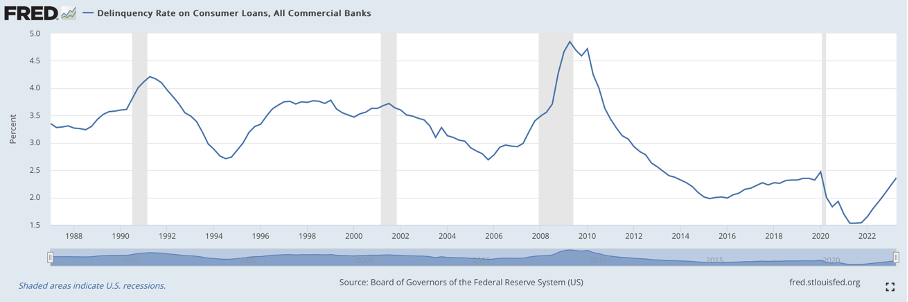

We are currently witnessing this trend. While the United States has not entered a recession, consumer delinquency rates have risen significantly. In the third quarter of 2021, the delinquency rate on consumer loans hit an all-time low. But it has returned to the level of late 2019. Nevertheless, I am not overly concerned at this point. Taking a historical perspective, we observe that the past few decades have seen robust economic performance.

{kind=link}

Delinquency Rate on Consumer Loans (FRED)

Partly due to the low delinquency rates, Credit Acceptance experienced strong growth. Over the past decade, revenue grew at a CAGR of 11.6%, with net income increasing at an average annual rate of 9.3%.

The increased credit delinquencies pose a risk to further profit growth. However, as of the third quarter, this is not yet reflected in the financial results . The figures appear commendable, with total write-offs amounting to $334 million, compared to $349 million in the same quarter the previous year.

Credit Acceptance does not foresee any increased risk in their loan portfolio. Provisions for credit losses have risen to $185 million, up from $180 million a year earlier. The slight increase does not trigger recession concerns for me. The United States continues to grow steadily, with the US GDP showing an increase of 2.1% Y/Y.

Short sellers are less optimistic and are speculating on a decline in the stock price. They have lent and sold more than 11% of the outstanding float. Whether they are correct remains to be seen.

Credit Acceptance's Performance Amid Shifting Dynamics

The third-quarter figures present a positive outlook. What stands out to me positively is that the percentage of Consumer Loans with either FICO scores below 650 or no FICO scores was significantly lower in the past quarter (78.6% of the consumer loan assignment volume) than in the same quarter in 2022. So the loans issued by Credit Acceptance are safer now.

Taking a broader view, Credit Acceptance has performed well over the past decade. The management has proven itself and achieved substantial annual revenue growth averaging 11.6%. The profit also increased significantly over the same period. Their sales method has proven effective.

However, since 2020, their aggressive sales approach has revealed some vulnerabilities. Credit Acceptance allegedly urged low-income consumers to take out car loans using aggressive sales techniques. Upon disclosure, the stock price plummeted from $500 to $300 per share. The case was eventually settled, but in my opinion, it indicates that the years of robust growth are behind us. Nevertheless, investors remain enthusiastic due to the higher stock valuation compared to industry peers.

Another positive aspect is that the inflation figures paint a favorable picture. In October, Core CPI (which excludes food and energy) increased by +4.0% YoY vs. an expected +4.1%. This could suggest a dovish policy from the Fed, where an interest rate cut may be warranted. The sharply decreased used car prices, in my view, act as a catalyst for subprime auto lenders. Coupled with a lower interest rate, this will stimulate growth in subprime loans, and Credit Acceptance is strongly positioned in this regard.

Decoding Valuations: Navigating Risk, Share Repurchases, and Investor’s Perspective

Credit Acceptance has a different risk profile compared to Ally Financial ( ALLY ), for instance. Ally Financial issues significantly fewer loans to subprime borrowers. Consequently, Credit Acceptance boasts a much higher profit margin than Ally Financial (net margin CACC = 17.3% versus net margin Ally = 13.3%).

Due to the increased risk, we anticipate that Credit Acceptance would have a more attractive stock valuation. However, this is not the case. Credit Acceptance's forward P/E ratio stands at 10.4, whereas Ally Financial's is only 8.1. The sector average is 8.9, indicating that Ally Financial is slightly undervalued compared to the sector. The P/B ratio offers a similar insight: Credit Acceptance is richly valued at a P/B ratio of 3 compared to Ally's P/B ratio of 0.7. I believe that Credit Acceptance's higher profit margin does not justify a more expensive valuation due to increased business risk.

Credit Acceptance's valuation also appears to be generous compared to Synchrony Financial ( SYF ). I am familiar with Synchrony Financial; I purchased its stocks in early 2020 during the depths of the COVID-19 crisis. The stock price rebounded well after the government swiftly intervened and provided financial aid to consumers. Berkshire Hathaway also held Synchrony in its portfolio for years but sold the entire position in the first quarter of 2021 (after the surge). Synchrony is undervalued as well; the forward P/E ratio is only 5.7, and the P/B ratio is 0.9.

There is another difference between Credit Acceptance and its peers. Synchrony, Ally, and Credit Acceptance all buy back their own shares, but the first two also pay dividends. This may explain why Credit Acceptance is more expensively valued than its peers; they repurchase more of their shares, increasing the stock price.

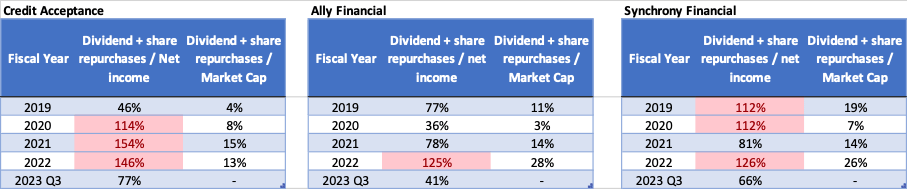

To make a fair comparison, I examine the cash flows from dividends + share repurchases and compare this with their net income from previous years until now. We also compare this with their market capitalization to investigate which stock offers the most value for investors.

{kind=link}

Total Payout (Analyst' calculations)

We observe that Credit Acceptance consistently repurchases more shares than it has made in profits in previous years. To finance share buybacks, Credit Acceptance has also tapped into its cash reserves. In the short term, this is favorable for shareholders due to the potential upward surge in the stock price. However, in the long run, this is not sustainable; the money will eventually run out. TTM Share repurchases now amount to $281 million, approximately 5.4% of the market capitalization. Now, Credit Acceptance adopts a conservative approach toward its shareholders.

Among the three examined companies in the above table, Ally Financial stands out. The total amount paid out in dividends plus share buybacks is (except for 2022) lower than the profit. This keeps their cash increasing while also paying out a decent dividend. The dividend also grows well due to the share buybacks. It's a win-win.

Ally’s total payout (dividends + share repurchases) compared to the market capitalization is significant. This makes the value for shareholders more attractive than it is for Credit Acceptance. And this holds true for Synchrony Financial as well. For Synchrony, the total payout is often higher than the profit made (and thus also not sustainable for the long term). In conclusion, Ally Financial appears most attractive when solely considering value for shareholders.

Furthermore, the company's growth is also a crucial factor. Analysts predict that Synchrony Financial's revenue will increase significantly, but the EPS will only rise in 2024. The EPS of Ally Financial will experience a strong increase only next year. Analysts for Credit Acceptance expect annual revenue growth in mid-single digits, with the EPS expected to rise in 2025. Among these three examined industry peers, Synchrony Financial looks the most appealing due to its stable revenue growth. Ally Financial follows closely with robust forward EPS growth.

{kind=link}

Earnings Estimates (Seeking Alpha)

Conclusion

The favorable inflation figures paint a positive picture of the subprime car loan market. Not only do the decreased used car prices serve as a robust catalyst, but also the anticipation of a decrease in interest rates next year is encouraging the issuance of subprime loans. Credit Acceptance, Ally Financial, and Synchrony Financial are clearly positioned for growth if a recession is averted. However, when considering the decision to invest in Credit Acceptance or its industry peers, I lean towards choosing the latter. Credit Acceptance is evidently more expensively valued than its sector peers. Despite likely deserving a higher stock valuation due to its strong growth in revenue and profit over the past 10 years, I still prefer Ally Financial or Synchrony Financial because their risk profile is safer. Additionally, the anticipated growth looks much more promising. Economic indicators provide a mixed perspective: consumer confidence is declining, and interest rates are high. On the flip side, we observe growth catalysts: decreased used car prices and the expected decline in interest rates next year. For now, I'm keeping Credit Acceptance on hold, as industry peers seem to offer more opportunities in the market.

For further details see:

Credit Acceptance: There Are Better Opportunities