CRDO - Credo Technology: Gross Margin Should Expand But Valuation Is Still Expensive

2023-07-11 16:42:26 ET

Summary

- I recommend a hold rating for Credo Technology due to its high valuation, despite expectations for margin normalization and growth in key areas.

- The company's strong balance sheet, with virtually no debt and $217 million in cash, and potential for increased gross margin are positive factors.

- Concerns over the timing of recovery for the IP business and the stock's current high valuation compared to historical averages lead to a cautious outlook.

Overview

My recommendation for Credo Technology ( CRDO ) is a hold rating as I expect valuation to revert back to average despite my expectation for normalization in gross margin eventually.

Note that I previously issued a holding rating for CRDO due to the high valuation that the stock was trading at, and I am reiterating it.

Business

CRDO is ahead of the curve when it comes to offering advanced network security and speed. Solutions from CRDO are both powerful and economical. Credo innovations are focused on easing system bandwidth bottlenecks while improving power, security, and reliability. Digital Signal Processor [DSP] and Serializer/Deserializer (SerDes) are the foundations of the technologies provided. The solutions provided excel in both optical and electrical ethernet settings. Businesses in the enterprise and HPC sectors, as well as hyper scalers, original equipment manufacturers, ODMs, and makers of optical modules, are among Credo's clientele.

Industry

Consegic Business Intelligence estimates that the value of the global serial device server market will rise from $227.12 million in 2022 to $367.46 million by 2030, representing a CAGR of 6.5%. Massive and rising cloud workloads, an increase in the use of streaming video, the rollout of 5G wireless networks, the proliferation of IoT devices, and the increasing popularity of AI are likely to fuel this expansion. This is putting a strain on the current data infrastructure and necessitating a shift from transistors to systems as a paradigm. Numerous private firms and divisions of publicly traded companies vie for a piece of this massive market. Companies like 3onedata, Atop Technologies, Comtrol Corp, Kyland, Advantech, etc. are just a few of the many in this sector.

Investment highlights

For CRDO, I anticipate development in a few key areas over the next few years.

I think the AI movement is good for CRDO because it presents a promising expansion possibility for Active Electrical Cables [AEC]. Due to the nature of AI cluster configuration (note that AI requires higher density racks to facilitate the higher computing power using the same footprint), I anticipate a much larger revenue opportunity in AI than in traditional compute racks.

Given CRDO's disproportionate exposure to China's cloud hyperscale customers in the past, the percentage of optical DSPs in CRDO should begin to inflect and increase over time as CRDO made inroads at a U.S.-based hyperscale customer with its 400G solution.

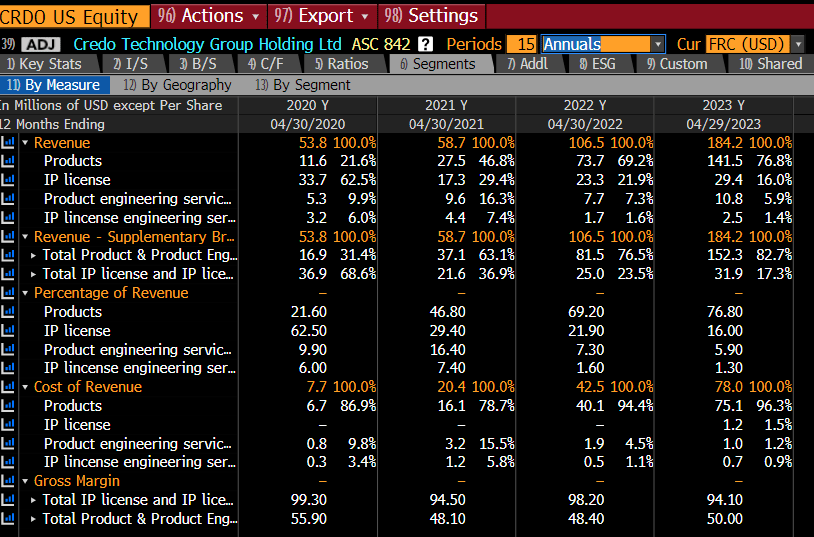

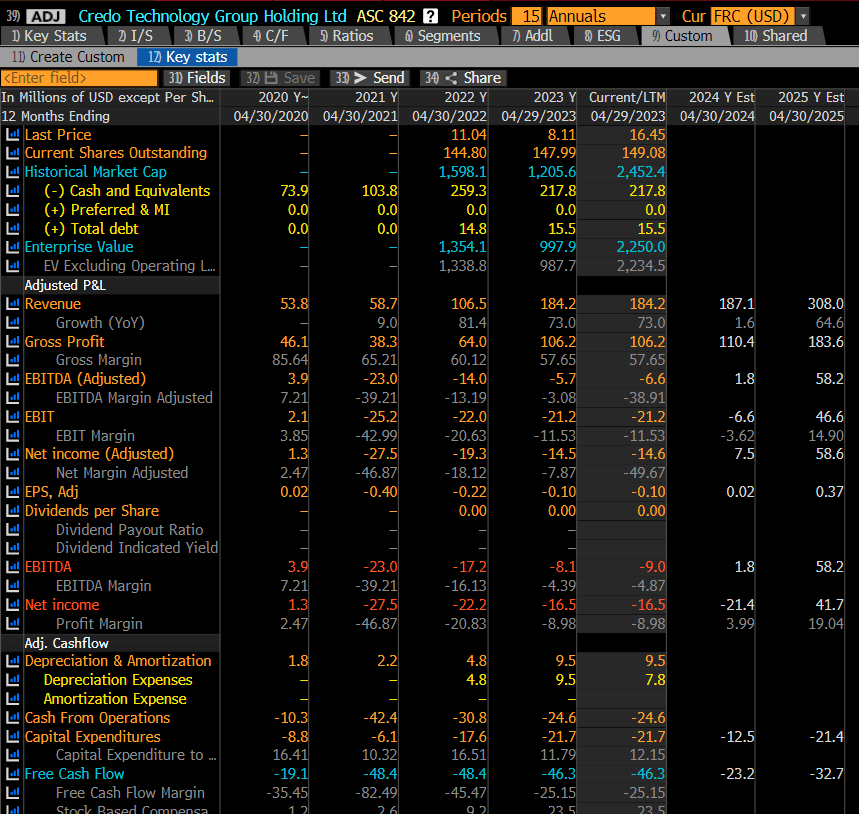

Since CRDO has shown they can increase margin even with a smaller revenue base, I am optimistic that my forecast for revenue growth will translate well into higher gross profit growth. Even though revenue was lower in 4Q23 compared to 2Q23, gross margin increased to 57.92%. Notably, the proportion of revenue coming from lower-margin businesses has risen (from 69% in FY22 to 77% in FY23), indicating that management has improved productivity. Assuming CRDO's high-margin IP business mix stabilizes, I anticipate gross margin will increase to above 60% from its current high 50s.

{kind=link}

Financial highlights

{kind=link}

While CRDO revenue was down last quarter due to a weak demand environment, I believe this is just a blip and that the long-term opportunity from AI will drive growth in the long run. Furthermore, CRDO has demonstrated their ability to land large customers in this difficult environment, which supports my belief that CRDO product offerings meet market demand.

As stated above, I expect gross margin to increase and likely exceed the high 50s% range to 60+% as the business appears to have a lower cost base now (on a COGS level). Given the high incremental margin (gross margin of 50+ to 60%), this should result in higher EBITDA margin. Additionally, normalizing product mix would be another driver of gross margin expansion.

Given that there is virtually no debt and $217 million in cash, the CRDO balance sheet is quite strong. The cash position should be sufficient to see the company through any periods of cash burn.

Valuation

Author’s valuation model

According to my model, CRDO is valued $15.82 in FY24, making the stock fairly valued today. This target price is based on my muted growth in FY24 due to the uncertainty in CY2023, but a strong rebound in growth in FY25. The rationale for the muted near-term growth rate is that I believe the macro environment will remain this way in the short term, and the majority of recovery will happen in FY25.

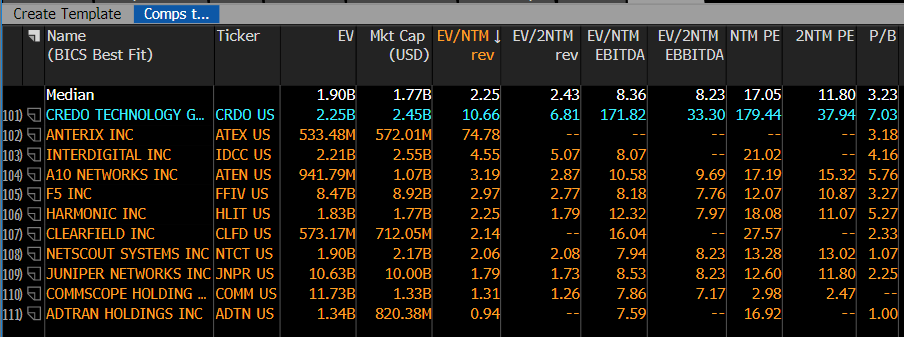

CRDO is now trading at 10x forward revenue, which I believe is too high as it's way above its historical average. In my opinion, this is because the market is expecting a strong recovery in the near-term. However, given the increase in interest rates, and slower expected growth than the past, I find it hard justify such a high multiple.

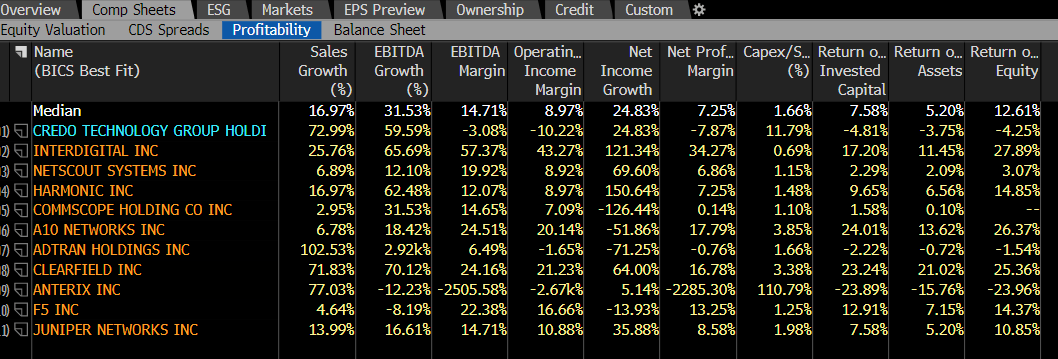

The only reason I believe a higher multiple is justified today is because CRDO is expected to grow faster than peers like ATEX, IDCC, and ATEN, that operate in a similar industry. However, I don’t think this is sufficient to justify a 10x forward revenue valuation.

{kind=link}

{kind=link}

Risk

On the point of IP business, while I am positive on it recovering, the problem is the timing of recovery as it is very lumpy. There might be periods where we see consecutive quarters of weak performance, which might cast doubt over the health of the segment, thereby driving a negative sentiment.

Conclusion

I maintain a hold rating for CRDO due to the stock's expensive valuation. While CRDO has shown the ability to improve margins, the valuation is currently high compared to historical averages.

For further details see:

Credo Technology: Gross Margin Should Expand But Valuation Is Still Expensive