CRDO - Credo Technology: Near-Term Growth Uncertainty Is Not A Good Thing

2023-08-31 07:11:58 ET

Summary

- I reiterate hold rating recommended due to valuation and potential stock price volatility.

- The concentration of customers and the inherent lumpiness of cloud CAPEX projects raise concerns about the predictability of revenue trajectory.

- CRDO competitive advantage in AEC is expected to drive high growth as the company remains a sole source for specialized programs.

Overview

My recommendation for Credo Technology (CRDO) is a hold rating, as I expect valuation to eventually rerate back to a 7x forward revenue multiple. At that valuation, the margin of safety is higher, which would cushion any stock price volatility in the event of another Microsoft ( MSFT )-like incident happening again. Note that I previously gave a hold rating for CRDO as the valuation remains elevated.

Recent results & updates

The $35.1 million in revenue that CRDO reported for 1Q24 was 2% above projections. The IP segment's revenue dropped by 73% to $2.8 million, while the product segment's revenue dropped by 10% to $32.3 million. As I had predicted in my previous article, gross margin increased to 59.8% (a 160bps increase from the previous quarter). This resulted in management raising their expectations for 2Q24 gross margin to 59% and revenue to $43 million, both of which are increases over the consensus estimates. The company's management has reaffirmed its forecast for sequential revenue growth throughout FY2024 after CRDI posted results that were slightly better than expected. The bullish part of me is positive that the business will see growth as management sees positive demand ramp up in the segments. For instance, Microsoft is catching up on its infrastructure expansion (which had been delayed) and seeing customer ramps in the AEC market. This should contribute nicely to FY24. The other major hyperscale customer is also predicted to experience rapid growth in the coming months.

Today, our largest customer deploys our AECs for both general compute and AI applications. Additionally, we continue to design custom AEC solutions to solve for their next-generation deployments, including our first internally developed 100 gig per lane AI deployment. At our second hyperscaler customer, our production ramp for both general compute and AI programs remains on track with expectations for continued growth throughout this fiscal year and fiscal '25. from: 1Q2024 earnings call

Understanding CRDO's dominant market position in AEC is crucial, in my opinion, because its rivals typically lack the necessary qualifications to compete. This was seen in the case for MSFT as management commented below. I expect this competitive advantage to enable CRDO to continue grow at a high rate as it is often the sole source of the program it offers..

And so the customer base -- we've talked at length about the work that we did for Microsoft enabling the dual-core architecture and delivering an intelligent AEC solution. The fact is, others try to compete, others never achieve qualification and we're sole source of that program and that trend continued, so every one of our high-volume relationships, every one of our high-volume discussions, the engineers understand there's an opportunity for innovation and our team is well organized to achieve those differentiated features that make their rack design that much more valuable. I think that's going to be a long-term advantage for us and it's going to continue to be a competitive moat. from: 1Q2024 earnings call

Despite accounting for only a fraction of CRDO's revenue, CRDO Optical DSP division has been expanding steadily in recent years. On the call, management revealed that CRDO had secured a design win with a 400G solution at a U.S.-based hyperscale customer. The growth acceleration guide for FY24 is supported by this customer's anticipated ramp in FY24 and FY25. Management also noted improvements in China, which had been a problem area for several quarters. As such, growth for the rest of FY24 seems promising if we put all of these together.

We're also seeing demand restart from data centers in China. While too early to create meaningful expectations, Credo stands to benefit as spending returns in this market. from: 1Q2024 earnings call

In a nutshell, the results of 1Q24 showed promising signs and pieces of data that growth is very likely to accelerate for the rest of FY24, as guided. Given the concentration of customers, though, I would warn that visibility into revenue growth trajectory is still lacking. The largest customer accounted for 41% of total revenue in the July quarter, and CRDI had three customers that each represented >10% of revenue. As such, CRDO growth trajectory might get severely impacted by the budgets and implementation timeline of these customers. This is in addition to the fact that cloud hyperscale capex projects tend to be inherently lumpy.

Valuation and risk

Author's valuation model

My valuation approach did not change for CRDO. According to my model, CRDO was valued at $16 in FY24, making the stock fairly valued today. While I am optimistic about growth acceleration through the rest of FY24, I feel uneasy about the revenue concentration with its largest customers. Remember that MSFT's ramp-up plans faced some hiccups in February , which impacted CRDO performance?

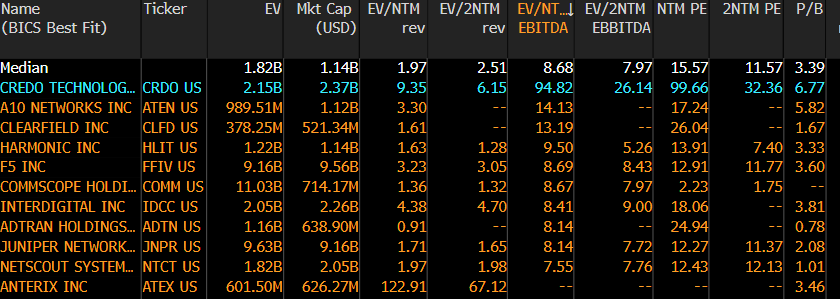

The good thing is that valuation has come down slightly by 1x, from 10.5x to 9.5x today. This is in line with my expectations that the valuation is too high and should eventually rerate to 7x forward revenue. My opinion remains the same: this is because the market is expecting a strong recovery in the near term. I give credit to this expectation based on management's comments, but this is outside of my risk appetite to invest in this multiple. I prefer to invest when the stock is nearer to its historical average multiple, which will give me a greater margin of safety.

{kind=link}

Summary

My recommendation for CRDO remains a hold due to ongoing uncertainty in near-term growth (customer concentration + inherent lumpy cloud CAPEX). Positive demand from major customers like Microsoft and improved performance in the Optical DSP division support potential growth acceleration for rest of FY24. However, revenue concentration and the potential impact of customer budgets and timelines increased the uncertainty of modeling quarterly revenue performance - which impacts market expectations and stock price volatility. While valuation slightly decreased from 10.5x to 9.5x, I continue to anticipate a rerating to 7x forward revenue, aligning with a historical average.

For further details see:

Credo Technology: Near-Term Growth Uncertainty Is Not A Good Thing