AVDV - Crescent Point Energy: Extra Boost

- The acquisition of the condensate production exposure is a huge plus for profitability in the future.

- The acquisition should lead to above-average profitability gains throughout the business cycle.

- Lower debt levels also argue for an enterprise valuation increase.

- Cost reductions and an emphasis on cash flow at lower selling price levels signal an outperformance during the next downturn.

- This management has done a lot for the company over the last few years. That outperformance is likely to continue well into the future.

(Note: This article appeared in the newsletter on May 29, 2022, and has been updated as needed. This is a Canadian company listed on the NYSE and the TSX that reports in Canadian dollars unless otherwise noted.)

Crescent Point Energy Corp. ( CPG , CPG:CA ) is a Canadian company that also trades on the NYSE. That gives this company a little more exposure than is the case for many Canadian companies as well as access to the United States debt market. The company has projects on both sides of the border to minimize any adverse effects of currency exchange swings. It also has an acquisition that will likely continue to provide a positive earnings influence that is not available to many of its peers of a similar size.

Larger companies like Crescent Point do not generally appreciate as much as do smaller companies. The reason is that the established production base is much larger. Therefore, the logistics challenges of growing fast can be very formidable. Smaller brethren can often add a rig or sometimes half a rig and show tremendous growth from a smaller established production base. That is not an option for this company.

But an acquisition, if done correctly, often changes the profitability mix of the acquiring company for a few years to enable more per share growth than peers of a similar size. Such an acquisition can be enhanced by the periodic sale of higher cost production (and then plowing that money back into new lower cost wells).

Crescent Point management has spent the last few years materially changing the company. This is really the first business cycle where the results can be seen. As those results become apparent, Mr. Market may look at the company in a far more positive light than has been the case in the past. In fact, at some point, the company could be acquired now that it is in far better shape than was the case a few years back.

Cost Reduction Effect

A lot of companies during a boom often talk about cost reductions. They then scramble to reduce costs a lot more during the next cyclical downturn.

(Canadian Dollars Unless Otherwise Noted)

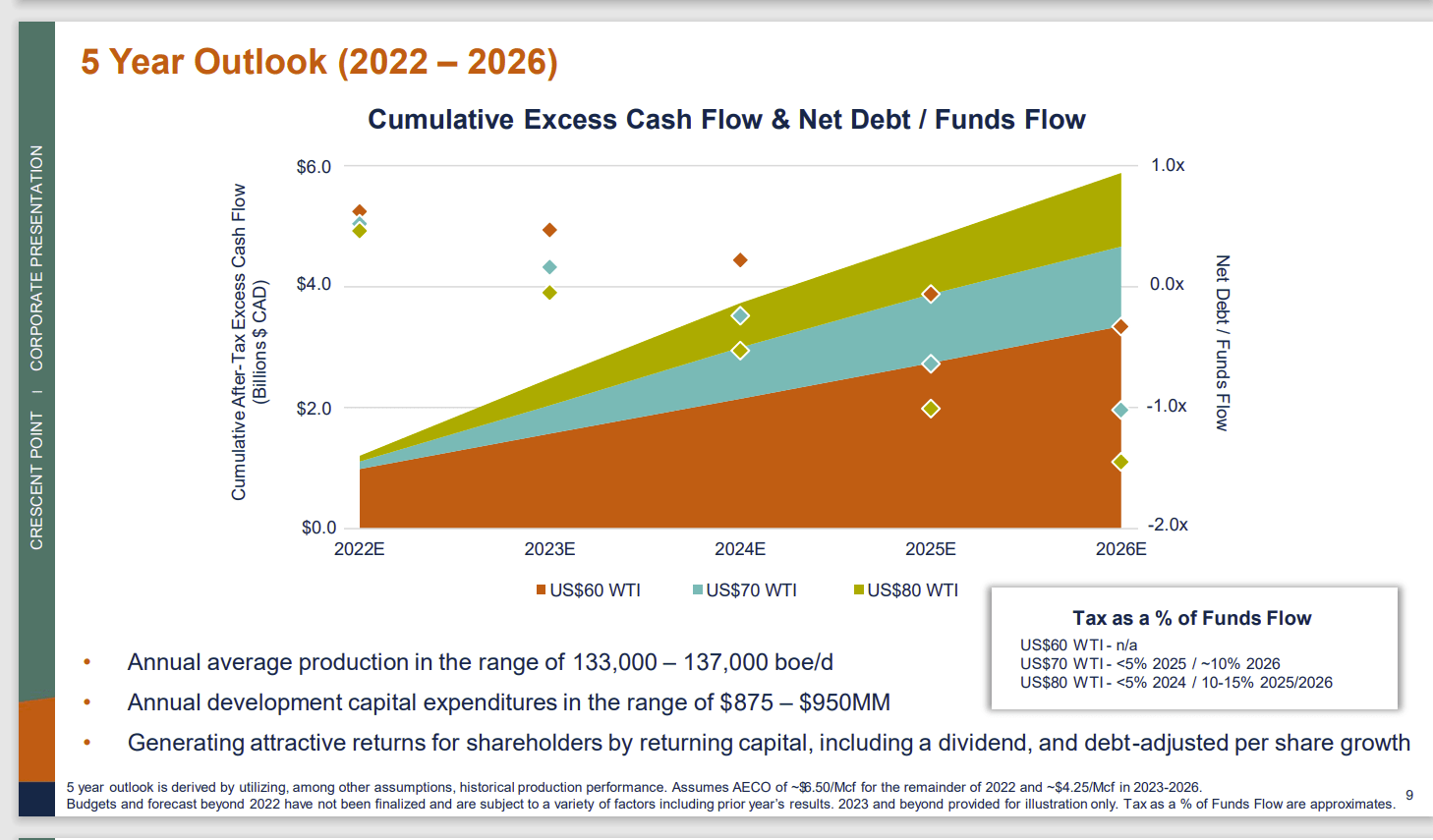

Crescent Point Energy Excess Cash Flow At Far Lower Selling Prices (Crescent Point Energy First Quarter 2022, Earnings Conference Call Slides)

{kind=link}

Management has kept the focus on extra cash flow at considerably lower prices. There is additional cost reduction progress in the form of continuing technology advances throughout the industry. The near term was updated with the second quarter report. In the meantime, the slide above remains unchanged (and for good reason as this industry is very volatile).

Management has an advantage in the form of some competitive secondary recovery prospects that have very low production decline profiles to lower the company average production decline each year. This means that there is less maintenance capital needed to maintain production than is the case with competitors that are strictly unconventional.

Furthermore, a selling price environment like the current one provides a fairly quick (if unexpected) payback of the sizable costs needed to begin secondary recovery in the first place. That means this company goes into the next cyclical downturn with the initial secondary costs paid back (regardless of what the accounting reports). The only thing that can happen is too many profits were stated during the boom times. Such an event would be corrected with an impairment charge at the industry cyclical bottom. What would remain unaffected is the early payback of expensive secondary recovery project costs.

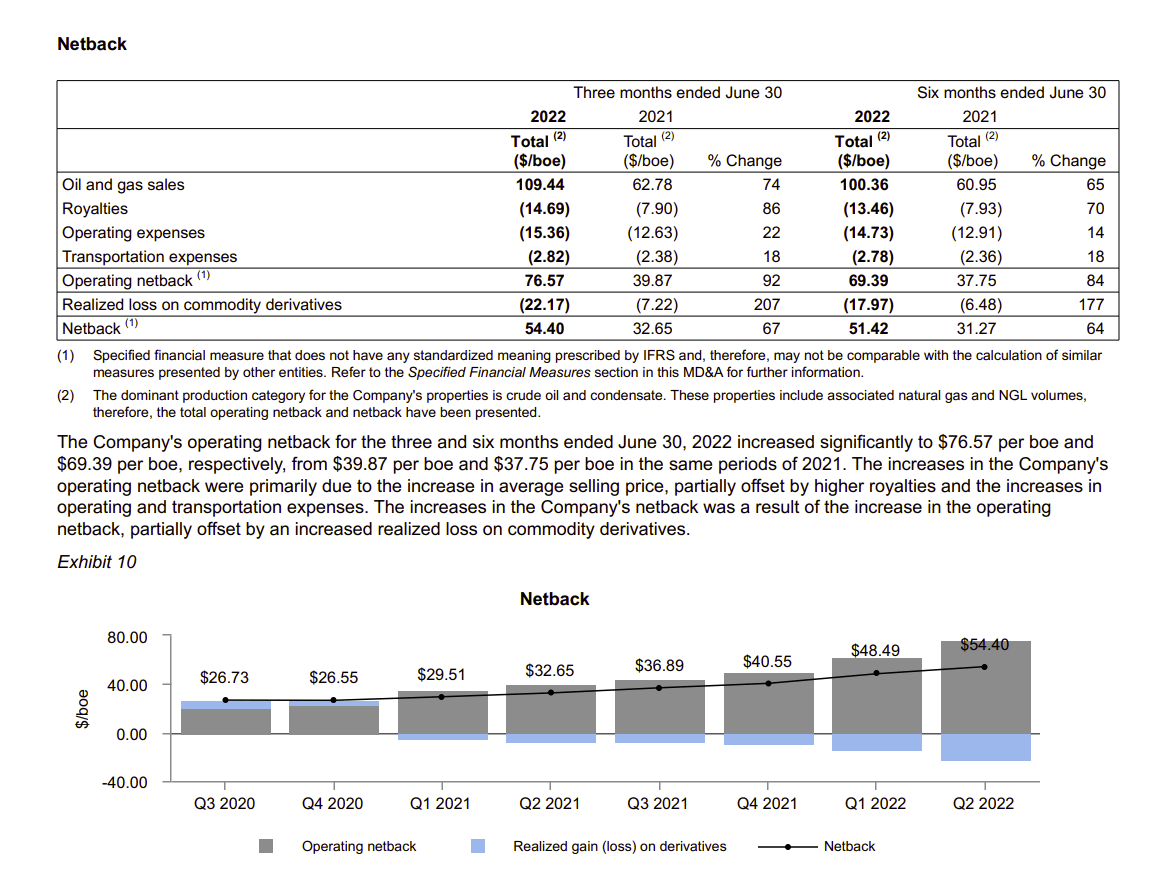

Netback Is Not Everything

So many companies focus on netback. Netback is definitely worth looking at, so here it is:

Crescent Point Energy Operating Netback History (Crescent Point Energy Management Discussion And Analysis)

{kind=link}

Crescent Point Energy is in the same position as many competitors to report increasingly favorable netbacks. The high oil percentage of production allows an almost "guaranteed improvement" although the recent price increases of other products certainly "help the cause along."

What is left out of the discussion is that there needs to be enough production at that wonderful netback to enable a decent return on investment and return on capital. There is a lot of unconventional and secondary recovery companies with wonderful netbacks both historically and currently that do not have enough production to produce a viable amount of cash flow and profits.

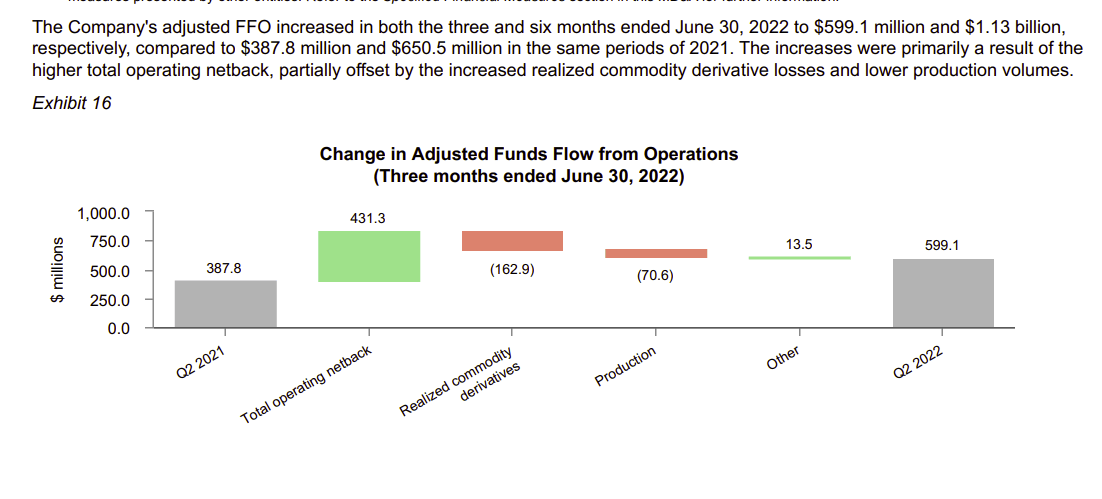

Crescent Point Energy Second Quarter 2022, Change In Adjusted Funds Flow (Crescent Point Energy Second Quarter 2022, Management Discussion And Analysis)

{kind=link}

That makes the change in cash flow real important. Every single company in the industry will benefit from rising commodity prices. The hedging program is currently also diminishing results. But the important part to watch is the increasing profitability due to production (and selling price changes). That change as well as the continuing speed of that change will likely determine the company performance during the next downturn.

Management has decreased the debt ratio to cash flow to 1.0. This management has been digging the company from a debt hole for some years. Therefore, that debt ratio is likely to go a lot lower so that it remains conservative at considerably lower prices.

So many do not realize that the market determines profitability of cyclical companies by their performance throughout the business cycle. Therefore, companies that produce heavy oil, for example, have a lower valuation in the current cycle despite often more profitable earnings because heavy oil is a discounted product. Losses are far worse when the discount often expands during a cyclical downturn to produce an overall lower level of profitability than is the case with light oil.

A large company like this has a fairly diversified amount of production with an emphasis on light oil and condensate. Therefore, the market is likely to look favorably upon continuing profit improvements as the cycle progresses. That kind of revaluation is going to be favorable for long term shareholders.

The Future

The continuing cash flow is likely to result in more returns to shareholders through higher dividends and share repurchases. Management increased the second quarter dividend. They also wisely initiated a share repurchase program that can be discontinued or suspended during times of weak commodity prices. As the debt gets paid down, less money will be needed for that purpose to automatically increase the amount available to return to shareholders.

Many companies in this industry are keeping dividends at a low percentage of cash flow so that the dividend can be maintained during the next inevitable cyclical downturn. These downturns will happen a lot faster (meaning they will not last long) because production declines quickly in the unconventional business that now dominates the industry. That is good news for an industry that has managed to surmount several challenging downturns.

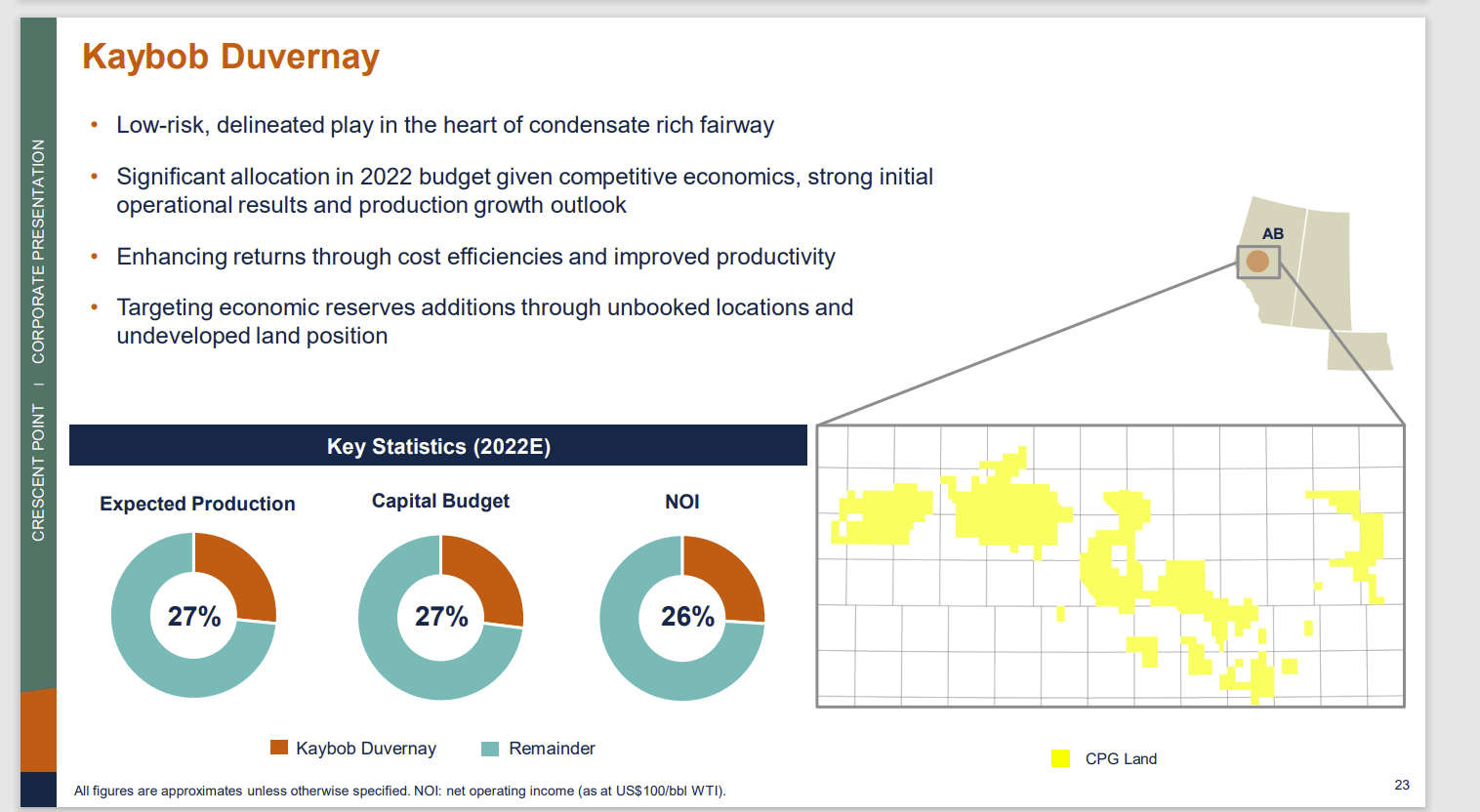

Kaybob Duvernay Acquisition Benefits (Crescent Point Energy Second Quarter 2022, Earnings Conference Call Slides)

{kind=link}

The acquisition provided significant exposure to the premium condensate market that exists in Canada. Naturally the company will spend "first call" capital money on the highest margin area. That turns out to be the acquisition. A large acquisition often takes a few years to optimize. That appears to be the case with this acquisition. In the meantime, high commodity prices will provide the necessary cash flow to optimize this acquisition faster than was expected to be the case.

This management team has accomplished a lot in the time it has been in control of the company. The result will be a far different company moving forward than was the debt laden company of years past. Not many companies can deleverage successfully in this industry. This is one of the few. That points to a far above average management.

Further indications of future outperformance come from the emphasis of cash flow at much lower commodity prices and a focus on the debt ratio at those lower prices. The result is a very valuable company going forward with a stock price that is likely to match.

For further details see:

Crescent Point Energy: Extra Boost