CPG - Crescent Point: Acquisition And Impact On Future Returns

Summary

- Crescent Point Energy surprised the markets with an acquisition.

- The purchase was a bit of a drift from its capital return and deleveraging strategy.

- We look at the purchase and the impact on future returns.

Note: Amounts are in USD or CAD as noted

When we last covered Crescent Point Energy Corp. ( CPG ), we gave it a rare "strong buy" rating. The appeal was the rapid deleveraging and a management that had learned that shareholder returns should take priority over empire building. Specifically, we said:

CPG is extremely cheap whichever way you slice it. Unlike the altar of growth stocks where you have to use 2030 estimates to start making sense of even decimated stock prices, the returns are here. The free cash flow yield after base dividend works out to 25% at our expected oil and natural gas prices. The dividend is sustainable down to $45/barrel. Yes, volatility is high and can be unnerving. But the stock is cheap, even if longer-term prices average closer to $65/barrel oil and $4.00/mcf for Natural gas. We reiterate our Strong Buy rating.

Source: Unhedged Natural Gas Adds Extra Firepower

The stock has not done much since then but outperformance against the broader market is always a plus.

Seeking Alpha

We look at the recently announced acquisition and see if this still deserves to be backed for a higher price.

The Purchase

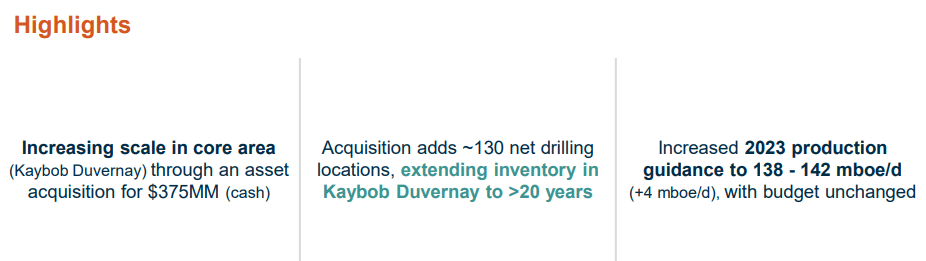

CPG announced in early December that it had agreed to acquire Paramount's Kaybob Smoky and Kaybob South Duvernay Assets for CAD375 million.

{kind=link}

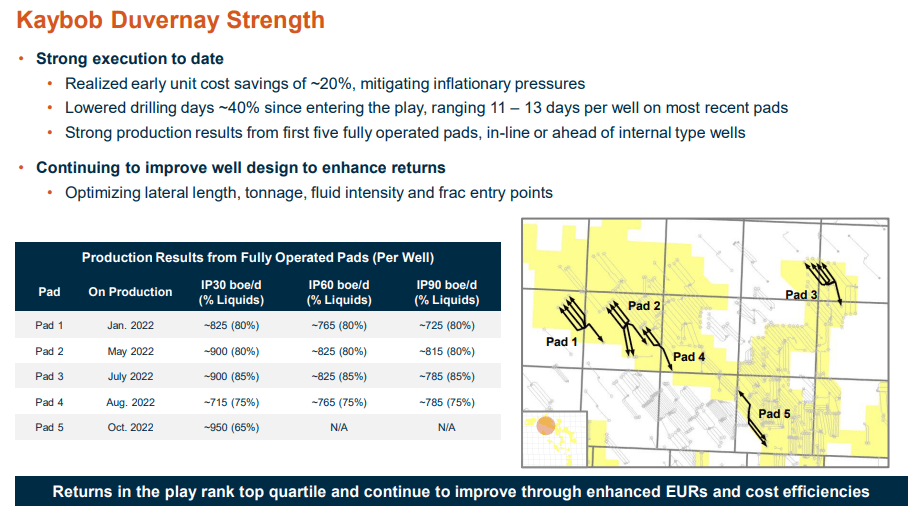

The purchase came with immediate production of about 4,000 barrels of oil equivalent a day. About half of this is liquids, so this is a bit different than CPG's entire base, which leans about 80% liquids. Even if we give this credit for being similar to CPG's higher return profile production, the purchase is expensive relative to where CPG's own enterprise value stands on a barrel of production. But fortunately, that is not all that CPG is getting. Firstly, the 2P reserves of 64 million barrels of oil equivalent help make the case for this purchase. The purchase price also includes gas infrastructure and 65,000 net acres of crown land, alongside 130 net future drilling locations. When we add all this up, the purchase price is a bit more expensive than one could assign on market values. Current production would be worth about CAD160-CAD200 million based on the closest publicly traded comparatives for a 40-60% gas play. This leaves about $200 million for future growth in Duvernay. With 130 locations, we are looking at close to $1.3 million CAD per site, and that is debatable whether it is too high. Certainly, for undeveloped inventory, one could argue that it is expensive. On the other hand, the results CPG has produced in that area are quite stellar.

{kind=link}

CPG has bolstered its position here over time, and so far, the results have borne out management strategy. So, our take here is that the worst case is an overpayment of CAD75-CAD100 million, something that does not materially move the needle on a CAD7.3 billion enterprise value.

Outlook

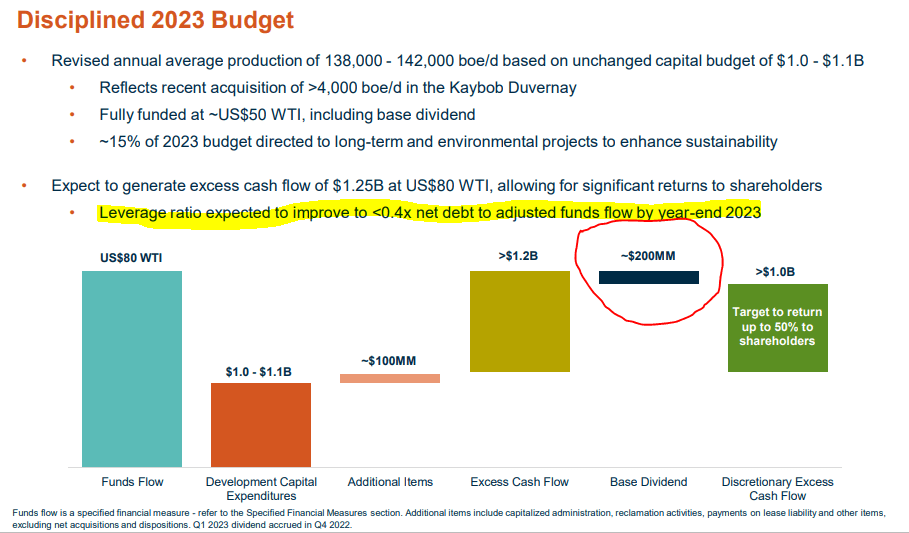

When you consider the flowing barrels added to the equation, the ending net debt to EBITDA for 2023 does not change materially. We estimate about 0.6X-0.7X using an average of USD75-USD70 WTI prices for the year. This is after factoring in the increased base dividend. We will note here that the base dividend consumes a very small portion of the cash flow, and the company itself expects a debt to EBITDA of under 0.4X.

{kind=link}

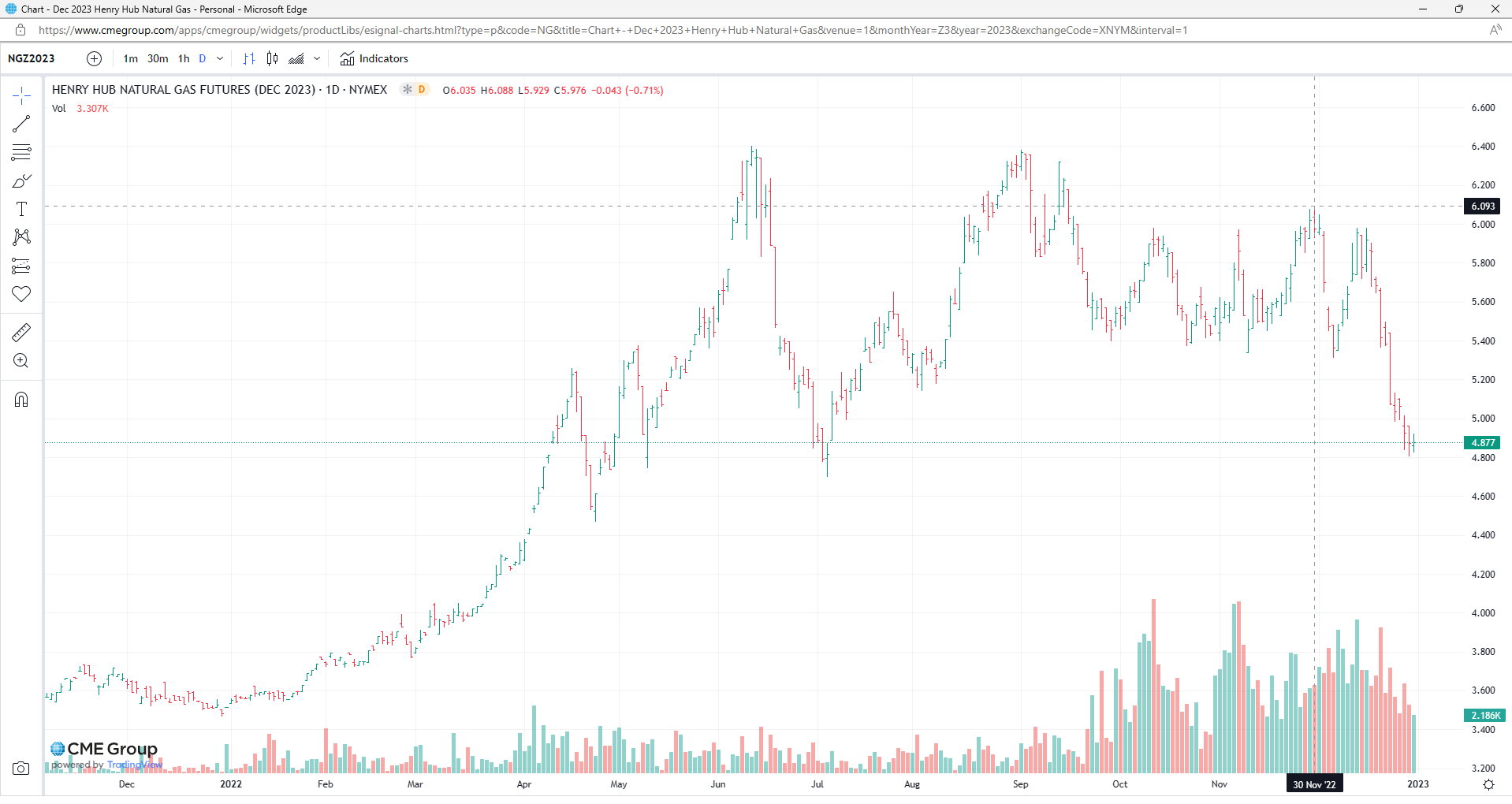

The difference here comes on two fronts with our estimates. The first being that we are using more conservative oil prices than management, and think oil services cost inflation is still being underestimated. The second is that the strip on natural gas prices has collapsed since this presentation was released. You can see this in the move of December 2023 Natural Gas Futures since November 30, 2022.

{kind=link}

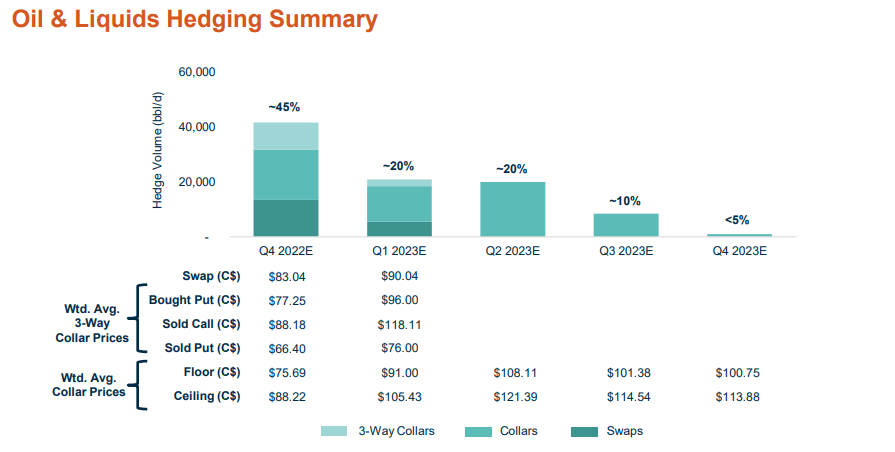

CPG has very modest protection on oil prices for 2023.

{kind=link}

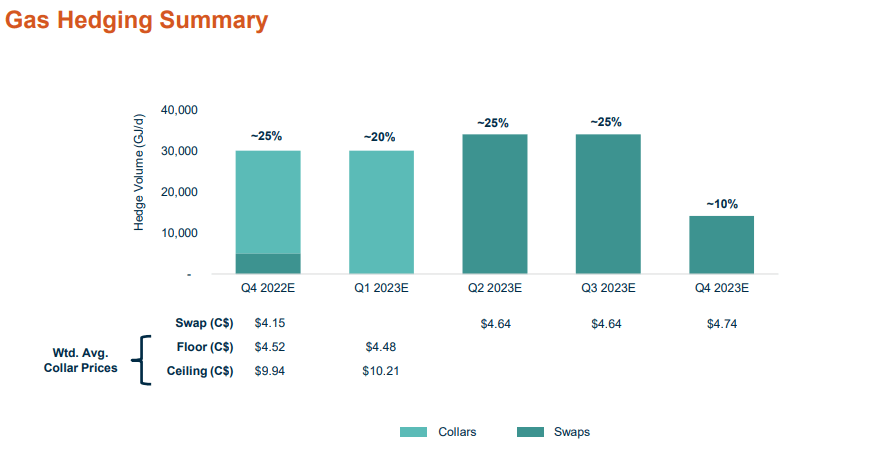

Gas hedging is a little better.

{kind=link}

But overall, the stock is likely to see more impact from moves in commodity prices than it did in 2022. An offset here is that debt is far lower. From year-end 2021 to year-end 2022, we see an CAD800 million delta. That makes the lower hedges acceptable. CPG's position continues to be quite strong, despite this purchase, and while we would have liked to see more hedging, the company has shown great execution.

Verdict

CPG's valuation continues to be compelling. It is trading at about 3X EV to EBITDA, even based on our conservative assumptions. This allows it to have a huge impact with every dollar of buyback or even debt reduction. That same multiple usually means that very little outside of buybacks or debt reduction makes sense for excess cash flow. So we understand the skepticism towards the purchase. We still think it was not bad, and you have to give management some runway here, considering their execution over the last 3 years in general and their Kaybob results in particular. If oil prices land up remaining anywhere over USD60 over the next decade, and that is certainly the way we see it, you will be glad they made this purchase. Even if we don't count on valuation expansion, we could see 20% annual returns from here at about USD75/oil. We are looking for a modest USD10 share price (CAD13.50) by the end of 2024 and that should outperform most index returns by a mile.

Please note that this is not financial advice. It may seem like it, sound like it, but surprisingly, it is not. Investors are expected to do their own due diligence and consult with a professional who knows their objectives and constraints.

For further details see:

Crescent Point: Acquisition And Impact On Future Returns