CPG - Crescent Point Energy: A Low-Cost Liquids-Rich Oil Producer With Growth Potential

2023-09-05 04:43:14 ET

Summary

- Crescent Point Energy is a Canadian oil producer with a majority of its production coming from crude oil & condensate.

- The company recently completed a strategic acquisition of oil and liquids-rich Montney assets, increasing its leverage but providing growth potential.

- Crescent Point is expected to deleverage quickly and reach a net debt of around C$2B by the end of the year while still distributing cash flows to shareholders.

Investment Thesis

Crescent Point Energy ( CPG ) is a Canadian oil producer, that is listed on both New York Stock Exchange and Toronto Stock Exchange ( CPG:CA ), and it reports in Canadian Dollars.

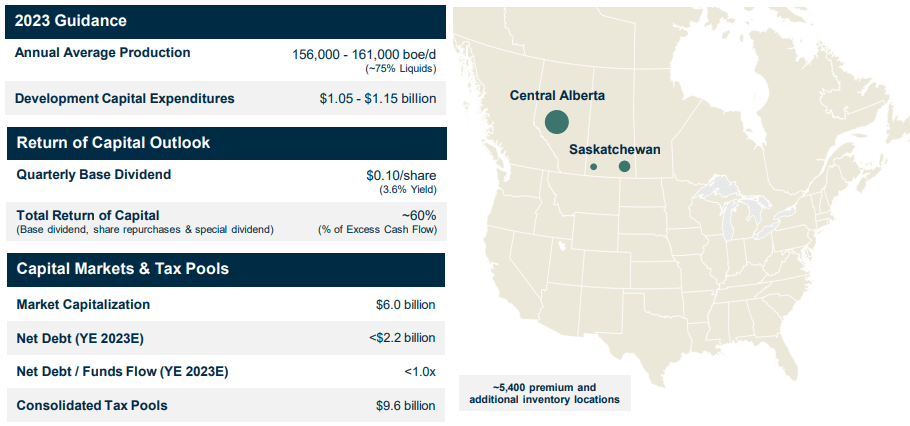

Figure 1 - Source: Crescent Point August Corporate Presentation

{kind=link}

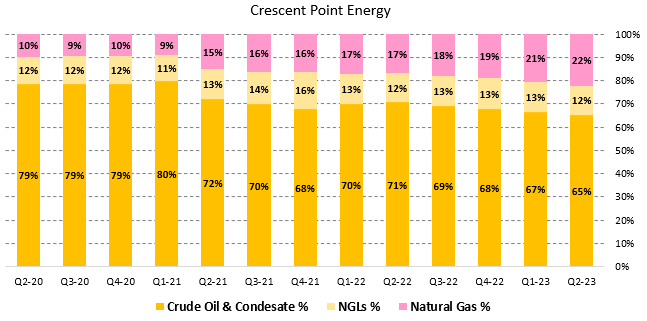

The company has some natural gas and NGLs production, but the majority of production is from crude oil & condensate. At current natural gas prices, an even larger percentage of revenues come from crude oil & condensate, it was 90% of total oil & gas sales during Q2-23.

Figure 2 - Source: Crescent Point Quarterly Reports

{kind=link}

While many oil & natural gas producers have focused on deleveraging and increasing shareholder returns, Crescent Point did earlier this year complete a C$1.7B strategic acquisition of oil and liquids-rich Montney assets. This acquisition has increased the leverage of the company, but it has been accretive to per-share metrics as the purchase was financed by debt. Apart from boosting production in 2023, the acquisition has also provided the company with excellent growth potential.

Select Financials

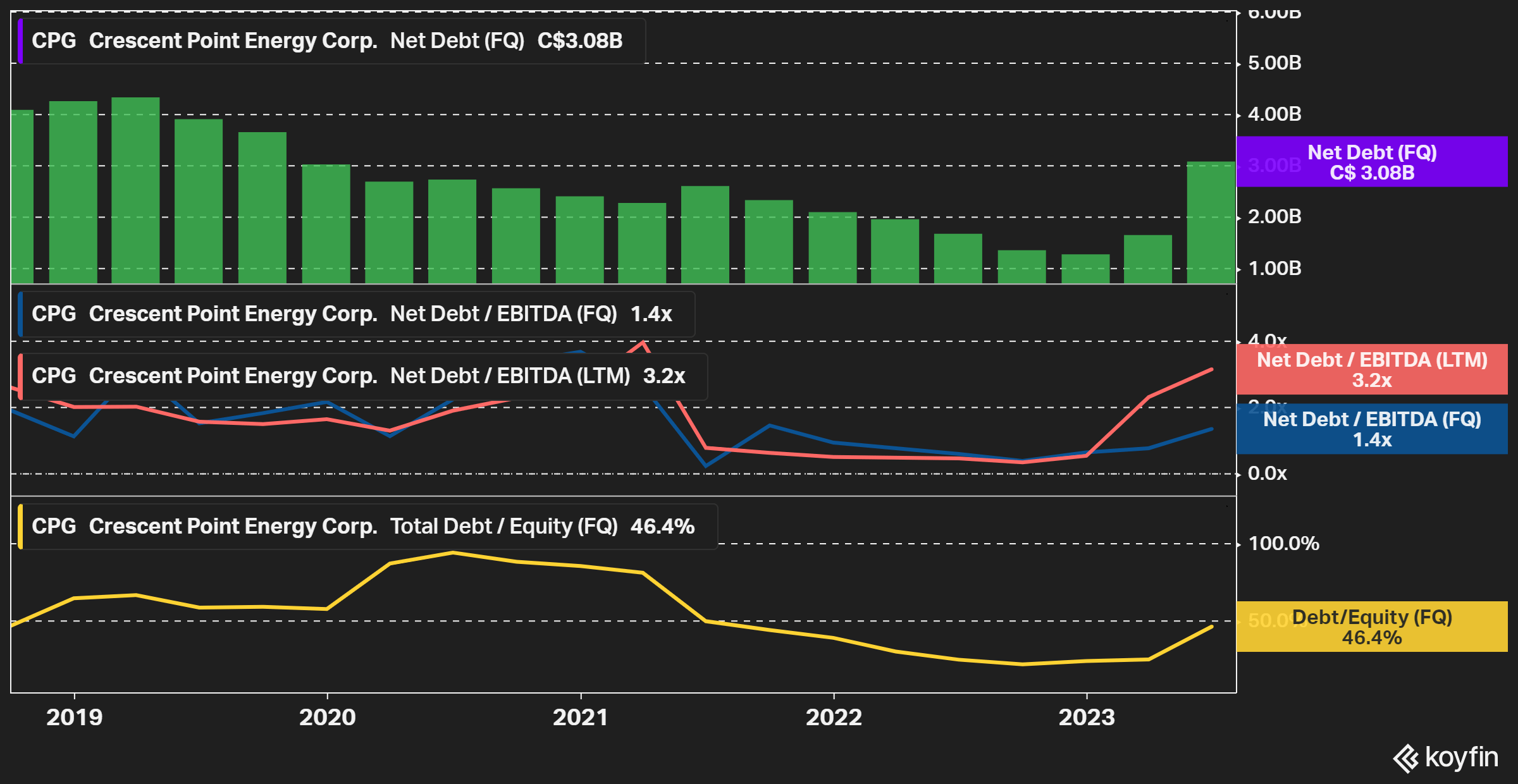

Crescent Point has spent the last few years decreasing the financial leverage up until 2023, where the net debt increased to around C$3B in the most recent quarter, and the debt-to-equity ratio was at 46%.

However, the company is now expected to deleverage relatively quickly and reach a net debt around C$2B by the end of this year. This will be achieved by relatively strong funds flow during H2-23 and the divestments of the assets in North Dakota, for about C$675M, that was announced in August. With that said, Crescent Point will by the end of this year still have slightly higher financial leverage than many other Canadian oil & natural gas producers.

{kind=link}

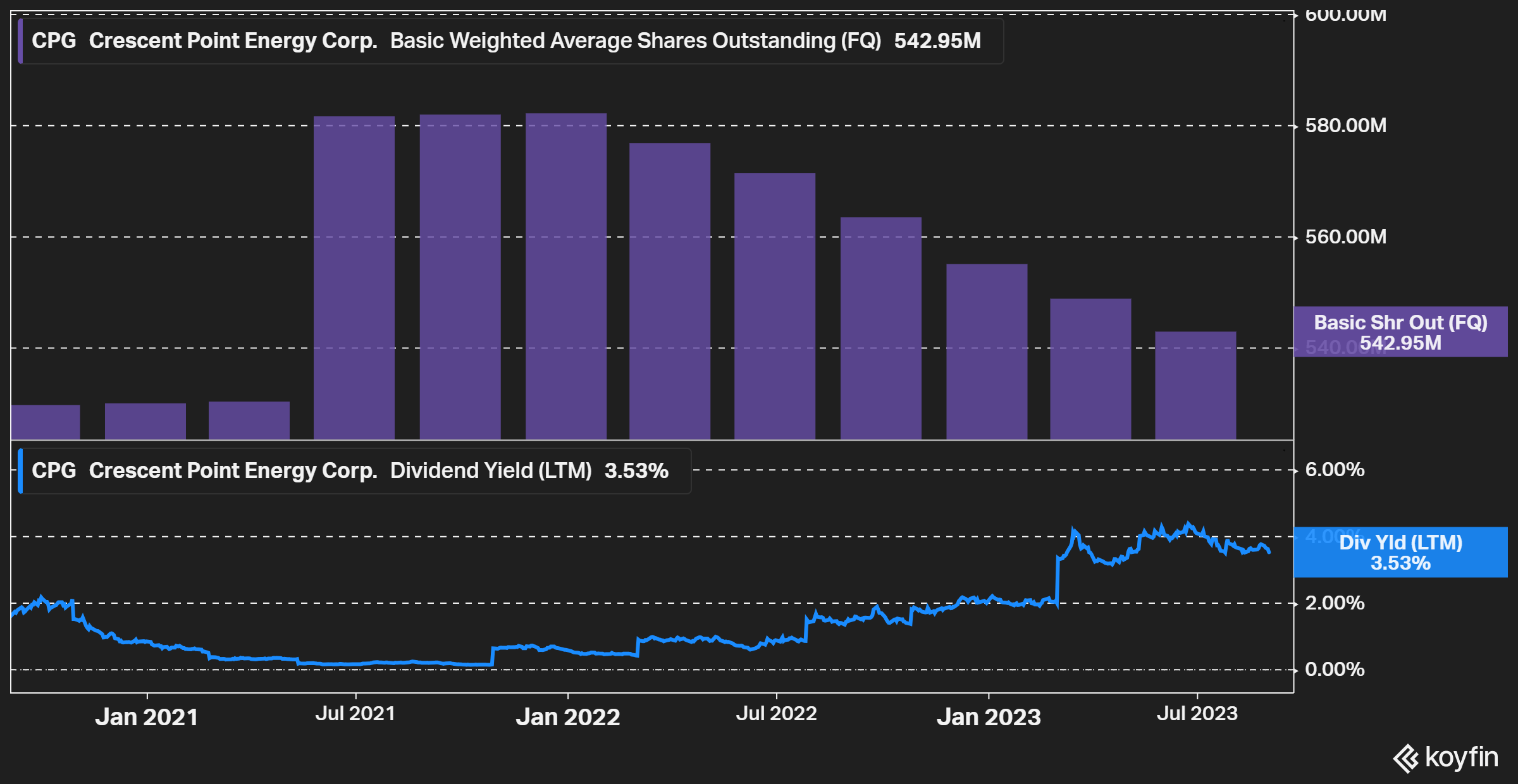

There is a strong focus on reducing the debt in 2023, but Crescent Point does still pay a regular quarterly dividend equal to a yield of about 3.5%. On top of that, we have seen some special dividends and relatively aggressive buybacks lately.

{kind=link}

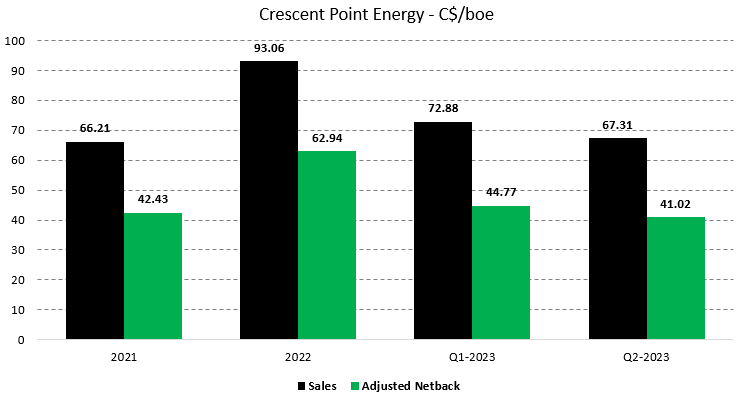

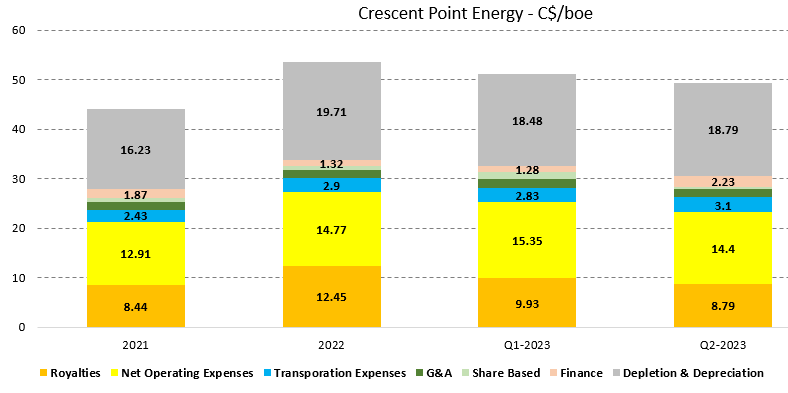

The ability to deleverage and distribute relatively large amounts of cash to shareholders is due to some very prospective assets, where the liquids rich production has generated healthy sales, while costs are very competitive. We have seen some cost inflation, but the overall impact has had a more minor impact on margins.

We can in the chart below see that the operating netback was as high as C$41/boe in Q2-23, which does not include around C$6/boe of hedging and FX gains, which boosted the margin even further.

Figure 5 - Source: Crescent Point Quarterly Reports Figure 6 - Source: Crescent Point Quarterly Reports

{kind=link}

{kind=link}

Valuation & Conclusion

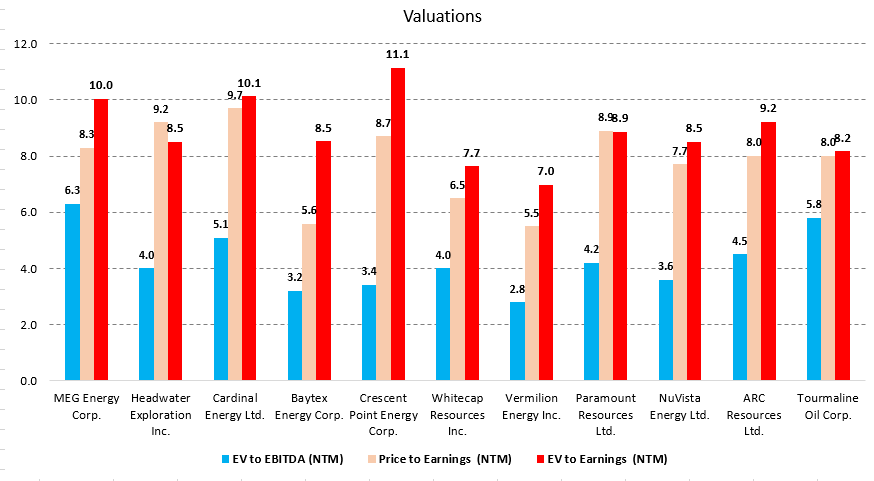

The below chart illustrates the valuation of Crescent Point and some other Canadian oil & natural gas producers, using broker estimates from Koyfin. Please note that I have adjusted the company's net debt figure to C$2B, which the company is likely to be around by year end.

{kind=link}

We can see that the near-term valuation is far from expensive, but Crescent Point is not the cheapest among the Canadian oil & natural gas producer either. Based on how the Crescent Point earnings estimates have progressed over time, it is fair to say the divestment of the assets in North Dakota has been taken into account. I do, however, think most brokers continue to be relatively conservative with their oil price assumptions for 2024, which makes the next twelve month estimates somewhat conservative, but that applies to all companies in the chart.

Crescent Point has a quality land package, which will allow the company to grow production over the next few years. We are also likely to continue to see solid excess cash flow, where the majority will be distributed to shareholders. So, I do think Crescent Point is likely to do reasonably well over the next few years.

Figure 8 - Source: Crescent Point Quarterly Reports

While several quality boxes are ticked with Crescent Point, I prefer companies with even less financial leverage and a lower valuation. So, I am neutral on the stock compared to peers today, even if I am relatively bullish on the overall industry. I would consider going long if we saw a 20% pullback in the stock price, which might be unlikely to materialize now that the sentiment looks to improve.

For further details see:

Crescent Point Energy: A Low-Cost Liquids-Rich Oil Producer With Growth Potential