PRMRF - Crescent Point Deals Transform Company

2023-04-13 16:56:58 ET

Summary

- Recent asset acquisitions transform Crescent Point Energy Corp. and position it for production growth.

- Deals add debt and thus risk, but Crescent Point Energy has gone into growth mode.

- Crescent Point Energy Corp. stock looks like a "Buy" for oil bulls looking for a company with a little more production growth.

For oil bulls looking for a company that is set to solidly grow production, Crescent Point Energy Corp. ( CPG ) is a name to consider.

Company Profile

Crescent Point Energy Corp. is a liquids-focused E&P with operations in Alberta, Saskatchewan, British Columbia, and Manitoba in Canada, as well as the Bakken in the U.S. At the end of 2022, the company had 5,558 gross producing oil wells and 5,132 net wells. It also has 462 gross producing natural gas wells and 395 net wells.

The company is focused on four primary basins. In the Kaybob Duvernay, the company averaged 37,000 boe/d of gross production in 2022, of which 47% was condensate. The play is a combination of natural gas and NGLS, with about 59% of production NGLs. The play consists of about 32% of its total proved plus probable reserves at the end of 2022.

The company's second largest area of production is the Viewfield resource area located in southeastern Saskatchewan. This area includes the Bakken resource play, as well as conventional oil fields such as Frobisher and Midale. The company averaged 31,000 boe/d of production in the play in 2022, most of which is high-quality light oil. The basin consists of about 26% of its total proved plus probable reserves at the end of 2022.

In the Shaunavon resource area in southwest Saskatchewan, the company's production averaged approximately 19,000 boe/d. The play produces mostly medium quality oil. In the Bakken in North Dakota, meanwhile, CPG also saw production of 19,000 boe/d. The basin produces mostly high-quality light oil. The basins represent about 15% and 12% of its total proved plus probable reserves in 2022, respectively.

Recent Asset Transactions

In December, CPG announced it was acquiring additional Kaybob Duvernay assets from Paramount Resources (PRMRF) for C$375 million in cash. The deal included 30 net drilling locations and nearly 65,000 areas with a 90% average working interest with no expiries. The acreage currently has production of over 4,000 boe/d, of which 50% is liquids.

The acquisition also included a gas plant, associated pipelines, water infrastructure, and seismic data. The deal closed in early January.

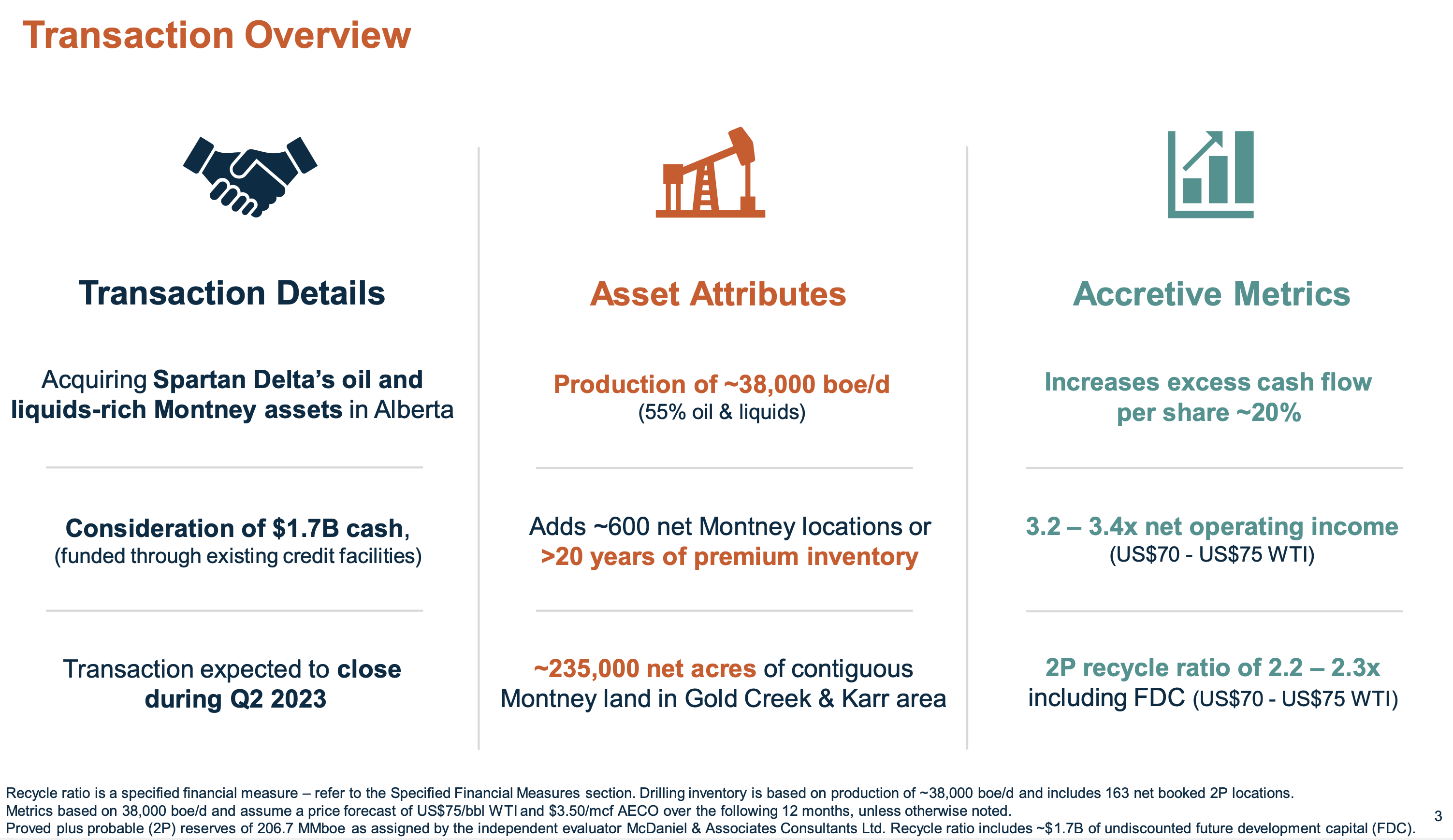

In March, the company announced it will buy oil and liquids-rich Montney assets in Alberta from Spartan Delta (DALXF) for C$1.7 billion. The deal includes 235,000 net acres of contiguous land with drilling inventory of 600 net Montney locations. The acquisition is expected to close in Q2.

The acreage is currently producing 38,000 boe/d, of which 55% is oil and liquids. The company said the acreage has low breakevens of US$40 oil. It is estimated that the deal was made at a 3.2-3.4x net operating income multiple base on US$70/bbl to US$75/bbl WTI and C$3.50/mcf AECO.

{kind=link}

In April 2021, the company first entered the Kaybob Duvernay, acquiring assets from Shell Canada for C$900 million. The acreage had 30,000 boe/d production at the time. Later that year, it sold some non-core assets in southeast Saskatchewan for C$90 million. That deal also allowed it to reduce its asset retirement obligations by approximately C$220 million.

Opportunities and Risks

Many E&Ps have focused more on their balance sheets and shareholder returns, while just looking towards modest production growth. That's not the case with CPG, which has been more aggressive in looking to grow production both organically and through acquisitions.

The company has really transformed its portfolio in the last few years, first with its original acquisition of Kaybob Duvernay acreage in 2021, followed by adding more acreage in the play at the start of this year. And now it is entering the Montney with its large recently announced acreage acquisition.

With no positions in either play entering 2021, the two basins are now expected to represent ~45% of CPG production this year, growing to ~60% of production in 2027. As a result of the Montney acreage acquisition, the company raised its full-year production guidance from 138-142 mboe/d to 160-166 mboe/d. It's looking to increase production to 195 mboe/d by 2027.

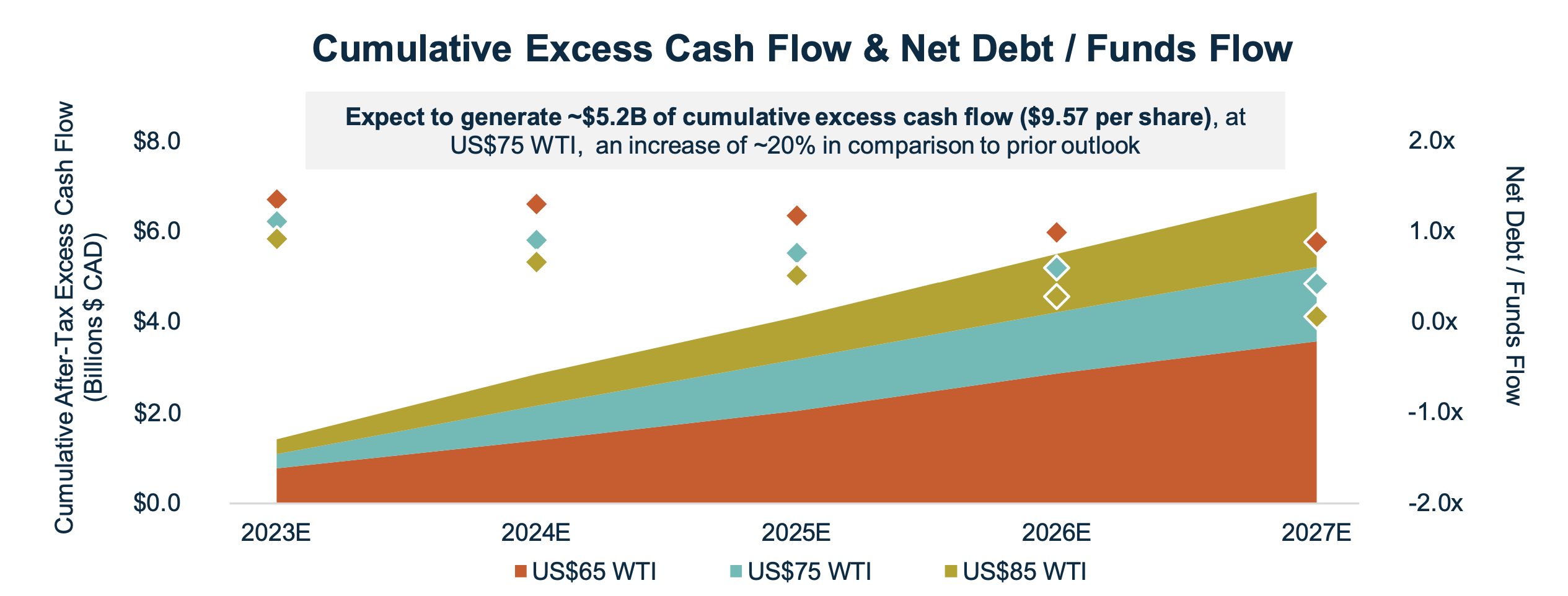

CPG will spend C$1.15-C$1.25 billion in CapEx this year, followed by C$1.25-C$1.35 billion in 2024 and thereafter. Given its U.S. $4.2 billion market cap, that's by no means a small amount. However, the company projects it can generate C$5.2 billion in cumulative excess cash flow over the next five years at U.S.$75 WTI. It says its CapEx program would be fully funded at U.S.$50 WTI, including paying out its dividend. (Note the current exchange rate is 1 CAD equals 0.75 USD.)

{kind=link}

CPG is going all in on the Kaybob Duvernay and Montney basins. It will have over 20 years of inventory in each basin, giving it a long runway. These are nice basins to be in with solid return characteristics, although it does add basin risk. The Kaybon Duvernay, in particular, has various production mix profiles from oil to more liquids, to lean gas, each with different return profiles.

Outside of these two Alberta basins, its Bakken North Dakota assets also have a strong growth profile. However, it's a smaller position for CPG in terms of inventory. Its Saskatchewan assets, meanwhile, are largely low-decline production assets at this point.

Following the Montney deal, CPG will have about C$3 billion in net debt, or about 1.3x leverage. 1.3x leverage isn't a lot, but that is in a strong energy price environment. Its market cap is only U.S.$4.2 billion, and leverage could quickly balloon if energy prices sink. The company is looking to reduce its net debt to C$2.0 billion by mid-2024. The debt load adds risk when many energy companies have been risk-averse.

The company typically hedges about 15-20% of its oil and gas production. Thus, energy prices will be a big driver of its results.

Valuation

Crescent Point Energy Corp. trades at 3.3x the 2023 EBITDA of $1.91 billion and 2.9x the 2024 EBITDA consensus of $2.21 billion. I've adjusted its enterprise value to take into account the Montney and Kaybob Duvernay acquisitions (and converting to USD).

On a PE basis, it trades at 7.3x EPS estimates of $1.06. Based on the 2024 consensus for EPS of $1.31, it trades at 5.9x.

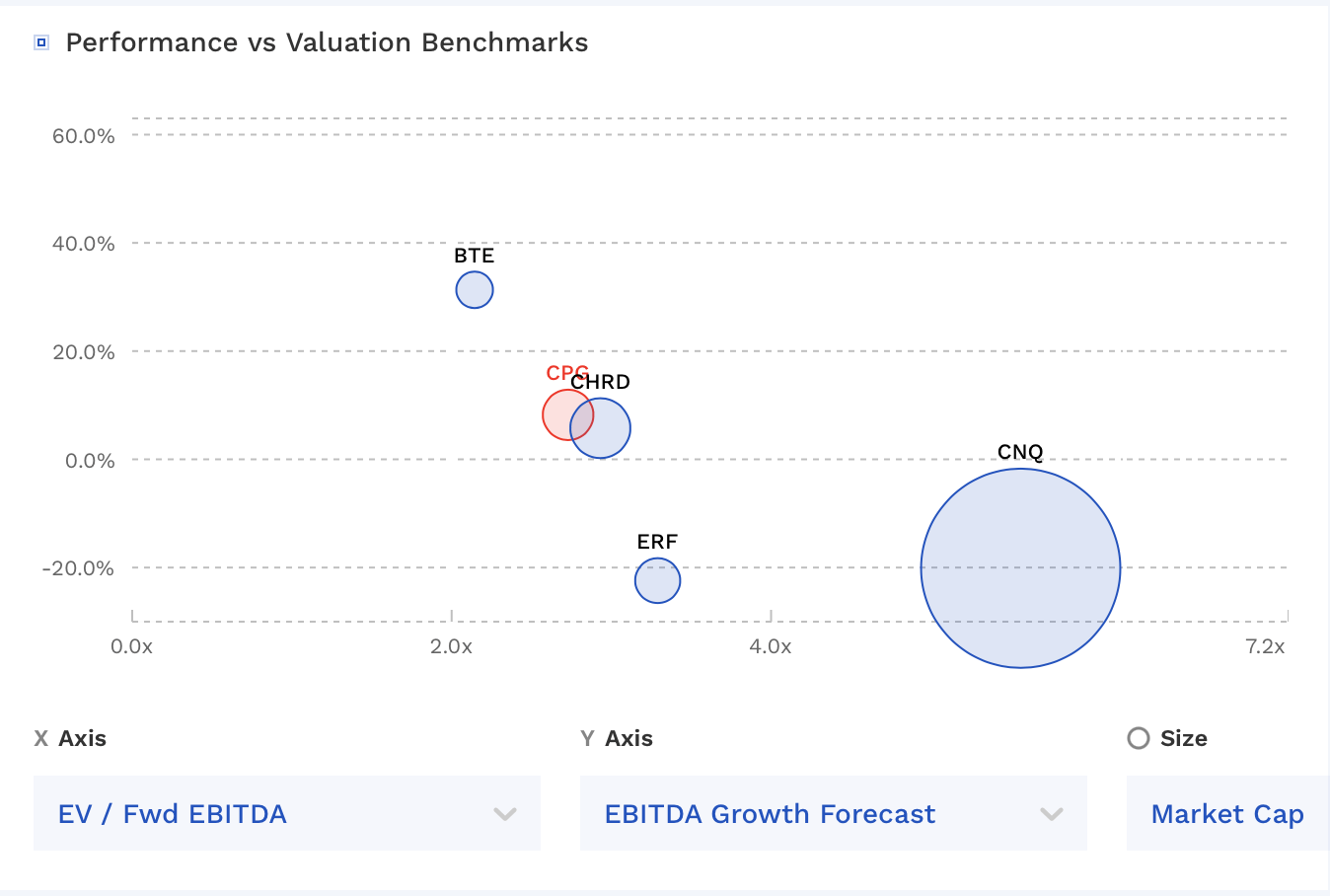

The stock trades towards the middle of other Canadian and Bakken liquids focused names.

CPG Valuation Vs Peers (FinBox)

{kind=link}

Conclusion

Crescent Point Energy Corp. has done a really good job of upgrading its asset base over the last couple of years. Before its foray into the Kaybob Duvernay and Montney basins, its assets were pretty lackluster. However, it was able to take advantage of a strong energy price environment and the cash generated by its more stable, low-decline assets to buy assets into two growth-oriented basins.

As a result, Crescent Point Energy Corp. is going to give you more production growth than many E&Ps. The downside is that this does come with more risk given the debt it is taking on to buy the Montney assets. If oil prices remain high, this isn't an issue, but it is a risk.

I'm generally bullish on oil, and I currently like the extra juice that Crescent Point Energy Corp. provides. As such, I'm going to rate the stock a "Buy." I see upside to $11+. At that price, the stock would keep almost the same forward multiple a year from now if it is able to reduce debt by the C$1 billion it is forecasting. This is getting to a market cap of US$6 billion ($11 stock * 547 million shares outstanding) plus a reduction to U.S.$1.5 billion in net debt divided by the US$2.2 billion 2024 consensus is a 3.4x multiple. Crescent Point Energy Corp. stock also has a nice 3.8% yield.

For further details see:

Crescent Point Deals Transform Company