UBS - Credit Suisse: A Contrarian Buy

Summary

- Credit Suisse is currently trading at only 0.2x book value, the cheapest valuation in the European banking sector.

- Liquidity was a major issue in recent months and the most concerning risk for me, but this seems to have improved in recent weeks.

- Credit Suisse’s shares are now a buy for contrarian (long-term) investors.

Credit Suisse ( CS ) has a depressed valuation that already reflects most of its fundamental issues, providing an opportunity for long-term (contrarian) investors to buy a deep value play that I think can perform quite well over the next three to five years.

Background

As I’ve covered in a previous article , Credit Suisse has faced a rough period in recent months, due to some fundamental issues that led to weak investor sentiment towards the bank. This is reflected both in its low share price and valuation, as well as its credit spreads that are near all-time highs.

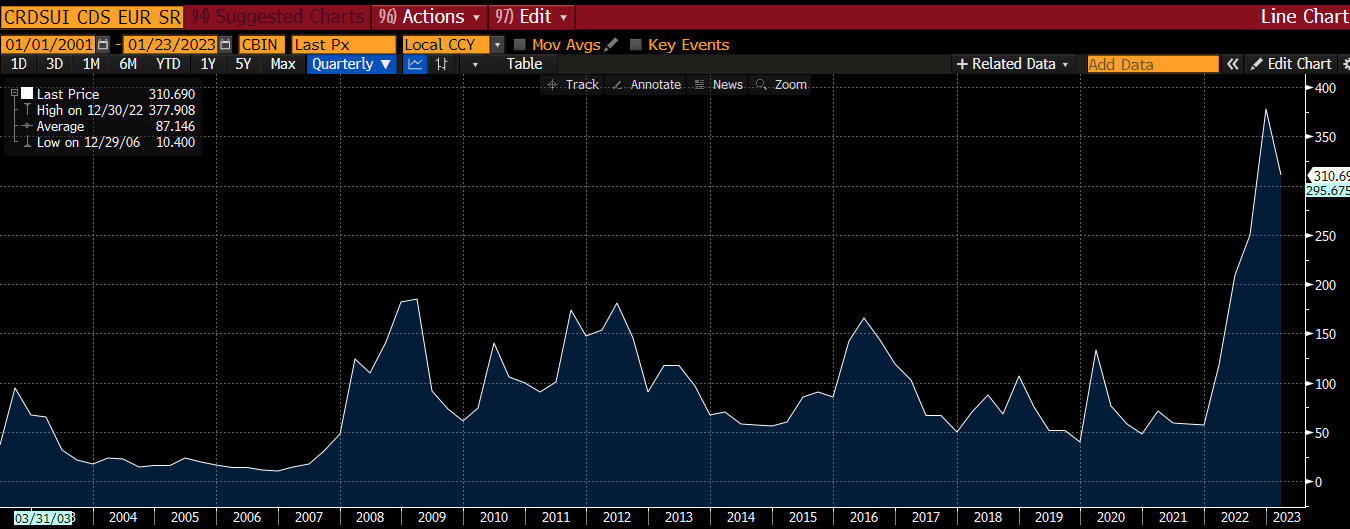

As can be seen in the next graph, Credit Suisse’s five-year credit default swaps currently trade at more than 300 basis points (bps), a higher spread than compared to the period during the global financial crisis of 2008-09, and also compared to the European debt crisis of 2012-13.

{kind=link}

This is very important because, contrary to most corporations, banks rely heavily on wholesale and customer’s funding, which makes them very vulnerable to investor sentiment. Indeed, reputational risk is something that investors usually don’t give much importance, but it’s critical for a bank to operate sustainably.

This happens because one of the major risks in the banking industry is a ‘bank run’, a situation that usually arises from customer’s perception that a bank may cease to function in the near future and withdraw their money from the bank. This can lead to the collapse of a bank, or at least to receive emergency bailout funds from the central bank, if a significant part of deposits are withdrawn from the bank.

While Credit Suisse did not have a ‘bank run’, its liquidity turned clearly worse during last October, as the bank experienced major cash outflows and was out of the bond market, due to the strategy presentation scheduled for the end of the month.

However, over the past couple of months, Credit Suisse completed an equity raise, issued bonds in the capital markets, and reportedly has been able to recover some deposits, showing that investor sentiment is likely now better than it was some months ago. While a restructuring and full recovery of investor confidence may take some time to happen, I think investors should question now if Credit Suisse’s current depressed valuation provides an interesting value play or if it’s a value trap.

Liquidity

As I’ve said, liquidity management is very important for banks in the short term, and while during normal times this usually doesn’t get much attention from investors, during periods of market turmoil or risk-aversion regarding a specific bank, liquidity can turn out to be one of the most critical factors for a bank.

Credit Suisse had a comfortable liquidity position at the end of Q3 2022, measured by its liquidity coverage ratio of 192%, which was practically unchanged from the end of the previous quarter. This ratio compares the bank’s high-quality liquid assets (HQLA) to its stressed net cash outflows ((NCO)) expected in 30 days, which means that Credit Suisse had almost double the assets required to cover its cash outflows expected in a stressed situation.

However, due to negative press and social media coverage during last October, the bank suffered significant deposits and assets under management (AuM) outflows, leading to a drop in its average daily liquidity ratio to 154% in the first 25 days of October. While this was still above the bank’s regulatory requirements, it was a concerning trend that could put the bank in a difficult situation. Moreover, as the bank was planning to perform a strategic update at the end of October, it was not issuing new debt, putting further pressure in its liquidity management.

Following its strategy presentation, the bank has reportedly been able to stop cash outflows and issued new debt, both in the dollar and euro markets, issuing about $7 billion in three senior bonds, showing that despite negative media coverage it still can successfully raise new funds in the credit markets.

Nevertheless, the bank’s most recent update about its average daily liquidity coverage ratio is related to third quarter-to-date, as of December 7, 2022, reporting that it was above 140%. As can be seen in the next graph, this liquidity ratio is much lower than its historical trend, showing that liquidity was a great concern for Credit Suisse during Q4.

LCR ratio (Credit Suisse)

According to Credit Suisse’s CEO , AuM outflows have decreased and the bank sees some money coming back in some parts of the business. While the bank did not update its liquidity position at the end of 2022, it is likely that it has improved towards the end of the year. The bank completed a $4.2 billion capital raise in December, and reportedly this helped to improve customer confidence in the bank, with some money returning to its Swiss bank before the end of the year.

With capital markets starting the year with improved investor sentiment, this should also help Credit Suisse to regain money that went out in the last few months, improving its liquidity position. This means that from a liquidity management perspective, Q4 is likely to have been the worst quarter of the current downtrend, and a new period of liquidity stress is not likely in the near future.

Valuation

Taking into account the difficult backdrop over the past few months, it is not surprising to see that Credit Suisse’s shares are trading near all-time lows. Indeed, over the past year, its shares have declined by about 60%, being a major underperformer in the European banking sector during this period.

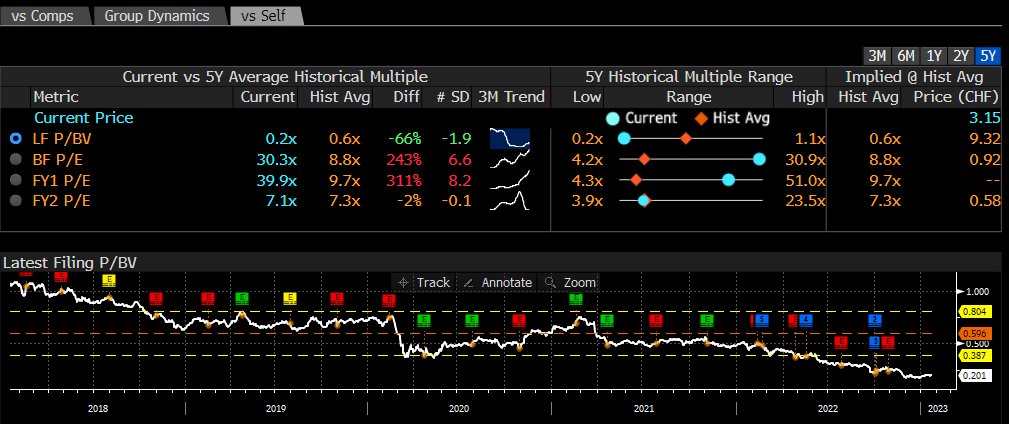

This weak share price performance has led to a very depressed valuation, as the bank is currently trading at only 0.20x book value. This represents a major discount to the European banking sector average (about 0.87x book value), and its own historical average over the past five years (around 0.6x book value).

{kind=link}

This depressed valuation represents extreme negative investor sentiment, and Credit Suisse is currently the cheapest bank in Europe. For instance, Deutsche Bank ( DB ) is currently trading at 0.4x book value, while its Swiss competitor UBS Group ( UBS ) is trading at 1.2x book value. This clearly shows that Credit Suisse’s valuation is too harsh and while the bank has many issues and its fundamental performance is not expected to improve rapidly, its valuation already seems to reflect this profile.

Indeed, Credit Suisse has guided for Q4 2022 pre-tax losses of about CHF 1.5 billion and, according to analysts’ estimates , the bank should report a net loss of about CHF 900 million in 2023.

While its restructuring phase will take some time to change the bank’s business profile in a significant way, its strategy to reduce its exposure to investment banking and allocate more capital to recurring and safer business operations, namely its Swiss bank, plus wealth and asset management, will lead to a bank with a lower risk profile and a more recurring earnings profile.

This justifies a higher valuation over the medium to long term compared to its historical pattern, even though there is significant execution risk in the next few years, as the bank needs to deliver on its planned business overhaul.

Conclusion

In my previous analysis I said most of Credit Suisse’s woes and fundamental issues were priced-in, but investors should wait to buy its shares as the bank was preparing to present its new business strategy. Even following its updated strategy presentation I was wary of buying Credit Suisse’s shares due to its liquidity issues, which now seem to have been largely fixed.

Therefore, even though a successful restructuring will take some time to perform and investor sentiment is likely to remain negative for some time, I now see Credit Suisse’s current depressed valuation as an opportunity for long-term (contrarian) investors, as Q4 2022 is likely to have been the bottom for the bank.

Nevertheless, investors should be patient and buy with an investment horizon of some years, as a rapid turnaround is not likely and earnings in the coming quarters can still surprise to the downside.

For further details see:

Credit Suisse: A Contrarian Buy